Direct procurement is the process of sourcing and managing materials, components, and sub-assemblies that physically become part of a finished product. It is the supply-side engine that keeps margins intact.

Australian manufacturers rely heavily on imported direct materials. Import duty exposure, AUD exchange rate movements, and commodity price cycles make direct spend management a critical competitive capability.

This article covers the direct procurement process, how it differs from indirect purchasing, the metrics that matter, and how Australian businesses across manufacturing, food production, and resources manage direct spend.

Key Takeaways

Direct procurement is the end-to-end process of sourcing raw materials, components, and services that are parts of the finished product and directly traceable to COGS.

Indirect procurement differs from direct procurement in financial classification, supplier strategy, and performance measurement.

The direct procurement process runs from demand planning and supplier qualification through purchase order creation, goods receipt, quality inspection, and invoice reconciliation.

Best practices for direct procurement include centralising supplier data, aligning purchasing with production planning, and using ERP to automate the purchase-to-pay cycle and reduce transaction errors.

What is Direct Procurement?

Direct procurement is the end-to-end process of sourcing, purchasing, and managing the raw materials, components, and sub-assemblies that are physically incorporated into a finished product.

Because these inputs become part of what the business sells, direct procurement is directly linked to the cost of goods sold, production continuity, and the gross margin of every product manufactured.

A failure in direct procurement, whether a delayed shipment, a substandard batch, or a supplier collapse, can halt an entire production line, idle labour, and cause missed commitments to customers.

Teams managing this function must combine commercial negotiation with a deep understanding of engineering specifications, quality standards, and the production schedules they are supporting.

It is an industry standard in the current business landscape to use a reliable procurement management platform to support this function with minimal risk and optimal operations.

"Direct procurement is where your cost of goods is set. Every sourcing decision at this level flows directly into product cost, margin, and your ability to compete on price."

Direct vs Indirect Procurement

| Dimension | Direct Procurement | Indirect Procurement |

|---|---|---|

| Definition | Purchasing materials that are physically incorporated into the finished product | Purchasing goods and services that support operations but do not become part of the product |

| COGS impact | Direct — every cent flows into the cost of goods sold | Classified as operating expense (OPEX), not COGS |

| Supplier relationships | Long-term and strategic — few suppliers, high interdependency | Transactional or preferred — broader base, lower individual dependency |

| Purchase frequency | Regular, scheduled by MRP or production planning | Ad hoc or periodic, driven by operational need |

| Key metrics | PPV, on-time delivery, incoming quality rate, supplier concentration | Cost avoidance, contract compliance, and catalogue adoption rate |

| Ownership | Procurement, supply chain, and production planning — cross-functional | Requesting department or centralised procurement team |

| Example categories | Raw materials, components, sub-assemblies, contract manufacturing | Office supplies, IT equipment, travel, facilities management, marketing services |

The distinction between direct and indirect procurement determines how purchases are accounted for, how suppliers are managed, and which performance metrics apply to each function.

1. Key differences in purpose and financial impact

Direct procurement acquires the inputs that form the finished product. Indirect procurement acquires goods and services that keep the business operational, such as IT systems, facilities, and professional services.

In manufacturing businesses, direct spend typically accounts for 50 to 80 percent of total revenue. A one percent reduction in direct material costs can deliver a substantial improvement to gross margin.

Indirect spend is diffuse and often managed by department heads. Direct spend is concentrated, strategically managed, and tightly tied to production output and the cost of every unit manufactured.

2. How each affects the cost of goods sold vs operating expenses

Direct procurement expenditure flows into cost of goods sold (COGS). Materials purchased are recorded as inventory on the balance sheet and expensed only when the product is sold.

This means direct procurement determines gross profit margin. Every dollar saved on direct materials, or lost through inefficiency, flows directly to the gross profit line.

Indirect procurement is classified under operating expenses (OPEX). These costs are recognised in the period incurred and do not affect inventory valuation or the gross margin calculation.

Understanding this distinction matters because savings in direct spend are visible on the gross margin, while indirect savings improve operating margins further down the income statement.

3. Why treating both the same way backfires

Indirect procurement is typically managed through supplier catalogues, purchasing cards, and transactional vendor relationships. The goal is to minimise administrative burden and enforce policy compliance.

Applying this transactional model to direct procurement creates serious supply risk. Direct materials require formal supplier qualification, inbound quality controls, long-term contracts, and production integration.

Conversely, applying direct procurement rigour to every indirect purchase creates unnecessary bureaucracy and slows internal operations without delivering meaningful supply chain benefits.

What Are Direct Materials?

Direct materials are the physical inputs consumed during manufacturing that become part of the finished product. They vary by industry but are defined by two criteria: physical inclusion and cost traceability to each unit produced.

1. How direct materials are defined in cost accounting

In cost accounting, a material is classified as direct if it is physically incorporated into the final product and its cost can be economically traced to a specific unit of output.

For a furniture manufacturer, the hardwood used in a dining table is a direct material. The cost per unit can be precisely calculated from the volume of timber consumed in each table produced.

Direct material costs are combined with direct labour and manufacturing overhead to determine the standard cost of a product, which drives retail pricing decisions and profitability reporting.

2. Direct materials vs indirect materials

Indirect materials are used in the production environment but do not physically become part of the finished product, or their individual cost is too small to trace economically to a single unit.

In the furniture example, the sandpaper used to smooth timber, the lubricant for the machinery, and the safety equipment worn by operators are all indirect materials. They support production but are not in the product.

Small consumables like fasteners, adhesives, or cleaning agents may be treated as indirect materials when calculating the exact cost per unit creates more administrative burden than the data is worth.

Indirect materials are classified under Maintenance, Repair, and Operations (MRO) spend or manufacturing overhead, not direct material cost.

3. What is a Bill of Materials (BOM)?

The Bill of Materials (BOM) is the foundational document of direct procurement. It lists every raw material, sub-assembly, and component required to produce one unit of the finished product, with exact quantities.

When production schedules a manufacturing run, enterprise software performs a BOM explosion, calculating the total volume of every direct material required across the planned output.

Procurement cross-references BOM requirements against current inventory and open purchase orders to identify sourcing gaps. An inaccurate BOM produces incorrect purchase orders and production failures.

For complex products such as electronics or automotive components, a BOM can contain thousands of line items in a multi-level hierarchy, with parent assemblies and child sub-components listed separately.

The Direct Procurement Process

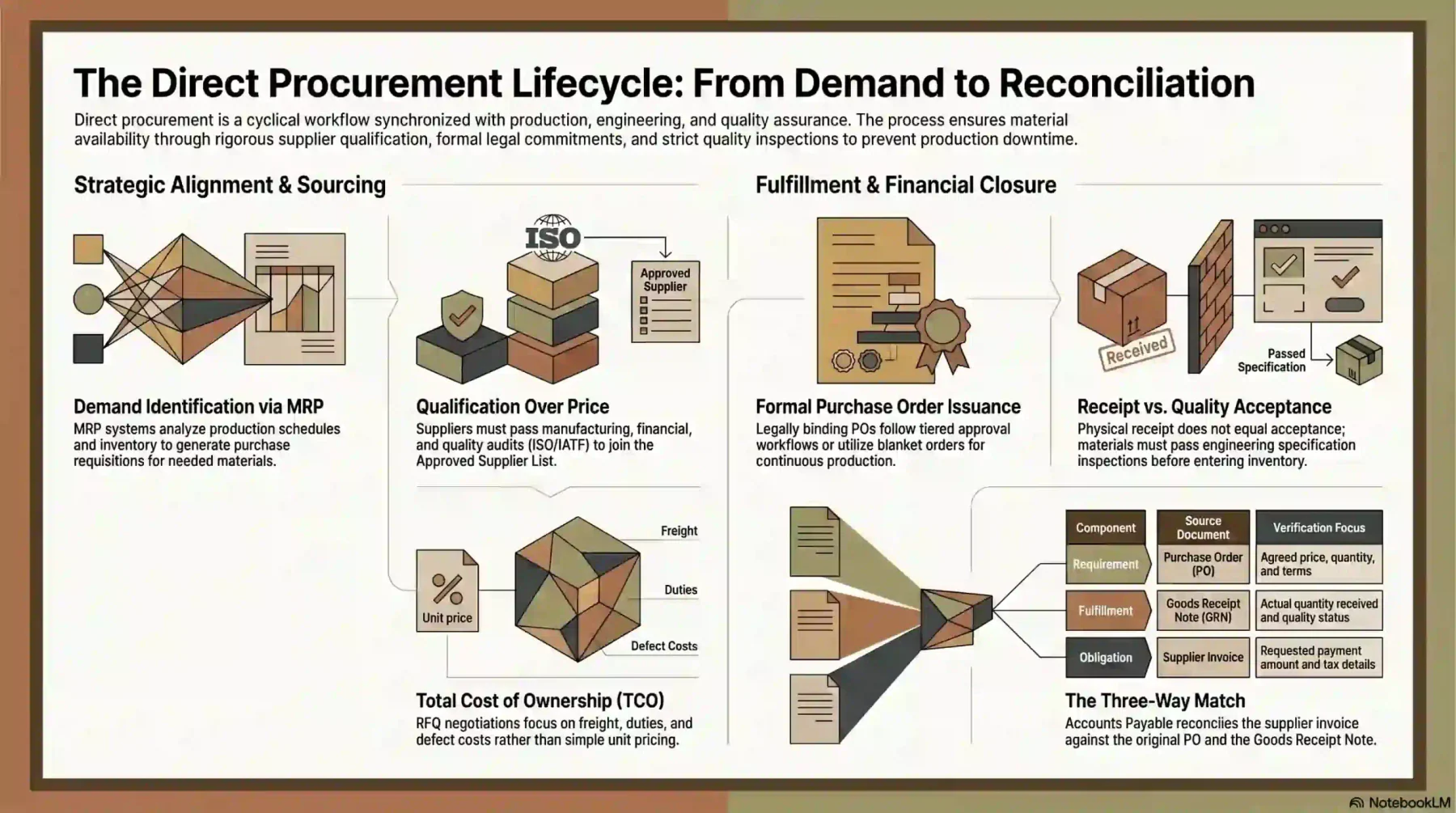

The direct procurement process is a structured, cyclical workflow that must stay synchronised with production planning, engineering, and quality assurance. Each step depends on the accuracy of the one before it.

1. Identify material requirements from the production schedule

The process begins in sales and operations planning. Production teams create a master production schedule based on confirmed orders and demand forecasts, which is processed by a Material Requirements Planning (MRP) system.

The MRP system analyses the BOM and current inventory levels to determine what materials are needed and when they must arrive. Using tools for streamlining raw material sourcing helps procurement teams turn these requirements into timely purchase requisitions and supplier actions.

Accuracy at this stage is critical. Flawed demand inputs produce either excess inventory that ties up working capital or material shortfalls that stop the production line.

2. Qualify and evaluate potential suppliers

Direct material suppliers are not selected on price alone. They must pass a formal qualification process assessing manufacturing capability, financial stability, quality management systems, and delivery reliability.

Quality certifications such as ISO 9001 are a baseline expectation. Regulated industries require additional compliance, such as GMP certification for pharmaceutical suppliers or IATF 16949 for automotive.

Suppliers who pass qualification are added to an Approved Supplier List (ASL). Only ASL-approved suppliers may receive purchase orders for direct materials, regardless of price or availability.

3. Issue RFQs and negotiate pricing terms

Once qualified suppliers are identified, the team issues a Request for Quotation (RFQ) specifying engineering tolerances, required volumes, delivery schedules, and quality acceptance criteria.

Negotiations focus on the total cost of ownership, not unit price alone. Freight costs, import duties, payment terms, minimum order quantities, and the financial cost of defects all affect true acquisition cost.

Long-term contracts with index-linked pricing are common for commodity-dependent direct materials. These protect both parties from price volatility while providing volume and scheduling certainty.

4. Raise and approve purchase orders

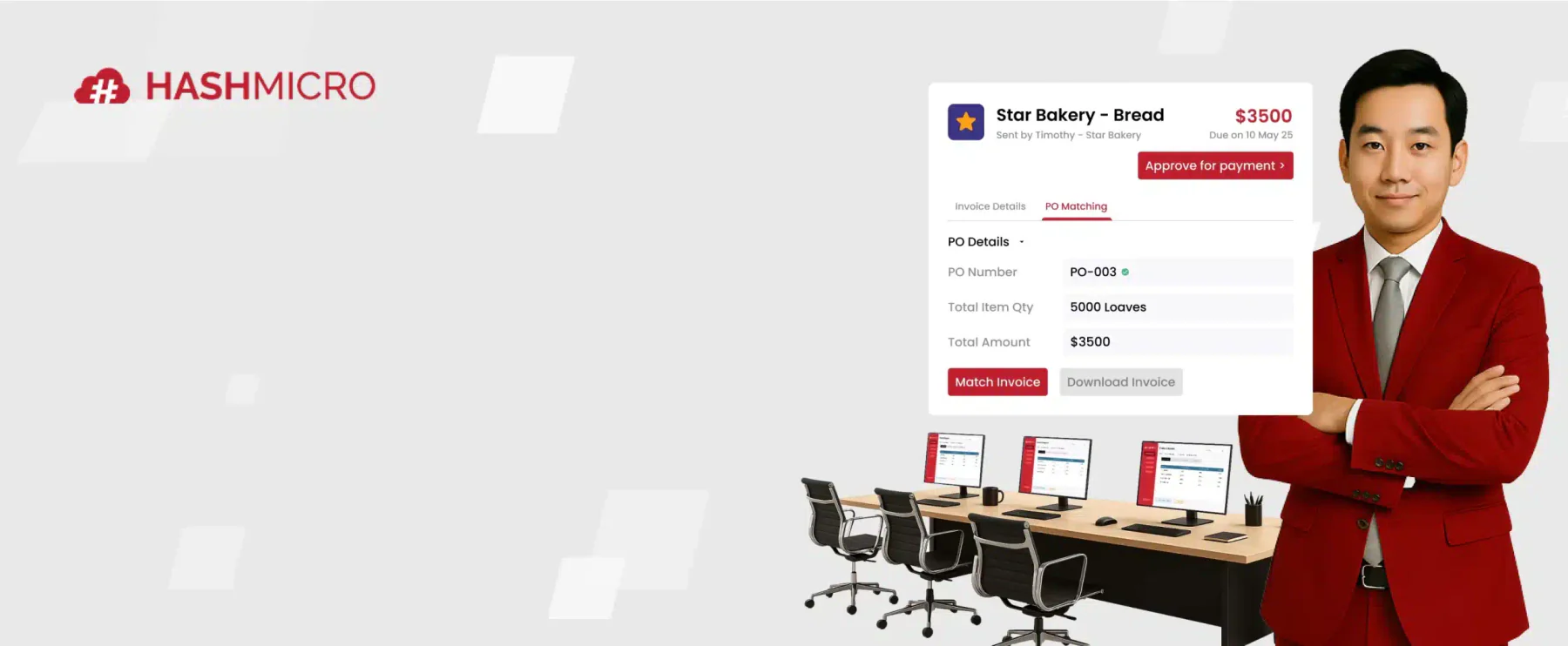

After finalising terms, a formal Purchase Order (PO) is raised. The PO is a legally binding document specifying the item, quantity, price, delivery date, and conditions of the transaction.

PO approval follows a tiered workflow based on spend value and the buyer’s authorisation limit. Higher-value orders escalate to senior approvers before the PO is released to the supplier.

In continuous production environments, blanket POs commit to a total annual volume. Specific delivery releases are triggered against the blanket as production schedules dictate each shipment.

5. Receive, inspect, and accept materials

When materials arrive, the receiving team logs the shipment and generates a Goods Receipt Note (GRN). Physical receipt does not constitute acceptance for direct materials.

Materials must pass inbound quality inspection before entering active inventory. Quality teams sample the goods and verify that they meet the engineering specifications stated in the PO.

Materials that fail inspection are quarantined, and a non-conformance is raised. The supplier must arrange replacements, rework, or credit. Production planning is used to manage schedule impact.

6. Reconcile invoices and close purchase orders

The accounts payable team performs a three-way match, comparing the supplier’s invoice against the original PO and the Goods Receipt Note. This process is essential for verifying supplier purchase details before payment is approved.

Discrepancies, whether a price variance or quantity mismatch, are escalated to procurement for investigation. Payment is only released once the discrepancy is formally closed.

Once payment is complete, the PO is closed in the system. Reconciliation data feeds directly into purchase price variance reporting, measuring how actual costs compare to approved standards.

Key Challenges in Direct Procurement

Direct procurement sits at the intersection of production planning, supplier risk, and cost management. Companies that treat it as a pure purchasing function tend to encounter the same avoidable disruptions repeatedly.

1. Supply continuity and production disruption risk

A disruption to a single critical material can halt production entirely, regardless of how well-managed the rest of the supply chain is.

Direct procurement’s most fundamental risk is the dependency between supplier performance and factory output. Building dual-source coverage for critical direct items is the primary mitigation.

2. Commodity price volatility and cost exposure

Raw material prices for steel, aluminium, plastics, and agricultural inputs move with global supply and demand.

A procurement team without a pricing strategy absorbs every commodity spike directly into the cost of goods sold. Digital sourcing solutions can help teams compare supplier options, track pricing trends, and respond faster to market volatility.

3. Supplier quality management and non-conformances

Non-conforming direct materials create a cascading effect: they delay production, inflate rework costs, and force emergency purchases at spot rates.

Quality failures in direct procurement are never contained to the quality department alone. Supplier quality agreements and incoming inspection protocols reduce the frequency and impact of non-conformances.

4. Lead time variability and inventory planning

Variable supplier lead times make it difficult to plan production schedules and safety stock levels with confidence.

When actual delivery times differ from quoted lead times, procurement teams are forced into reactive expediting. Tracking lead time variance by supplier and part number identifies where unreliability is concentrated.

5. Demand forecasting inaccuracies

Direct procurement is only as accurate as the demand signals it receives. When production forecasts overstate demand, teams carry excess direct material inventory that ties up working capital and risks obsolescence.

Understated demand creates the opposite problem: material shortages that stop production. Closer integration between sales, production planning, and procurement addresses persistent forecast inaccuracy.

Direct Procurement KPIs and Performance Metrics

Measuring direct procurement performance requires a mix of cost, quality, and delivery metrics. Tracking any one dimension in isolation gives an incomplete picture of how well the function is performing.

1. Purchase price variance (PPV)

Purchase price variance measures the difference between the standard cost of a direct material and the actual price paid in a given period.

A favourable PPV means the procurement team bought below the standard rate, improving gross margin. An unfavourable PPV signals overspend that flows directly into the cost of goods sold.

2. Supplier on-time delivery rate

On-time delivery rate measures the percentage of purchase orders fulfilled by the supplier-confirmed delivery date. A rate below 95% in manufacturing supply chains typically introduces measurable schedule disruption.

Track the metric at the line-item level, not the order level. A supplier who delivers 9 out of 10 lines on time may still cause a line stoppage if the missing item is on the critical path.

3. Incoming quality rate

Incoming quality rate measures the percentage of direct material receipts that pass inspection without defect, rework, or rejection.

A declining rate signals supplier process degradation before it escalates to a formal non-conformance. Tracking by supplier and part number allows quality issues to be caught before the production line.

4. Spend under management

Spend under management measures the proportion of total direct procurement spend that passes through formal sourcing, contract, and approval processes rather than being purchased outside the procurement function.

A low spend under management percentage indicates that a significant portion of direct spend is being placed through informal channels, which erodes contracted pricing and creates compliance exposure.

5. Supplier concentration ratio

Supplier concentration ratio measures the proportion of total direct spend attributable to the top 3 to 5 suppliers.

A high ratio flags dependency risk across critical direct categories. Many teams set a threshold ensuring no single supplier represents more than 30% of any critical direct spend.

Supplier Relationship Management in Direct Procurement

Direct procurement depends on a small number of high-impact suppliers. Managing those relationships proactively rather than reactively is what separates well-run procurement functions from reactive buying desks.

1. Tiered supplier classification

Not every direct supplier warrants the same management attention. A tiered model segments suppliers into strategic, preferred, and approved tiers based on spend volume, supply risk, and strategic importance.

Strategic-tier suppliers receive dedicated account management, joint development programs, and early involvement in new products. Approved-tier suppliers need only contract compliance management and periodic pricing reviews.

2. Joint business planning and performance reviews

Quarterly business reviews with strategic suppliers create a structured forum for discussing forecast visibility, capacity commitments, quality trends, and joint cost reduction targets. Strong strategic supplier planning helps manufacturers reduce supply risk and improve long-term procurement performance.

Companies that share forward-looking production forecasts with key direct suppliers consistently report shorter lead times and higher fill rates than those who purchase purely on spot demand.

Direct Procurement for Australian Manufacturers

Australian manufacturers source materials across domestic suppliers, Asia-Pacific partners, and global commodity markets. Each pathway carries different lead time, cost, and compliance implications.

1. Local sourcing vs imported materials

Domestic sourcing reduces lead times, eliminates import duties, and simplifies quality audits.

For direct materials where just-in-time delivery is critical, a local supplier at a higher unit price often delivers better total value than an offshore alternative when total landed cost is compared.

2. Free trade agreement leverage

Australia’s free trade agreements with China, Japan, South Korea, ASEAN nations, and the United States create preferential tariff rates on thousands of direct material categories.

Claiming those rates requires compliant certificates of origin and correct HS code classification.

According to the Australian Bureau of Statistics, manufacturing contributes significantly to Australia’s GDP, making FTA leverage a material competitive advantage for local producers.

Direct Procurement Across Industries in Australia

Direct procurement looks different across industries because the materials, supplier markets, and production dynamics differ. The underlying principles are consistent, but the operational details vary significantly.

1. Food and beverage manufacturing

For food and beverage producers, direct procurement covers agricultural inputs, packaging materials, and processing additives.

Seasonal supply variation, weather-driven shortages, and food safety compliance make forward contracting and alternative sourcing essential competencies in this sector.

2. Construction and engineering

Direct procurement in construction covers structural steel, concrete, timber, and specialist mechanical or electrical components.

Project-based demand makes blanket purchase agreements less practical than in manufacturing, so construction procurement teams rely more heavily on spot buying and subcontractor coordination.

3. Electronics and technology assembly

Electronics assembly depends on semiconductors, PCBs, connectors, and passive components sourced from global supply chains concentrated in Asia.

Lead times for electronic components can extend to 52 weeks during supply constraints. Australian assemblers with multi-source strategies and safety stock programs manage this risk more effectively.

Best Practices for Direct Procurement

The companies that consistently outperform on direct procurement costs and supply reliability share a common set of practices. They are not complex, but they require discipline to sustain.

1. Centralise supplier data and contracts

A single repository for supplier records, certificates, contracts, and performance data removes the version-control issues that affect procurement teams relying on shared drives and email threads.

Centralised data also enables spend analysis across all direct categories, which is a prerequisite for any meaningful commodity strategy or supplier consolidation initiative.

2. Align procurement with production planning

When procurement receives demand signals from production planning in real time, it can generate purchase orders at the right time rather than too early or too late.

The integration between MRP outputs and the purchase order process is where most ERP implementations deliver the clearest value for direct procurement teams.

3. Use ERP to automate the purchase-to-pay cycle

Manual purchase order creation, approval chasing, and invoice matching are the activities most likely to introduce delays, errors, and compliance gaps in direct procurement.

Automating these steps through an ERP system reduces cycle time, eliminates re-keying errors, and creates an auditable three-way matching record for every direct purchase.

A system for managing purchasing operations also keeps approvals, supplier data, and purchase records connected across the procurement cycle.

Conclusion

Direct procurement shapes product cost, production continuity, and supplier reliability more than any other purchasing function. Treating it strategically is what separates high-performing manufacturers from reactive ones.

For Australian manufacturers facing import lead time pressure, commodity volatility, and tightening margins, a structured approach to direct procurement is not optional.

To learn further regarding this topic, book a free consultation with our experts and learn deeper industry insight to improve your business.

FAQ

Direct procurement can be partially outsourced to a managed service provider who negotiates and manages supplier contracts on the buyer’s behalf. This model suits companies seeking volume-aggregated pricing in specific direct categories. The trade-off is reduced cost visibility and weaker direct supplier relationships, both of which become significant if the outsourced categories are strategically important to your product cost.

Incoterms 2020 rules define the point at which cost and risk transfer from the supplier to the buyer. For direct materials, the choice between EXW, FOB, or CIF directly affects what gets included in your landed material cost and where freight and insurance risk sit. Buyers using DDP (Delivered Duty Paid) transfer more cost to the supplier but lose visibility into freight and duty components, making it harder to benchmark true material costs across suppliers.

New product introduction (NPI) creates procurement demand before production volumes are confirmed, requiring buyers to qualify suppliers, negotiate prototype pricing, and set up part numbers without the leverage of a committed forecast. Early procurement involvement at the design stage allows engineers to treat sourcing risk and material lead times as design constraints rather than discovering them after the bill of materials is locked.

A standard purchase order is raised for a specific quantity at a specific price for a single delivery. A blanket purchase order establishes an agreed price and total volume over a defined period, with individual release orders drawn down against it. Blanket POs suit direct procurement better because they reduce transaction volume, lock in pricing for planning periods, and signal a committed volume the supplier can use to justify better rates.

Standard cost is calculated by taking the budgeted purchase price for the material plus estimated inbound freight, duty, and handling costs, then dividing by the standard yield rate expected from the production process. The resulting figure is used in product costing, gross margin calculations, and purchase price variance reporting. It is typically reviewed and reset at the start of each financial year or when market conditions shift materially.