Deferred revenue is money you’ve received but haven’t earned yet. Customer pays upfront → you owe them a service → it’s a liability, not income.

Mastering the deferred revenue journal entry is not merely a bookkeeping exercise; it is a fundamental requirement for compliance with global accounting standards such as ASC 606 and IFRS 15. Mismanagement of these entries can lead to inflated revenue figures, inaccurate financial statements, and severe regulatory penalties. For financial controllers and business owners, understanding the lifecycle of unearned revenue—from the initial receipt of cash to the eventual recognition of income—is essential for maintaining the integrity of financial reporting and ensuring strategic decision-making based on accurate data.

Key Takeaways

Automates the complex process of revenue recognition, ensuring compliance with ASC 606 and reducing manual errors.

Provides real-time visibility into deferred revenue liabilities, helping businesses manage cash flow and future obligations effectively.

Seamlessly integrates with invoicing and billing modules to automatically trigger journal entries upon payment receipt.

Generates detailed audit trails and financial reports, simplifying the month-end closing process for finance teams.

Defining Deferred Revenue in Modern Accounting

Deferred revenue, often referred to as unearned revenue, represents a prepayment received by a company for goods or services that have not yet been delivered or performed. In the context of accrual accounting, revenue cannot be recognized on the income statement until it is “earned.” Therefore, when a customer pays in advance, the company has an obligation to provide value in the future. This obligation classifies the received cash not as income, but as a liability on the balance sheet.

So the key distinction that you should highlight is Cash in your bank ≠ Revenue on your books. You recognize revenue only when you deliver.

Why is it a Liability?

It feels counterintuitive with the money in your bank, but it’s a liability? Here’s the logic: you owe the customer a service. If you don’t deliver, you refund. So until you fulfill that obligation, the cash isn’t truly yours.

For classification, it’s straightforward: if you’ll deliver within 12 months, it’s a current liability. Multi-year contracts? Split them with the portion beyond 12 months goes to long-term liabilities.

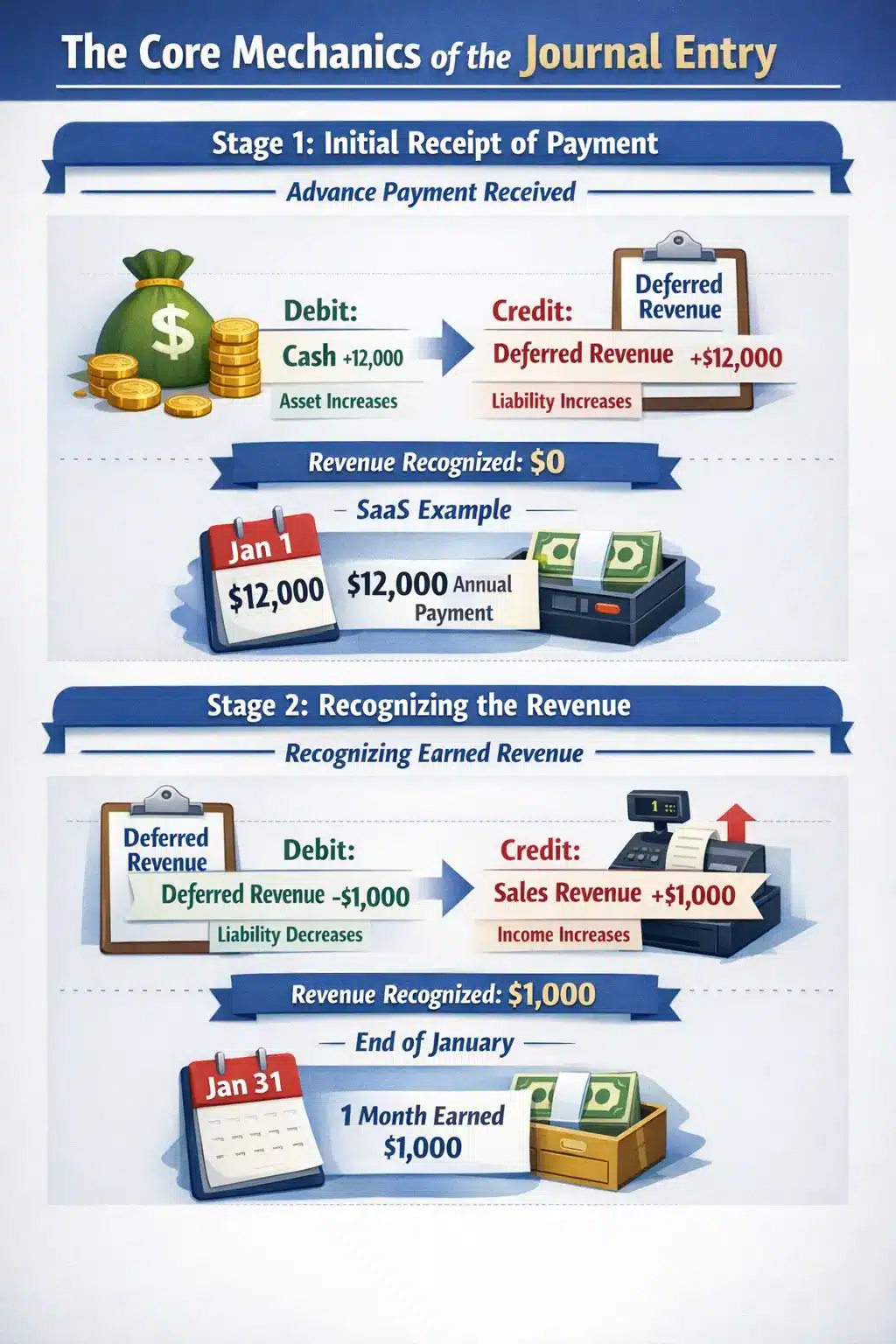

The Core Mechanics of the Journal Entry

The accounting cycle for deferred revenue involves two primary stages: the initial recording of the prepayment and the subsequent recognition of revenue as it is earned. Understanding the debit and credit flows in these stages is vital for accurate bookkeeping.

Stage 1: Initial Receipt of Payment

When a customer makes an advance payment, the company’s cash account increases. Simultaneously, the company incurs an obligation. The journal entry reflects an increase in assets (Cash) and an increase in liabilities (Deferred Revenue).

- Debit: Cash (Asset increases)

- Credit: Deferred Revenue (Liability increases)

For example, consider a SaaS company that receives an annual subscription payment of $12,000 on January 1st. The entry would be a debit to Cash for $12,000 and a credit to Deferred Revenue for $12,000. At this specific moment, the revenue recognized on the income statement is zero.

Stage 2: Recognizing the Revenue

As time passes or services are rendered, the company fulfills its obligation. Consequently, the liability decreases, and the revenue is recognized. This is typically done through adjusting entries at the end of each month or accounting period.

- Debit: Deferred Revenue (Liability decreases)

- Credit: Sales Revenue (Equity/Income increases)

Continuing the SaaS example, at the end of January, the company has earned one month of the subscription ($1,000). The entry would debit Deferred Revenue for $1,000 and credit Sales Revenue for $1,000. This process is repeated monthly until the entire $12,000 liability has been moved to revenue.

Regulatory Framework: ASC 606 and IFRS 15

The treatment of deferred revenue is heavily governed by accounting standards, specifically ASC 606 (Revenue from Contracts with Customers) in the US and IFRS 15 internationally. These standards introduced a five-step model that entities must apply to determine when and how much revenue to recognize.

| Step | Action | Example |

|---|---|---|

| 1 | Identify contract | Signed SaaS agreement |

| 2 | Identify obligations | Software + Support |

| 3 | Determine price | $12,000/year |

| 4 | Allocate price | $10K software + $2K support |

| 5 | Recognize when delivered | Monthly as service provided |

This framework ensures consistency across industries and prevents companies from manipulating earnings by recognizing revenue too early or too late. It places a heavy emphasis on the transfer of control of goods or services to the customer as the defining moment for revenue recognition.

Industry-Specific Application of Deferred Revenue

The core principle stays the same across industries—it’s a liability until you deliver. But how you recognize that revenue varies based on your business model.

Manufacturing: Deposits and Milestone Billin

Heavy machinery and custom fabrication often require upfront deposits before production begins. That deposit? Deferred revenue until the product is delivered.

The tricky part is when to recognize it. Under ASC 606, you either recognize revenue at final delivery (point in time) or progressively as you build (over time). If the product is custom-made with no alternative use, you can often recognize revenue as milestones are completed—say, 30% when the frame is done, another 30% after assembly. Your ERP needs to track percentage-of-completion and adjust the entries automatically.

Retail and E-commerce: Gift Cards and Breakage

Gift cards are textbook deferred revenue. Customer pays $100, you’ve delivered nothing—that’s a liability until they redeem it.

The complication is “breakage”: gift cards that never get used. You can recognize breakage as revenue, but only based on historical redemption patterns. If data shows 8% of cards expire unused, you recognize that 8% proportionally as other cards are redeemed—not all at once.

Distribution: Warranties and Bundled Services

Sell a $50,000 machine with a 2-year maintenance contract worth $5,000? You need to split it. The $45,000 for equipment is recognized on delivery. The $5,000 for maintenance is deferred and amortized monthly over 24 months.

This separation ensures you’re not inflating current revenue with services you’ll provide over the next two years.

The Critical Role of Adjusting Entries

The accuracy of financial statements hinges on the timely recording of adjusting entries. If a company fails to move amounts from deferred revenue to earned revenue, its liabilities will be overstated, and its revenue (and consequently, net income) will be understated. This distortion can affect tax liabilities, shareholder perception, and loan covenants.

When the end of the accounting period arrives, the finance team must determine the portion of the liability that has been satisfied. This process often involves reviewing schedules and understanding how to adjust journal entry records to reflect the transfer from liability to income. This is not always a simple division calculation; it may involve verifying delivery logs, consulting timesheets, or checking software usage data.

Automated accounting systems play a pivotal role here. Manual calculations in spreadsheets are prone to human error, especially as transaction volumes grow. Advanced Enterprise Resource Planning (ERP) systems can automate these recognition schedules, ensuring that the adjusting entry is posted precisely when the performance obligation triggers it.

Deferred Revenue vs. Accrued Revenue

Confusion often arises between deferred revenue and accrued revenue, as they are essentially opposites in the accounting cycle. Distinguishing between them is vital for accurate classification.

- Deferred Revenue: Cash is received before the service is provided. (Liability).

Example: Airline ticket purchased months in advance. - Accrued Revenue: Service is provided before the cash is received. (Asset).

Example: An electricity company supplying power for a month before sending the bill.

In deferred revenue, the company “owes” a service. In accrued revenue, the customer “owes” the money. Both require adjusting entries to reconcile the timing difference between cash flow and economic activity.

Impact on Financial Metrics and Analysis

Deferred revenue has a profound impact on the analysis of a company’s financial health. Analysts and investors scrutinize this account heavily, particularly in growth-stage technology companies.

Working Capital and Liquidity

Since deferred revenue is a current liability, an increase in this account technically reduces working capital (Current Assets minus Current Liabilities). However, unlike accounts payable, deferred revenue does not require a cash outflow to settle (except in the case of refunds). It is settled by delivering services, which usually have a lower marginal cost than the revenue value. Therefore, a high deferred revenue balance is often seen as a positive indicator of future health and customer commitment, despite its negative impact on standard liquidity ratios.

Valuation Metrics

For SaaS companies, “Billings” is a key metric calculated as Revenue plus the Change in Deferred Revenue. This metric provides a better proxy for the cash momentum of the business than GAAP revenue alone. Investors look for growing deferred revenue balances as a sign of strong sales pipelines and market demand.

Tax Implications of Deferred Revenue

The treatment of deferred revenue for tax purposes can differ from its treatment for financial reporting (GAAP/IFRS). This divergence creates deferred tax assets or liabilities.

Generally, tax authorities prefer to tax income as soon as the cash is received (the “Claim of Right” doctrine). However, financial accounting defers the income. This means a company might pay taxes on cash received in Year 1, even though the revenue isn’t recognized on the books until Year 2. Conversely, specific tax rules (like IRS Revenue Procedure 2004-34 in the US) allow for a one-year deferral of advance payments for tax purposes under certain conditions.

Navigating these discrepancies requires careful reconciliation between the tax books and the financial books to ensure compliance and optimal tax planning.

Auditing Deferred Revenue

Deferred revenue is a high-risk area for auditors because of the potential for manipulation. Management might be tempted to recognize revenue prematurely to meet earnings targets, or conversely, keep revenue deferred to smooth earnings in future periods (“cookie jar accounting”).

Key Audit Assertions:

- Completeness: Ensuring all cash receipts that represent future obligations are recorded as liabilities.

- Cut-off: Verifying that revenue is recognized in the correct period. Auditors will test transactions near the end of the year to ensure they aren’t pushed into the next year or pulled back into the current year inappropriately.

- Valuation: Ensuring the calculation of the deferred portion is mathematically accurate and consistent with the contract terms.

Auditors will typically request a “Deferred Revenue Roll-forward” schedule, reconciling the beginning balance, new billings, revenue recognized, and the ending balance. Discrepancies in this schedule are red flags for internal control weaknesses.

Future Trends in Revenue Accounting (2026 and Beyond)

Looking ahead, the management of deferred revenue is set to become even more data-driven. The rise of usage-based pricing models (e.g., pay-per-API-call, pay-per-gigabyte) is replacing simple flat-rate subscriptions. This shift makes revenue recognition highly dynamic, as the “earned” portion changes every minute based on consumption.

AI and Predictive Analytics: Artificial Intelligence is beginning to play a role in predicting revenue streams. AI models can analyze historical redemption patterns, churn rates, and usage data to forecast how deferred revenue will unwind with high precision. This allows CFOs to predict cash flow gaps and revenue shortfalls months in advance.

Blockchain for Smart Contracts: In the longer term, blockchain technology could automate revenue recognition through smart contracts. When a service delivery is verified on the blockchain (e.g., a shipment arrives or a digital key is used), the smart contract could automatically trigger the accounting entry, eliminating the need for manual recognition and reconciliation entirely.

Common Pitfalls and Mitigation Strategies

Even with sophisticated software, the management of unearned revenue is prone to errors that can lead to material weaknesses in financial audits. Awareness of these pitfalls is the first line of defense.

Handling Contract Modifications

One of the most frequent errors occurs during mid-term contract modifications—upsells, downsells, or early cancellations. When a customer upgrades their subscription halfway through a term, the remaining deferred revenue from the original contract must be treated correctly. The pitfall is often “prospective” versus “cumulative catch-up” treatment. Systems must be configured to either re-allocate the remaining deferred balance over the new term or recognize a one-time adjustment, depending on whether the modification adds distinct goods or services.

Foreign Exchange (FX) Adjustments

For global entities, deferred revenue sits on the balance sheet as a non-monetary liability in the functional currency of the subsidiary. However, complications arise during consolidation. Unlike Accounts Receivable, which is revalued at the current spot rate, deferred revenue is typically carried at the historical exchange rate (the rate at the time of the transaction). A common mistake is revaluing deferred revenue at the month-end spot rate, which creates artificial FX gains or losses. Mitigation involves strict system rules that lock the exchange rate for revenue schedules upon creation.

Cutoff Errors at Period End

Timing is everything. A common audit issue is the misalignment between the service start date and the revenue recognition start date. For instance, if a contract is signed on the 28th of the month but implementation doesn’t begin until the 5th of the following month, revenue recognition should generally not commence until the 5th. Automated systems often default to the invoice date, leading to premature revenue recognition. Mitigation requires a validation step where the “Revenue Start Date” is a distinct field from the “Invoice Date,” requiring manual confirmation or a trigger from the provisioning system.

Advanced Best Practices for Scale

As organizations mature, the management of deferred revenue should evolve from a compliance task to a strategic asset. Advanced best practices involve leveraging this data for broader business insights.

Continuous Auditing and Flux Analysis: Rather than waiting for the annual audit, high-performing finance teams perform monthly flux analysis on deferred revenue accounts. By comparing the expected amortization against the actuals, anomalies caused by data entry errors or system glitches can be detected immediately. This continuous auditing approach reduces the burden of the year-end close.

Integration with CRM for Forecasting: Integrating the ERP revenue module with the CRM (Customer Relationship Management) system allows for “Bookings to Revenue” forecasting. By applying the revenue recognition rules to the sales pipeline (weighted by probability), finance can project not just cash flow, but the actual P&L revenue impact of future sales quarters in advance. This alignment between sales and finance enables more accurate guidance for stakeholders and investors.

Conclusion

Deferred revenue is more than just a line item on the balance sheet; it is a reflection of a company’s future performance and its obligation to its customers. The journal entries associated with it—debiting cash and crediting liability, followed by the gradual shift to revenue—are fundamental to the integrity of accrual accounting.

For businesses navigating the complexities of ASC 606, multi-element contracts, and subscription models, precision is non-negotiable. The risks of errors range from audit failures to misinformed strategic decisions. As business models evolve toward more service-oriented and usage-based structures, the reliance on robust, automated systems to manage these entries will only grow. By mastering the mechanics of deferred revenue, finance professionals ensure that their organization’s financial narrative remains accurate, compliant, and transparent.

Frequently Asked Question

The initial entry is a debit to the Cash account and a credit to the Deferred Revenue account (a liability). When the service is delivered, you debit Deferred Revenue and credit Sales Revenue.

Deferred revenue is classified as a liability on the balance sheet because it represents an obligation to provide goods or services to a customer in the future.

Initially, deferred revenue does not affect the income statement. It is only recognized as revenue on the income statement gradually as the performance obligations are satisfied over time.

If a contract is cancelled and the service is not delivered, the remaining deferred revenue usually must be refunded to the customer. The entry would be a debit to Deferred Revenue and a credit to Cash.

For SaaS companies, payments are often collected upfront for annual subscriptions. Correctly recording deferred revenue ensures that income is recognized smoothly over the subscription period, providing a true picture of monthly performance.