Managing payroll in Malaysia often feels like a race against deadlines, especially when you have to ensure every cent of your statutory deductions is spot on. Mistakes in calculating the EPF contribution rate don’t just frustrate your team; they expose your business to unnecessary legal risks and heavy penalties that can disrupt your cash flow.

Struggling with manual spreadsheets or outdated processes makes it nearly impossible to keep up with the latest regulations from the Kumpulan Wang Simpanan Pekerja (KWSP) Malaysia that change as your business grows. One small miscalculation in a monthly contribution can lead to compliance headaches and audit issues that drain your time and focus away from more important tasks.

To stay ahead and protect your company’s reputation, you need a way to automate these tedious tasks once and for all. By integrating a modern human resource management system, you can eliminate manual errors, ensure 100% accuracy in every deduction, and finally focus on growing your workforce while the technology handles the compliance for you.

Key Takeaways

|

By integrating a centralized Human Resource Management (HRM) software system, businesses can fully automate complex payroll calculations, guarantee strict statutory compliance, and ensure that employees receive accurate, timely payouts every single time.

Why EPF Framework Matter For Your Business

The EPF Act 1991 is Malaysia’s statutory framework that mandates retirement savings contributions from all private sector employers and their employees — including Malaysian citizens, Permanent Residents, and increasingly, foreign workers. Every business that hires at least one eligible employee must register with KWSP and remit contributions on a monthly basis.

Compliance with this framework is not optional. Failing to contribute accurately or on time exposes employers to late payment penalties, dividend restitution claims, and criminal liability under Section 43(2) of the EPF Act 1991, which carries a fine of up to RM10,000 or imprisonment of up to three years.

In May 2024, KWSP launched the EPF account restructuring initiative, reorganizing member savings into three accounts — Akaun Persaraan (75%), Akaun Sejahtera (15%), and Akaun Fleksibel (10%) — without changing the total contribution rate. For businesses with aging workforces, using payroll software for managing retirement-age employee contributions helps ensure that reduced rates for employees aged 60 and above are applied correctly at every payroll cycle.

Key compliance timelines employers must follow:

Register with KWSP: within 7 days of hiring your first employee

Remit contributions: by the 15th of the following month via i-Akaun

Maintain accurate employee data: as age and residency status directly determine the applicable contribution rates

Detailed Breakdown of the EPF Contribution Rate Malaysia

| Age Group | Wage Bracket | Employee Rate (%) | Employer Rate (%) | Total (%) |

|---|---|---|---|---|

| Below 60 (Malaysian / PR) |

≤ RM5,000 | 11% | 13% | 24% |

| Below 60 (Malaysian / PR) |

> RM5,000 | 11% | 12% | 23% |

| 60 & above (Malaysian / PR) |

All wages | 0%* | 4% | 4% |

| 60 & above (Non-Malaysian) |

All wages | 5.5% | RM5.00 / month | — |

The statutory EPF contribution rate Malaysia is meticulously structured to balance the need for adequate retirement savings with the immediate financial realities of both employees and employers. The rates are primarily dictated by the employee’s age and their monthly wage bracket. It is crucial for payroll administrators to apply the correct percentages to avoid underpayment or overpayment.

Standard Rates for Employees Below 60 Years Old

For the majority of the workforce,specifically Malaysian citizens and Permanent Residents (PR) aged below 60 years, the contribution rates are divided into two main wage categories:

- Monthly Wages of RM5,000 and Below: To support lower-income earners in building a substantial retirement nest egg, the employer is mandated to contribute a higher percentage. The employer’s contribution rate is set at 13%, while the employee contributes 11% of their monthly salary.

- Monthly Wages Exceeding RM5,000: For employees earning a higher income, the employer’s mandatory contribution rate is slightly reduced to 12%. The employee’s contribution remains at 11%.

This tiered approach demonstrates a progressive social policy, ensuring that those with lower disposable incomes receive a proportionally larger boost to their retirement funds directly from their employers.

Rates for Employees Aged 60 and Above

Recognizing the changing dynamics of the aging workforce and to encourage the continued employment of senior citizens, the EPF contribution rates are significantly reduced once an employee reaches the age of 60. This reduction lessens the financial burden on employers hiring older workers and increases the take-home pay for the employees themselves.

- Employer Contribution: The mandatory contribution from the employer drops to a flat rate of 4%, regardless of whether the monthly wage is above or below RM5,000.

- Employee Contribution: The mandatory employee deduction is entirely waived, bringing the rate to 0%. However, employees in this age bracket have the option to voluntarily continue contributing if they wish to keep growing their retirement funds.

Employees Aged 60 and Above (Non-Malaysian Citizens)

It is important to note that the reduced rates for senior citizens generally apply to Malaysian citizens and Permanent Residents. For non-Malaysian citizens aged 60 and above, the employer is required to contribute RM5.00 per month, while the employee contributes 5.5% of their monthly wage. However, this is subject to ongoing legislative updates, which brings us to the topic of expatriate workers.

Navigating EPF for Foreign Employees and Expatriates

Mandatory EPF for Foreign Workers Historically voluntary (RM5 employer / 11% employee), managing payroll for foreign workers in Malaysia is transitioning toward mandatory EPF contributions. This phased mandate aims for parity with local standards, eventually requiring employers to budget for the standard 12% or 13% contribution rates. HR departments must stay vigilant for official KWSP and Ministry of Finance announcements to adjust their payroll systems as these changes take full effect.

What is Subject to EPF?

A common pitfall in payroll processing is misunderstanding which components of an employee’s remuneration are subject to EPF deductions. The EPF Act 1991 provides a specific definition of “wages” for the purpose of contribution calculations. Properly defining gross pay and identifying EPF-liable elements is non-negotiable for compliance.

Payments Subject to EPF Contribution

All monetary payments made as wages under a contract of service or apprenticeship are generally subject to EPF deductions, including but not limited to the following:

| Allowance Type | Subject to EPF? | Notes |

|---|---|---|

| Basic salary | Yes | Always included. |

| Housing allowance | Yes | If fixed monthly. |

| Travel allowance | No | Exempt under EPF Act. |

| Overtime pay | Yes | Included. |

| Bonus | No | Exempt. |

Payments Exempted from EPF Contribution

The EPF Act explicitly excludes the following payments from the definition of wages. Employers must exclude these from EPF calculations to avoid over-deducting from employees and overpaying from company funds:

| Payment Component | Description |

|---|---|

| Overtime Payments | Any payment made for work performed beyond normal working hours. |

| Gratuity | A lump sum given to an employee upon retirement or at the end of a contract as a token of appreciation. |

| Retirement Benefits | Specific pension or retirement fund payouts independent of the EPF system. |

| Retrenchment, Lay-off, or Termination Benefits | Compensation paid to employees due to the cessation of employment. |

| Travel Allowances | Reimbursements or allowances provided specifically to cover the cost of official business travel. |

| Director's Fee | Fees paid to Board of Directors members, provided they are not also salaried employees of the company. |

| Gifts and Customary Payments | Non-contractual gifts such as festive 'ang pows' or wedding gifts given to employees. |

The Calculation Method: Third Schedule vs. Exact Percentage

Payroll administrators are legally advised to use the Third Schedule (Jadual Ketiga) rather than exact percentage calculations. This system uses fixed wage bands to determine contributions, ensuring uniformity across the workforce. If you choose manual percentage calculation, you must round up every result containing cents to the next Ringgit failing to do so is a frequent compliance trap that leads to actionable underpayments.

Scenario 1: Employee Earning RM 4,500 (Below RM 5,000)

Let’s consider an employee aged 30 earning a basic salary of RM 4,000 and a fixed monthly allowance of RM 500. The total EPF-liable wage is RM 4,500.

- Employer Contribution (13%): 13% of 4,500 is RM 585.

- Employee Contribution (11%): 11% of 4,500 is RM 495.

- Total Remittance to EPF: RM 1,080.

Note: If the wage was RM 4,500.50, the exact 11% would be RM 495.055. This must be rounded up to RM 496. Consulting the Third Schedule eliminates this rounding ambiguity.

Scenario 2: Employee Earning RM 6,500 (Above RM 5,000)

Consider an employee aged 45 earning a basic salary of RM 6,500.

- Employer Contribution (12%): 12% of 6,500 is RM 780.

- Employee Contribution (11%): 11% of 6,500 is RM 715.

- Total Remittance to EPF: RM 1,495.

The Impact of EPF on Overall Compensation and Benefits

While the statutory EPF contribution rate Malaysia establishes the legal minimum, forward-thinking organizations frequently leverage the EPF system as a strategic tool for talent acquisition and retention. In a competitive labor market, offering comprehensive employee benefits packages that exceed statutory requirements can significantly differentiate an employer.

Many corporations offer enhanced employer EPF contributions as part of their remuneration strategy. For instance, an employer might choose to contribute 15% or even 16% instead of the mandatory 12% or 13%. This voluntary excess contribution serves multiple purposes:

- Tax Efficiency: From a corporate perspective, employer contributions to the EPF are tax-deductible expenses up to a limit of 19% of the employee’s remuneration. By maximizing this deduction, companies can optimize their corporate tax liabilities while simultaneously rewarding their staff.

- Long-Term Retention: Enhanced EPF contributions are highly valued by employees who are conscious of their retirement planning. It acts as a powerful retention mechanism, as employees recognize the long-term financial benefits of remaining with an organization that actively accelerates their wealth accumulation.

- Employee Morale: Demonstrating a commitment to an employee’s future financial security fosters loyalty, higher job satisfaction, and a stronger employer-employee relationship.

Employees themselves also have the option to increase their individual contribution rate beyond the statutory 11%. They can submit a formal request to their employer and the EPF board to deduct a higher percentage (e.g., 12%, 15%) from their monthly wages. This allows financially savvy employees to enforce disciplined savings behavior and take advantage of the historically stable and competitive dividend rates offered by the KWSP.

Employer Compliance: Deadlines, Penalties, and Audits

The regulatory framework surrounding the EPF is stringently enforced. The KWSP board possesses extensive powers to audit employers, demand documentation, and penalize non-compliance. Understanding the operational timelines is critical for any business.

Payment Deadlines

Employers are legally required to remit both the employer’s and the employee’s share of the EPF contributions to the KWSP by the 15th day of the following month. For example, contributions deducted from wages earned in January must be successfully credited to the EPF by the 15th of February. It is important to note that this deadline refers to the date the funds must be received and cleared by the EPF, not merely the date the payment is initiated.

Penalties for Late Payment or Non-Payment

Failure to meet the 15th-of-the-month deadline triggers immediate consequences. The EPF Act stipulates that late payments are subject to:

- Late Payment Charges: A penalty calculated based on the outstanding amount and the number of days delayed.

- Dividend Restitution: The employer is required to compensate the employee for any loss of dividends that would have accrued had the contribution been made on time.

More severely, chronic non-compliance or deliberate evasion of EPF responsibilities is a criminal offense. Under Section 43(2) of the EPF Act 1991, employers found guilty of failing to pay contributions can face imprisonment for up to three years, a fine not exceeding RM10,000, or both. Furthermore, company directors can be held personally liable for unpaid EPF contributions under Section 46 of the Act, meaning their personal assets can be targeted to recover the owed amounts.

The e-Caruman System

To facilitate smooth compliance, the KWSP mandates the use of the i-Akaun (Majikan) portal and the e-Caruman facility. Manual submissions via physical forms (Form A) and cheques at physical counters have been largely phased out to improve efficiency and reduce errors. Employers must generate their contribution details electronically, either by direct data entry on the portal or by uploading a specialized text file generated by their payroll software. Payments are then executed via integrated online banking channels (FPX) or direct debit authorizations.

The New EPF Account Restructuring (2026): Akaun Persaraan, Sejahtera, and Fleksibel

| Principle | Core Requirement | HR Application Example | Key Action |

| 1. Consent | Process data only with clear, specific consent | Signed consent forms during employee onboarding | Use active opt-ins; avoid pre-ticked boxes |

| 2. Notice & Choice | Inform individuals of data collection purpose & give choice | Bilingual Privacy Notice (BM & EN) before recruitment | Include DPO contact & consequences of non-provision |

| 3. Disclosure | Limit data sharing to legitimate purposes & authorized parties | Share payroll data only with contracted vendors | Sign Data Processing Agreements (DPA) with third parties |

| 4. Security | Protect data against unauthorized access or breaches | Encrypt employee databases + role-based access controls | Implement MFA, regular security audits, staff training |

| 5. Retention | Delete data once purpose is fulfilled or retention period ends | Keep tax records for 7 years; delete unsuccessful applications after 12 months | Document retention policy + schedule secure disposal |

| 6. Data Integrity | Ensure data is accurate, complete, and up-to-date | Validate employee inputs via self-service portals | Schedule periodic data audits; encourage employee updates |

| 7. Access Rights | Honor individuals’ right to access & correct their data | Respond to Subject Access Requests (SAR) within 21 days | Prepare identity verification flow + redact third-party data |

The New EPF Account Restructuring (2026): Akaun Persaraan, Sejahtera, and Fleksibel

In a landmark move to adapt to the changing economic realities and the evolving needs of its members, the EPF implemented a major restructuring of member accounts effective May 2024. Previously, contributions were split into Account 1 (70%) and Account 2 (30%). The new structure introduces three distinct accounts, fundamentally altering how members interact with their savings.

Understanding this restructuring is important for HR professionals, as employees frequently turn to their HR departments with questions regarding their statutory deductions and how their money is being allocated.

Akaun Persaraan (Account 1)

Akaun Persaraan serves as the core retirement fund. Under the new structure, 75% of the monthly EPF contribution rate Malaysia is allocated here. The primary objective of this account remains unchanged: to accumulate wealth for post-retirement life. Funds in this account cannot be withdrawn until the member reaches the age of 55, ensuring that the bulk of the savings is preserved for its intended purpose.

Akaun Sejahtera (Account 2)

Akaun Sejahtera receives 15% of the monthly contributions. This account is designed to address life cycle needs that contribute to overall well-being before retirement. Members can utilize funds from Akaun Sejahtera for specific, approved purposes, such as purchasing a first home, funding tertiary education, covering critical medical expenses, or paying for approved insurance products.

Akaun Fleksibel (Account 3)

The most significant addition is the Akaun Fleksibel, which receives 10% of the monthly contributions. This account acts as an emergency fund, providing members with short-term liquidity. Members are allowed to withdraw funds at any time for any purpose, subject to a minimum withdrawal amount (typically RM50). This innovation acknowledges the financial pressures faced by the workforce and provides flexibility without compromising long-term retirement savings.

For employers, this restructuring does not change the total EPF contribution rate Malaysia or the remittance process. The employer still remits the total 23% or 24% (combined employer and employee share) as a single lump sum. The EPF’s internal backend systems automatically distribute the funds into the three accounts based on the 75:15:10 ratio.

Streamlining EPF Management in the Modern Payroll Cycle

Given the intricate rules governing the EPF contribution rate Malaysia, ranging from age-based tiers to specific salary component exemptions. Relying on manual calculations or outdated spreadsheet templates is a high-risk strategy. Human error in data entry, misinterpretation of the Third Schedule, or failing to update rates when an employee turns 60 can lead to a cascade of compliance failures.

Transitioning to a modern payroll process powered by advanced technology is the most effective way to mitigate these risks. Automated Human Resource Information Systems (HRIS) and payroll software are designed to handle the heavy lifting of statutory compliance effortlessly.

A robust payroll system will automatically:

- Identify which salary components are subject to EPF and which are exempt.

- Apply the correct contribution rates based on the employee’s date of birth and residency status.

- Calculate exact amounts using the integrated Third Schedule logic, ensuring perfect rounding.

- Generate the necessary e-Caruman text files for seamless uploading to the KWSP i-Akaun portal.

- Maintain historical records of all deductions for audit purposes and generating EA forms at year-end.

Implementing HashMicro’s ERP centralizes employee data and payroll, eliminating silos to ensure absolute accuracy in EPF remittances. This automation drastically reduces processing time, freeing HR professionals from tedious administrative tasks to focus on strategic initiatives like talent development and organizational culture.

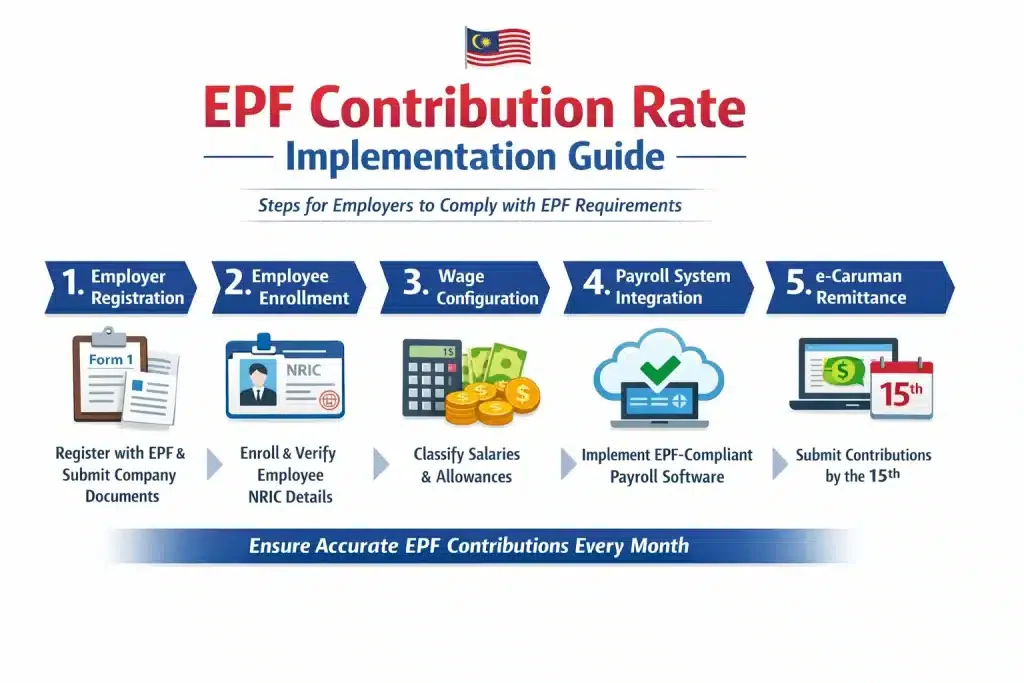

Step-by-Step Implementation Guide for Employers

Transitioning from understanding the legal framework to executing accurate payroll processes requires a highly systematic approach. For new businesses, foreign investors setting up operations in Malaysia, or HR professionals looking to overhaul their current systems, following a structured implementation plan ensures seamless compliance with the EPF contribution rate Malaysia.

Step 1: Official Employer Registration

Before any deductions can occur, a business must register with the EPF within seven days of hiring its very first employee. This critical step is accomplished by submitting Form 1 (Borang 1) along with the necessary company incorporation documents (such as SSM certificates) via the EPF’s online portal or at a physical EPF branch.

Step 2: Employee Enrollment and Data Synchronization

Once the corporate entity is registered, every eligible employee must be enrolled under the company’s profile. Employers must verify that their new hires are registered EPF members. Accurate synchronization of employee data, particularly their National Registration Identity Card (NRIC) numbers and exact dates of birth is critical, as age directly dictates the applicable statutory contribution rate.

Step 3: Wage Classification and Rate Configuration

The most technically demanding step in implementation is configuring your payroll system to correctly identify what constitutes “wages” under the EPF Act 1991. Employers must meticulously separate base salaries, bonuses, arrears of wages, and fixed allowances (which are subject to EPF) from travel reimbursements, overtime pay, gratuities, and retirement benefits (which are strictly exempt).

Step 4: Integration with Cloud-Based Payroll Software

Manual calculation via spreadsheets is highly susceptible to human error and is generally discouraged for growing businesses. Companies should implement LHDN-approved and EPF-compliant cloud payroll software. These modern systems automatically update their internal algorithms whenever the Malaysian government announces changes to statutory rates during the annual budget.

Step 5: Monthly Remittance via e-Caruman

The final step in the monthly cycle is the actual financial remittance. Employers are legally mandated to remit both the employer’s and employee’s shares to the EPF board by the 15th of the following month. The EPF’s i-Akaun (Employer) portal features the highly efficient e-Caruman facility.

Advanced Practices for Strategic Payroll Management

Beyond basic legal compliance, progressive organizations leverage the EPF framework to enhance their overall human capital strategy. Adopting advanced practices regarding the EPF contribution rate Malaysia can transform a mundane statutory obligation into a core component of employer branding.

1. Implementing Voluntary Excess Contributions

Offering a 15%, 16%, or even 18% employer contribution is a highly effective executive retention strategy. It provides distinct tax advantages for the company corporate tax deductions are allowed for employee remuneration up to a 19% EPF contribution limit, while significantly boosting the employee’s retirement nest egg.

2. Conducting Periodic Internal Payroll Audits

Advanced HR departments conduct rigorous internal payroll audits. These audits involve cross-referencing EPF submission files (Form A) against original employment contracts, promotion letters, and daily attendance records to identify discrepancies in allowance classifications or missed age-bracket updates.

3. Integrating Financial Wellness Programs

Modern employers are increasingly recognizing that financial stress impacts productivity. By integrating EPF education into corporate wellness programs. explaining compounding interest and how to leverage Account 2 companies, demonstrate a profound commitment to the holistic well-being of the workforce.

4. Utilizing API Integrations

For enterprise-level organizations, advanced payroll management involves utilizing APIs provided by modern Human Resource Information Systems (HRIS) to create a direct pipeline to the EPF system. This ensures that salary adjustments and bonus payouts are instantly and flawlessly reflected in the EPF database.

Conclusion

The EPF contribution rate Malaysia is a cornerstone of the nation’s labor framework, designed to ensure the long-term financial security of the workforce. For employers, mastering the nuances of EPF from accurate wage classification to timely monthly remittances is essential for maintaining legal compliance and fostering a secure work environment.

By leveraging modern payroll technology, businesses can automate complex calculations, stay ahead of regulatory changes, and ensure their employees’ future financial well-being, ultimately supporting the success of both the organization and its people.

Stop wasting your time on manual spreadsheets that leave your business vulnerable to costly KWSP audit errors and penalties. You can take full control of your statutory compliance today by booking a free demo to see how our automated system handles every deduction with absolute precision.

Frequently Asked Questions About EPF

Is EPF mandatory for foreign workers and expatriates?

Yes, the regulation is transitioning toward mandatory EPF contributions for foreign workers to reach parity with local standards (the standard 12% or 13% employer rate). Historically, it was voluntary with a minimum RM5 employer contribution and 11% employee contribution. Employers should monitor official KWSP announcements for full implementation details.

Are overtime payments or travel allowances subject to EPF?

No. The EPF Act explicitly exempts certain payments from deductions. These exemptions include overtime payments, travel allowances, gratuities, retirement benefits, retrenchment/termination benefits, director’s fees, and non-contractual gifts.

When is the legal deadline for employers to remit EPF contributions?

Employers must remit both the employer’s and the employee’s share to the KWSP by the 15th day of the following month. For example, January deductions must be successfully credited to the EPF by February 15th.

What are the penalties if an employer is late or fails to pay EPF contributions?

Late payments will incur late payment charges and dividend restitution to compensate the employee. Furthermore, chronic non-compliance is a criminal offense under Section 43(2) of the EPF Act 1991, punishable by up to three years of imprisonment, a fine of up to RM10,000, or both. Company directors can also be held personally liable for unpaid amounts.

Should employers calculate EPF using exact percentages or the Third Schedule?

Payroll administrators are legally advised to use the Third Schedule (Jadual Ketiga) instead of exact percentage calculations. The schedule uses fixed wage bands that ensure uniformity and eliminate compliance traps caused by incorrect decimal rounding.

Can an employee above 60 opt out of EPF?

For Malaysian citizens and PRs aged 60 and above, the mandatory employee EPF contribution is already 0%, so there is no employee deduction to opt out from. However, the employer must still contribute 4%, and employees may choose to make voluntary contributions if they want to continue growing their retirement savings.