Accrual accounting records income when a business earns it and expenses when a business incurs them, even if money has not moved yet. This method gives Australian businesses a clearer view of profit, unpaid invoices, supplier bills, and future cash obligations.

For growing companies, accrual accounting often provides a more accurate financial picture than cash accounting. It helps owners track performance, prepare reports, manage BAS obligations, and make decisions based on real business activity.

Key Takeaways

Accrual accounting records income when a business earns it and expenses when it incurs them, even if cash has not moved yet.

This method gives Australian businesses a clearer view of profit, unpaid invoices, supplier bills, GST timing, and future cash obligations.

Accrual accounting often suits growing companies with invoices, credit terms, inventory, supplier accounts, or detailed reporting needs.

Accounting software helps businesses manage accrual accounting by tracking invoices, bills, GST, receivables, payables, and reports in one system.

What Is Accrual Accounting?

"Accrual accounting gives growing businesses a clearer view of real performance because it records income and expenses when they happen, not only when cash moves"

Accrual accounting is an accounting method that records revenue and expenses when they happen, not only when cash enters or leaves the bank account. For example, a company records a sale when it issues an invoice, even if the customer pays later.

This approach helps businesses match income with related costs in the same reporting period. As a result, the profit and loss statement shows how the business actually performed during that period.

Accrual accounting suits companies that offer credit terms, hold inventory, manage supplier accounts, or need detailed financial reporting. Therefore, many medium and growing businesses use it to understand their financial position more clearly.

How Accrual Accounting Works

Accrual accounting follows a few core principles that help businesses record transactions in the right period. These principles keep financial reports consistent and easier to compare over time.

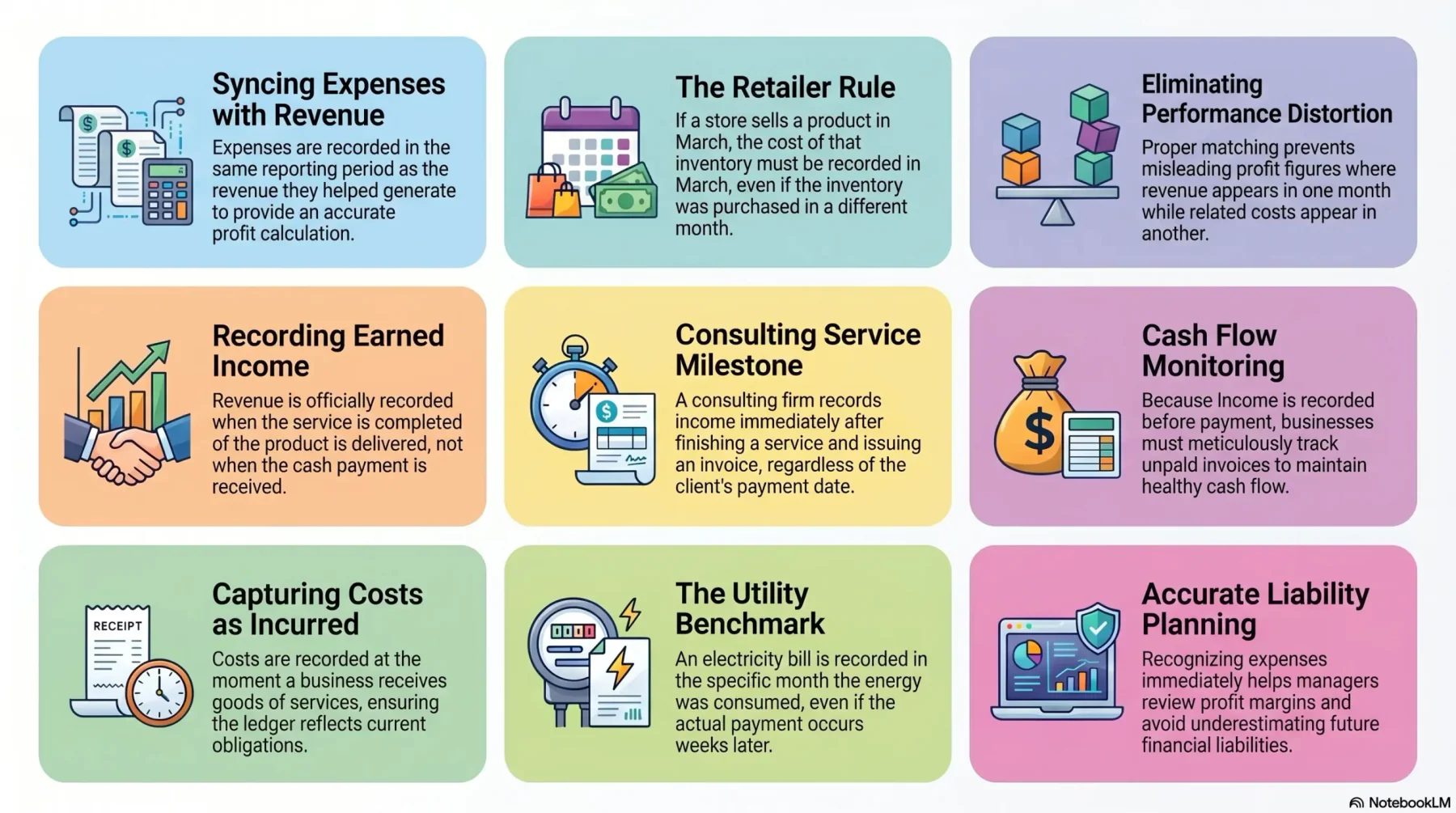

1. The matching principle

The matching principle records expenses in the same period as the revenue they helped generate. For example, if a retailer sells products in March, it should record the cost of those products in March as well.

This principle helps a business avoid misleading profit figures. Without it, revenue may appear in one month while the related costs appear in another, which can distort performance.

2. Revenue recognition

Revenue recognition means a business records income when it earns the revenue, not when it receives payment. For example, a consulting company records income after completing a service and issuing an invoice.

This method gives owners a clearer view of sales activity. However, it also means the business must track unpaid invoices carefully to protect cash flow.

3. Expense recognition

Expense recognition records costs when the business receives goods or services, even if it pays later. For instance, a company records an electricity bill in the month it uses the electricity.

This approach helps businesses see their true operating costs. Then, managers can plan payments, review margins, and avoid underestimating future liabilities.

Cash vs Accrual Accounting

Cash and accrual accounting both track business activity, but they record transactions at different times. The table below shows the key differences.

| Aspect |

Cash Accounting |

Accrual Accounting |

| When income is recorded |

When payment is received | When income is earned |

| When expenses are recorded |

When payment is made | When expenses are incurred |

| Best for |

Small businesses with simple cash flow | Growing businesses with invoices, credit terms, or inventory |

| Profit visibility |

Simpler but less complete | More accurate across reporting periods |

| Cash flow visibility |

Easy to track bank movement | Requires separate cash flow monitoring |

| Complexity |

Easier to manage | More detailed and structured |

| BAS impact |

GST usually reported when payment happens | GST usually reported when invoice activity happens |

Pros and cons of cash accounting

Cash accounting is simple because it follows actual money movement. A business records income only when customers pay and records expenses only when it pays suppliers.

The main advantage is ease of use, especially for sole traders and small businesses with few invoices. However, cash accounting may hide unpaid bills, outstanding customer invoices, and real profitability.

For example, a company may look profitable because it has received several payments. However, it may still owe large supplier bills that do not appear in the report yet.

Pros and cons of accrual accounting

Accrual accounting gives a more complete view of business performance. It records sales, costs, receivables, and payables in the period they relate to.

The main benefit is accuracy, especially for companies that manage stock, credit sales, or long payment terms. However, it takes more effort because the business must track invoices, bills, and adjustments carefully.

For example, a company may show strong revenue before customers pay. Therefore, it still needs cash flow reports to ensure it can cover payroll, rent, and supplier payments.

Accrual Accounting Example

A furniture business sells $8,800 worth of goods to a customer on 20 June and gives 30-day payment terms. Under accrual accounting, the business records the $8,800 sale in June because it earned the income in June.

If the goods cost $5,000, the business also records the cost in June. As a result, the June profit report reflects both the sale and the related expense.

If the customer pays in July, the payment affects the bank balance in July. However, the income already appeared in the June profit and loss report because the business earned it then.

Which Method Should Australian Businesses Use?

The right method depends on business size, GST reporting obligations, transaction volume, and how much detail the owner needs. Australian businesses should also consider ATO rules before choosing an accounting basis.

ATO requirements and the $10 million threshold

The ATO allows many businesses with GST turnover below $10 million to choose cash or non-cash accounting for GST reporting. Businesses at or above the relevant threshold may need to use fuller reporting methods for GST.

This threshold matters because it affects how a company reports GST on its BAS. Therefore, businesses should confirm their GST turnover and reporting obligations before changing methods.

Some businesses may still choose accrual accounting even when they qualify for cash accounting. For example, a company with inventory, many invoices, or investor reporting needs may prefer accrual reports for better accuracy.

When accrual accounting makes sense

Accrual accounting makes sense when a business issues invoices before payment, receives supplier bills before paying them, or needs to monitor profit margins closely. It also helps companies that sell on credit or manage recurring contracts.

Retailers, wholesalers, construction companies, professional service firms, and distribution businesses often benefit from accrual accounting. Their financial activity usually happens before cash moves, so cash reports alone may miss important details.

Accrual accounting also supports better planning. For example, managers can review unpaid invoices, upcoming bills, sales trends, and product costs before making purchasing or hiring decisions.

Accrual accounting and BAS reporting

Accrual accounting affects when a business reports GST on its BAS. Under a non-cash method, a company generally reports GST when it issues or receives an invoice, not only when payment happens.

This timing can create a gap between GST reporting and cash flow. For example, a business may need to report GST on a sale before the customer has paid the invoice.

Therefore, businesses using accrual accounting need strong accounts receivable controls. They should monitor overdue invoices, reconcile GST codes, and review BAS figures before lodgement.

Accurate tax invoices also matter because GST credits depend on proper records. If a business misses a valid tax invoice, it may need to claim the credit in a later BAS period.

How Accounting Software Handles Accrual Accounting

Accounting software helps businesses manage accrual accounting by recording invoices, bills, payments, GST, and account balances in one system. It reduces manual work and improves reporting accuracy.

For example, the software can record revenue when a sales invoice is issued and track the unpaid amount as accounts receivable. Then, once the customer pays, the system updates the bank balance and clears the outstanding invoice.

Good accounting software also supports BAS reporting, GST code mapping, supplier bills, expense recognition, and financial statements. As a result, businesses can review profit, cash flow, receivables, and payables without rebuilding reports manually.

For growing Australian businesses, software also helps maintain consistency across teams. Sales, finance, inventory, and procurement teams can work from the same transaction data.

Conclusion

Accrual accounting helps Australian businesses record revenue and expenses when they happen, not only when cash moves. It gives a clearer view of profit, unpaid invoices, supplier bills, GST timing, and future cash obligations.

Cash accounting may suit smaller businesses with simple transactions, but accrual accounting often works better for companies with inventory, credit terms, or recurring invoices. Before choosing a method, review ATO requirements, GST turnover, BAS reporting needs, and internal goals, then book a free consultation to find the right accounting software.

Frequently Asked Question

Accrual accounting records income when a business earns it and expenses when it incurs them, even if payment happens later.

Accrual accounting works by matching revenue and related expenses in the same reporting period. For example, a business records a sale when it issues an invoice, not only when the customer pays.

Cash accounting records transactions when money moves, while accrual accounting records transactions when income is earned or expenses are incurred. Accrual accounting gives a clearer view of profit, unpaid invoices, and supplier bills.

Australian businesses should consider accrual accounting when they manage invoices, credit terms, inventory, supplier accounts, recurring contracts, or detailed BAS reporting needs.