Managing a cost structure means breaking down every expense to maintain efficiency and profitability. From my experience, using the best accounting software with ERP integration is the smartest way to optimize costs, refine pricing, and strengthen financial control.

With HashMicro, I can automate expense tracking, analyze costs in detail, and allocate resources accurately across departments. It’s a powerful tool that helps ensure long-term success. Want to experience it yourself?

Try our free demo today and see how it can transform your financial operations!

Key Takeaways

|

What is Cost Structure?

Cost structure definition refers to the composition of a business’s expenses, outlining how costs are distributed between fixed costs and variable costs. Understanding this cost structure analysis allows businesses to analyze their spending patterns, set strategic pricing, and improve profitability. On top of that, it makes budgeting and forecasting way more accurate, so teams can plan smarter, avoid surprises, and focus their resources where they matter most.

In addition, a well-defined product cost structure allows businesses to identify cost-saving opportunities and enhance operational efficiency. By regularly reviewing and optimizing their cost components, companies can reduce waste, improve production processes, and maintain a competitive edge in the market. This proactive approach ensures long-term sustainability and adaptability in an ever-changing business environment.

Hashy AI Fact

Need to Know

Hashy AI instantly accesses accurate financial reports and business insights, helping to make more precise decisions. Hashy AI Finance helps you figure out an accurate forecast of your income and expenditure over a specified future period of time.

Request a free demo today!

Types of Cost Structure

Businesses generally adopt two primary cost structures: cost-driven and value-driven, each with its own approach to managing pricing and value.

1. Cost-Driven

Cost-driven businesses focus on providing low-cost products and services, prioritizing affordability for customers. To achieve this, they implement various cost-cutting strategies and optimize processes to maintain the lowest possible costs.

Their goal is to offer competitive pricing while still making a profit, often by finding savings that competitors may overlook. Examples of cost-driven companies include budget airlines, discount retailers, and service providers that offer lower prices than their competitors.

2. Value-Driven

Value-driven businesses, on the other hand, aim to deliver exceptional value to their customers. While their products or services may not always be the cheapest, they focus on providing the best possible experience or quality for the price.

Pricing is competitive, but the core value proposition is centered around superior quality or service. Examples include premium airlines, luxury retailers, and highly skilled service providers who focus on delivering greater value rather than the lowest price.

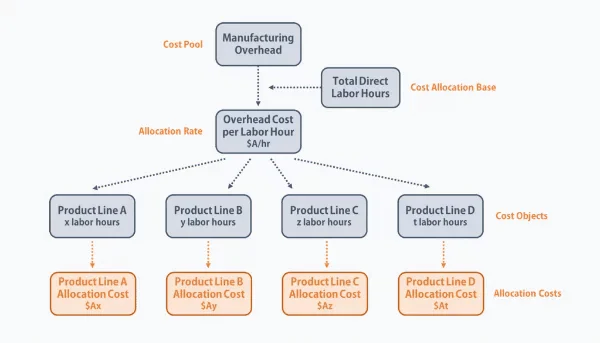

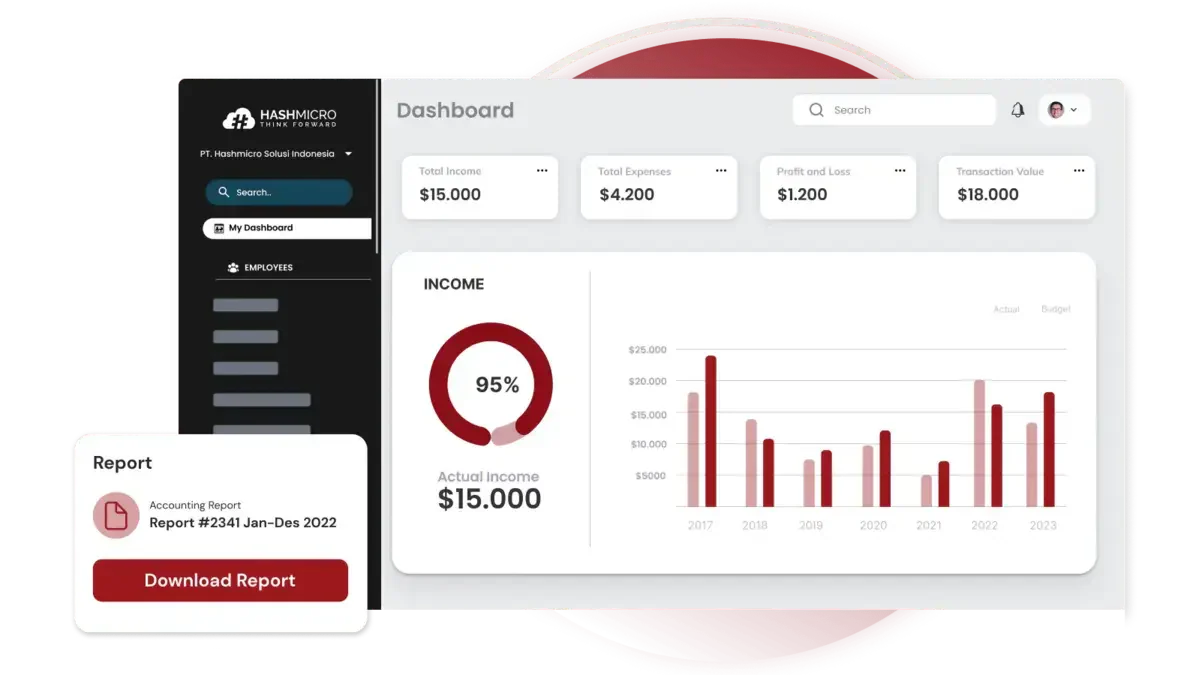

Understanding a company’s cost structure analysis is crucial for managing expenses and maximizing profitability. It involves categorizing costs into fixed, variable, and semi-variable components, each playing a role in overall business efficiency. The following are some examples of production expenditure structure elements: The business’s product cost structure is fundamental, especially for the finance division. Generally, it helps define how expenses are distributed across different types of costs—primarily fixed costs and variable costs—which are essential for pricing, profitability, and financial planning. Given that this is related to the business’s financial health, then it should be that every company should be able to make a cost structure. By utilizing an expenditure structure, the company will be able to control various divisions and make efficient spending efforts in the future. After discussing the product cost structure of a business, you now have a basic understanding of financing and its various forms. Arrange and choose the rules for multiple activities intelligently and carefully. Budget management can help your business become more efficient and reduce the risk of loss. The basic formula for a company’s cost structure can be expressed as: Total Costs = Fixed Costs + Variable Costs Where: For more detailed analysis, businesses often break down costs further: Total Costs = Fixed Costs + (Variable Cost per Unit × Quantity Produced) This formula helps businesses understand how total costs increase with production and sales, guiding decisions on pricing, profitability, and resource allocation. With the collection of costs, the production overhead cost uses direct working hours to calculate cost allocation. At first, the business will undoubtedly accumulate the company’s overhead costs over time. For a cost structure analysis example, in one year, the total overhead costs are divided by the total hours worked to determine overhead costs, i.e., cost per hour or allocation rate. Thus, the business will double the hourly cost by the number of hours worked in producing the product to arrive at a specific overhead cost. To maximize profits, businesses must explore every opportunity to reduce costs. While certain fixed costs are necessary for operations, financial analysts should regularly review financial statements to pinpoint any excessive expenses that do not contribute to core business functions. By understanding a company’s overall cost structure, analysts can identify cost-cutting opportunities that don’t compromise product quality or customer service. They must also monitor cost trends to ensure consistent cash flows and prevent sudden cost increases. Cost management also plays a crucial role in decision-making. If costs are not allocated correctly, businesses may make poor decisions, such as mispricing products or investing in non-profitable areas. This process enables analysts to determine the per-unit costs for various product lines, departments, or business units. With this data, financial analysts can provide recommendations for improving product profitability and eliminating low-margin products. HashMicro’s online accounting software provides a robust solution for streamlining cost structure, crucial for any business in Singapore looking to optimize its financial performance. By integrating advanced features such as real-time reporting and automated expense tracking, this system ensures that businesses can maintain accurate and up-to-date records of all financial transactions. This visibility allows for immediate identification of financial trends and cost-saving opportunities. Moreover, HashMicro’s system simplifies the complex processes involved in financial management. It automates the categorization of fixed and variable costs, making it easier to track expenses against budgets. This precision not only aids in better resource allocation but also enhances the accuracy of financial forecasting. The software’s capacity to integrate with other business systems, like CRM and ERP, further streamlines operations by providing a unified view of the company’s finances and operations. Additionally, the system supports detailed cost analysis and allocation, crucial for businesses with multiple departments or product lines. By accurately assigning costs to specific projects or departments, HashMicro’s accounting software enables businesses to pinpoint exactly where efficiencies or adjustments are needed. This targeted approach helps in effectively managing and reducing unnecessary expenditures, leading to a more streamlined cost structure and improved overall financial health. “Cost structure is the blueprint of how a business spends money to operate and grow, breaking down fixed vs. variable costs so leaders can price smarter, protect margins, and make faster decisions when demand shifts.” — Angela Tan, Regional Manager The financial statements should show whether there is a possibility of high costs and whether the economic activity is making a profit. With a clear cost structure definition, you can classify fixed and variable expenses more accurately to spot inefficiencies early. To support these processes, businesses need tools that can provide accurate financial insights and streamline their daily accounting operations. Automate cash flow management, financial statement generation, bank reconciliation, adjustment journals, invoice creation, and more with our accounting software. If you’re a large enterprise, HashMicro’s accounting software is tailored to scale alongside your business. Our budget management feature efficiently handles budget management tasks and establishes approval matrices based on available budgets. Click here to explore our free demo and 70% funding from the CTC grant today!

What are the Cost Structure Components?

Cost Structure Component

Explanation

Examples

Fixed Costs

Costs that stay the same regardless of production volume.

Rent, salaries, insurance premiums

Variable Costs

Costs that change in direct proportion to production or sales.

Raw materials, production labor, shipping fees

Semi-Variable Costs

Costs with a fixed base but that increase as usage/volume rises.

Utilities with a base rate and usage charges

Direct Costs

Costs directly linked to producing a product or delivering a service.

Raw materials, direct labor

Indirect Costs

Operational costs that support the business but aren’t tied to one product/service.

Admin expenses, marketing, shared utilities

Marginal Costs

The additional cost of producing one extra unit.

Extra materials and labor for one more unit, calculated as the cost per unit of one additional unit.

Contribution Margin

Revenue left after subtracting variable costs; used to cover fixed costs and profit.

Sales revenue minus variable costs

Allocating costs

Process of assigning costs to specific cost objects for better accuracy.

Allocating overhead to projects, departments, and products

Cost Pool

A grouped set of similar indirect costs makes allocation easier.

Overhead pools like rent, utilities, shared salaries

Elements of Cost Structure

Customer Cost Structure

Product Cost Structure

Service Cost Structure

The Cost Structure of the Product Line

Cost Structure-Function for the Company

Cost Structure Formula

Examples of Cost Structure

The Importance of Cost Structures and Cost Allocation

Streamline Your Cost Structure with HashMicro’s Accounting Software

Conclusion

FAQ About Cost Structure

What is a cost structure example?

Fixed costs typically include expenses like amortization, taxes, employee salaries and benefits, interest, rent, insurance, repairs and maintenance, and IT. Variable costs commonly cover transportation, utilities, parts, raw materials, and licensing fees.What are the 4 types of costs?

There are four common cost categories used in cost accounting: fixed costs, variable costs, direct costs, and indirect costs.How to calculate cost structure?

A basic way to calculate the cost structure is to sum fixed and variable costs to get total costs: FC + VC = TC. Fixed costs remain the same even when production is low or zero, while variable costs rise and fall depending on output.