Many Malaysian businesses operate on 30 to 90-day payment terms, leaving them with outstanding invoices while payroll, supplier payments, and other operating costs still need to be paid. Invoice financing provides immediate working capital by unlocking cash tied up in unpaid invoices, helping businesses maintain smoother cash flow.

Long B2B payment terms remain common across Malaysia's construction, manufacturing, and trading industries. At the same time, the rollout of the LHDN e-Invoice system is making invoice verification faster, allowing financing providers to approve applications more efficiently. This makes invoice financing an increasingly practical option for businesses seeking short-term liquidity.

Choosing the right invoice financing solution requires more than comparing funding options. Businesses should also understand the associated costs, accounting treatment, and how stronger accounts receivable management can reduce future cash flow pressures.

Chasing overdue invoices is only part of the problem when accounts receivable records are scattered and payment tracking is done manually. Invoice financing helps businesses improve collections, reduce payment delays, and strengthen long-term cash flow management.

What Is Invoice Financing?

Invoice financing allows businesses to use outstanding invoices to obtain immediate funding. Depending on the financing arrangement, invoices may be used as collateral or sold to a financing provider. In most cases, the lender advances around 80% to 90% of the invoice value and releases the remaining balance after the customer pays, less the agreed financing fee.

For example, a business issues an invoice worth RM100,000 with 60-day payment terms. The financing provider advances RM85,000 within 48 hours. Once the customer pays on day 60, the business receives the remaining RM15,000 after deducting a service fee of approximately RM1,500 to RM2,000, resulting in a final payment of RM13,000 to RM13,500.

Invoice financing primarily relies on the creditworthiness of your customer rather than your business. This makes it a practical funding option for companies with reliable buyers but limited access to traditional bank financing. Businesses should also ensure their accounting software can accurately record financing charges and related journal entries.

Invoice Financing vs. Bank Loan

| Factor | Invoice Financing | Bank Loan | Business Credit Line |

|---|---|---|---|

| Approval time | 24–48 hours | 2–6 weeks | 1–3 weeks |

| Collateral required | Invoice only | Property / assets | Business assets |

| Based on | Buyer's credit history | Your credit history | Business revenue |

| Typical amount (RM) | RM10K – RM5M+ | RM50K – RM10M+ | RM20K – RM2M |

| Creates new debt? | No | Yes | Yes |

Invoice Financing vs. Factoring

Although the terms invoice financing and invoice factoring are often used interchangeably, they refer to different financing arrangements. The biggest distinction lies in who manages customer payment collection, which can affect customer relationships, confidentiality, and internal accounts receivable processes.

Types of Invoice Financing in Malaysia

Businesses can choose from several types of invoice financing depending on their operational needs and preferred level of control. The three most common options in Malaysia are outlined below.

Invoice Discounting

Invoice discounting allows businesses to unlock cash from outstanding invoices while retaining full control over customer relationships and payment collection. Since customers are generally unaware that financing is being used, this option helps maintain confidentiality and business trust.

It is commonly chosen by companies with established credit control processes, long-term B2B contracts, or key accounts where direct communication with customers is important. Most providers also require a minimum invoice value and a trading history of at least six to twelve months.

Invoice Factoring

Invoice factoring involves selling outstanding invoices to a financing provider, who then takes responsibility for collecting payment from customers. Businesses receive an advance quickly, but customers are aware that a third party is managing the collection process.

This option is suitable for SMEs or growing businesses that want to reduce the time and effort spent on accounts receivable management. By outsourcing collections, companies can improve cash flow while focusing more on daily operations and business growth.

Islamic Invoice Financing (IF-i)

Islamic Invoice Financing (IF-i) provides working capital through Shariah-compliant structures such as Murabahah or Wakalah. Instead of charging interest, the financing provider applies a profit margin that is agreed upon before the transaction begins.

IF-i is ideal for Muslim-owned businesses, government contractors, and companies that prefer or require Islamic financing. Many Malaysian banks, including Maybank Islamic, CIMB Islamic, and Bank Islam, offer IF-i facilities to support businesses seeking Shariah-compliant funding solutions.

The table below summarises the key differences between each type of invoice financing, making it easier to identify the option that best suits your business needs.

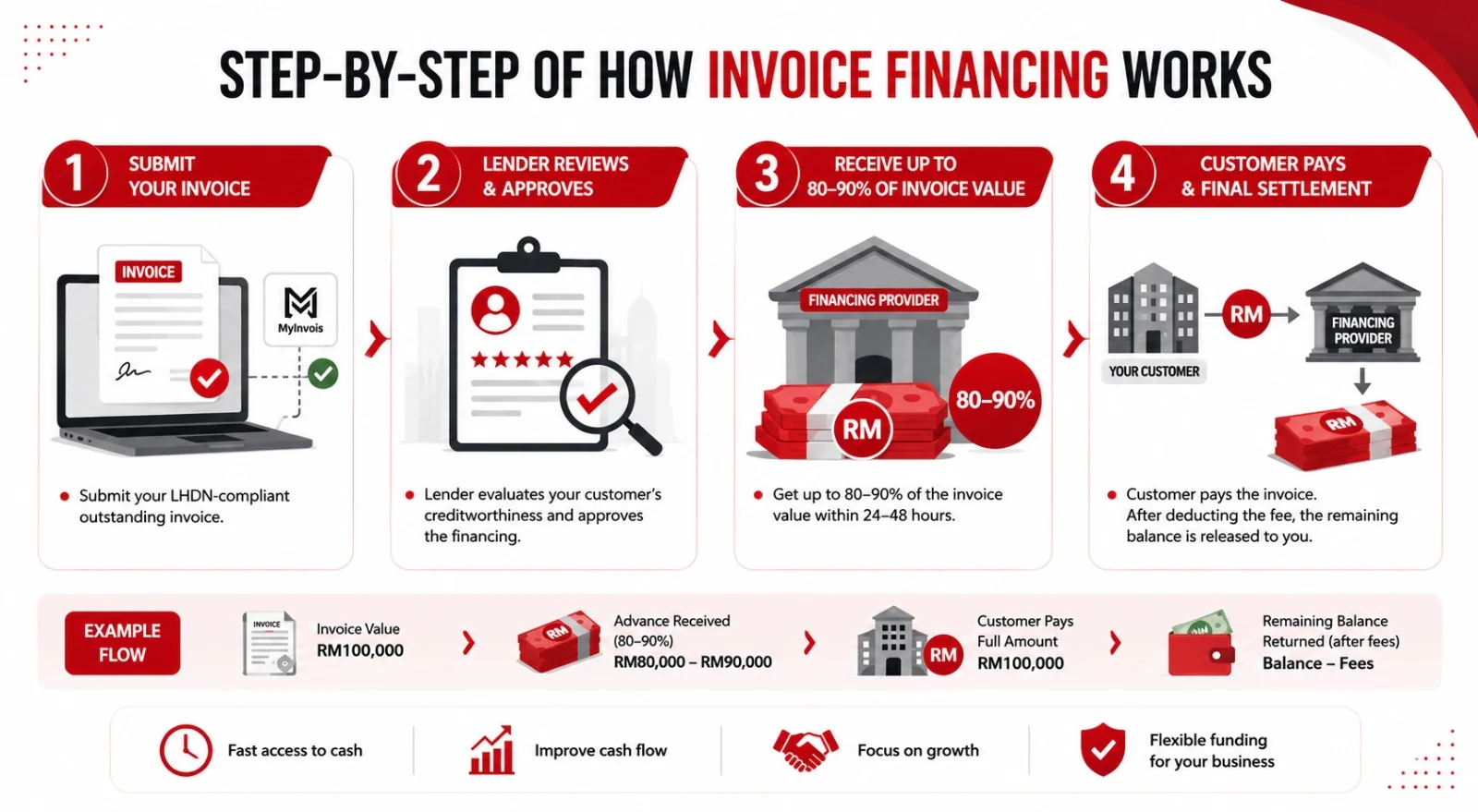

Step-by-Step of Invoice Financing Works

The invoice financing process is straightforward, allowing businesses to access working capital without waiting for customers to complete payment terms. Below is a step-by-step overview of how the process works.

Step 1: Submit Your LHDN-Compliant Invoice

The process begins by submitting an outstanding invoice for goods delivered or services completed. Most providers only finance verified receivables, and invoices validated through the MyInvois portal under Malaysia's e-Invoice framework can help speed up the verification and approval process.

Step 2: Lender Reviews and Approves

The financing provider evaluates your customer's creditworthiness rather than focusing solely on your business. This allows companies with reliable buyers to qualify more easily, with approval taking anywhere from a few hours to several business days depending on the provider.

Step 3: Receive Up to 80–90% of the Invoice Value

Once approved, the financing provider advances around 80% to 90% of the invoice value, with funds typically transferred within 24 to 48 hours. For example, an RM100,000 invoice with an 85% advance rate provides RM85,000 in immediate working capital to support payroll, supplier payments, or daily operations.

Step 4: Customer Pays and Final Settlement

When the customer pays the invoice, the financing provider deducts the agreed financing fee before releasing the remaining balance. Using the same example, after receiving the full RM100,000 payment, the provider returns the remaining RM15,000 less a financing fee of around RM1,500 to RM2,000, leaving the business with approximately RM13,000 to RM13,500.

Who Should and Shouldn't Use Invoice Financing?

Best Fit: Industries in Malaysia That Benefit Most

- Construction contractors

Especially CIDB-registered firms working on government or GLC projects, where payment terms often extend to 60–90 days. Invoice financing helps contractors maintain cash flow for labour, materials, and subcontractor payments while waiting for project invoices to be settled. - Trading and wholesale companies

Businesses that sell goods on credit often have a significant amount of cash tied up in outstanding invoices. Invoice financing provides immediate working capital, allowing them to replenish inventory and fulfil new customer orders without delays. - Manufacturers

Manufacturers supplying retailers, distributors, or export customers frequently operate on extended payment terms. Invoice financing helps cover production costs, purchase raw materials, and keep production lines running without relying on long-term loans. - Healthcare and medical suppliers

Suppliers serving hospitals, clinics, and government healthcare facilities often wait 30–60 days for payment. Invoice financing helps businesses manage operating expenses while ensuring a stable supply of medical products and equipment. - Professional services firms

Engineering, IT, consulting, and other project-based businesses typically invoice clients based on project milestones. Invoice financing provides access to funds between billing cycles, helping cover salaries, project costs, and business operations.

When Invoice Financing Is Not the Right Move

- B2C retail business

Invoice financing is designed for businesses that issue invoices to other businesses. Since retail customers usually pay immediately at the point of sale, there are no trade receivables available to finance. - Has very thin profit margins

Financing fees of around 1–3% per month can significantly reduce profitability if operating margins are already low. In this situation, improving cost control or payment terms may provide better long-term results. - Has a poor payment history

Financing providers prefer invoices from reliable customers with strong repayment records. Under recourse financing, unpaid invoices may become your responsibility again, increasing financial risk instead of reducing it. - Funding for long-term investments

Invoice financing is intended to solve short-term cash flow needs rather than finance business expansion. Purchasing machinery, vehicles, or other long-term assets is generally better suited to equipment financing or term loans.

Invoice Financing: Pros, Cons & Real Costs

Invoice financing offers several advantages, but it also involves costs and risks that should not be overlooked. The sections below provide a balanced overview to help businesses evaluate this financing option.

Cost Breakdown: Discount Rate, Service Fees & Hidden Charges

The advertised discount rate does not always reflect the total cost of invoice financing. Many providers also charge additional fees that can increase overall financing expenses, so it is important to review the full pricing structure before signing an agreement.

Common charges include:

- Application or setup fee: Usually a one-time fee of RM500–RM2,000 for opening a financing facility.

- Due diligence fee: Charged when assessing the creditworthiness of buyers.

- Administration or management fee: A monthly fee for maintaining the financing facility.

- Minimum usage fee: Charged by some providers even if no funds are drawn during the month.

Risks and How to Mitigate Them (Recourse vs. Non-Recourse)

The biggest risk in invoice financing depends on whether the facility is recourse or non-recourse. Under recourse financing, the business must repay the advance if the customer fails to pay, while non-recourse financing shifts most of that risk to the provider for a higher fee.

Businesses with a few large customers may benefit from the added protection of non-recourse financing. For companies with a diversified customer base and consistent payment history, recourse financing is often the more affordable option.

Invoice Financing Solves a Symptom, AR Automation Fixes the Cause

Invoice financing is a valuable source of short-term working capital, but it addresses the immediate cash flow gap rather than the underlying business process. Improving how invoices are managed and collected can help businesses rely less on external financing over time.

Common Causes of Cash Flow Gaps

For many Malaysian SMEs, cash flow problems stem from operational processes rather than a lack of sales. Long customer payment terms, delayed follow-ups, and limited visibility into outstanding invoices often result in cash being tied up longer than expected.

Businesses that still rely on spreadsheets or manual reminders may experience longer collection cycles and slower payments. Identifying these bottlenecks is the first step toward improving cash flow and reducing reliance on external financing.

How AR Automation Reduces the Need for Invoice Financing

Automating accounts receivable helps businesses collect payments faster and gain better control over cash flow. Automated invoice reminders, AR aging reports, and real-time payment tracking make it easier to identify overdue invoices before they become serious cash flow issues.

With greater visibility into outstanding receivables and customer payment behaviour, businesses can improve collection efficiency and forecast cash flow more accurately. As invoices are paid sooner, the need to rely on invoice financing for short-term working capital naturally decreases.

Accounting Treatment: Journal Entry for Invoice Financing

Proper accounting treatment is essential to ensure invoice financing transactions are accurately reflected in your financial records. Recording the advance, financing fee, and final settlement correctly provides a clearer picture of cash flow and financing costs.

The example below illustrates the journal entries using a financing facility with an RM100,000 invoice, an 85% advance (RM85,000), a financing fee of RM2,000, and a final balance of RM13,000.

Conclusion

Invoice financing is a practical solution for Malaysian businesses facing long payment cycles, providing quick access to working capital when cash is tied up in outstanding invoices. Used strategically for temporary funding needs or large invoices, it can help businesses maintain operations without waiting for customers to pay.

However, invoice financing should complement, not replace, effective accounts receivable management. If your business relies on it frequently, recurring payment delays and collection inefficiencies may be limiting your cash flow. Strengthening your receivables process can reduce overdue invoices, improve cash flow visibility, and lessen the need for external financing over time.

Discover how automation can improve invoice management and cash flow visibility. Book a free demo to see how integrated accounting software can improve accounts receivable management and cash flow visibility.

FAQ about Invoice Financing

What is the difference between invoice financing and invoice factoring?

Invoice financing, also known as invoice discounting, allows businesses to borrow against outstanding invoices while retaining full control over customer relationships and payment collection. In contrast, invoice factoring transfers the responsibility for collecting payments to the financing provider. The main difference is confidentiality. With invoice financing, customers are generally unaware that a third party is involved, whereas factoring is often preferred by businesses that want to outsource accounts receivable management.

What are the typical invoice financing rates in Malaysia?

Invoice financing rates in Malaysia typically range from 1% to 3% per month on the advanced amount, depending on factors such as the financing provider, invoice value, and the buyer's credit profile. In addition to the discount rate, businesses should also consider application, administration, and due diligence fees to understand the total financing cost.

Is Islamic Invoice Financing (IF-i) available in Malaysia?

Yes. Islamic Invoice Financing (IF-i) is widely available in Malaysia and operates under Shariah-compliant structures such as Murabahah or Wakalah. Instead of charging interest, providers apply a pre-agreed profit margin that is disclosed before the financing begins. IF-i is commonly chosen by Muslim-owned businesses, government contractors, and companies that require Shariah-compliant financing.

Which banks and providers offer invoice financing in Malaysia?

Invoice financing is available from both traditional banks and alternative financing providers in Malaysia. Major financial institutions include Maybank, Maybank Islamic, CIMB, CIMB Islamic, OCBC, and Hong Leong Bank, while digital financing platforms such as Funding Societies and CapBay offer faster application processes and lower minimum invoice requirements.

Can a new business apply for invoice financing?

Eligibility requirements vary by provider, but most lenders prefer businesses with at least six to twelve months of operating history and invoices issued to creditworthy customers. While newly established businesses may face stricter requirements, some providers place greater emphasis on the buyer's creditworthiness, particularly when supplying large corporations or government agencies.