Bad debts are an expense that a business incurs once the repayment of credit previously extended to a customer is estimated to be uncollectible and is thus recorded as a charge-off. Companies do business by selling products whose purpose is to make a profit.

However, with the existence of receivables, the situation is reversed. The company gets terrible credit because the buyer does not pay the loan. Non-performing loans eventually become debt which reduces net income. To avoid this, use an accounting system so that financial statements are maintained.

Is Bad Debt an Expense?

Bad debts are usually an operating expense in the organization’s selling, general, and also administrative expenses. These costs will reduce the company’s net profit for the same period.

As a result, bad debts are recorded in the income statement. This burden can help companies know which customers are more likely to default. The existence of this component of bad debt is one that companies must record and account for in their financial statements.

How to Handle Bad Debts

Companies can do it in two ways to charge receivables to consumers no longer. The first way is to do a direct write-off. The second way companies can do this is to gradually decrease the receivables, known as allowance methods. Here we summarize a more precise explanation of both approaches:

Write-off method

Under the direct write-off method, bad debt is charged to expense as soon as it is apparent that an invoice will be unpaid. Because this method writes off directly to customers’ accounts receivable, companies need to consider the requirements for writing off bad debts from consumers.

In this way, the burden of bad debts is a loss for the company and also reduces profits. Instead, the company will include the bad debts in an expense account, increasing the liability.

Allowance method

The allowance method for bad debts does not include it in the journal. This method prioritizes the allowance receivables gradually with small amounts. Companies that use the allowance for doubtful accounts method do not show losses in their financial statements.

On the other hand, bad debts will gradually reduce the company’s profit. This method is considered far superior to the company, especially from a stakeholder point of view. There are three main components of the allowance method, including:

- Bad debts estimation.

- Journal entry records by debiting bad debts expense and crediting allowance.

- When you decide to write off an account, debit the allowance for doubtful accounts and also credit the account receivable accordingly.

Doing business is always about trying to foresee the unforeseen,” – says Latoria Williams, the CEO of 1F Cash Advance. “Therefore, I find the allowance method preferable. This is because it can help you prevent a bad debt burden and manage it more efficiently.

First, you do a calculation based on your current accounts receivable to determine what percentage of your total receivables will go uncollected. Then, you reduce your company’s profit gradually by recording your estimated bad debts in a journal.

The amount of bad debts will be calculated by multiplying the rate by your net credit sales. You can also use the accounts receivable method, which assumes that the longer the debt is unpaid, the higher the chance that you won’t get your money back.

Method of Estimating Bad Debts

Bad debts are calculated as a percentage of the total receivables. To calculate the cost of bad debt, divide all receivables by the total number of bad debts and also multiply that number by 100 to get a percentage.

For example, a company with accounts receivable of $10,000 and bad debts of $5,000 uses the following formula to calculate the cost of bad debts.

$5,000 ÷ $10,000 x 100% = 5%

In this case, its bad debt expense represents 5% of its accounts receivable. The best way to manage bad debt is to use this formula to monitor it as a whole and within each customer account.

By setting certain thresholds for current and potential non-performing loans, companies can take steps to manage and also prevent problem loan burdens before they get out of control.

Counting receivables manually with large amounts is prone to errors that have a negative impact on company finances. The time needed to calculate manually is also not small, for that use the financial software from HashMicro to help calculate your company’s finances.

Recording Bad Debts on Journal

Sales percentage

The first way is to create a report based on the percentage of sales. The first step is to add up the net and bad debts to determine the percentage of sales. Management then determines the cost of non-performing loans through the time between the sale of net debt and also the total sales proceeds. Management calculates the rate and then multiplies it by net credit sales or total credit sales to determine the cost of bad debts. Here’s an example:

On April 30, 2021, Great Bobby Ltd reported net credit sales of $100,000. Using the percentage of sales method, they estimate that 1% of their credit sales will go uncollected. Based on the table below, the $1,000 (1% of $100,000) represents the cost of bad debts that management expects to incur.

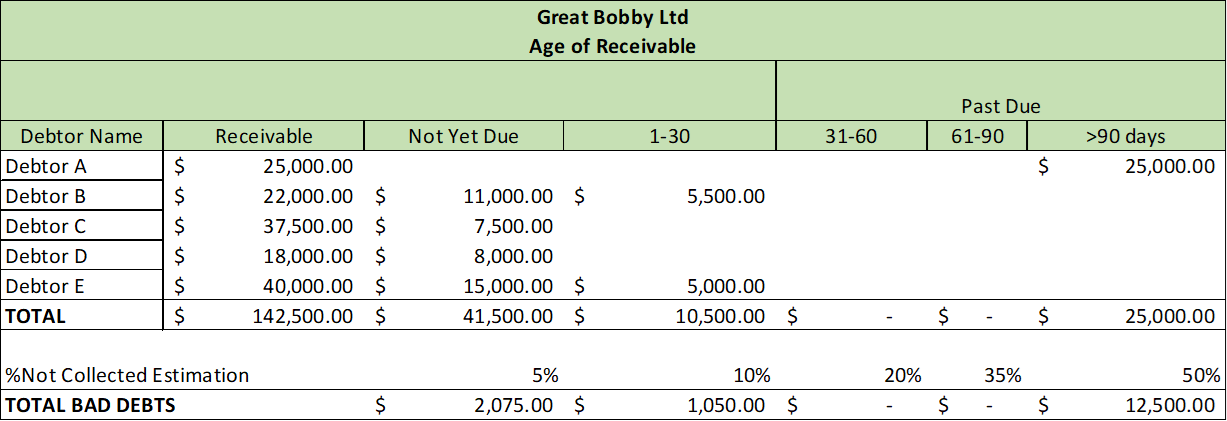

Account receivable age percentage

Based on the percentage of accounts receivable method, which estimates the cost of bad debts, companies make a list of receivable ages that varies depending on each policy. For instance, Great Bobby Ltd has a list of receivables with estimated bad debts.

As of July 30, 2021, Debtor A’s receivables have exceeded the billing limit of 90 days, while debtors B and E are due for one week. To keep the financial condition safe, the estimated writing off bad debts in the July 30 journal would be:

= Not Due + Past Due

= $2,075 + $1,050 + $12,500 = $15,625

Related article: Amortization: Definition, Method, and Examples in Accounting

Conclusion

Bad debts are receivables from the company for a transaction, but the company cannot collect them from creditors. To write off consumer debt, the company can do it in two ways: write-off and allowance. The existence of bad debts is one that companies must record and also account for in the financial statements.

Now you don’t have to worry anymore to do your business accounting calculations! The Accounting System from HashMicro can help your business to automate the entire financial calculation process, from cash flow management, financial statement creation, bank reconciliation, and also others with the best system for Singapore enterprises.