Key Takeaways

Understand how manufacturing costs combine direct materials, direct labour, and factory overhead to show the real cost of making finished goods.

Review the main cost types, including direct materials, direct labour, overhead, fixed costs, and variable costs that affect production margins.

Use the total manufacturing cost formula to calculate production spending and review manufacturing cost per unit more accurately.

See how manufacturing software connects BOMs, work orders, inventory usage, variance reports, and accounting data for better cost control.

What Are Manufacturing Costs?

Manufacturing costs are the total costs involved in turning raw materials into finished products. They usually include direct materials, direct labour, and manufacturing overhead.

These costs sit at the centre of product costing because they show how much a business spends to make goods. Therefore, manufacturers use them to set prices, measure margins, and review production efficiency.

A manufacturer should separate production-related costs from selling or administrative expenses. For example, factory electricity may count as manufacturing overhead, while sales team salaries usually do not.

Why Manufacturing Costs Matter for Australian Manufacturers

Manufacturing costs affect pricing, profitability, cash flow, and operational planning. If a business underestimates production costs, it may sell products at margins that look profitable but fail to cover real expenses.

Australian manufacturers also face local pressures such as wage obligations, supplier lead times, freight distances, and energy costs. As a result, cost visibility helps managers respond faster when input prices change.

Accurate manufacturing cost data also supports better decisions across procurement, inventory, and production scheduling. For example, managers can compare supplier prices, detect waste, and adjust batch sizes before costs escalate.

Types of Manufacturing Costs

Manufacturing costs fall into several categories. Understanding each type helps businesses calculate total production cost more accurately and identify where savings are possible.

1. Direct materials

Direct materials are the raw materials and components used to make a finished product. Examples include timber for furniture, steel for machinery, fabric for clothing, or ingredients for packaged food.

These costs usually change with production volume. If a business produces more units, it normally needs more materials.

2. Direct labour

Direct labour covers wages and related labour costs for workers directly involved in production. This may include machine operators, assembly staff, production technicians, and factory workers.

Direct labour matters because it shows how much human effort goes into each product. Therefore, manufacturers often track labour hours by work order, production line, or batch.

3. Manufacturing overhead costs

Manufacturing overhead includes factory costs that support production but cannot be traced easily to one unit. Examples include factory rent, equipment depreciation, maintenance, quality control, and production supervisor salaries.

Overhead costs need careful allocation because they affect product costing. If overhead is assigned poorly, some products may look cheaper or more expensive than they really are.

4. Fixed manufacturing costs

Fixed manufacturing costs stay relatively stable within a certain production range. These may include factory rent, insurance, equipment leases, and salaried production management.

Fixed costs do not disappear when production slows. Therefore, lower output can increase the cost per unit because the same fixed cost spreads across fewer products.

5. Variable manufacturing costs

Variable manufacturing costs rise or fall with production volume. Direct materials, packaging, power usage, and hourly labour can all behave as variable costs.

Tracking variable costs helps manufacturers understand how production changes affect margins. It also helps teams calculate break-even points and review pricing.

Production Cost vs Manufacturing Cost

Production cost and manufacturing cost are often used together, but businesses should understand the difference. Manufacturing cost usually refers to the direct and overhead costs needed to make physical goods.

Production cost can sometimes include a wider set of costs depending on the industry and reporting context. For example, some businesses may use production cost to include planning, quality checks, packaging, or other production-related activities.

In manufacturing accounting, the safest approach is to define cost categories clearly. This helps finance, operations, and management teams use the same numbers when reviewing product profitability.

Total Manufacturing Cost Formula

The total manufacturing cost formula combines the three main cost categories used to make goods. This formula helps businesses calculate production spending before inventory movements and finished goods adjustments.

Direct materials cost

Direct materials cost includes the raw materials used during production. A business usually calculates this by reviewing beginning raw materials, purchases, and ending raw materials.

This calculation helps manufacturers avoid counting unused inventory as a production cost. As a result, cost reports reflect materials actually consumed.

Direct labour cost

Direct labour cost includes wages and related costs for staff who work directly on production. Businesses may calculate it using labour hours multiplied by hourly rates.

Manufacturers should track labour by job, product, or production line where possible. This makes labour efficiency easier to review.

Manufacturing overhead cost

Manufacturing overhead includes indirect production costs such as factory utilities, maintenance, depreciation, and quality control. These costs often need allocation across products or work orders.

A business may allocate overhead using labour hours, machine hours, or another relevant cost driver. The method should reflect how production actually consumes resources.

How to Calculate Manufacturing Costs

Calculating manufacturing costs requires clean operational spending records from procurement, inventory, payroll, and production. The process below helps businesses build a practical and repeatable calculation.

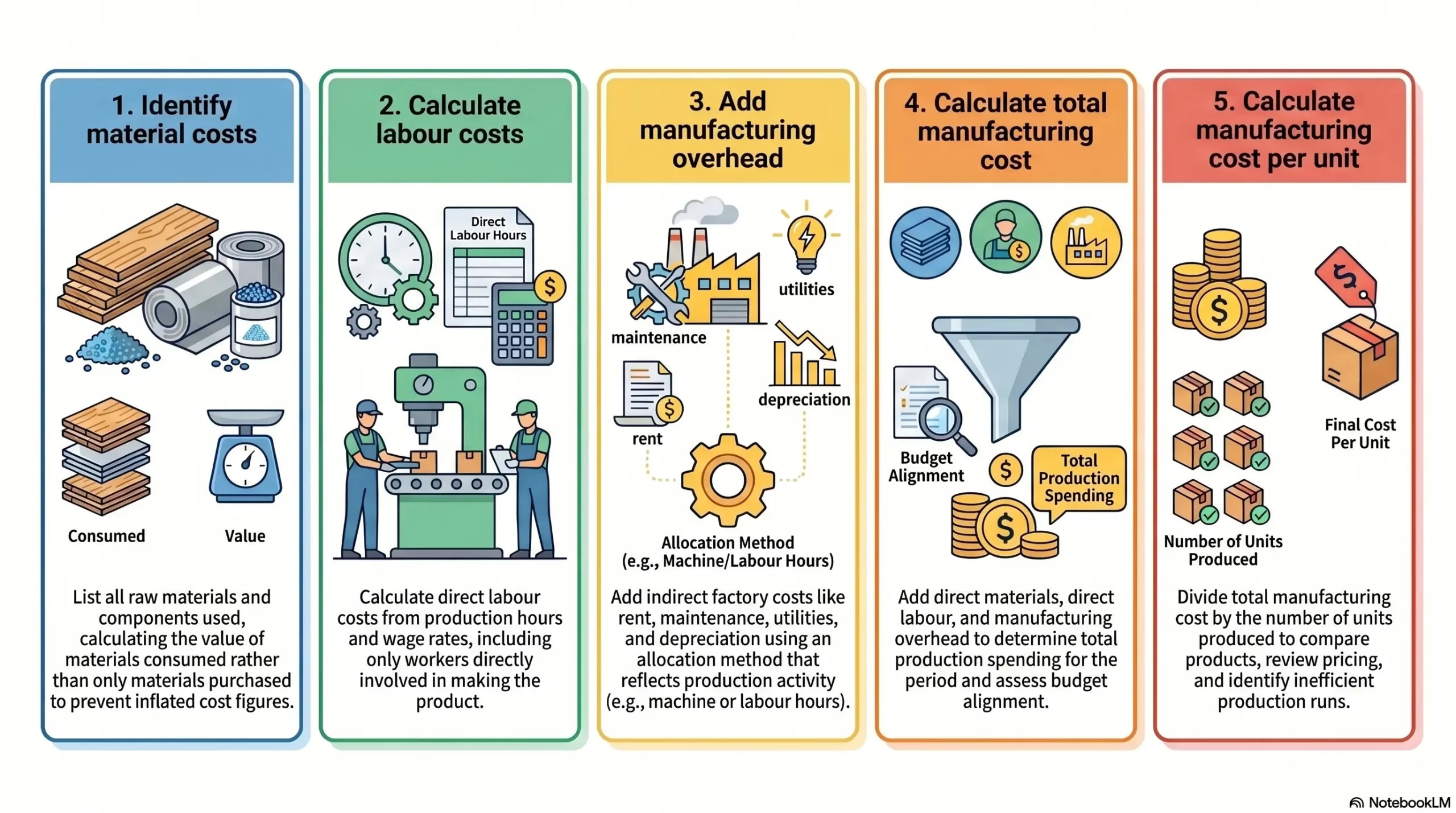

1. Identify material costs

Start by listing all raw materials and components used during the production period. Then, calculate the value of materials consumed rather than only materials purchased.

This distinction matters because inventory may remain unused at the end of the period. Accurate material costing helps prevent inflated production cost figures.

2. Calculate labour costs

Next, calculate direct labour costs from production hours and wage rates. Include only workers directly involved in making the product.

If staff work across several products, allocate their time based on work orders, timesheets, or production routing. This helps each product carry a fair share of labour cost.

3. Add manufacturing overhead

After direct costs are calculated, add manufacturing overhead. This includes indirect factory costs such as rent, maintenance, utilities, depreciation, and production supervision.

Choose an allocation method that reflects production activity. For example, machine-heavy factories may use machine hours, while labour-heavy production may use labour hours.

4. Calculate total manufacturing cost

Add direct materials, direct labour, and manufacturing overhead to calculate total manufacturing cost. This figure shows total production spending for the period.

This total helps managers assess whether production costs align with budgets. It also supports pricing and margin reviews.

5. Calculate manufacturing cost per unit

To calculate manufacturing cost per unit, divide total manufacturing cost by the number of units produced. This gives a clearer view of product-level cost.

Cost per unit helps manufacturers compare products, review pricing, and identify inefficient production runs. However, businesses should update the calculation when volumes or input costs change.

Manufacturing Cost Example

A furniture manufacturer produces 1,000 chairs in one month. During that month, the business uses $35,000 in timber, screws, fabric, and other direct materials.

The business also records $22,000 in direct labour and $18,000 in manufacturing overhead. These overheads include factory rent, machine maintenance, electricity, and production supervision.

If the factory produces 1,000 chairs, the manufacturing cost per unit is $75. This means the business spends $75 to make each chair before selling, distribution, and administrative costs.

Manufacturing Costs vs COGS vs COGM

Manufacturing costs, cost of goods manufactured, and cost of goods sold are connected but not identical. Each figure answers a different accounting question.

Total manufacturing cost

Total manufacturing cost measures the cost of production inputs during a period. It includes direct materials, direct labour, and manufacturing overhead.

This figure does not automatically show how much finished inventory was completed or sold. It only shows the cost incurred to support production activity.

Cost of goods manufactured

Cost of goods manufactured shows the total cost of goods completed during a period. It adjusts total manufacturing cost for changes in work-in-progress inventory.

COGM helps manufacturers understand the cost of completed goods moved into finished inventory. Therefore, it links production activity with inventory accounting.

Cost of goods sold

Cost of goods sold measures the cost of products sold to customers during a period. It adjusts finished goods inventory for goods available and goods remaining at the end.

COGS appears on the income statement and affects gross profit. As a result, accurate manufacturing cost data flows directly into financial performance reporting.

| Aspect |

Total Manufacturing Cost |

COGM |

COGS |

| Meaning |

Total cost incurred to support production during a period. | Total cost of goods completed and moved into finished inventory. | Total cost of goods sold to customers during a period. |

| Main focus |

Production inputs. | Completed goods. | Sold goods. |

| Includes |

Direct materials, direct labour, and manufacturing overhead. | Total manufacturing cost adjusted for work-in-progress inventory. | COGM adjusted for beginning and ending finished goods inventory. |

| Used for |

Tracking production spending and cost control. | Measuring the cost of finished goods produced. | Calculating gross profit on the income statement. |

| Formula |

Direct Materials + Direct Labour + Manufacturing Overhead | Beginning WIP + Total Manufacturing Cost – Ending WIP | Beginning Finished Goods + COGM – Ending Finished Goods |

How to Control Manufacturing Costs

Cost control works best when manufacturers track the cause of cost increases, not only the final number. The methods below help businesses reduce waste, improve planning, and protect margins.

Improve material planning

Better material planning helps manufacturers buy the right quantity at the right time. This reduces emergency purchases, stockouts, and excess inventory.

Demand forecasts, bill of materials data, and supplier lead times should guide purchasing decisions. As a result, production teams can avoid delays and unnecessary carrying costs.

Reduce waste and rework

Waste and rework increase material, labour, and overhead costs without adding value. Manufacturers should track defects, scrap, and repeated production errors by product or work order.

Quality checks, staff training, and clearer work instructions can reduce avoidable waste. Over time, small improvements can create meaningful cost savings.

Monitor labour efficiency

Labour efficiency shows how well production teams use time during manufacturing. Businesses can compare planned labour hours with actual labour hours to find gaps.

If actual hours exceed the standard, managers should review causes such as machine downtime, unclear instructions, or poor scheduling. This helps the business improve productivity without relying only on headcount cuts.

Review supplier and purchasing costs

Supplier prices can affect manufacturing margins quickly. Businesses should review supplier terms, freight charges, minimum order quantities, and price changes regularly.

A structured purchasing process gives manufacturers stronger cost control. For example, approved supplier lists and purchase order workflows reduce unplanned spending.

Track overhead by production activity

Manufacturing overhead often hides cost problems because it includes many indirect expenses. Businesses should allocate overhead based on real production drivers where possible.

Machine hours, labour hours, or production runs can help assign overhead more fairly. This gives managers a clearer view of which products consume the most factory resources.

Use accurate production data

Cost control depends on reliable data from inventory, production, and accounting systems. Inaccurate stock counts, missing labour records, or delayed overhead entries can distort product costs.

Manufacturers should use real-time production data where possible. This helps teams make faster decisions when costs move away from budget.

How Manufacturing Software Helps Track Costs

A factory operations platform helps businesses connect production activity with inventory, labour, overhead, and accounting data. It reduces manual work and gives managers clearer cost visibility.

Bill of materials cost tracking

A bill of materials lists the materials and components needed to make a product. Manufacturing software uses BOM data to calculate expected material costs before production starts.

When supplier prices change, the system can update product cost estimates. This helps businesses adjust pricing or purchasing decisions faster.

Work order and routing visibility

Work orders show what needs to be produced, while routing shows the production process. Together, they help manufacturers track labour, machine time, and production progress.

Software for production control can compare planned production activity with actual results. This makes it easier to find delays, bottlenecks, and cost overruns.

Inventory and material usage tracking

Material consumption tracking follows raw materials as they move from inventory into production. This reduces the risk of missing stock, double entry, or inaccurate material usage.

Accurate inventory tracking also supports better purchasing. Businesses can reorder based on actual consumption instead of estimates.

Production variance reporting

Variance reporting compares planned costs with actual costs. It helps manufacturers identify whether cost differences came from materials, labour, overhead, or production inefficiency.

For example, a material variance may show supplier price increases or excess scrap. A labour variance may point to downtime, training gaps, or slower production.

Accounting and inventory integration

An integrated production framework connects production data with accounting and inventory records. This helps finance teams calculate COGM, COGS, margins, and inventory values more accurately.

Integration also reduces manual reconciliation. As a result, managers can review production costs without waiting for spreadsheets to be updated.

Conclusion

Manufacturing costs show how much a business spends to turn raw materials into finished goods. By tracking direct materials, direct labour, and manufacturing overhead, Australian manufacturers can price products better, protect margins, and improve production decisions.

Strong cost control depends on accurate production data, reliable inventory records, and clear reporting across the factory and finance team. To track manufacturing costs more accurately and improve profitability, consult the experts from our team today.

Frequently Asked Question

Manufacturing costs are the expenses involved in producing finished goods. They usually include direct materials, direct labour, and manufacturing overhead.

Manufacturing overhead includes indirect factory costs that support production. Examples include factory rent, utilities, maintenance, equipment depreciation, quality control, and production supervision.

The formula is direct materials plus direct labour plus manufacturing overhead. This calculation shows the total cost incurred to produce goods during a period.

Manufacturing cost usually refers to the direct and overhead costs used to make physical goods. Production cost can sometimes cover a broader set of production-related expenses, depending on the business context.

Manufacturers can reduce costs by improving material planning, reducing waste, monitoring labour efficiency, reviewing supplier costs, tracking overhead, and using accurate production data.