Cost accounting helps businesses see what it really costs to produce goods, deliver services, complete projects, and run daily operations.

For Australian businesses, that visibility supports better pricing, tighter budgets, stronger margin control, and clearer decisions across departments.

This article explains what cost accounting means, how it works, which methods businesses use, and how it supports reporting, compliance, and profitability.

Key Takeaways

Cost accounting is the process of recording and allocating what each product, service, or project costs to run.

Cost accounting and compliance are linked because the ATO requires accurate expense records for BAS, tax returns, and audits.

How cost accounting works follows five steps: identify cost objects, collect data, classify costs, allocate overheads, and compare actuals against budgets.

Accounting software supports cost accounting by capturing purchasing, inventory, payroll, and sales data in one place.

What Is Cost Accounting?

Cost accounting is the process of recording, classifying, analysing, and allocating business costs. It shows how much a product, service, project, branch, or department costs to run.

Unlike financial accounting, cost accounting mainly supports internal decisions. It helps managers understand cost behaviour before they set prices, approve budgets, or adjust operations.

It covers direct costs, such as materials and labour, and indirect costs, such as rent, utilities, insurance, and administration. Together, these costs show the full operating picture.

Why Cost Accounting Matters for Australian Businesses

Cost accounting matters because revenue alone does not prove profitability. A business can sell more while still losing margin if labour, freight, materials, or overhead costs rise faster.

Australian businesses face cost pressure from wages, energy, inventory, logistics, and supplier changes. Cost accounting gives teams a practical way to monitor those movements.

The Australian Bureau of Statistics tracks business sales, wages, profits, and inventories. These indicators show why accurate cost visibility matters.

With reliable cost data, businesses can review pricing, compare branches, plan stock purchases, assess project margins, and decide whether expansion or hiring is financially sound.

Cost Accounting vs Financial Accounting

Both types of accounting use business data, but they serve different goals. Cost accounting explains operational detail, while financial accounting reports overall results.

| Feature | Cost accounting | Financial accounting |

| Primary audience | Managers and operations teams | Regulators, investors, lenders, and owners |

| Purpose | Cost control, pricing, planning, and margin analysis | Reporting financial position and performance |

| Time focus | Current costs, future budgets, and expected performance | Historical results for a reporting period |

| Format | Internal reports, cost sheets, dashboards, and variance reports | Profit and loss, balance sheet, and cash flow statement |

| Legal requirement | Not always mandatory, but highly useful | Required for many registered businesses |

Financial accounting shows whether the business made a profit. Cost accounting helps explain where that profit came from, where costs increased, and which areas need action.

Cost Accounting and Compliance in Australia

This form of accounting is not a formal legal requirement for most Australian businesses. Even so, detailed cost records support tax preparation, audit readiness, inventory valuation, and reporting.

1. Supporting accurate financial records

The Australian Taxation Office expects businesses to keep records that reflect income and expenses accurately. Cost accounting helps keep direct and indirect costs clear and traceable.

Clean cost records make it easier to prepare business activity statements, tax returns, management reports, and end-of-financial-year summaries with fewer manual adjustments.

2. Tracking costs for tax and reporting purposes

Businesses that hold inventory, manufacture goods, or manage long projects often need to track cost of goods sold, work in progress, and overhead allocation.

These figures affect taxable income and reported profit. A consistent costing system reduces guesswork and helps teams meet Australian tax compliance requirements when explaining how key figures were calculated.

3. Preparing for audits and business reviews

Structured cost data helps when a business faces an ATO review, investor due diligence, bank assessment, or internal performance review.

Records by product, project, branch, or department make it easier to support reported figures and answer questions about spending, margins, and cost allocation.

4. Keeping cost data consistent across departments

Businesses with several branches, departments, or project teams need consistent cost categories. Without them, reports become hard to compare, and decisions become less reliable.

Cost accounting creates common rules for classifying materials, labour, overheads, and project expenses, so managers compare results on the same basis.

Types of Costs in Cost Accounting

Cost accounting groups costs by behaviour and business use. These categories help managers understand what changes with activity, what stays stable, and what needs allocation.

1. Fixed costs

Fixed costs stay broadly the same over a period, even when sales or production volume changes. Examples include rent, annual insurance, equipment leases, and salaried staff wages.

These costs matter because the business must cover them before profit improves. Higher volume can spread fixed costs across more units and reduce the cost per unit.

2. Variable costs

Variable costs move with production or sales volume. Raw materials, packaging, freight per unit, hourly production labour, and sales commissions are common examples.

Tracking variable costs helps businesses measure contribution margin, set minimum pricing, and understand how increased sales affect total cost.

3. Direct costs

Direct costs can be traced to a specific product, service, job, or project. Examples include project labour, materials for a customer order, or freight for one shipment.

These costs give managers a clearer view of unit, job, or project profitability because they do not need broad estimation to assign them.

4. Indirect costs

Indirect costs support the business but cannot be linked to one output without allocation. Examples include shared utilities, management wages, software, and facility maintenance.

Businesses need a fair allocation method for indirect costs, or they risk overstating profit in some areas and understating it in others.

5. Overhead costs

Overhead costs are indirect costs tied to running production or service operations. They may include factory rent, machine depreciation, maintenance, office space, or support tools.

Overhead visibility is important because these costs often grow quietly. If businesses ignore them, product and project margins can look healthier than they really are.

Common Costing Methods

Different businesses use different costing methods because they produce, sell, and deliver work in different ways. The right method depends on how costs are created and measured.

1. Job costing

Job costing tracks costs for a specific job, order, project, or client engagement. It suits construction, trades, custom manufacturing, agencies, and professional services.

Each job receives its own cost record for labour, materials, subcontractors, equipment, and allocated overhead. This helps compare quoted costs with actual costs.

2. Process costing

Process costing suits businesses that produce similar or identical goods in a continuous flow. Food processing, chemicals, printing, and bulk manufacturing often use this method.

Instead of tracking each unit separately, the business averages costs across units produced during a period. This gives a practical cost per unit for mass output.

3. Activity-based costing

Activity-based costing assigns overhead based on the activities that consume resources. Examples include machine hours, purchase orders, inspections, setups, or support tickets.

This method gives more accurate overhead allocation than one broad rate. It is useful when products or services use shared resources in very different ways.

4. Standard costing

Standard costing sets expected costs for materials, labour, and overhead before work begins. The business then compares actual costs with these standards.

Variance analysis shows where spending, efficiency, or usage differed from plan. Manufacturers and budget-heavy operations often use this method to monitor performance.

5. Marginal costing

Marginal costing separates variable costs from fixed costs. It focuses on how much each extra unit contributes towards fixed costs and profit.

This method supports short-term pricing, break-even analysis, and special order decisions. It helps managers judge whether extra sales improve contribution.

6. Absorption costing

Absorption costing includes direct materials, direct labour, variable overhead, and fixed production overhead in product cost.

Businesses often use it for inventory valuation and external reporting because it assigns full production cost to each unit, rather than variable cost only.

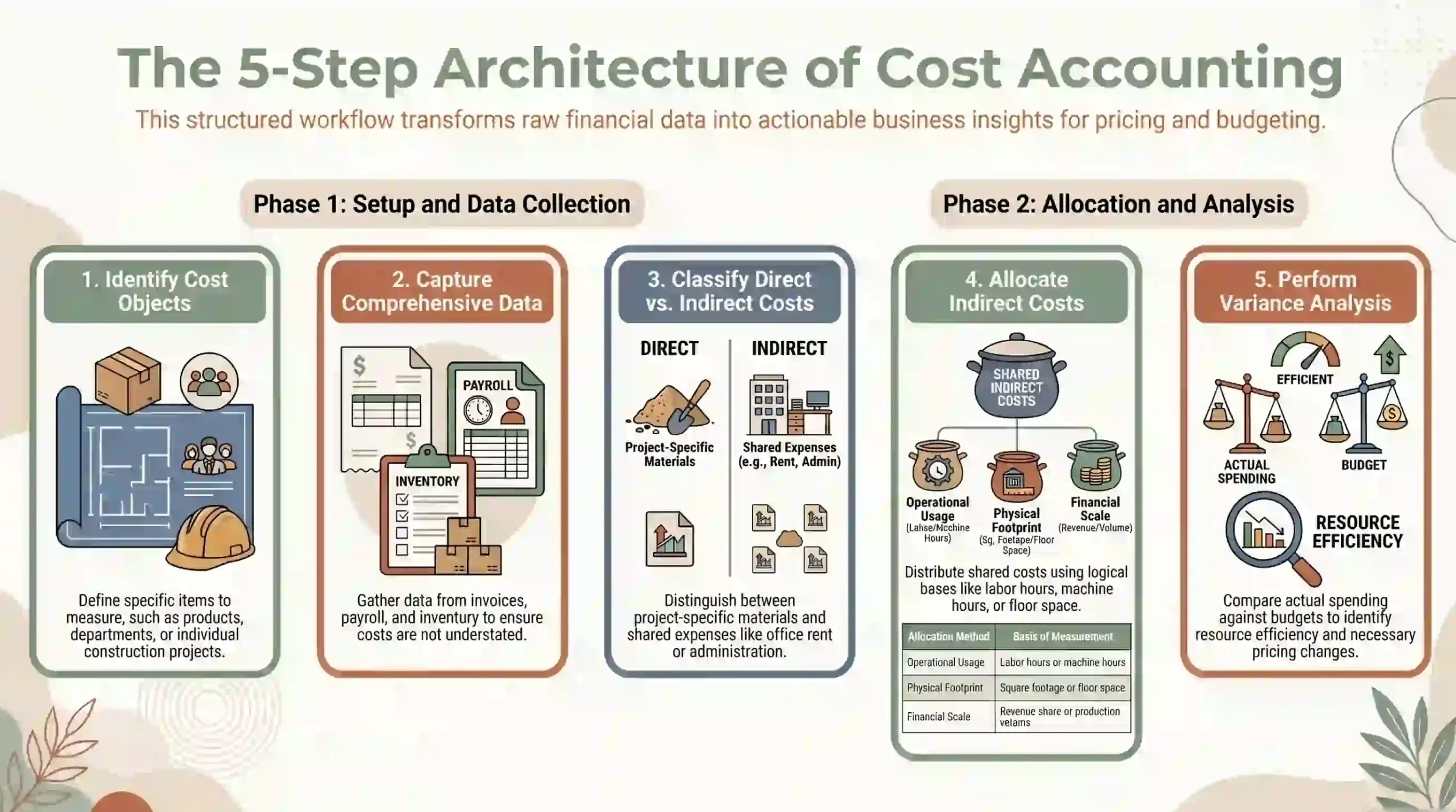

How Cost Accounting Works

Cost accounting works through structured financial workflows. Each step turns raw spending data into useful cost information for pricing, budgeting, and operational decisions.

1. Identify cost objects

A cost object is anything the business wants to measure separately. It may be a product, service, project, customer, department, branch, or production line.

Clear cost objects help teams decide how much detail the system needs. A construction firm may track each project, while a retailer may track each store or product category.

2. Collect cost data

The business collects data from invoices, payroll, supplier bills, inventory records, job sheets, timesheets, and production reports.

Reliable cost accounting depends on complete data capture. If staff miss expenses or record them late, reports will understate the true cost of work.

3. Classify direct and indirect costs

Each cost must be classified based on how it relates to the cost object. Materials used for one project are direct costs for that project.

Shared expenses, such as office rent or administration wages, are indirect costs. The business must allocate them using a consistent method.

4. Allocate costs to products, services, or projects

Indirect costs are allocated using a logical basis. Common methods include labour hours, machine hours, floor space, production volume, or revenue share.

The allocation method should reflect how the cost is consumed. Poor allocation can distort margins and lead managers to back the wrong products or projects.

5. Compare actual costs with expected costs

After costs are recorded and allocated, managers compare actual results with budgets, estimates, or standards.

This comparison highlights variances. It shows where costs rose, where teams used resources efficiently, and where pricing or process changes may be needed.

Cost Accounting Examples by Business Type

Cost accounting applies across many industries, but each business uses it differently. The main focus depends on how the business earns revenue and controls costs.

1. Retail businesses

A retailer may track cost of goods sold, freight-in, warehousing, store wages, rent, shrinkage, and supplier rebates.

This helps the business compare margins by store, product category, supplier, or sales channel. It can also reveal products that sell well but deliver weak profit.

2. Manufacturing businesses

Manufacturers track direct materials, direct labour, machine time, waste, rework, factory overhead, and production output.

Standard costing and absorption costing are common because they help measure efficiency, allocate overhead, and value inventory more consistently.

3. Service businesses

Service firms use cost accounting to track billable hours, staff costs, contractor fees, software, travel, and project expenses.

This helps firms see which clients, engagements, or service lines are profitable. It also supports better quoting for future work.

4. Project-based businesses

Construction companies, architects, engineers, and project managers often use job costing to track each project separately.

They compare estimated costs with actual labour, materials, subcontractor fees, equipment hire, and site expenses. This supports stronger tendering and margin control.

Benefits of Cost Accounting

A good cost accounting system gives managers practical insight. It turns everyday spending into decision-ready data for pricing, planning, control, and growth.

1. Better pricing decisions

Cost accounting helps businesses understand the full cost of selling a product or delivering a service.

With accurate cost data, managers can avoid selling below cost, test discount limits, and set prices that support both competitiveness and margin.

2. More accurate budgeting

Budgets become more reliable when they reflect actual cost behaviour. Fixed costs, variable costs, and overheads can be planned with better assumptions.

This helps finance teams build budgets that match business activity, rather than relying on broad estimates or last year’s figures alone.

3. Improved profit margin visibility

Cost accounting shows margin by product, project, branch, service line, or customer group. This detail is hard to see in high-level financial statements.

Managers can then focus on profitable areas, adjust weak-margin offerings, or stop work that consistently fails to cover its full cost.

4. Stronger cost control

Regular cost reports help teams spot overspending early. This may include material price changes, labour inefficiency, freight increases, or rising overhead.

Early visibility gives managers time to act before small cost issues become larger profit problems.

5. Better project and product profitability tracking

Businesses often run several projects, products, branches, or client accounts at once. Cost accounting gives each area its own financial view.

This helps managers assign resources, prioritise work, and make decisions based on actual profitability instead of overall revenue alone.

Common Cost Accounting Challenges

Cost accounting is useful, but it can be difficult to manage when data is scattered or teams use different methods.

Manual cost tracking often creates delays and errors. Spreadsheets may work at first, but they become harder to control as transactions, suppliers, and projects grow.

Inaccurate cost allocation can distort profitability. A single overhead rate may look simple, but it can misrepresent costs across very different products or services.

Poor overhead visibility makes indirect costs harder to manage. Rent, utilities, support tools, and administration costs can quietly reduce margins.

Disconnected inventory and accounting data can weaken cost reporting. If stock movements and accounting records do not align, COGS figures may become unreliable.

Weak actual-versus-budget comparison limits improvement. Without consistent data, managers cannot see whether cost issues came from price, volume, waste, or process gaps.

How Accounting Software Supports Cost Accounting

A financial management platform reduces the manual work behind cost accounting. It helps teams capture cost data from purchasing, inventory, production, payroll, and sales in one place.

With the right accounting support system, businesses can track direct costs, allocate overheads, compare budgets with actuals, and report costs by product, project, branch, or department.

Integrated software also supports cleaner records for tax preparation, end-of-financial-year reporting, inventory valuation, and internal reviews.

HashMicro delivers Australian financial solutions through an integrated ERP platform that connects finance, inventory, purchasing, production, and sales data.

This connection reduces duplicate entry and gives finance teams a clearer view of cost movement across the business. Managers can act faster when margins, budgets, or projects shift.

Conclusion

Cost accounting gives Australian businesses the visibility they need to understand what operations really cost.

It supports better pricing, stronger budgets, clearer margin analysis, and more disciplined cost control across products, services, projects, and departments.

To support you in cost accounting implementation, we offer you a free consultation with our experts that you can book anytime. Our insights extend to more than just accounting, so start today and grow your business.

Frequently Asked Questions

-

Is cost accounting required for Australian businesses?

Cost accounting is not a legal requirement for most Australian businesses. However, detailed cost records support tax preparation, inventory valuation, reporting, and audit readiness.

-

How does cost accounting support compliance in Australia?

Cost accounting supports compliance by keeping clear records of expenses, overheads, COGS, and project costs. These records can help during BAS preparation, tax returns, and reviews.

-

What is the difference between cost accounting and management accounting?

Cost accounting focuses on recording and analysing business costs. Management accounting is broader and also includes budgeting, forecasting, performance analysis, and planning.

-

Which costing method is best for small businesses?

Job costing often suits small service, trade, and project-based businesses. Product-based businesses may use marginal costing or simple absorption costing, depending on operations.

-

Can service businesses use cost accounting?

Yes. Service businesses use cost accounting to track staff time, project expenses, contractor costs, overheads, and profit by client, job, or engagement.