There are several stages in the accounting process, and one of these stages is compiling trial balances. The old accounting arrangement led to the emergence of a system called the Accounting Management System which aims to facilitate accounting processes such as making a trial balance.

Without compiling it, the ongoing accounting process will become incomplete. A company can obtain various benefits in compiling this. One of them is knowing the balance of the debit and credit amount. Check out this article to find out more about this process in accounting!

The Definition of Trial Balance

A trial balance is a working paper in the form of a balance list that contains account names and balances on the general ledger. This is used to determine the suitability of the amount of the debit column and the credit column at the end of the accounting period.

Some experts from Indonesia expressed their opinions about the definition of this term. For example, Effendi said that trial balance is an accounts list in the company or business entity’s general ledger in a certain period. Meanwhile, Soemarso said that it is a list of account balances in the company’s general ledger in a certain period.

The Functions of Trial Balance

It has several functions. Here are the 4 functions of trial balance:

- Check for errors that can occur when posting financial transactions.

- Helping with the preparation of financial statements.

- Supervision of the used company accounts.

- Recording business financial transaction data according to the account.

The Benefits of Trial Balance

As one of the stages in the accounting process, it has several benefits for the company. Here are the benefits of trial balance :

- The checking process will run smoothly.

- The posting process will be easy.

- Assessment material on the company’s credibility.

Several Steps in Compiling Trial Balance

There are several steps in compiling trial balance. To begin with, you must calculate the balance of each account on the general ledger. Next, if this step passes, you should write the account names of the assets, debts, capital, income, and expenses elements according to the general ledger in the “Account Name” column.

Furthermore, do not forget to write each balance contained in the general ledger to the working sheet according to the account name. No less important, make sure that you calculate the total debit and credit columns and match them.

Accumulated depreciation in trial balance increases until it nears the original cost of the asset, at which point, the depreciation expense account is closed out.

Types of Trial Balance

There are several types of trial balances. Here is the explanation of each type:

Unadjusted

This type can be said as a balance list compiled after the entire transaction has been posted to the general ledger. The account balance in the general ledger will be moved to the balance list. This type will determine if there are any errors when posting debits and credits into the general ledger.

In addition, a balance list that has not been adjusted will make it easier for you to detect errors that occur. With this, you can immediately make improvements to the error.

Speaking of how to create it, this type can be done by posting transactions on the general ledger. When all successful transactions are posted on the general ledger, the next step is preparing the unadjusted balance list.

Adjusted

This type is a balance list that is compiled after the adjustment process on certain accounts is complete. Adjustments must be made because some accounts must be adjusted first before compiling the financial statements—examples of these accounts such as account balances for unearned expenses and unearned revenue.

In compiling this type, moving the account balance into an adjustment journal becomes the first step. When the adjusting entries have been posted, the next step is to create an adjusted account balance.

Post-closing

This type is a balance list that ensures the general ledger already has a balance for the next first period. This procedure is the last step taken in the one accounting period after being inputted into the closing entries.

Talking about how to compile this type, closing the book is the first step. This is because, previously, some accounts moved to the general ledger. Later on, the data on the general ledger will be the same as the data reported in the financial statements. Account balances reported on the trial balance are permanent, while data on income statements only report the amounts for one period.

In reporting the amount of one period, the account balance at the beginning of the period must be 0 (zero). To make the balance 0 (zero), the closing entries can be used balance of expenses and income. Keep in mind that using general ledger software is a great way of automating some of these tasks and ensuring your financials are on point.

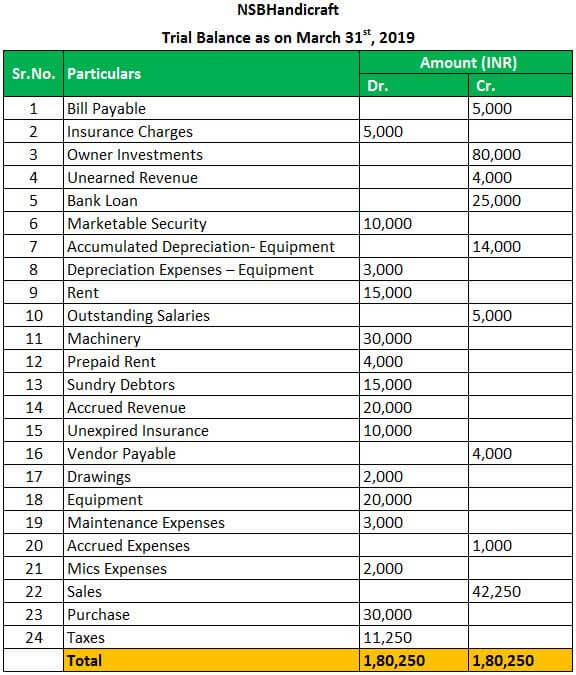

Example

To make you better understand this here is an example of it:

Conclusion

It is important to compile financial statements. Without doing so, a company cannot determine the accuracy or suitability of the debit and credit column totals at the end of the accounting period. Compiling a trial balance offers various benefits, one of which is simplifying the posting process. This process becomes even more efficient when using the best ERP software, which automates data entry, ensures real-time accuracy, and streamlines financial reporting.

HashMicro as a leading ERP Software vendor in Singapore provides solutions for your company in operating business automatically, such as an Accounting System to a Competency Management System.

While optimizing your business’ finances using the Accounting System, the Competency Management System can help you monitor your employees’ work performance, which can even help you better optimize your business growth.