As a business professional, I’ve seen how inventory management is essential for smooth operations. It involves controlling the ordering, storage, and usage of inventory to meet demand efficiently without overstocking.

Companies using optimized inventory systems often achieve up to a 30% improvement in order fulfillment, minimizing delays and boosting customer satisfaction. With the right tools, I can balance supply and demand while reducing costly stock issues.

This article explains what inventory management is, why it matters, the benefits it delivers, and the key features behind an effective inventory process, so inventory stays accurate, available, and under control as operations scale.

Key Takeaways

|

Understanding Inventory Management

I view inventory management as keeping stock under control, from purchasing and receiving through storage, usage, and fulfillment, so I can meet demand without tying up cash in excess inventory. When I manage it well, I can reduce carrying costs, avoid stockouts, and keep customers satisfied.

In practice, it’s the operating rules I rely on to answer four recurring questions:

- What items should I stock (and where)?

- How much should I hold at any time?

- When should replenishment trigger?

- How will I maintain and prove stock accuracy?

If those answers change depending on who I ask, my inventory becomes fragile—especially across multiple locations and sales channels.

What are the 4 Main Types of Inventory?

I find it essential to understand the different types of inventory that I need to manage in my business. Each type plays a crucial role in ensuring a smooth and efficient supply chain. Here are the four main types of inventory:

- Raw materials: These are the basic materials that a company uses to produce goods. Managing raw materials efficiently ensures production runs smoothly without interruptions from material shortages.

- Work-In-Progress (WIP): These items are in production but have not yet been completed. Effective management of WIP inventory helps track production progress and minimize delays.

- Finished goods: Products that are completed and ready for sale. Proper management of finished goods is crucial to promptly meeting customer demand and maintaining high customer satisfaction.

- Maintenance, Repair, and Operations (MRO): This includes supplies used in the production process but is not part of the final product, such as maintenance supplies, spare parts, and tools.

Inventory Benchmarks to Set Real Targets

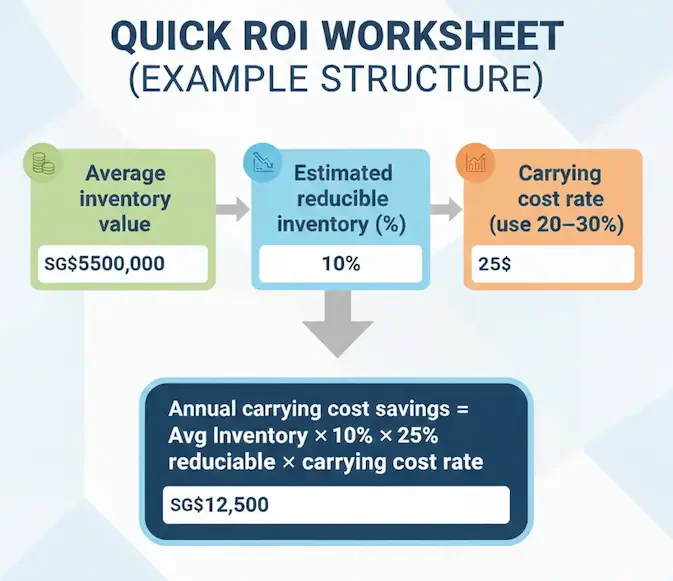

Benchmarks help you avoid guessing. Two numbers that matter early are inventory turnover and carrying cost.

Inventory turnover benchmarks (rule-of-thumb):

- Many retailers and e-commerce brands target 4–8 turns/year as a healthy range (varies by category and model).

- Grocery and fast-moving environments tend to run higher than specialty or luxury categories, so it’s better to benchmark against your closest peers than a universal number.

Carrying cost benchmark:

Carrying costs are often estimated at around 20%–30% of the average inventory value per year, including capital costs, storage, shrinkage, insurance, obsolescence, and handling.

Why it matters: if a business holds $500,000 in average inventory and the carrying cost is 25%, that’s $125,000/year just to keep stock on hand (before any stockouts or write-offs).

What are the Benefits of Inventory Management?

By understanding and implementing this system, I’ve experienced numerous advantages that greatly enhance my business operations. Here’s my explanation of why inventory management is so important:

- Streamlined processes reduce the time and effort required to manage stock levels, orders, and deliveries.

- Avoid overstocking and understocking to reduce storage costs and minimize waste.

- A structured stock control system supports compliance with legal and industry regulations.

- Improved customer satisfaction and loyalty by ensuring that products are available.

- Accurate inventory data provides insights that can inform better business decisions.

- Provides a detailed inventory movement report to monitor stock movements.

- PPIC meaning production planning and inventory control aligns stock with production to meet demand.

Inventory Management Challenges

I often face stock control challenges that can affect my business growth and profitability. Effectively addressing these issues while understanding the role of a well-structured system is essential for overcoming them. This includes managing inventory holding costs and other key challenges I commonly encounter:

- Achieving accurate inventory counts

- Balancing inventory levels

- Managing multiple sales channels

- Fluctuating customer demands and market trends

- Ensuring data accuracy and security

Inventory Management Methods

Effective stock control requires me to use different methods that suit my business needs. Each method has its own advantages and can be applied individually or combined for better inventory control. Here are some of the inventory management methods I often use:

1. ABC Analysis

ABC analysis categorizes inventory into three groups based on importance and value:

- A items are high-value products with a low frequency of sales.

- B items are moderate-value products with a moderate frequency of sales.

- C items are low-value products with a high frequency of sales.

This method helps businesses prioritize their focus and resources on managing the most critical items, ensuring that high-value products are closely monitored.

2. Just-In-Time (JIT)

The Just-In-Time method aims to minimize inventory by receiving goods only when needed for production or sales. This approach reduces carrying costs and minimizes waste but requires precise forecasting and strong supplier relationships to avoid stockouts.

3. Batch Tracking

Batch tracking involves monitoring inventory by batch or lot. This method is particularly useful for businesses dealing with perishable goods or products with expiration dates. It helps track each batch’s production, usage, and remaining shelf life, ensuring product quality and regulatory compliance.

4. Demand Forecasting

Demand forecasting uses historical data, market trends, and statistical methods to predict future inventory needs. Accurate demand forecasting helps businesses plan their inventory levels, avoid stockouts, and reduce excess inventory, ultimately improving customer satisfaction and operational efficiency.

5. Material Requirements Planning (MRP)

MRP is a system that calculates the materials needed for production and schedules their purchase. It is based on the production schedule and inventory levels, ensuring that materials are available just in time for manufacturing, reducing delays, and optimizing production processes.

6. FIFO and LIFO

- FIFO (First-In, First-Out): This method assumes that the oldest inventory items are used or sold first. It is particularly beneficial for perishable goods, as it ensures that older stock is used before it expires.

- LIFO (Last-In, First-Out): This method assumes that the most recently acquired items are used or sold first. While it can be advantageous for certain tax and accounting purposes, it may not suit businesses dealing with perishable products.

7. Economic Order Quantity (EOQ)

EOQ is a mathematical formula used to determine the optimal order quantity that minimizes total inventory costs, including ordering and holding costs. By calculating the ideal order size, businesses can reduce carrying costs and ensure that inventory levels are sufficient to meet demand without overstocking.

How to Implement Inventory Management in 5 Phases

This is the core repositioning: inventory management implementation, not a generic overview.

Phase 1: Baseline and Map Current Reality (Week 1–2)

Goal: establish the truth before optimizing anything.

Deliverables:

- SKU master cleanup (units, barcodes, pack sizes, categories)

- Warehouse/location mapping (zones, bins, storage rules)

- Baseline KPIs: current stock accuracy, stockouts, dead stock %, lead times

Success metrics

- SKU data completeness (e.g., 95%+ core fields filled)

- Initial stock accuracy measurement (cycle count sample)

Phase 2: Define Policies and Control Rules (Week 2–4)

Goal: decide how inventory will be governed.

Deliverables:

- Reorder policy per item group (min/max or reorder point)

- Safety stock logic tied to supplier lead time variability

- Receiving/putaway standards and issue/transfer rules

- Counting policy (cycle count schedule + tolerances)

Success metrics:

- Policy coverage (e.g., reorder rules applied to top 80% of revenue SKUs)

- Reduction in emergency purchasing/expediting

Phase 3: Improve Planning and Replenishment (Week 4–6)

Goal: align replenishment with demand and constraints.

Deliverables:

- Demand signal selection (sales history, seasonality, promotions)

- Supplier lead time and MOQ documentation

- Forecast cadence (weekly/monthly) + exception review

Success metrics:

- Stockout rate trending down (set a target; many retailers aim to keep it very low)

- Service level improvement (fill rate or OTIF)

Phase 4: Execution Discipline (Week 6–10)

Goal: make the warehouse process predictable and auditable.

Deliverables:

- Standard receiving: GRN, QC checks, discrepancy handling

- Bin location control + picking rules

- Inter-warehouse transfer workflow

- Shrinkage and damage handling

Success metrics:

- Faster putaway-to-available time

- Higher pick accuracy and fewer fulfillment reversals

Phase 5: Optimize and Scale (Week 10–Ongoing)

Goal: reduce cost, increase speed, and standardize across sites.

Deliverables:

- SKU segmentation review (ABC)

- Dead stock liquidation playbook

- Supplier scorecarding

- Continuous improvement cadence (monthly KPI reviews)

Success metrics:

- Higher turnover without service loss

- Lower carrying costs and reduced write-offs

ROI Framework: How to Quantify Savings Before Investing

A simple ROI model focuses on three levers:

- Carrying cost reduction: If the carrying cost is 20–30% annually, every dollar of inventory removed yields a meaningful annual return.

- Stockout reduction: Stockouts have a direct revenue impact and also erode loyalty at scale, especially in omnichannel environments.

- Shrinkage and write-off reduction: Better receiving, bin control, and counting lowers “invisible losses” (damage, expiry, mispicks, theft).

7 Critical Implementation Mistakes That Cost Money

These mistakes don’t look dramatic on day one, but they quietly compound into expediting costs, missed sales, and inventory numbers no one fully trusts. The goal of this section is to surface the implementation blind spots that drain cash, so we can lock in clear rules, clean data, and a process that holds up under real operational pressure.

- Automating before mapping the real process: If I digitize receiving, putaway, picking, returns, and adjustments before I align everyone on the actual flow (including exceptions, approvals, and handoffs), I’m not fixing chaos; I’m hard-coding it. The result is predictable: workarounds become “the process,” data quality drops, and the audit trail no longer reflects what truly happened on the floor.

- Setting reorder points without lead-time variability: Reorder points should be based on demand during the lead time plus safety stock, and safety stock should reflect how suppliers behave in practice, not how I want them to behave. When I treat lead time as a single fixed number, replenishment triggers at the wrong moments, which forces expensive expediting or creates avoidable stockouts.

- Ignoring seasonality and promo spikes: Demand doesn’t move in a straight line, especially when seasonality and campaigns create sharp peaks and troughs across channels. If I place purchase orders without a demand calendar and a clear uplift plan (what drives the spike, for which SKUs, in which channels), I’ll either carry surplus into slow months or run dry exactly when the business needs stock the most.

- Treating cycle counts as “optional”: Accuracy decays quietly unless I run a disciplined counting routine with clear frequency, tolerance limits, and a root-cause workflow when variances appear. Once cycle counts get deprioritized, shrinkage and transaction errors pile up until procurement, fulfillment, and finance start working off different versions of “the truth.”

- No owner for SKU master data: Item master data needs ownership because one wrong detail, UOM conversion, pack size, barcode, lead time, or storage attribute, spreads downstream into purchasing, picking, valuation, and reporting. Without governance, duplicates and inconsistent setups proliferate, and I end up making decisions based on reports that look clean but are built on flawed foundations.

- No rules for substitutions and bundles: Substitutions and bundles only work when there are explicit rules for consumption logic (kit/BOM behavior), approved substitutes, and how cost and revenue mapping should follow the physical movement of goods. If those rules are missing, orders may still “complete,” but inventory quietly breaks, creating phantom availability, messy reconciliation, and distorted margins that surface late.

- Letting dead stock stay invisible: Dead stock must be visible and measurable through ageing (days-on-hand, last movement, obsolescence risk) and paired with predefined actions such as redeploy, RTV, liquidation, or write-down. If I don’t intentionally track slow movers, they become long-term cash traps that keep adding carrying, handling, and obsolescence costs month after month.

How Is Inventory Management Different from Other Processes?

I’ve noticed that stock management is often confused with other related processes. Understanding these differences is essential for me to optimize overall efficiency. Let’s explore why inventory management is important and how it differs from other processes I handle:

1. Inventory Management vs. Inventory Control

| Inventory Management | Inventory Control |

|

|

2. Inventory Management vs. Inventory Optimization

| Inventory Management | Inventory Optimization |

|

|

3. Inventory Management vs. Order Management

| Inventory Management | Order Management |

|

|

4. Inventory Management vs. Warehouse Management

| Inventory Management | Warehouse Management |

|

|

5. Inventory Management vs. Logistics

| Inventory Management | Logistics |

|

|

6. Inventory Management vs. ERP

| Inventory Management | ERP |

|

|

Maximize Efficiency & Accuracy with Inventory Solution

Effective inventory management is crucial for my business’s operational success. With HashMicro’s Inventory Management Software, I can streamline processes, automate tracking, and gain real-time visibility, ensuring precise stock control and optimal resource management.

To make informed decisions, I took advantage of HashMicro’s free consultation, which helped me explore the system’s full capabilities. Trusted by leading enterprises like McDonald’s, Forbes, and Brinks, HashMicro has proven to be a reliable solution tailored to diverse industry needs.

Moreover, I can benefit from up to 70% funding support through the CTC Grant, making it easier to implement a system that perfectly aligns with my operational requirements.

Features:

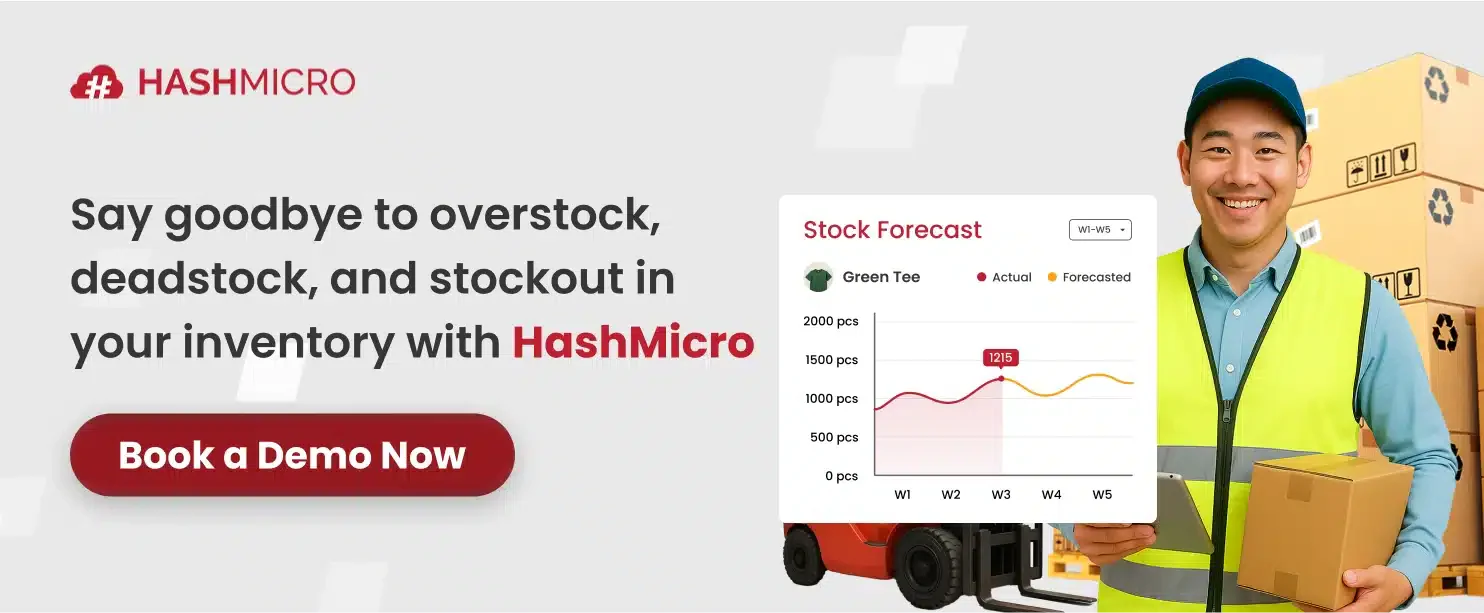

- Stock Forecasting – Leverage historical data to accurately predict demand and optimize inventory levels.

- RFID Automation – Enhance stock tracking precision with automated in/out recording.

- Inventory Performance Analysis – Identify fast- and slow-moving items to refine purchasing strategies.

- Barcode & QR Code Integration – Improve inventory accuracy with seamless scanning technology. The system integrates with barcode and QR code technology, streamlining inventory tracking and management.

- Multi-Location Inventory Management – Monitor and manage stock across different locations with ease.

- Comprehensive Real-Time Reporting – Access detailed inventory insights for data-driven decision-making. Additionally, the inventory aging report provides insights into the age of your stock, helping you identify slow-moving items and prioritize the sale of older inventory before it becomes obsolete.

“Inventory management is more than tracking stock; it drives cash flow, efficiency, and customer satisfaction. With automation, businesses gain visibility and make smarter, data-driven decisions.”

— Angela Tan, Regional Manager

Ready to see how HashMicro can fit into your budget? Click the banner below to explore our pricing schemes and discover the best plan for your business needs.

Conclusion

Maintaining control over inventory is crucial for optimizing the supply chain, reducing costs, and ensuring timely delivery. Implementing a cloud-based system enhances control by providing real-time stock visibility, preventing stockouts, overstock, and lost sales.

The best Inventory Management Software provides me with a comprehensive solution through real-time tracking, automated reordering, and detailed analytics. With this system, I can maintain optimal inventory levels, prevent stock discrepancies, and streamline my daily operations.

I’ve experienced firsthand how efficient inventory control can transform my business. That’s why I signed up for a free consultation to explore how HashMicro’s software can optimize my inventory processes and drive sustainable growth.

Frequently Asked Questions

What makes a good inventory manager?

Accurate data recording. Inventory managers must accurately record all stock details, including quantities, quality, style, type, and other relevant information. This ensures precise inventory tracking.

How can we manage inventory?

How to manage inventory:

1. Implement inventory management software

2. Regular audits and stock counts

3. Set reorder points

4. Use FIFO method

5. Categorize inventory

6. Forecast demand

7. Optimize storage

8. Supplier management

What is the goal of inventory management?

The goal of inventory management is to maintain optimal stock levels to meet customer demand without overstocking or understocking. This ensures efficient operations, minimizes costs and maximizes profitability.