Current assets are short-term resources a business expects to convert into cash, sell, or use within 12 months. They appear on the balance sheet and reflect the short-term financial flexibility of the business.

A business may appear profitable on paper but still face cash pressure when too much value is locked in overdue receivables or slow-moving inventory. Current assets reveal the real short-term financial position.

This article explains what current assets are, how each category works, how to calculate the total, and why the figure matters for liquidity and working capital management.

Key Takeaways

Current assets are short-term resources, including cash, receivables, inventory, and prepaid expenses, that a business expects to use or convert into cash within 12 months.

Current assets are calculated by adding all qualifying short-term assets on the balance sheet, each confirmed as convertible within 12 months before inclusion.

Current assets matter for liquidity and working capital, helping managers spot funding pressure before it affects operations.

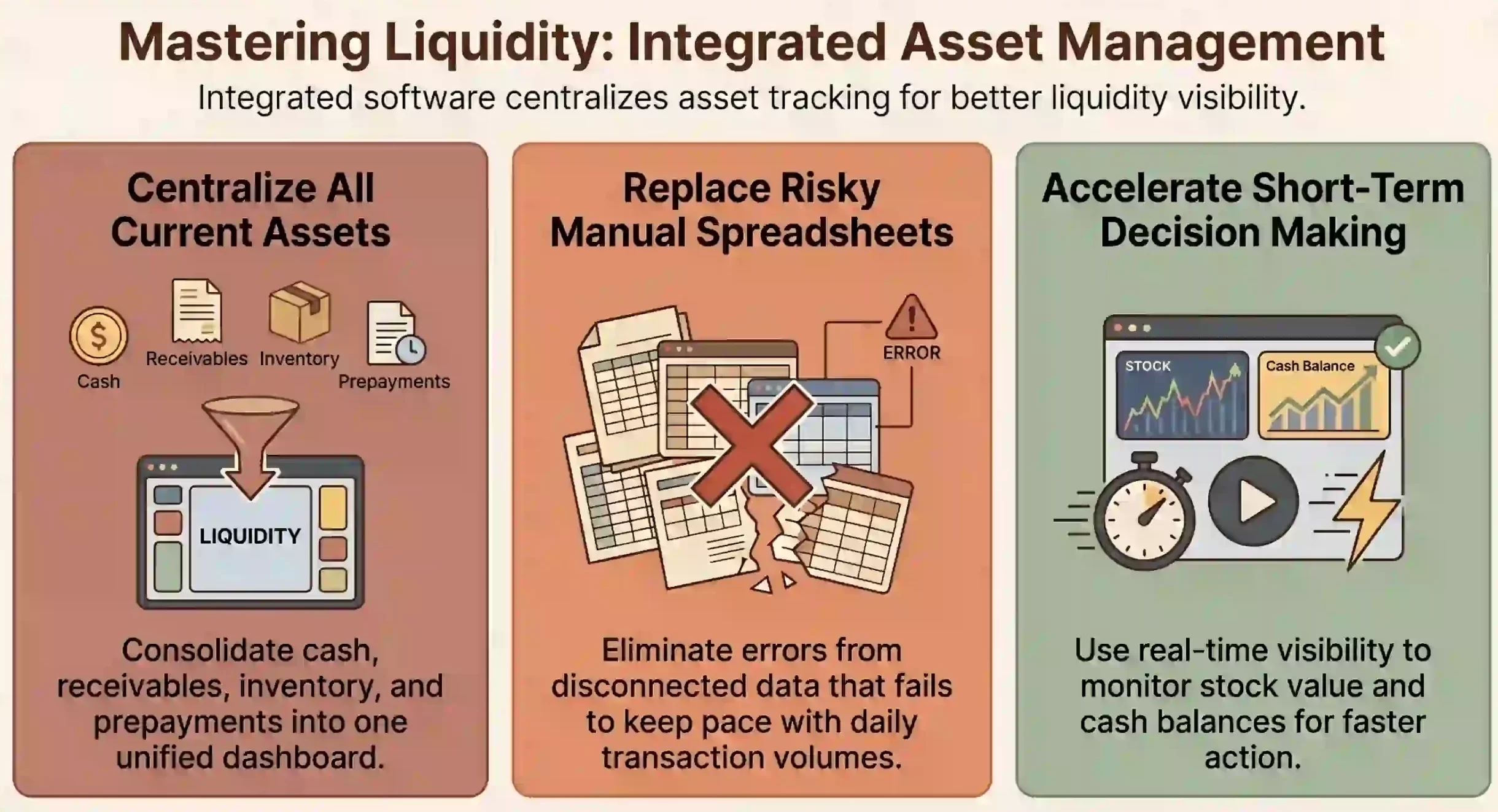

Accounting software centralises cash, receivables, inventory, and prepayments in one system, giving businesses clearer visibility over current assets.

What Are Current Assets?

Current assets are assets a business expects to convert into cash, sell, or use within one year or its operating cycle. They appear on the balance sheet and help assess short-term financial strength.

These assets support daily business needs. A business uses current assets to pay suppliers, meet wage obligations, purchase stock, settle tax liabilities, and cover recurring operating expenses.

Current assets differ from non-current assets such as property, machinery, and long-term investments. The business holds those for extended use and does not expect to convert them within the year.

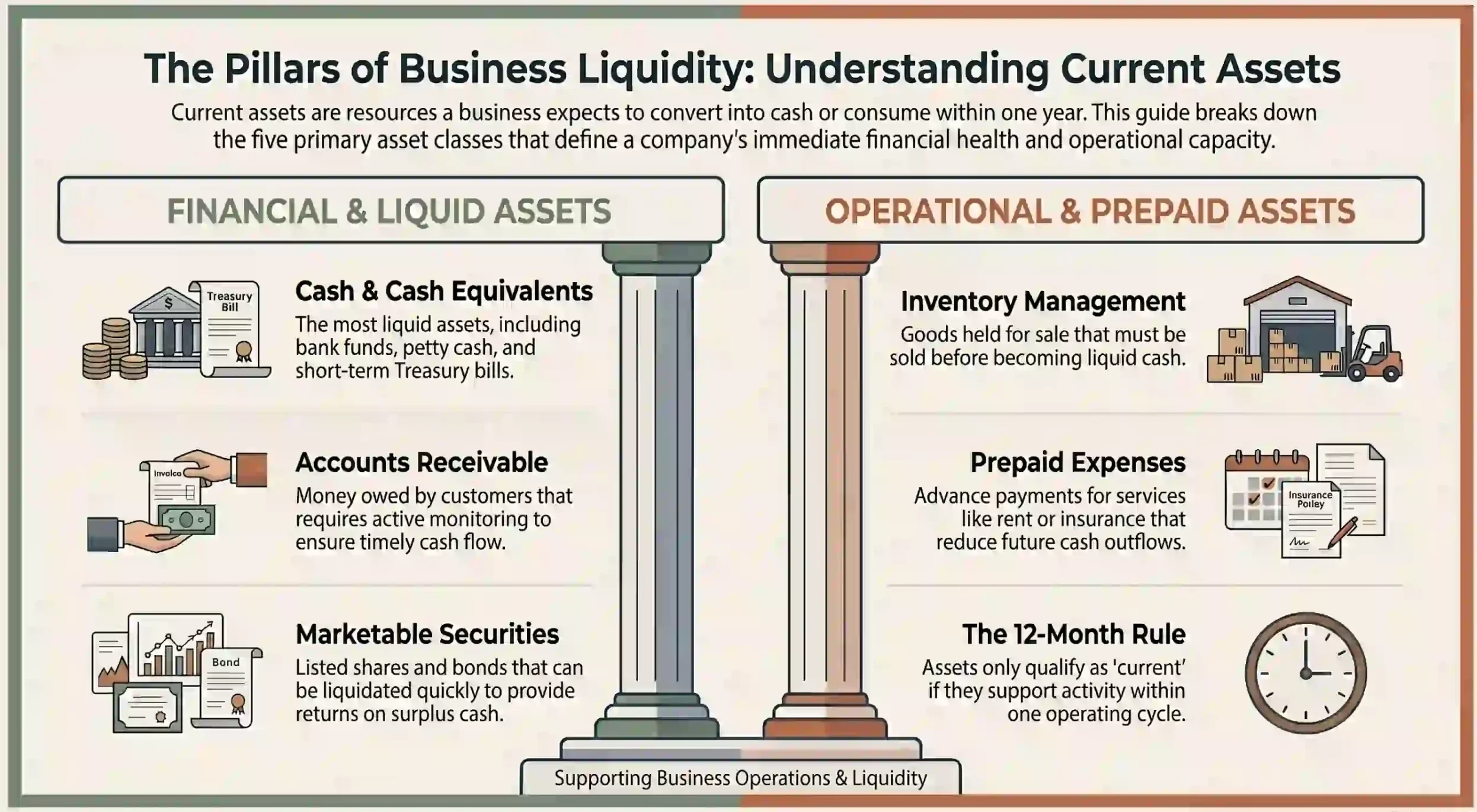

The operating cycle matters for classification. An asset may still qualify as current if it falls within the cycle, even when that cycle exceeds 12 months. The standard threshold is 12 months.

Current Assets List and Examples

Current assets vary by business type. A retailer holds more inventory, while a services firm relies more on receivables and cash. Each asset is expected to support short-term activity within the year.

1. Cash and cash equivalents

Cash is the most liquid current asset. It includes funds in business bank accounts, petty cash, and money available for immediate use.

Cash equivalents are short-term investments that convert into cash quickly with minimal value risk. Examples include Treasury bills, term deposits under three months, and money market instruments.

Businesses use cash and equivalents to pay suppliers, wages, rent, and other immediate obligations. Adequate cash balances reduce the need to borrow at short notice.

2. Accounts receivable

Accounts receivable is money owed to the business by customers for goods or services already delivered. It is classified as a current asset because payment is expected within normal credit terms.

Receivables need active monitoring. A business can show strong sales while still facing cash pressure if customers pay late. Ageing analysis helps flag overdue accounts before they affect cash flow.

Allowances for doubtful debts should be reviewed regularly. Receivables unlikely to be collected should not inflate the current assets figure on the balance sheet.

3. Inventory

Inventory includes goods held for sale, raw materials, and work in progress. It is classified as a current asset because the business expects to sell or use it within the operating cycle.

Inventory is less liquid than cash or receivables because it must be sold first. Slow-moving, obsolete, or damaged stock can reduce effective liquidity even when the balance sheet value looks high.

Businesses should review inventory regularly for write-downs. Carrying inflated inventory values overstates current assets and can mislead liquidity assessments.

4. Prepaid expenses

Prepaid expenses are costs paid in advance for goods or services the business will consume soon. Examples include prepaid rent, insurance premiums, software licences, and service contracts.

They qualify as current assets when the business expects to use the benefit within 12 months. Prepaid amounts do not convert into cash, but they reduce future outflows as payment is already made.

After the benefit is consumed, the prepaid amount is expensed on the income statement. Tracking prepayments accurately prevents double-counting in expense reporting.

5. Marketable securities and short-term investments

Marketable securities are financial assets that can be sold or converted into cash within a short period. They include listed shares, government bonds, and other instruments traded on active markets.

Short-term investments are classified as current assets when the business expects to liquidate them within 12 months. They offer a return on surplus cash while remaining accessible when needed.

The value of marketable securities can fluctuate with market conditions. Businesses should apply fair value measurement and review classifications if circumstances change.

Current Assets Formula

The current assets formula adds all short-term assets a business expects to convert into cash, sell, or use within 12 months. This total forms the basis for liquidity and working capital analysis.

Current assets = Cash + Cash equivalents + Accounts receivable + Inventory + Prepaid expenses + Short-term investments + Other current assets

The formula varies by business type and balance sheet structure. The key rule is classification: only assets that meet the definition of current assets should be included.

Other current assets may include GST credits receivable or tax refunds expected within the year. Any short-term amount the business is owed may qualify, depending on the balance sheet structure.

How to Calculate Current Assets

Calculating current assets involves three steps: identifying all short-term assets, confirming each qualifies as current, and adding the values. Each step matters for an accurate final figure.

-

List all short-term assets

Start by reviewing the balance sheet, bank records, receivables ledger, inventory reports, and prepaid expense accounts. List every item that could qualify as a current asset.

| Current Asset | Value |

| Cash | AUD 40,000 |

| Accounts receivable | AUD 25,000 |

| Inventory | AUD 60,000 |

| Prepaid expenses | AUD 8,000 |

| Short-term investments | AUD 12,000 |

Completeness matters at this stage. Missing a category, such as GST credits or short-term deposits, will understate the total current assets figure.

-

Confirm each asset can be converted within 12 months

Review each item and confirm it is expected to be collected, sold, consumed, or converted into cash within 12 months. Remove anything that does not meet this test.

For example, a term deposit maturing in 18 months is not a current asset. Inventory that has not moved for two years may need reclassification or write-down before inclusion.

-

Add the value of all current assets

Once all items are confirmed as current, add the values together. The result gives a total current assets figure the business can use for liquidity and working capital assessments.

Current assets = AUD 40,000 + AUD 25,000 + AUD 60,000 + AUD 8,000 + AUD 12,000

Current assets = AUD 145,000

Why Current Assets Matter for Business Liquidity

Current assets show how much short-term value a business can access to fund operations. They help leaders assess liquidity, working capital, and cash flow risk.

1. They help measure the ability to pay short-term obligations

Current assets help businesses pay suppliers, wages, tax obligations, rent, utilities, and loan instalments. They show whether short-term resources can cover near-term liabilities.

A higher current asset balance can improve financial flexibility. However, the quality of each asset matters because cash is more usable than overdue receivables or ageing stock.

2. They support cash flow planning

Cash movement planning relies on current assets to forecast short-term financial activity. Cash shows what is available now, while receivables show expected inflows from customers.

Inventory also affects cash planning because stock must be sold before it becomes cash. If stock moves slowly, managers may need tighter purchasing or discounting decisions.

3. They affect working capital and financial stability

Working capital measures the gap between current assets and current liabilities. It helps businesses understand whether short-term resources exceed short-term obligations.

Working capital = Current assets – Current liabilities

Positive working capital can indicate stronger short-term stability. Negative working capital may signal pressure, although the right level depends on industry and operating model.

4. They help managers spot liquidity risks earlier

Current assets can reveal warning signs before cash pressure becomes urgent. Rising receivables may point to collection delays, while excess inventory can show weak stock turnover.

Low cash balances may indicate short-term funding pressure. Regular review helps managers act earlier through collections, stock control, supplier terms, or expense timing.

Why Current Assets Matter for Australian Businesses

Business asset technologies in Australia help teams manage liquidity across tax obligations, supplier payments, wages, and seasonal trading cycles. Current assets give owners the visibility needed to plan these short-term commitments.

The Australian Bureau of Statistics tracks business indicators that reflect changing sales, inventories, and operating conditions. These shifts can affect cash timing and working capital needs.

For businesses with stock, branches, or credit sales, current assets need close control. Better visibility helps reduce overdue invoices, excess inventory, and avoidable cash gaps.

How Accounting Software Helps Track Current Assets

Real-time asset monitoring helps businesses track current assets by centralising cash, receivables, inventory, prepayments, and reports. This improves visibility over short-term resources.

Manual tracking may work for simple operations, but it becomes harder as transaction volume grows. Bank balances, invoices, stock movements, and prepayments can change daily.

Organised asset records reduce the risk of managers missing the true liquidity position. Integrated software supports this by linking financial data with operational activity

HashMicro’s accounting software helps Australian businesses connect accounting, inventory, and reporting workflows. Leaders can monitor current assets more clearly and act faster.

With better financial visibility, teams can review receivables, stock value, prepaid expenses, and cash balances from one system. This supports more accurate short-term decisions.

Conclusion

Current assets are short-term resources a business expects to use, sell, or convert into cash within 12 months. They include cash, receivables, inventory, prepayments, and short-term investments.

Accurate classification helps Australian businesses assess liquidity and manage working capital. It also keeps financial reports clearer and more reliable over time.

If you want to improve your asset management with us, then you can book free consultation with our experts today.

Frequently Asked Questions

-

Are accounts receivable always current assets?

Accounts receivable are usually current assets when the business expects to collect payment within 12 months. If collection is not expected within the short term, or if the receivable is doubtful, the business may need to review its classification and allowance treatment.

-

Is inventory always counted as a current asset?

Inventory is usually counted as a current asset because businesses normally expect to sell or use it within the operating cycle. However, obsolete, damaged, or slow-moving inventory may need review because its recorded value may not reflect how quickly it can become cash.

-

Can prepaid expenses be current assets?

Yes. Prepaid expenses can be current assets when the business expects to receive the benefit within 12 months. Examples include prepaid insurance, rent, subscriptions, and software services.

-

What happens if current assets are lower than current liabilities?

If current assets are lower than current liabilities, the business may have negative working capital. This can signal liquidity pressure because short-term obligations may exceed short-term resources.

-

How often should businesses review current assets?

Businesses should review current assets regularly, especially during month-end reporting, cash flow planning, stocktake, and invoice collection reviews. High-volume businesses may need weekly or real-time visibility over cash, receivables, and inventory.