Fixed assets are a company’s relatively durable tangible assets used to carry out operations and generate income. So, they do not consume or sell it but produce goods or services. Due to their long-term use, the value of fixed assets decreases as they age. Some examples of depreciable fixed assets are buildings, machinery, and office equipment.

However, land is not one of them, because it has an unlimited useful life and it increases in value over time. In short, depreciation is the allocation of fixed asset acquisition costs that have a decrease in value.

With the right Accounting system, you can run your business more efficiently and accurately, especially with the most complete Accounting software in Singapore. Thus, to find out what factors affect the depreciation of fixed assets and how to calculate them, see the explanation below.

Key Takeaways

|

The Causes of Depreciation

In general, there are two main causes of depreciation:

Physical Factor

The value of a company’s assets can shrink due to overuse, aging, and damage.

Functional Factor

The cause of asset depreciation can also be the inability of assets to meet production needs, so there needs to be a change with new ones.

Also read: Fixed Asset Definition | Examples, Journal Entries & Acquisition Methods

Factors That Affect the Depreciation Expenses

Acquisition Cost

This is the most influential factor in calculating depreciation expense in financial reporting. In addition, the acquisition cost refers to the total cost of buying an asset. Thus, it becomes the basis for calculating the depreciation that should be allocated for every accounting period.

The acquisition cost includes shipping, sales, and customs duty, as well as site preparation, installation, and testing fees. In addition, About manufacturing or production equipment, any costs related to bringing the equipment to an operational state may also be included in the acquisition cost.

This includes the cost of shipping & receiving (logistic management), general installation, mounting, and calibration.

Salvage Value

The salvage value is the amount for which the asset can be sold at the end of its useful life. To determine the total amount depreciated, the salvage value must be subtracted from its initial cost.

For example, company A buys an asset worth 100,000,000 and they estimate that the salvage value will be 20,000,000 in five years. That means, they will depreciate 80,000,000 of the total cost of the asset and may expect to sell it for 20,000,000.

Economic Life

The economic life of an asset is the expected period as long as the asset remains useful to the owner. It can differ from its actual age. Business owners need to estimate the economic life of their assets, so they can determine when the right time to invest in or allocate funds for new assets.

If you are already interested in the best-fixed asset management software, you can start trying the price calculation offered by HashMicro by clicking the image below.

How to Calculate Depreciation on Fixed Assets

There are several methods that you can implement to calculate depreciation on your fixed assets. Here are the five general methods:

Straight-Line Depreciation Method

According to the straight-line method, the depreciation value of a fixed asset will always be stable until the end of its economic life.

For example, if you buy a production machine for 50,000,000, the depreciable amount is 5,000,000, and the estimated economic life is 5 years, then the calculation is as follows:

Depreciation expense = (50,000,000 – 5,000,000)/5

Depreciation expense = 9

Double Declining Balance Method

The double-declining balance method is a type of purposeful depreciation used by fast-moving businesses. According to this method, most of the depreciation related to fixed assets is applied during the first few years of the business’s economic existence.

Multiply the asset’s book value as it stood at the beginning of the financial year by a multiple of the straight-line depreciation rate to arrive at the amount of depreciation that should be taken into account. The formula can be broken down as follows:

Amount of Depreciation Digit Year

A form of accelerated depreciation known as year-digit depreciation is founded on the presumption that the productivity of an asset will decrease over time.

This strategy aims to charge a higher depreciation cost in the early years of an asset’s economic life because it is most productive in the early years of its use. The formula can be broken down as follows:

Depreciation expense per year = ACCESSIBLE WORKING HOURS X hourly depreciation rate

Service Unit Method

The depreciation of company automobiles can benefit significantly from using this strategy. When calculating depreciation using this method, an asset’s useful life is considered.

Depreciation is calculated using this method by dividing the total net cost of the asset by the expected useful life. For example, the total number of miles traveled by a car can be used to calculate its useful life.

Also read: 3 Benefits of School Asset Tracking Software

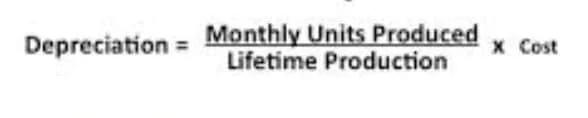

Production Unit Method

Depreciation is computed based on the actual utilization of the asset when using the units of production technique. The amount of money spent on depreciating a fixed asset is calculated using this approach, which counts the number of individual products that have been manufactured.

The formula can be broken down as follows:

Instant Way to Calculate Depreciation of Your Fixed Assets

Depreciation of fixed assets must be calculated to account for the wear and tear of business assets over time. Since depreciation is a non-cash expense, the amount must be estimated. Each year, a certain amount of depreciation is written off, and the asset’s book value is reduced.

Not only does HashMicro assist your business in calculating asset depreciation accurately, but it also offers an advanced Asset Management Software to effectively manage all your company’s assets. This comprehensive solution ensures real-time tracking, automated maintenance scheduling, and detailed reporting, helping you optimize asset utilization while minimizing risks and costs.

By integrating HashMicro’s Asset Management Software into your operations, you can enhance efficiency, reduce downtime, and ensure compliance with regulatory standards. Streamline your asset management process today and empower your business to make data-driven decisions with ease.

Read more: 8 Best Fixed Asset Management Software in Singapore 2025

Conclusion

Accounting software by HashMicro helps automate your depreciation calculations. This accounting software allows you to record and manage your asset list easily. It can also generate reports for asset evaluation in seconds.

For more information about the accounting system from HashMicro, please visit our website or discuss it directly with our software experts. After you have determined the pricing structure of the ERP software, you can then select the appropriate ERP vendor.

Give us some information about your line of work and we will provide the most effective business alternatives for you to consider. If you want to get a free demo of our touring product, click here!