Did you know that efficient tax filing can significantly improve your business’s financial management in Singapore? A streamlined approach helps organizations stay compliant, avoid penalties, and reduce the administrative burden during tax season.

Failing to manage your tax obligations properly can lead to errors, delays, and unnecessary fines. It may also limit your company’s ability to focus on strategic growth, especially in a fast-evolving regulatory environment.

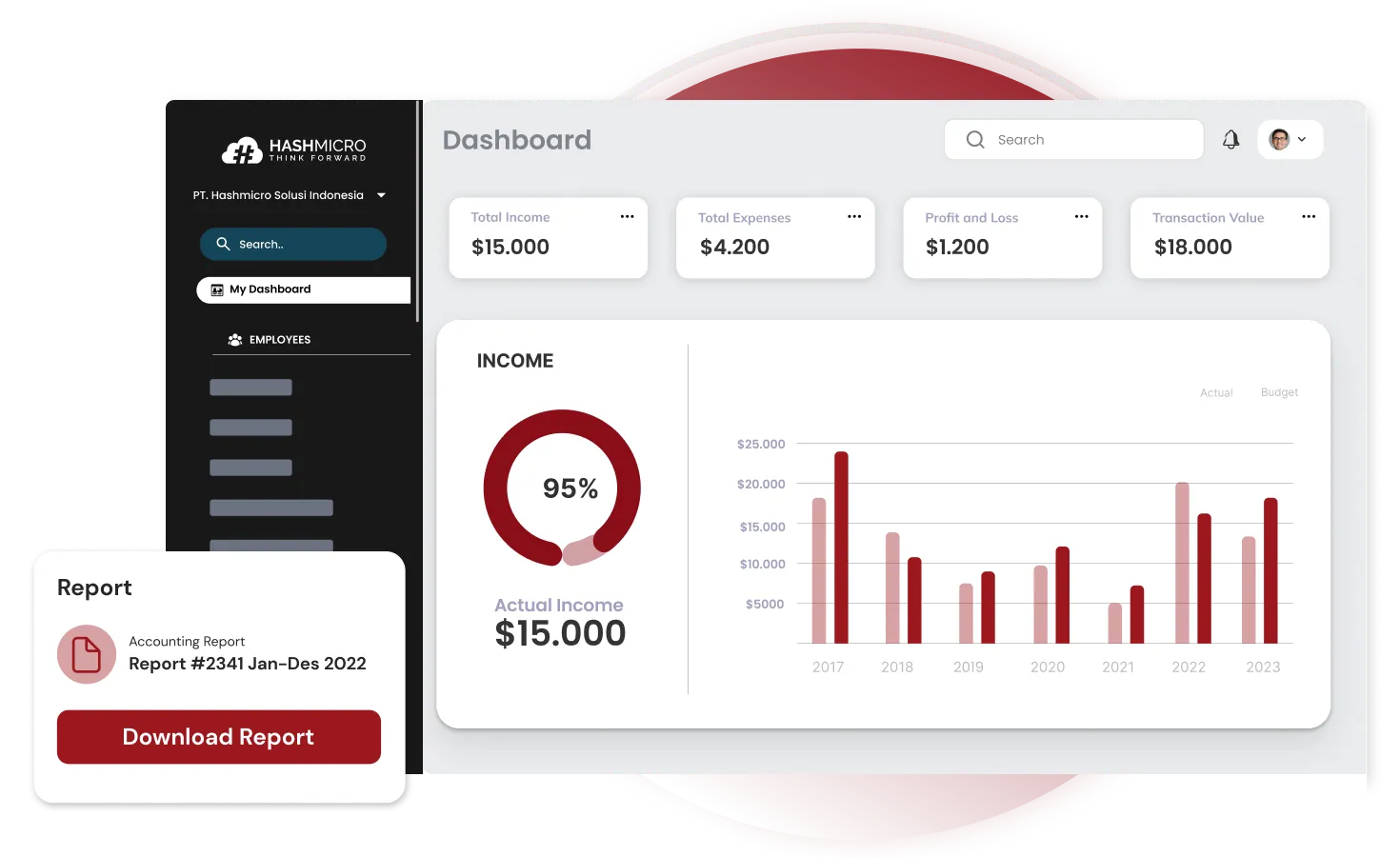

HashMicro’s Accounting Software simplifies tax filing through automated calculations, accurate reporting, and real-time updates on compliance requirements. With intelligent workflows and reliable data, the system helps businesses reduce manual work, stay compliant, and file taxes with confidence.

Keep reading to learn how efficient tax filing works and how HashMicro’s digital solutions can help you grow your business in Singapore.

Key Takeaways

|

Understand Your Tax Filing Obligations

Tax filing is the process of submitting income and financial information to the Inland Revenue Authority of Singapore (IRAS) to determine tax liabilities. For individuals, this involves declaring yearly earnings through the Income Tax Return.

For businesses, it requires filing the Estimated Chargeable Income (ECI) within three months of the financial year-end and submitting the Corporate Income Tax Return. Companies must also ensure proper bookkeeping and maintain records to support their declarations.

In Singapore, all companies, including private limited firms and foreign entities with branches in the country, are required to file corporate tax in Singapore. Sole proprietorships and partnerships are also exempt from this obligation, as their business income is reported under the owner’s tax return.

Corporate Tax Filing in Singapore

To calculate the tax due, companies must derive their taxable income by subtracting allowable business expenses, capital allowances, and relevant exemptions from their total revenue. Accurate financial records must be maintained to justify these claims and ensure compliance.

The tax filing process involves two main obligations: first, the submission of the Estimated Chargeable Income (ECI) within three months from the end of the financial year, unless the company qualifies for a waiver, and second, the annual filing of the Corporate Income Tax Return using Form C or Form C-S, due by November 30.

To simplify tax compliance, businesses are encouraged to use IRAS’s myTax Portal. This digital platform enables them to file required documents, monitor deadlines, access previous filings, and stay updated on their tax matters securely and efficiently.

Common Tax Filing Mistakes to Avoid

Tax filing can sometimes lead to mistakes, which may happen to anyone. These errors generally fall into two main categories: those made for employees and those made for self-employed individuals. Below is an explanation of each type.

Mistakes for employees

If you’re an employee, start by checking whether your employer is part of the Auto-Inclusion Scheme (AIS). Even if your employer has submitted your income details to IRAS, you must still file an Income Tax Return if you receive a notification via SMS, email, or letter.

To ensure accurate filing and avoid issues with your tax obligations, it’s essential to be aware of common errors when filing personal income tax and how to prevent them. Here are the explanations:

- Incorrect relief claims: Review the eligibility for each of your claims, even if the information was automatically carried over from last year’s tax assessment.

- Not filing your income tax return: You must file your income tax return if IRAS has sent you a notification to do so, even if you had no income in the previous year.

- Incorrect expense claims: You should only claim employment expenses that were directly related to performing your official job duties.

- Not informing IRAS when you discover mistakes in your submission: You are allowed to submit a revised tax return once before April 18, before receiving your tax assessment notice.

- Not clicking the “submit” button: After clicking “submit” on the Consolidated Statement page under My Declaration, an acknowledgment page will appear confirming your tax return submission.

Mistakes for self-employed individuals

If you earn self-employment income, it should be declared under the ‘Trade, Business, Profession or Vocation’ section of your Income Tax Return.

This requirement also applies to employees or retirees who transition into self-employment, such as starting a business after leaving a job, offering independent consultancy tax services after retirement, or turning a personal hobby into a home-based venture.

To ensure compliance, it’s essential to understand the common pitfalls freelancers and business owners face when filing taxes and learn how to avoid them.

- Reporting net income as “revenue”: In the 2-line/4-line statement, you should declare your gross income or sales as “revenue” before subtracting any allowable business expenses.

- Claiming self-employed CPF relief: You don’t need to submit a claim, as it is automatically granted based on information provided by the CPF Board.

- Declaring estimates/not keeping proper records: Providing estimates or failing to maintain accurate records is not permitted. You are required to keep adequate business records and accounts for five years.

- Declaring revenue only: You must fill in all sections of the 2-line/4-line statement. If your business incurred losses, follow the profit and loss guide and enter the amount in the “adjust profit/loss” field instead of listing it as “0”.

- Declaring self-employment income as “employment income” or “other income”: Your self-employment income should be reported under the “Trade, Business, Profession or Vocation” section in your income tax return.

Key Documents Needed for Tax Filing

When preparing to file taxes, businesses need to compile their financial statements. These records provide a detailed snapshot of the company’s financial position, including revenues, costs, assets, and debts. They play a key role in accurately determining taxable income.

Alongside financial statements, collecting receipts is essential. These documents verify the expenses and transactions made throughout the fiscal year, supporting any deductions claimed and ensuring all costs are properly substantiated.

Additionally, tax computation sheets must be prepared to outline taxable income and deferred tax payable, providing clarity on deferred tax assets and liabilities. Keeping these documents well-organized is essential for an efficient and accurate tax filing process in Singapore.

Tips for Improving Your Tax Filing Process

After understanding the definition, key document, and common mistakes in tax filing, the next step is to explore practical tips for improving your tax filing process and ensuring greater accuracy and efficiency.

1. Knowing the deadline for personal income tax filing

It’s important to be aware of the tax filing deadline for personal income tax filing in Singapore: April 15 for paper submissions and April 18 for e-filing. Filing notifications are typically sent between January and February, with the filing period running from March 1 to April 18.

Most taxpayers receive their tax bills starting from the end of April. If additional time is needed, a filing extension of up to 14 days may be requested. Fulfilling your tax responsibilities involves two key steps: submitting your income tax return and addressing your tax bill once it has been issued.

2. Be prepared with the necessary documents to file an income tax return

Before accessing the myTax Portal, make sure you have all the necessary documents prepared. It includes your Singpass or Singpass Foreign User Account, Form IR8A if your employer is not part of the Auto-Inclusion Scheme (AIS), details of dependents for new relief claims, and information on any rental or additional income.

The Consolidated Statement will specify if any documents need to be uploaded. It’s also important to keep accurate records for at least five years to support your declared income and claimed expenses.

3. Avoid mistakes when making tax relief claims

IRAS has identified that the most commonly misclaimed tax reliefs include qualifying child relief, spouse relief, and parent relief, often due to taxpayers not meeting the necessary eligibility criteria. Errors also frequently occur when multiple individuals claim the same dependent, leading to duplicate claims.

Suppose more than one taxpayer qualifies for the same dependent. In that case, the relief can be shared based on an agreed division, provided the total amount claimed does not exceed the allowable limit. To avoid these issues, it’s important to verify your eligibility or seek guidance from a Singapore tax professional.

4. Making changes after filing or receiving an income tax bill

Suppose you need to make changes after submitting your original income tax return. In that case, you can refile through the myTax Portal within seven days of your latest submission or by April 18, whichever comes first.

Starting from YA 2024, IRAS has been sending out tax bills, also referred to as the Notice of Assessment (NOA). It’s important to review your bill carefully to ensure all reported income and relief claims are correct.

If you notice any missing income or unclaimed reliefs in your bill, you must notify IRAS by using the Object to Assessment feature on the myTax Portal within 30 days. In cases where you discover mistakes in your tax return, it’s advisable to inform IRAS and rectify the issues voluntarily and promptly.

5. File your income tax with ease using digital or software tools

Filing your income tax and property tax in Singapore can be simple when you use the right digital tools and software solutions. Staying updated on important deadlines, available reliefs, and eligible deductions helps you manage your taxes efficiently and remain compliant with IRAS requirements.

If the process feels complex or you want to ensure everything is filed correctly while maximizing potential savings, digital tax solutions and professional assistance can make the entire experience much more manageable.

Simplify Your Tax Filing Process with HashMicro’s Accounting Software

HashMicro’s Accounting Software is the ideal solution for simplifying your tax filing process with accuracy and efficiency. Equipped with smart features like automated tax calculations, real-time reporting, and AI-powered assistance, it ensures your business remains compliant without the manual burden.

The software streamlines complex tax filing procedures, minimizing errors and saving valuable time. With a user-friendly interface, powerful performance, and scalable capabilities, it caters to businesses of all sizes and industries in Singapore.

HashMicro offers a free demo to explore how HashMicro’s accounting solution can make your tax preparation faster, easier, and more accurate. Here are the key features designed to support tax filing:

- Auto-Generated Tax Reports: Automatically generate tax reports based on real-time financial data. This feature ensures that all required documents are ready and accurate, reducing the need for manual calculations or cross-checking.

- Multi-Entity Tax Filing Support: File taxes for multiple business units or subsidiaries with consolidated reporting. It simplifies coordination and ensures unified compliance across entities.

- Budget vs. Tax Projection Comparison: Compare your budget estimates with projected tax obligations to plan and avoid unexpected liabilities.

- Tax Summary by Department or Branch: Gain a clear breakdown of tax contributions across different branches, projects, or departments. It helps identify high-impact areas and ensures better tax management.

- Real-Time Compliance Tracking: Monitor changes in tax regulations and system alerts to stay compliant. This proactive approach helps avoid penalties and late filings.

In addition, HashMicro also offers Hashy AI to boost efficiency by automating data input, verifying tax-related entries, and flagging inconsistencies across reports. It supports faster reviews and higher accuracy.

Another standout tool is the AR Tax Tracker, which automates the tracking of tax on receivables and prepares Statements of Account (SoA) with tax details, perfect for ensuring proper documentation and timely submissions.

Lastly, the AP Tax Module enhances vendor payment coordination with proper tax classifications and deductions, making the whole filing process more transparent and reliable.

Conclusion

Choosing the right tax filing solution in Singapore is essential for businesses looking to enhance accuracy, save time, and ensure regulatory compliance. A reliable system streamlines financial reporting, reduces manual errors, and supports better decision-making throughout the tax season.

HashMicro’s Accounting Software offers an all-in-one platform with a user-friendly interface, powerful automation tools, and integration with other core business systems. It enables companies to manage tax computations, generate reports, and file returns more efficiently.

For businesses in Singapore seeking to improve their financial processes, the NTUC CTC Grant provides valuable support. Eligible companies can receive up to 70% funding to adopt digital solutions like HashMicro.

Request your free demo today and experience how HashMicro’s Accounting Software can simplify your tax filing process while enhancing overall financial management.

Frequently Asked Questions

-

When to file Singapore income tax?

Filing notifications (SMS/Email/Letter) are sent from Feb to Mar. If you received a notification to file, you may e-file from March 1 to April 18. Generally, most taxpayers will be receiving their tax bills from the end of April onwards. Use the filing checker below to determine whether you’re required to file.

-

What is the best time to file taxes?

To avoid penalties: If your objective is to avoid late fees, you’ll want to get your return in by Tax Day. If you miss the April deadline, the IRS could hit you with a late-filing penalty of 5% of your bill, up to a maximum of 25% of your taxes owed.

-

What happens if you don’t pay income tax in Singapore?

If you fail to make payment for your overdue tax, IRAS may appoint your banks, tenant, employer, etc., as an agent to recover the unpaid tax. Your appointed agent(s) will be required to pay money due to you to the Comptroller to settle your tax liabilities.