Under a RM2 million PAM contract, a contractor may need to provide a performance bond worth RM100,000 to RM200,000. Yet many contractors sign without fully understanding what a performance bond in construction allows the employer to claim when delays, defaults, or contract breaches happen.

In Malaysia, performance bonds depend on contract wording, bond type, and project risk. PAM 2006 standard form contract, widely used in Malaysian private construction projects, treats the bond as part of the contractor’s security obligation, while on-demand bonds, bank guarantees, and surety bonds can affect cash flow and claim exposure differently.

By the end, contractors can see how bond percentage, issuer type, claim wording, and DLP release timing affect project risk. The aim is to help teams review clauses in construction contracts with clearer context before accepting a performance bond, bank guarantee, or surety bond requirement.

Key Takeaways

Performance bond protects the employer if the contractor fails to complete the project or breaches the contract.

The contractor submits the bond, and the employer can call it if default occurs.

On-demand bonds need a written demand; conditional bonds need proof of breach.

Track bond expiry dates, DLP timelines, contract milestones, and project documents in one place to reduce missed follow-ups.

What Is a Performance Bond in Construction?

A performance bond in construction is a performance guarantee that protects the employer if the contractor fails to complete the works or breaches key obligations in the construction contract. It involves three parties: the employer or obligee, the contractor or principal, and the bond issuer or surety. A call on the bond may happen when contractor default, non-completion, or another stated breach occurs.

In Malaysia, performance bonds are common in PAM 2006 contracts, where they act as financial security for the employer. The bond does not replace the contractor’s obligation to finish the project; it only gives the employer a remedy if performance fails. Unlike a payment bond, which protects unpaid subcontractors or suppliers, a performance bond focuses on contract completion.

Key Parties in a Construction Performance Bond

| Party | Role | Also Called |

| Employer | The project owner or beneficiary who can claim against the bond if the contractor defaults. | Obligee or beneficiary |

| Contractor | The party responsible for completing the construction works under the contract. | Principal |

| Bank or insurer | The bond issuer that provides the financial guarantee if the claim conditions are met. | Surety |

How Do Performance Bonds Work in Construction?

A performance bond works when the contractor obtains a bond from a bank or insurer and submits it to the employer as security under the construction contract. If contractor default occurs, the employer may make a bond call by sending a written demand to the bond issuer, which then pays based on the bond wording.

For example, a RM5 million project with a 5% performance bond gives the employer RM250,000 in security. If the contractor abandons the works, the employer may call the bond. Under Malaysian case law, an on-demand bond can usually be called by written demand without proof of breach, while a conditional bond requires proof that the bond trigger has occurred.

- Contract is signed: The construction contract states whether the contractor must provide a performance bond, the bond amount, validity period, and required form.

- Contractor obtains the bond: The contractor applies to a bank, insurer, or surety provider as part of the procurement and bond submission process. The issuer reviews the contractor’s credit, project risk, and supporting documents.

- Bond is submitted to the employer: The employer checks whether the bond matches the contract requirements, including amount, wording, expiry date, and on-demand or conditional terms.

- Project runs as agreed: The contractor carries out the works through proper construction project management, while the bond remains available as a completion guarantee if serious non-performance occurs.

Default or bond trigger occurs: A trigger may include abandonment, failure to complete, refusal to remedy serious breaches, or another default stated in the contract.

Employer submits a demand: This is the bond call. For an on-demand bond, the demand may not require proof of default if the wording allows payment on first demand.

Issuer pays and seeks recovery: After paying the employer, the surety may recover the amount from the contractor based on the counter-indemnity or facility agreement.

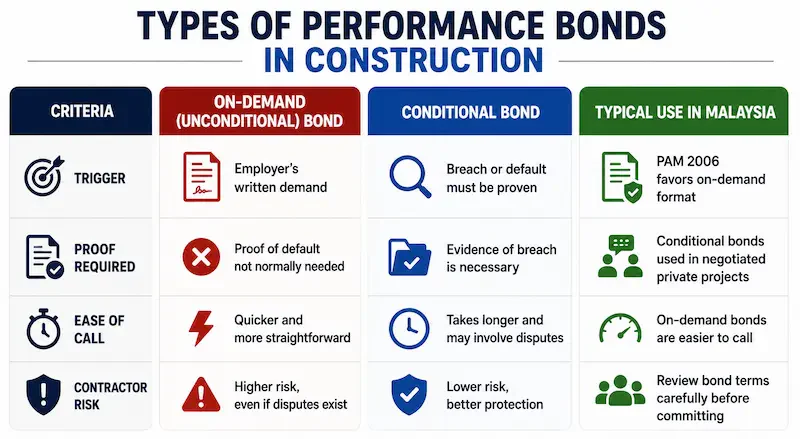

Types of Performance Bonds in Construction

There are two main types of performance bonds used in Malaysian construction: on-demand or unconditional bonds and conditional bonds. The practical difference is simple: an on-demand bond can usually be called with a written demand, while a conditional bond requires proof that the contractor has breached the construction contract.

On-Demand or Unconditional Bonds

An on-demand bond is payable once the employer submits a written demand that follows the bond wording. Under PAM 2006 Clause 37, this is commonly treated as the standard form of performance bond in Malaysian private construction projects, although the exact bond wording should still be checked before signing.

This type creates higher risk for contractors because the employer may call the bond even when a dispute is still ongoing. For example, if the contractor disputes an alleged delay, the bond issuer may still have to pay first if the bond is written as an on-demand performance guarantee.

Conditional Bonds

A conditional bond gives the contractor more protection because the employer must show that a contractor default or breach has occurred. The bond issuer does not simply pay because a written demand is made.

This type is more common where parties want stronger safeguards before payment is released under the bond. It may suit private sector arrangements where the employer accepts a slower claim process in exchange for clearer proof requirements.

| Criteria | On-Demand Bond | Conditional Bond | Typical Use in Malaysia |

| Trigger | Written demand from the employer | Proven breach or default | PAM 2006 commonly uses on-demand wording |

| Proof required | Usually no proof of default required | Evidence of breach is required | Conditional bonds may appear in negotiated private contracts |

| Ease of call | Easier and faster to call | Slower and more disputed | On-demand bonds create higher contractor exposure |

| Contractor risk | Higher, even during disputes | Lower, because proof is needed | Contractors should review wording before signing |

Performance Bond Value: What Percentage Is Standard in Malaysia?

Performance bonds in Malaysia typically range from 5% to 10% of the contract value. Under PAM 2006, the standard performance bond value is commonly 5%, while government or JKR contracts may require a higher amount, often up to 10% depending on tender conditions and project risk.

It is useful to separate bond value from bond cost. Bond value is the guaranteed amount the employer can claim if the contractor defaults, while bond cost is the premium or fee paid by the contractor to the bank or insurer. In Malaysia, the cost may vary by provider, credit profile, project size, and bond type, but a practical working estimate is around 0.5% to 1.5% of the bond value per year.

| Contract Value | Bond at 5% | Bond at 7.5% | Bond at 10% |

| RM 500,000 | RM 25,000 | RM 37,500 | RM 50,000 |

| RM 1,000,000 | RM 50,000 | RM 75,000 | RM 100,000 |

| RM 2,000,000 | RM 100,000 | RM 150,000 | RM 200,000 |

| RM 5,000,000 | RM 250,000 | RM 375,000 | RM 500,000 |

For contractors, the practical issue is cash flow. A 10% bond on a RM5 million project gives the employer RM500,000 in security, but the contractor may also need to pay yearly fees, provide collateral, or use part of its banking facility. This is why the performance bond percentage should be reviewed together with retention, payment terms, construction equipment costs, and working capital before signing the contract.

Performance Bond vs Bank Guarantee: What’s the Difference?

While often used interchangeably, a performance bond and a bank guarantee differ in who issues them, cost structure, collateral requirements, and cash flow impact. In Malaysian construction, both can serve as security for contract performance, but the route matters because one may rely more on insurance underwriting while the other may use the contractor’s banking facility.

The key point is this: on-demand vs conditional is about the claim mechanism, not the issuer type. A performance bond issued by an insurer can be on-demand or conditional. A bank guarantee can also be on-demand or conditional, depending on the wording. Contractors should therefore check both the issuer and the bond wording before assuming how easily the employer can call it.

| Criteria | Performance Bond (Surety/Insurance) | Bank Guarantee |

| Issued by | Licensed insurance company or surety provider | Bank |

| Collateral required | Usually based on creditworthiness, with less cash tied up | Often requires cash, fixed deposit, or credit facility |

| Premium or cost | Around 0.5% to 1.5% of bond value per year | Around 1% to 3% of bond value, plus bank fees |

| Processing time | Often around 3 to 7 business days, depending on documents | Often around 5 to 14 business days, depending on bank review |

| Ease of calling | If on-demand, payment may be made after a valid written demand | If on-demand, payment may also be made after a valid written demand |

| Cash flow impact | Usually lower because less cash is locked as collateral | Usually higher because banking limits or deposits may be used |

| Best for | Contractors with limited cash or fixed deposits | Contractors with established banking facilities |

For contractors, the practical difference often comes down to liquidity. An insurance-backed performance bond may preserve working capital because the contractor may not need to lock up the same amount of cash or fixed deposit. This can matter in projects where mobilisation, materials, labour, subcontractor payments, and project cash flow and accounting records already need close tracking before progress payments arrive.

A bank guarantee may still make sense where the contractor has a strong banking relationship, available credit lines, or an employer that specifically requires bank-issued security. It may also be more familiar to certain employers and project owners. Neither option is automatically better. The right choice depends on contract requirements, issuer acceptance, available cash, banking facilities, and whether the bond wording is on-demand or conditional.

Performance Bond in Malaysia: Legal Framework

Performance bonds in Malaysian construction are mainly shaped by three frameworks: PAM 2006 Contract Conditions, the CIDB Act, and CIPAA 2012. PAM 2006, widely used in Malaysian private construction projects, covers performance bond requirements under Clause 37 and commonly uses an on-demand bond structure.

- The CIDB Act, or Lembaga Pembangunan Industri Pembinaan Malaysia Act 1994 (Act 520), governs contractor registration in Malaysia. This matters because employers often review CIDB status, contractor grade, and project eligibility before accepting contractors for bonded works.

- CIPAA 2012, or the Construction Industry Payment and Adjudication Act 2012, provides a statutory route for construction payment disputes. It does not override the bond wording, but it can become relevant when a bond call is linked to unpaid claims, set-offs, or alleged contractor default.

The key risk is practical: Malaysian courts generally treat on-demand bonds as payable once a valid written demand is made. Government contracts such as JKR or PWD forms may also have their own bond terms, so contractors should check the exact clause, bond type, and demand wording before signing.

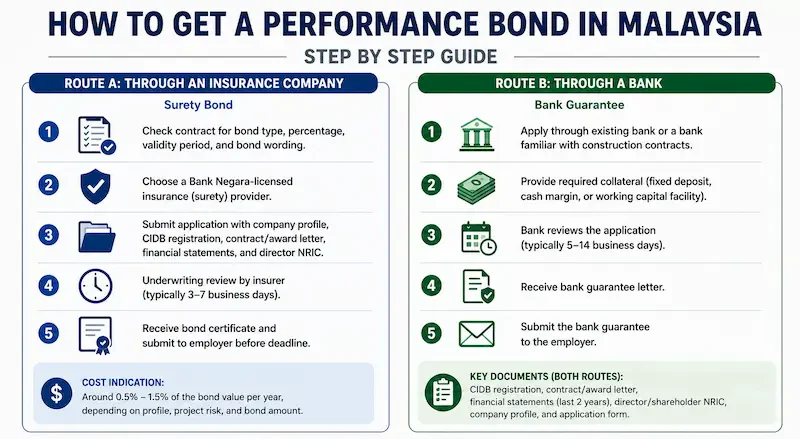

How to Get a Performance Bond in Malaysia Step by Step

In Malaysia, contractors can obtain a performance bond through two routes: via a licensed insurance company as a surety bond or via a bank as a bank guarantee. The right route depends on the contract requirement, bond wording, available collateral, and how much cash flow the contractor wants to preserve.

Before applying, check the contract first. The employer may state the required bond percentage, validity period, issuer type, and whether the bond must be on-demand or conditional. Contractors should also prepare their CIDB registration details, as employers and issuers commonly review contractor status before accepting or issuing the bond.

Route A: Through an Insurance Company (Surety bond)

This route is usually used when the contractor wants a surety bond with lower cash tied up. The insurer will assess the contractor’s financial position and project risk before issuing the bond.

- Confirm the bond type required in the contract, including percentage, expiry date, and on-demand or conditional wording.

- Choose a Bank Negara-licensed surety insurance provider in Malaysia.

- Submit the application with company profile, CIDB registration, contract or letter of award, financial statements, and director NRIC.

- Wait for underwriting review, which commonly takes around 3 to 7 business days for standard bonds.

- Receive the bond certificate and submit it to the employer before the commencement deadline.

The cost is usually around 0.5% to 1.5% of the bond value per year, depending on the contractor’s profile, project risk, and bond amount.

Route B: Through a Bank (Bank Guarantee)

A bank guarantee is more common for contractors with existing banking facilities or fixed deposits. The bank may require collateral before issuing the guarantee.

- Apply through the contractor’s existing bank or a bank familiar with construction contracts.

- Provide the required collateral, such as fixed deposit, cash margin, or use of a working capital facility.

- Allow time for bank review, which may take around 5 to 14 business days.

- Receive the bank guarantee letter and submit it to the employer.

Documents usually needed include CIDB green card or registration details, contract or letter of award from the construction procurement process, company financial statements for the last two years, director or shareholder NRIC, company profile, and completed application form. Insurance routes may preserve cash flow better, while bank routes may suit contractors with available credit lines.

When and How Is a Performance Bond Released?

A performance bond is usually released after the Defects Liability Period (DLP), once the employer confirms that defects have been rectified. DLP is the post-completion period where the contractor must fix defects found in the works, and its duration should be checked in the PAM 2006 contract particulars.

The contractor should request the release in writing after DLP ends. If no request is made, the bond may stay active longer than needed and continue affecting the contractor’s facility or cost.

The usual release process is:

- The architect or contract administrator issues the certificate of practical completion.

- The DLP begins from the practical completion date.

- The contractor completes defect rectification during the DLP.

- The DLP ends and no major defects remain outstanding.

- The contractor submits a written request to release the performance bond.

- The employer reviews the request and confirms whether release is acceptable.

- The bond issuer is notified, and the bond is returned, cancelled, or allowed to expire.

Release can be delayed if defects remain unresolved, the employer disputes completion quality, or the contractor does not follow up with proper documents. In some projects, missing certificates, unclear correspondence, or late confirmation from the employer can also hold back the release. Contractors managing multiple construction projects should track the DLP end date, defect list, and release request in writing to avoid leaving the bond open unnecessarily.

"Contractors should track DLP expiry, defect closure, and written release requests early. Bond release does not happen automatically, so missing follow-up can keep the bond active longer than needed."

Common Mistakes Contractors Make

- Not checking the bond type

Some contractors sign without confirming whether the bond is on-demand or conditional. To avoid this, check the bond wording before signing and confirm whether a written demand alone is enough for the employer to call the bond. - Letting the bond expire too early

A bond that expires before practical completion can breach the construction contract, reduce construction productivity, and delay project commencement or payment. Set an internal reminder at least 30 to 60 days before expiry so renewal can be arranged on time. - Forgetting to request release after DLP

Bond release does not always happen automatically after the Defects Liability Period (DLP). Contractors should submit a written release request once defects are cleared and keep proof of employer confirmation. - Assuming a bond call can easily be stopped

Under Malaysian on-demand bond principles, stopping a valid bond call is difficult once the demand is made. Review the call conditions early and seek advice before a dispute escalates. - Not comparing provider rates

Bond costs can vary by issuer, contractor profile, project value, and collateral requirement. Compare several banks or insurers before committing so the final cost and cash flow impact are clear.

Conclusion

A performance bond in construction should not be treated as a routine contract attachment. Contractors need to check the bond percentage, expiry date, issuer type, and whether the wording is on-demand or conditional before signing, because these details affect cash flow, claim exposure, and release after the Defects Liability Period.

For Malaysian projects, the safest approach is to read the bond together with the PAM 2006 clause, CIDB requirements, payment terms, and practical project risks. A 5% bond may look manageable, but it can still affect working capital if the contractor must lock up collateral, renew the bond, or respond to a disputed call.

If your team manages several projects, progress claims, subcontractor documents, and contract milestones at the same time, a free demo can help you review how these workflows are tracked and organised before gaps turn into costly disputes.

Frequently Asked Questions About Performance Bonds in Malaysia

A performance bond in construction is a financial guarantee that protects the employer if a contractor fails to complete the project or breaches the terms of the construction contract. It involves three parties: the employer (beneficiary), the contractor (principal), and the bond issuer (surety or insurer). The bond can be called upon when contractor default, non-completion, or another specified breach occurs.

A performance bond is typically issued by an insurance company or surety provider, whereas a bank guarantee is issued by a bank. The key difference lies in cash flow impact. Bank guarantees often require fixed deposits, cash margins, or utilization of banking facilities, while insurance-backed performance bonds generally rely more on underwriting assessments. Both instruments can be structured as either on-demand or conditional guarantees.

Performance bond requirements in Malaysia commonly range from 5% to 10% of the total contract value. Private-sector contracts using PAM 2006 often require a 5% bond, while government and JKR projects may require up to 10%. This percentage represents the bond amount itself and should not be confused with the premium paid to obtain the bond.

A performance bond is usually released after the Defects Liability Period (DLP), which commonly lasts between 18 and 24 months following practical completion, depending on the contract terms. Contractors generally submit a formal release request, after which the employer confirms that all defects have been rectified before notifying the bond issuer to release the guarantee.

Performance bonds in Malaysia are primarily influenced by PAM 2006, the Construction Industry Development Board (CIDB) Act, and the Construction Industry Payment and Adjudication Act (CIPAA) 2012. PAM 2006 provides standard contract conditions for private-sector projects, the CIDB Act governs contractor registration and industry requirements, and CIPAA 2012 facilitates dispute resolution for construction payment claims.

Start with the contract value, then apply the bond percentage stated in the tender or contract document. If the contract value is RM2 million and the required bond is 5%, the bond value is RM100,000. Contractors should also separate this from the premium cost, because the fee paid to the bank or insurer is usually only a portion of the bond value.

A performance bond gives the employer financial protection when the contractor does not meet agreed project obligations. For contractors, it also becomes a contract requirement that affects cash flow, banking facilities, and project risk. This is why the bond type, expiry date, and release conditions should be reviewed before signing, not after a dispute begins.