Generating reports is one of the most important tasks in the financial industry. Reports can reveal your financial situation. Reporting has various purposes, such as statement of changes in equity and assessing the company’s current situation.

This report is very much needed in business because the company’s capital will definitely fluctuate. It either spends or creates a new source of income for the business. The statement of changes in equity is significant because it contains information on money that is not available elsewhere in the financial statements.

Therefore, every organization should generate this report to reap several advantages, particularly in achieving its objectives. Using accounting software is important to automate the reporting process, without the need to worry about human error or inaccurate data.

HashMicro accounting software is the best solution to automate the financial reporting process. This software includes budget management, financial statements, and comprehensive reporting and analysis. If you’re looking for the best software to streamline financial management, you can try HashMicro.

Understanding Statement of Changes in Equity

The Statement of Changes in Equity reconciles the opening and closing equity balances. It is a financial statement that summarizes the transactions affecting the shareholder’s equity during a specific period. This report tracks changes in retained profits, other reserves, and share capital, such as issuing new shares and the payment of dividends.

The statement is usually given separately, although it may sometimes included in another financial report. It is also feasible to present a more detailed version of the statement consisting of all equity components.

It might, for example, specify the par value of the common stock, additional paid-in capital, retained profits, and treasury stock individually, with all of these parts eventually adding up to the total ending equity.

Why Does Your Business Need a Statement of Changes in Equity?

The primary objective of the Statement is to give information about all changes in the equity account throughout an accounting period that is not otherwise accessible in the financial statements.

It provides shareholders with information that will help them make better investment decisions that you can use to determine the par value of ordinary and treasury stocks, explain retained profits, and boost investor confidence in your business.

As a result, it assists shareholders and investors in making better-educated investment choices. It also helps analysts and other financial statement readers understand what variables contributed to the change in equity capital. According to the IND AS, this statement must contain the following:

- Reconciliation of the opening and closing equity balances, including a detailed description of the changes.

- Comprehensive income for the accounting period is exact.

- Details of modifications and their effect when equity components are restated or retroactively applied align with IAS/Ind-AS 8.

Statement of Changes in Equity Components

A statement of equity generally summarises the changes in the equity components listed below:

1. Opening Balance

The starting balance is the finishing balance of the previous year’s shareholder equity statement. All subsequent additions and subtractions in the current fiscal year made to the equity statement’s beginning balance.

2. Net Income

Secondly, net income is a business’s revenue after all operating, and non-operating expenditures are deducted during a fiscal year. The value derived from the income statement sometimes called the profit and loss statement, is produced after each fiscal year.

3. Other Income

Thirdly, the equity statement accounts for any extra money received by the firm that was not recorded in the income statement. Other income sources include actuarial gains and unrealized profits on financial instruments.

4. Issue of New Capital

Amounts added to the total shareholder’s equity occur when new shares are issued and when capital is brought into the firm. This results in an increase in the total shareholder’s equity.

5. Net Loss

Net loss is the loss experienced by the business as a consequence of its activities within the fiscal year. It diminishes the company’s total capital and is therefore subtracted from the shareholder’s equity statement.

6. Other Loss

Like other income, the expenses or losses incurred by the company but not recognized in the income statement are accounted for in the equity statement. An excellent example of other comprehensive losses is actuarial or unrealized losses from financial derivatives.

7. Dividends

As with other income, the equity statement accounts for costs incurred or losses sustained by the business that are not recorded in the income statement. Other comprehensive losses include actuarial or unrealized losses resulting from financial derivatives.

8. Withdrawal of Capital

When shares are already redeemed, the amount is automatically deducted from the statement of shareholder’s equity since it diminishes the company’s overall equity.

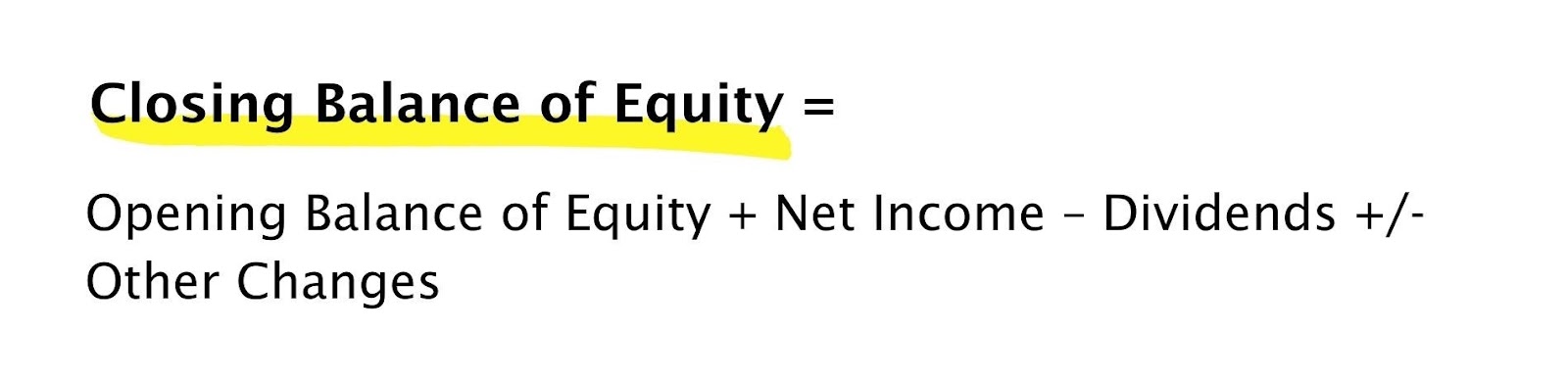

Statement of Changes in Equity Formula and Example

If you’re unfamiliar with the process of preparing for this, we’ve included a formula and example below.

Closing balance of equity formula:

Cover the criteria outlined above, and you can make sure that your statement of changes in equity is suitable for its intended use.

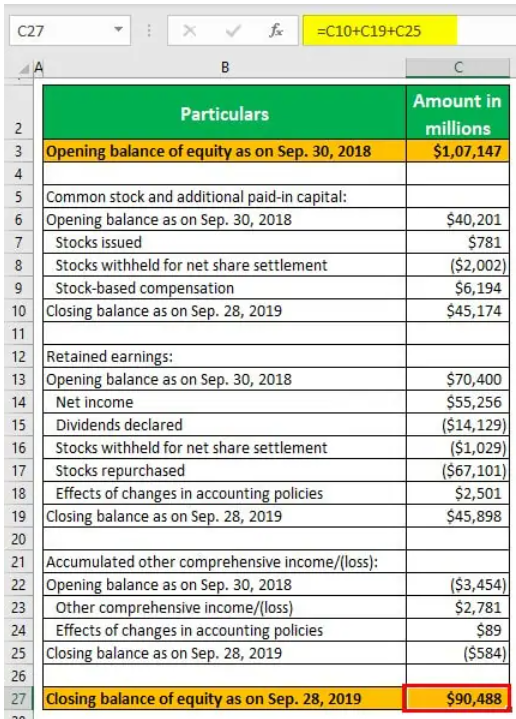

Example:

Source: Annual report of Apple Inc. for the year 2019

Conclusion

Not every company bothers to provide a statement of changes in equity. Not sure whether it’s worth putting one together? However, your yearly reporting should include a notice of changes in equity. It may assist shareholders in understanding what drives gains or losses in equity over the accounting period. Investors will be happier and more driven if informed.

Suppose you’re experiencing difficulty preparing a statement of changes in equity for your company. In conclusion, you may enlist the help of HashMicro’s Accounting System to assist you.

This system will assist you in handling invoices and payments, localized taxes, and creating numerous financial reports. Businesses need this system to keep track of all transactions to do business efficiently. So try the free demo today by clicking here!