Ecommerce accounting helps online stores track sales, fees, GST, refunds, stock costs, and profit. It shows how much money the business actually keeps after each sale.

This is useful because ecommerce revenue does not always match bank deposits. Orders, payout deductions, platform fees, and refunds all need to be recorded before profit can be measured.

Key Takeaways

Ecommerce accounting records online store sales, expenses, tax, stock, fees, and cash flow.

Ecommerce accounting needs more detail because each sale can move through platforms, gateways, inventory, and tax records.

Businesses need to track costs, tax, inventory, fees, and payments to understand real profit.

Accounting software helps connect sales, costs, tax, and profit data in one system.

What Is Ecommerce Accounting?

Ecommerce accounting is the process of recording and reviewing the financial activity of an online store. It covers sales, expenses, tax, inventory, payment fees, and cash flow.

For example, AUD 10,000 in sales may become much lower profit after shipping, refunds, marketplace fees, GST, and cost of goods sold are included.

With accurate records, businesses can reconcile payouts, monitor margins, prepare BAS reports, and make better pricing or stock decisions.

Why Ecommerce Accounting Is Different from Traditional Accounting

Ecommerce accounting needs more detail because each sale can move through sales platforms, payment gateways, inventory records, and tax reports before reaching the bank.

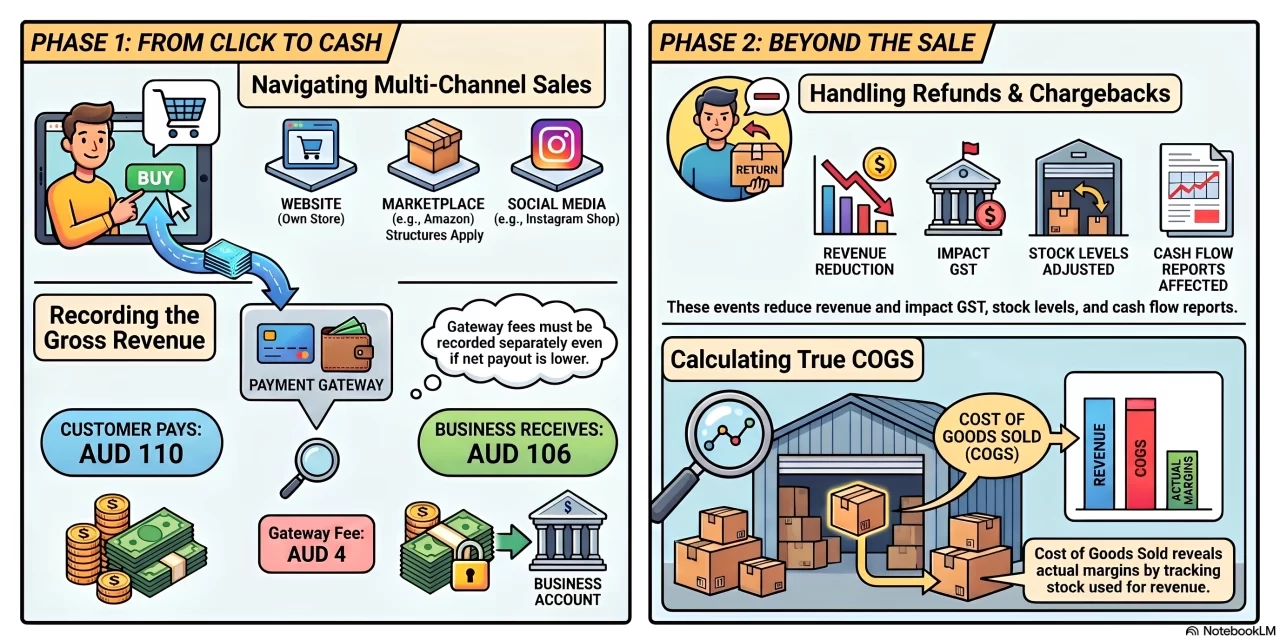

1. Multiple sales channels

Unified sales channels bring together websites, marketplaces, social media, and wholesale portals in one view. Each channel can have different fees, discounts, refunds, and payout dates.

2. Payment gateway fees

Payment gateways often deduct fees before sending funds. If a customer pays AUD 110 and the business receives AUD 106, the fee should still be recorded.

3. Refunds and chargebacks

Refunds, returns, and chargebacks reduce revenue and may affect GST, stock, and cash flow. Recording them separately keeps reports clearer.

4. Inventory and COGS tracking

Cost of goods sold (COGS) shows how much stock was used to earn revenue. Without it, sales may look profitable even when margins are low.

Ecommerce Accounting vs Ecommerce Bookkeeping

Ecommerce bookkeeping focuses on recording transactions. Ecommerce accounting uses those records to review profit, tax, cash flow, and business performance.

Most online stores need bookkeeping to keep records accurate, then accounting to understand what those records mean for growth and profit.

Key Components of Ecommerce Accounting

Ecommerce accounting includes more than sales records. Businesses need to track costs, tax, inventory, fees, and payments to understand real profit.

1. Sales and revenue tracking

Sales records should show where each order came from, how much was paid, and whether the amount includes GST, discounts, refunds, or shipping charges.

2. Cost of goods sold

Cost of goods sold (COGS) shows the direct cost of products sold. The basic formula is COGS = opening inventory + purchases – closing inventory.

3. Inventory accounting

Inventory accounting tracks stock value as products are bought, stored, sold, returned, or written off. This helps keep profit and stock reports accurate.

4. GST and BAS considerations

Australian financial solutions help businesses registered for GST record taxable sales, GST collected, GST credits, and BAS amounts correctly. This reduces errors during reporting periods.

5. Shipping, platform, and payment fees

Shipping costs, marketplace fees, subscription charges, and payment gateway fees should be recorded separately. These costs can reduce profit on each order.

6. Accounts payable and receivable

Tracking outgoing payments to suppliers sits alongside monitoring money owed by customers or sales channels. Both affect cash flow planning.

Accounting Methods for Ecommerce Businesses

Ecommerce businesses usually use cash accounting or accrual accounting. The right method depends on business size, inventory needs, reporting requirements, and growth plans.

Cash accounting can work for small stores with simple transactions. However, accrual accounting is usually better for growing ecommerce businesses because it gives a clearer view of inventory, unpaid bills, sales timing, and real profitability.

How to Do Ecommerce Accounting

Structured financial workflows keep sales, payouts, fees, stock, and tax records in one clear process. This helps reduce gaps between store data and financial reports.

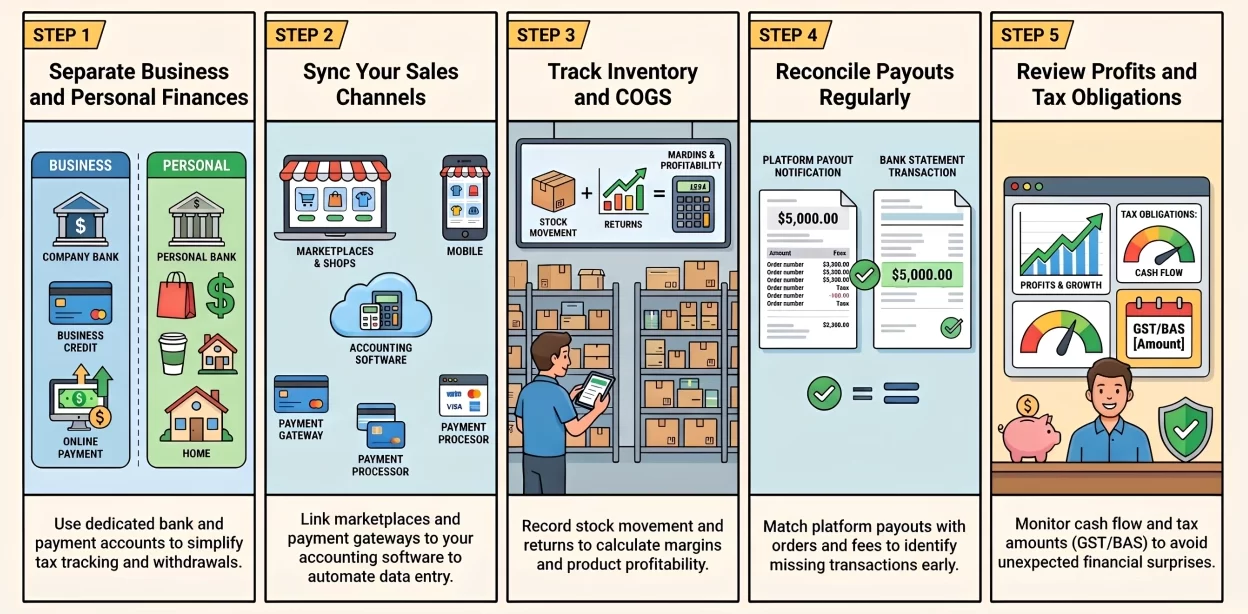

1. Separate business and personal finances

Use a dedicated business bank account and payment account. This makes sales, expenses, tax, and owner withdrawals easier to track.

2. Connect sales channels and payment gateways

Link ecommerce platforms, marketplaces, and payment gateways to the accounting system where possible. This reduces manual entry and keeps order data more consistent.

3. Track inventory and COGS

Record stock purchases, sales, returns, and closing inventory. This helps calculate COGS and shows whether products are generating enough margin.

4. Reconcile payouts regularly

Match platform payouts with orders, refunds, shipping charges, and fees. Regular reconciliation helps find missing transactions before reports are prepared.

5. Review profit, cash flow, and tax obligations

Check profit, GST, BAS amounts, supplier bills, and cash flow regularly. This helps businesses plan stock purchases, control costs, and avoid tax surprises.

Common Ecommerce Accounting Mistakes

Small accounting errors can quickly affect profit reports, GST records, and cash flow. These mistakes are common when sales data, payouts, fees, and inventory are handled separately.

- Recording full payouts as sales.

Bank deposits often already exclude fees, refunds, or platform deductions. Recording only the payout can make sales and costs inaccurate. - Ignoring payment gateway fees.

Gateway fees reduce the amount kept from each sale. If they are not tracked, profit can look higher than it really is. - Not tracking inventory costs.

Sales reports alone do not show how much stock was used. Without inventory costs, businesses cannot calculate accurate margins. - Mixing personal and business expenses.

Personal spending in business accounts can make reporting harder. It also creates extra work during tax and BAS preparation. - Delaying GST and BAS preparation

Waiting until the reporting deadline can lead to missing records and rushed checks. GST data should be reviewed throughout the period.

How Accounting Software Helps Ecommerce Businesses

Manual ecommerce accounting can become difficult when orders, payouts, fees, refunds, and inventory updates come from different platforms. Even small delays can create gaps between sales reports and bank records.

Integrated finance management connects these records in one system. It reduces manual entry and gives businesses a clearer view of sales, costs, tax, and profit.

- Sync sales, payments, and inventory data.

Connected data helps businesses match orders with stock movement, gateway payments, and platform deductions. - Automate reconciliation and reporting.

Automated records make it easier to compare payouts, fees, refunds, and bank deposits before reports are prepared. - Improve visibility over cash flow and profit.

Real-time financial data helps businesses see whether sales are producing enough margin after costs are included.

Conclusion

Ecommerce accounting helps online stores track sales, fees, GST, refunds, inventory costs, and profit more clearly. It gives businesses a better view of what each sale is really worth after costs are recorded.

By improving payout reconciliation, inventory tracking, and tax preparation, businesses can manage ecommerce finances with fewer reporting gaps.

If you’re looking to improve ecommerce financial management, you can consult our experts to see how accounting software can support your business.

Frequently Asked Question

Ecommerce accounting is the process of recording and reviewing sales, fees, GST, inventory costs, payments, cash flow, and profit for an online store.

Ecommerce accounting is important because sales totals do not always show real profit. Businesses need to track fees, refunds, shipping, GST, and stock costs to understand financial performance.

Cash accounting can suit small ecommerce stores, while accrual accounting is usually better for growing businesses that manage inventory, suppliers, and unpaid bills.

Ecommerce businesses track COGS by recording opening inventory, purchases, and closing inventory. The basic formula is COGS equals opening inventory plus purchases minus closing inventory.

Accounting software helps ecommerce businesses sync sales, payments, inventory, fees, and reports. This reduces manual work and improves visibility over profit and cash flow.