Every fixed asset loses value as your business uses it. Accumulated depreciation records the total depreciation charged on that asset from the day it was ready for use until the current reporting period.

In Malaysia, accumulated depreciation follows accounting principles under Malaysian Financial Reporting Standards (MFRS) 116 or Malaysian Private Entities Reporting Standards (MPERS) Section 17 for small and medium enterprises. This differs from capital allowance claimed to Lembaga Hasil Dalam Negeri (LHDN), so financial statement values may not match tax values.

Clear depreciation records help you understand asset value, profit impact, and tax differences more confidently. Businesses can also use accounting tools to manage depreciation records more consistently. You will see how accumulated depreciation works on the balance sheet, how to calculate it using Ringgit Malaysia examples, and how Malaysian businesses in manufacturing, construction, and F&B can avoid common reporting mistakes.

Key Takeaways

Accumulated depreciation is the running total of depreciation recorded against a fixed asset from the time it is ready for use.

It appears on the balance sheet as a contra asset account, reducing the value of Property, Plant and Equipment (PPE).

Malaysian businesses use Malaysian Financial Reporting Standards (MFRS) 116 for accounting and Lembaga Hasil Dalam Negeri (LHDN) capital allowance for tax.

Straight-line and reducing balance methods are commonly used to calculate depreciation for business assets in Malaysia.

Accurate depreciation records are easier to manage when asset values, journal entries, and financial reports stay connected in one system. Accounting software helps keep those records organised and reduces the risk of manual reporting mistakes.

What Is Accumulated Depreciation?

Accumulated depreciation is the total depreciation recorded against a fixed asset since it was ready for use. It is not one period’s expense, but the running total that shows how much asset value has already been charged over time.

In Malaysia, depreciation follows Malaysian Financial Reporting Standards (MFRS) 116, while SMEs may refer to Malaysian Private Entities Reporting Standards (MPERS) Section 17. Machinery, vehicles, buildings excluding land, office equipment, and leasehold improvements can be depreciated, while intangible assets follow different treatments such as goodwill accounting.

Accumulated Depreciation Account on the Balance Sheet

The accumulated depreciation account appears on the balance sheet under Property, Plant and Equipment (PPE). It works as a contra asset account, which means it reduces the recorded value of a fixed asset instead of being shown as a separate liability. The asset still belongs to the business, but its carrying amount becomes lower as depreciation builds up. Here is a simple example in Ringgit Malaysia.

| Item | Amount (RM) |

| Equipment at cost | 150,000 |

| Less accumulated depreciation | (52,000) |

| Net Book Value (NBV) | 98,000 |

Net Book Value (NBV) is the amount left after accumulated depreciation is deducted from the original asset cost. In this example, the equipment was bought for RM150,000, and RM52,000 has already been recorded as accumulated depreciation. That leaves RM98,000 as the value shown on the balance sheet. Accumulated depreciation affects the three main financial statements in different ways:

- Balance sheet: Accumulated depreciation reduces the gross value of PPE to calculate Net Book Value.

- Income statement: The business records depreciation expense for the current period as an operating expense, which reduces profit before tax.

- Cash flow statement: Depreciation expense is added back under operating activities because it is a non-cash expense. No new cash leaves the business when depreciation is recorded.

The key difference is that depreciation expense only covers one accounting period, while accumulated depreciation shows the total depreciation recorded over time.

With accounting software in Malaysia, each period’s depreciation expense can flow into the income statement and increase the accumulated depreciation balance on the balance sheet more consistently. On the cash flow statement, the same expense is added back because it does not involve a new cash payment.

Is Accumulated Depreciation an Asset or a Liability?

Accumulated depreciation is neither an asset nor a liability. It is a contra asset account, which means it reduces the value of a fixed asset on the balance sheet.It normally has a credit balance, but that does not make it a liability. A liability means the business owes money or has an obligation to another party. Accumulated depreciation does not create any payment obligation.

Instead, it reduces the gross value of Property, Plant and Equipment (PPE) to show a more realistic carrying value. You will usually see it on the asset side of the balance sheet, below PPE, not under liabilities.Think of it like the odometer on a company vehicle. The mileage reading does not create a debt. It simply shows how much use the vehicle has absorbed over time.

"Accumulated depreciation should be treated as a contra asset, not a liability. It reduces the carrying value of fixed assets under Property, Plant and Equipment (PPE), while the credit balance simply reflects recorded asset usage over time."

Accumulated Depreciation Debit or Credit?

Accumulated depreciation normally has a credit balance. It increases on the credit side because it reduces the carrying value of a fixed asset, while fixed assets usually have a debit balance. When a business records yearly depreciation, the depreciation expense is debited and accumulated depreciation is credited.

| Account | Debit (RM) | Credit (RM) |

|---|---|---|

| Depreciation Expense | 13,000 | |

| Accumulated Depreciation | 13,000 |

This entry shows that RM13,000 has been charged as the current period’s depreciation expense. At the same time, the accumulated depreciation account increases by RM13,000. The asset cost stays unchanged in the equipment account unless the asset is sold, written off, or disposed of.

Accumulated depreciation is debited when the asset leaves the business. For example, a machine costs RM150,000 and has accumulated depreciation of RM91,000 after seven years. Its Net Book Value (NBV) is RM59,000. If the machine is sold for RM70,000, the business records a gain of RM11,000 because the selling price is higher than the NBV.

| Account | Debit (RM) | Credit (RM) |

|---|---|---|

| Cash or Bank | 70,000 | |

| Accumulated Depreciation | 91,000 | |

| Equipment | 150,000 | |

| Gain on Disposal | 11,000 |

If the same machine is sold for RM50,000, the business records a loss of RM9,000 because the selling price is lower than the NBV.

| Account | Debit (RM) | Credit (RM) |

|---|---|---|

| Cash or Bank | 50,000 | |

| Accumulated Depreciation | 91,000 | |

| Loss on Disposal | 9,000 | |

| Equipment | 150,000 |

Accumulated Depreciation Formula and How to Calculate It

The accumulated depreciation formula depends on the depreciation method your business uses. According to KTP & Company PLT’s explanation of MFRS 116 in Malaysia, depreciation for Property, Plant and Equipment should reflect how an asset’s value is allocated over its useful life, so businesses need to choose a method that matches how the asset is used.

Straight-line method

The straight-line method is commonly used because it is simple and predictable. To find annual depreciation, subtract the salvage value from the original cost and divide the result by useful life.

For example, a manufacturing company buys a factory machine for RM150,000. The machine has a salvage value of RM20,000 and a useful life of 10 years. Annual depreciation is RM13,000 because RM150,000 minus RM20,000 equals RM130,000, then divided by 10 years.

| Year | Annual Depreciation (RM) | Accumulated Depreciation (RM) | Net Book Value (RM) |

|---|---|---|---|

| 0 | 150,000 | ||

| 1 | 13,000 | 13,000 | 137,000 |

| 2 | 13,000 | 26,000 | 124,000 |

| 3 | 13,000 | 39,000 | 111,000 |

| 4 | 13,000 | 52,000 | 98,000 |

| 5 | 13,000 | 65,000 | 85,000 |

Under this method, the depreciation expense stays the same each year. The accumulated depreciation increases by RM13,000 annually, while the Net Book Value (NBV) decreases at the same pace. This method works well for assets that provide stable use over time, such as office equipment, furniture, and some factory machines.

Reducing balance method

The reducing balance method applies a fixed depreciation rate to the asset’s opening NBV each year. It creates higher depreciation in earlier years and lower depreciation later. This method is useful when an asset loses value faster at the beginning of its useful life.

Using the same RM150,000 machine and a 20% depreciation rate, the first year depreciation is RM30,000. In year two, the 20% rate is applied to the new opening NBV of RM120,000, not the original cost.

| Year | Opening NBV (RM) | Depreciation 20% (RM) | Accumulated Depreciation (RM) | Closing NBV (RM) |

|---|---|---|---|---|

| 1 | 150,000 | 30,000 | 30,000 | 120,000 |

| 2 | 120,000 | 24,000 | 54,000 | 96,000 |

| 3 | 96,000 | 19,200 | 73,200 | 76,800 |

| 4 | 76,800 | 15,360 | 88,560 | 61,440 |

| 5 | 61,440 | 12,288 | 100,848 | 49,152 |

By year five, accumulated depreciation reaches RM100,848, while the closing NBV is RM49,152. Compared with straight-line depreciation, the reducing balance method records a larger expense earlier. That makes it more suitable for assets that lose efficiency quickly, such as heavy equipment, vehicles, and technology assets.

Another method is the Sum-of-Years Digits method. It also records higher depreciation in earlier years, but it uses a fraction based on the remaining useful life of the asset. Malaysian businesses usually use it less often because straight-line and reducing balance methods are easier to explain, apply, and review during reporting.

Accounting Depreciation vs Capital Allowance in Malaysia

Accounting depreciation

Used for financial reporting under Malaysian Financial Reporting Standards (MFRS) 116. It helps show how much of an asset’s cost has been used over its useful life, based on the depreciation method selected by management.

Capital allowance

Used for tax filing to Lembaga Hasil Dalam Negeri (LHDN). It is governed by the Income Tax Act 1967 and applies to qualifying capital expenditure on assets used for business purposes. LHDN Public Ruling No. 12/2014 states that capital allowances are deductible in determining statutory business income, while the rates are prescribed under Schedule 3 of the Income Tax Act 1967.

Accounting depreciation example

For financial reporting, the RM150,000 machine can be depreciated over 10 years under Malaysian Financial Reporting Standards (MFRS) 116, based on the company’s chosen method and useful life.

Capital allowance example

For tax filing, the same RM150,000 machine follows Lembaga Hasil Dalam Negeri (LHDN) capital allowance rates, such as 20% Initial Allowance and 14% Annual Allowance for general plant and machinery.

| Year | Accumulated Depreciation, Straight-Line | Net Book Value, Accounting | Capital Allowance | Tax Written Down Value |

| 0 | – | RM150,000 | – | RM150,000 |

| 1 | RM13,000 | RM137,000 | RM50,000, IA 20% plus AA 14% | RM100,000 |

| 2 | RM26,000 | RM124,000 | RM21,000, AA 14% | RM79,000 |

| 3 | RM39,000 | RM111,000 | RM21,000, AA 14% | RM58,000 |

The table shows why accounting and tax records can show different asset values. After three years, the accounting Net Book Value is RM111,000, while the Tax Written Down Value is RM58,000 because capital allowance is claimed faster in the early years.

This creates a temporary difference that may affect deferred tax. For business owners, the key point is clear: do not use accounting depreciation as the LHDN claim, and do not apply LHDN capital allowance rates as your accounting policy without checking the reporting impact.

Accumulated Depreciation Examples by Industry

Accumulated depreciation can look different across industries because each business uses different types of assets. A factory machine, an excavator, and kitchen equipment do not lose value in the same way. That is why Malaysian businesses should choose a depreciation method that reflects how the asset is actually used.

Manufacturing

For manufacturing companies, factory machinery is often depreciated using the straight-line method because the asset usually supports production over several years in a stable pattern. For example, a manufacturer buys a factory machine for RM150,000, with a salvage value of RM20,000 and a useful life of 10 years. The annual depreciation is RM13,000.

By the end of year three, the accumulated depreciation is RM39,000. The Net Book Value (NBV) becomes RM111,000. This method works well when the machine is expected to generate similar production benefits each year.

Property and Construction

Construction companies often use heavy equipment such as excavators, cranes, and loaders. These assets may lose value faster in the early years because they are exposed to heavy site usage, rough conditions, and higher maintenance needs. In this case, the reducing balance method may give a more realistic view of asset usage.

For example, a construction company buys an excavator for RM300,000 and applies a 20% reducing balance rate. In year one, depreciation is RM60,000. In year two, depreciation is RM48,000 because the rate applies to the reduced book value of RM240,000. In year three, depreciation is RM38,400. By the end of year three, accumulated depreciation reaches RM146,400, and the NBV becomes RM153,600.

Retail and F&B

Retail and F&B businesses usually depreciate assets such as commercial ovens, display chillers, coffee machines, and point-of-sale equipment. These assets often provide steady use over their useful life, so the straight-line method is usually easier to apply.

For example, a restaurant buys kitchen equipment for RM25,000, with a salvage value of RM2,500 and a useful life of 5 years. The annual depreciation is RM4,500. After three years, accumulated depreciation is RM13,500, and the NBV is RM11,500.

These examples show why one method does not fit every industry. Manufacturing may prefer straight-line depreciation for stable production assets, construction may use reducing balance for equipment with heavier early usage, while F&B businesses often need a simple method for smaller operational assets.

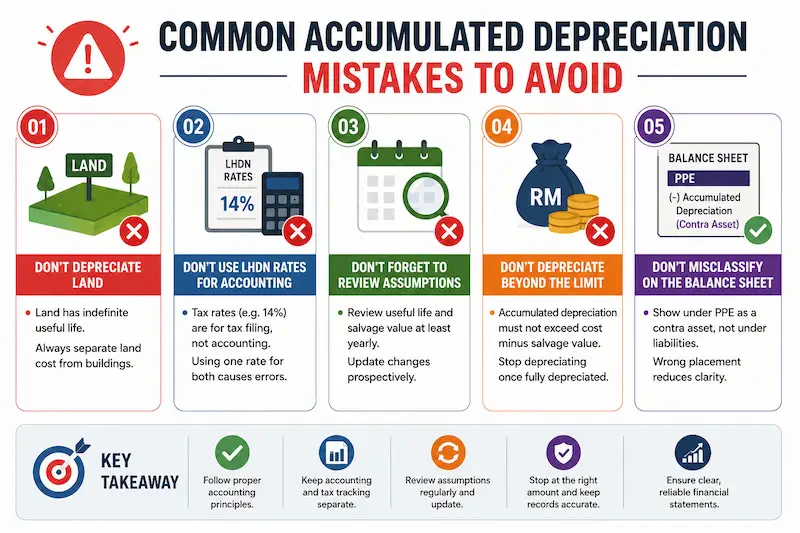

Common Accumulated Depreciation Mistakes to Avoid

1. Depreciating land

Land should not be depreciated because it usually has an indefinite useful life. A common mistake happens when land and buildings are purchased together, then the full purchase cost is depreciated without separating the land portion. This can overstate depreciation expense and understate the asset value on the balance sheet.

2. Using LHDN rates for accounting depreciation

Capital allowance rates from Lembaga Hasil Dalam Negeri (LHDN), such as 14% for certain plant and machinery, are for tax filing. They are not automatically the same as accounting depreciation rates under Malaysian Financial Reporting Standards (MFRS) 116. Without proper tracking through financial management software, using one rate for both accounting and tax can make financial reports inaccurate and may create tax filing issues.

3. Forgetting to review useful life and salvage value

MFRS 116 paragraph 51 requires the residual value and useful life of an asset to be reviewed at least at each financial year end. If expectations change, the adjustment should be handled prospectively as a change in accounting estimate. Many businesses set the useful life once and forget to review it, which can make depreciation figures outdated.

4. Letting accumulated depreciation exceed depreciable amount

Accumulated depreciation should not exceed the asset cost minus its salvage value. Once the asset is fully depreciated, the business should stop recording depreciation expense even if the asset is still being used. Continuing to depreciate it can distort both profit and Net Book Value (NBV).

5. Classifying accumulated depreciation in the wrong section

Accumulated depreciation should appear below Property, Plant and Equipment (PPE) as a contra asset account. It should not be shown under liabilities because it does not represent money owed to another party. Wrong classification can make the balance sheet harder to read and reduce confidence during audit review.

When to Replace vs Continue Depreciating an Asset

Accumulated depreciation can help management decide whether an asset still makes business sense. The decision should not rely only on the remaining value in the accounts, but also on repair costs, downtime, output quality, and operational risk.

A business may continue depreciating an asset when the asset still performs reliably, maintenance costs remain manageable, and the Net Book Value (NBV) is still above the expected salvage value. For example, if a RM150,000 machine still runs well and annual maintenance stays below its RM13,000 depreciation charge, keeping the asset may be more practical than replacing it too early.

A business should consider replacing an asset when the NBV is close to the salvage value, downtime becomes frequent, or annual maintenance costs exceed the depreciation charge. In year 8, the same RM150,000 machine may have accumulated depreciation of RM117,000 and an NBV of RM33,000. If annual maintenance reaches RM22,000 while annual depreciation is RM13,000, the maintenance to depreciation ratio is about 1.7 times.

Many financial controllers start reviewing replacement options when maintenance spending exceeds 1.5 times the annual depreciation charge. At that point, the asset may look inexpensive in the accounts, but costly to operate in daily business.

Conclusion

Accumulated depreciation helps businesses see how fixed assets affect financial reports over time. It reduces asset value on the balance sheet, connects to depreciation expense in the income statement, and is added back in the cash flow statement because it does not involve new cash outflow.

For Malaysian businesses, accounting depreciation and tax capital allowance must be handled separately. Malaysian Financial Reporting Standards (MFRS) 116 guides financial reporting, while capital allowance follows Lembaga Hasil Dalam Negeri (LHDN) rules under the Income Tax Act 1967. The right depreciation method also depends on the asset type, industry, and how the asset supports daily operations.

Before closing the books, review the depreciation schedule, check whether useful life and salvage value still make sense, and confirm that the accounting method aligns with auditor expectations. Businesses that need clearer guidance can also arrange a free consultation to review depreciation records and avoid reporting mistakes.

FAQ About Accumulated Depreciation

FAQ

No, accumulated depreciation is not a current liability. It is a contra asset account with a credit balance. It appears under Property, Plant and Equipment (PPE) on the balance sheet and reduces the carrying value of fixed assets.

Accumulated depreciation stays in the accounting records until the asset is sold, written off, or disposed of. Depreciation expense stops once the asset reaches its salvage value. The asset can still be used in operations even after it is fully depreciated.

No, accumulated depreciation cannot exceed the depreciable amount of an asset. The maximum amount is the asset cost minus its salvage value. Once that point is reached, the business should stop recording depreciation expense.

A common journal entry records a debit to depreciation expense and a credit to accumulated depreciation. For example, a RM150,000 machine depreciated using the straight-line method may record Depreciation Expense of RM13,000 and Accumulated Depreciation of RM13,000 each year.

Accumulated depreciation does not directly determine taxable income in Malaysia. Lembaga Hasil Dalam Negeri (LHDN) uses capital allowance instead of accounting depreciation under the Income Tax Act 1967. The difference between Net Book Value (NBV) and Tax Written Down Value (Tax WDV) may create a temporary difference for deferred tax purposes.

Depreciation is the expense recorded for one accounting period. For example, a company may record RM13,000 depreciation expense for one year. Accumulated depreciation is the total depreciation recorded over time, such as RM39,000 after three years.

Accumulated depreciation does not directly affect cash flow. Depreciation is a non-cash expense because no cash leaves the business when it is recorded. In the cash flow statement, depreciation expense is added back under operating activities.