Selling a residential property in Kuala Lumpur or a commercial unit in Penang may seem simple until the Real Property Gains Tax (RPGT) payment becomes due. Many sellers only realize later that part of their profit must be paid to Lembaga Hasil Dalam Negeri Malaysia (LHDN). The final amount depends on the purchase date, eligible expenses with receipts, and the seller category, all within a 60-day filing period.

Malaysia’s property market remains active, with National Property Information Centre (NAPIC) recording over 311,000 transactions worth RM196.83 billion in 2023. Since RPGT rates under the RPGTA have changed several times, many older references may no longer match the latest LHDN rates. Understanding the current tax structure is important before selling any property in Malaysia.

Understanding RPGT can help property owners avoid surprises when selling real estate in Malaysia. This guide covers the latest RPGT rates, exemptions, calculation methods, and reporting requirements, as well as the role of accounting software in maintaining accurate records and supporting tax compliance.

Key Takeaways

Real Property Gains Tax (RPGT) can help property owners reduce tax exposure and avoid costly filing mistakes before selling any property in Malaysia.

RPGT formula allowable expenses and exemptions can significantly reduce the final tax payable on a property sale in Malaysia.

Missing RPGT filing deadlines can lead to penalties for both the seller and buyer.

Many property owners struggle to organize RPGT documents and expense records properly. Using accounting software with financial reporting and asset management features helps simplify CKHT preparation and tax calculations.

What is Real Property Gains Tax (RPGT)?

Real Property Gains Tax (RPGT), also known as Cukai Keuntungan Harta Tanah (CKHT), is a tax imposed on profits earned from selling property in Malaysia. RPGT applies to residential properties, commercial buildings, vacant land, and shares in real property companies (RPCs). The taxable amount is based on the chargeable gain, calculated from the difference between the selling price and acquisition cost after allowable deductions.

Under the Real Property Gains Tax Act 1976 (RPGTA), which serves as the legal framework for Real Property Gains Tax (RPGT) in Malaysia, tax rules apply to Malaysian citizens, permanent residents, companies incorporated in Malaysia, and non-citizens, including foreign companies, under different tax rate categories. The latest RPGT rates, exemptions, and CKHT forms are published by LHDN.

Real Property Gains Tax (RPGT) Rates in Malaysia

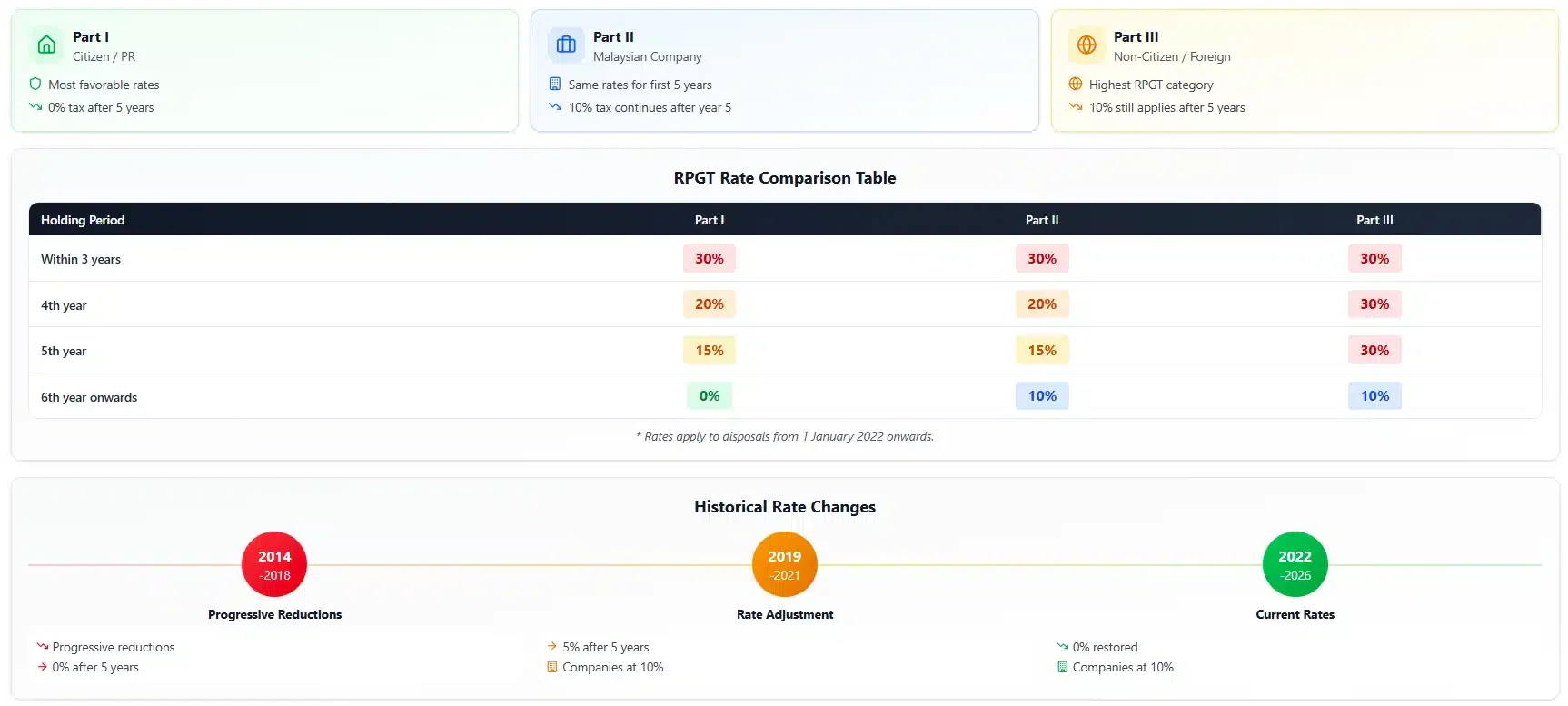

Two variables determine the rate you pay, namely how long the property was held before disposal and which disposer category applies to you. The current rates took effect on 1 January 2022 and continue to apply for the 2026 assessment year.

Disposer Categories

Under Schedule 5 of the RPGTA (Real Property Gains Tax Act 1976), taxpayers are divided into three categories based on their residency and ownership status. Each disposer category is subject to different RPGT rates depending on how long the property is held before disposal.

Citizen/PR: Applies to Malaysian citizens and permanent residents selling property under their personal name. This category receives the most favorable treatment, including a 0% RPGT rate once the property has been owned for more than five years.

Malaysian Company: Covers companies incorporated in Malaysia. While local companies enjoy the same RPGT rates as individuals during the first five years, a 10% tax rate still applies from the sixth year onwards.

Non-Citizen: Applies to non-citizens, foreign-owned companies, and other parties that do not fall under Part I or Part II. This category is subject to higher RPGT rates, including a 10% rate even after the fifth year of ownership.

| Holding Period | Part I (Citizen/PR) | Part II (Malaysian Company) | Part III (Non-Citizen) |

| Within 3 years | 30% | 30% | 30% |

| In the 4th year | 20% | 20% | 30% |

| In the 5th year | 15% | 15% | 30% |

| 6th year and onwards | 0% | 10% | 10% |

Notes. : Rates apply to disposals from 1 January 2022 onwards.

Historical Rate Changes

RPGT rates have changed over time helps property owners identify which tax rules apply based on the year the property was acquired and sold. Over the past decade, Malaysia has implemented several revisions to improve market stability and adjust tax treatment for different categories of property disposers.

2014–2018

- Individuals paid 30% RPGT when disposing of property within the first three years.

- The rates gradually decreased depending on the holding period.

- Individuals received 0% tax from the sixth year onwards.

- Companies followed a similar decreasing structure but maintained a higher minimum rate.

2019–2021

- A 5% RPGT rate was introduced for individuals selling property in the sixth year and beyond.

- This change removed the previous 0% exemption available after long-term ownership.

- Foreign property disposers were subject to 10% RPGT.

- Companies also paid 10% for disposals during the same period.

From 1 January 2022 onwards (Current Structure)

- The 5% rate for individuals was removed.

- The 0% rate for individuals after the fifth year was reinstated.

- Companies and non-citizens continued to pay 10% for property disposals after the fifth year.

These historical changes show that RPGT policies have evolved over time to balance government revenue objectives with long-term property ownership incentives. Reviewing these changes helps sellers better understand how different periods can affect tax obligations and financial planning decisions.

How to Calculate Real Property Gains Tax (RPGT)?

Calculating RPGT involves more than subtracting your purchase price from your sale price. Several costs are deductible from the gain, and applying the right exemption can lower the final bill significantly.

RPGT Formula

RPGT calculation process generally follows three steps, starting from identifying the gain earned from the property disposal to the total tax amount payable.

- Chargeable Gain:

Disposal Price minus Acquisition Price minus Allowable ExpensesFormula:

Disposal Price − Acquisition Price − Allowable ExpensesExample:

RM600,000 − RM400,000 − RM20,000 = RM180,000 - Taxable Amount:

Chargeable Gain minus Exemption (RM10,000 or 10% of gain, whichever is higher, for Part I individuals)Formula:

Chargeable Gain − Exemption (RM10,000 or 10% of gain, whichever is higher)Example:

Exemption = 10% × RM180,000 = RM18,000Taxable Amount:

RM180,000 − RM18,000 = RM162,000 - RPGT Payable:

Taxable Amount multiplied by the applicable RPGT rateFormula:

Taxable Amount × Applicable RPGT RateExample:

RM162,000 × 15% = RM24,300

What Counts as Allowable Expenses?

The Act permits sellers to deduct specific costs incurred during ownership and property disposal. Each deduction must be backed by an official receipt, invoice, or signed agreement. Without supporting documents, LHDN can disallow the deduction during assessment. The recognized allowable expenses include the following items.

- Legal fees paid for the purchase and the disposal, including stamp duty incurred at acquisition

- Real estate agent commission paid to facilitate the sale

- Renovation and improvement costs that enhance the property capital value, such as structural extensions or major refurbishment (routine repairs are not deductible)

- Advertising and marketing costs related to selling the property

- Valuation fees charged by a registered valuer for the disposal

- Interest paid on loans taken to acquire the property, where the interest has not been claimed previously against rental income

Routine maintenance, utility bills, and quit rent are not deductible because they preserve rather than enhance the property value.

Calculation Example: Individual (Malaysian Citizen, Year 4)

Consider a Malaysian citizen who bought a condominium in Selangor for RM850,000 in 2021 and disposed of it in 2025 for RM1,150,000. The seller is now in the fourth year of ownership and incurred several allowable expenses during the sale process.

| Item | Amount (RM) |

| Disposal Price | 1,150,000 |

| Acquisition Price | 850,000 |

| Legal fees and stamp duty (purchase) | 12,000 |

| Renovation (with receipts) | 38,000 |

| Agent commission (3%) | 34,500 |

| Total Allowable Expenses | 84,500 |

| Chargeable Gain | 215,500 |

| Exemption (10% of gain or RM10,000, higher) | 21,550 |

| Taxable Amount | 193,950 |

| RPGT Rate (Year 4, Part I) | 20% |

| RPGT Payable | 38,790 |

The chargeable gain works out to RM215,500. Because the seller is a Part I disposer and the gain exceeds RM100,000, the 10% exemption of RM21,550 is more favourable than the flat RM10,000 option. The taxable amount of RM193,950 is then taxed at 20%, the year-four rate, producing an RPGT bill of RM38,790.

Calculation Example: Company (Sixth Year of Ownership)

Now consider a Sdn Bhd that purchased a commercial shoplot in Johor Bahru for RM1,400,000 in 2018 and disposed of it in 2025 for RM1,950,000. The company is now in the seventh year of ownership.

| Item | Amount (RM) |

| Disposal Price | 1,950,000 |

| Acquisition Price | 1,400,000 |

| Legal fees and stamp duty (purchase) | 22,000 |

| Improvement works | 75,000 |

| Agent commission | 58,500 |

| Total Allowable Expenses | 155,500 |

| Chargeable Gain | 394,500 |

| Exemption (companies not eligible) | 0 |

| Taxable Amount | 394,500 |

| RPGT Rate (Year 6+, Part II) | 10% |

| RPGT Payable | 39,450 |

Even though the company held the property beyond five years, the 10% floor rate still applies. Companies are not entitled to the RM10,000 or 10% personal exemption that Part I individuals enjoy. This is a common oversight in corporate property management planning, and it can shift expected net proceeds by tens of thousands of ringgit.

Real Property Gains Tax (RPGT) Exemptions in Malaysia

Several categories of disposers and transactions qualify for full or partial exemption. Each one comes with specific conditions, and missing the right form can mean losing the benefit entirely.

Individual Exemption (RM10,000 or 10%)

Every Malaysian citizen and permanent resident is entitled to a basic exemption on each disposal, equal to RM10,000 or 10% of the chargeable gain, whichever is higher.

This exemption applies per transaction rather than per year. A seller disposing of two properties in the same year receives the exemption on each disposal, and LHDN grants it automatically without a separate claim form.

Once-in-a-Lifetime Residence Exemption

Individuals who dispose of one private residence can claim a one-time exemption that waives RPGT on that single transaction. The claim is made by submitting Lampiran 3 attached to Form CKHT 1A within the 60-day filing window.

Conditions apply. The property must be a residential unit, the claimant must not have used this exemption before, and the election must be made in writing. Proper asset management and ownership records are also important, as the exemption can only be claimed once in the disposer lifetime.

Family Transfer Exemption

Transfers of property between certain family members are treated as no-gain-no-loss transactions, which means no RPGT applies at the time of transfer. Qualifying relationships include transfers between spouses, between parent and child, and between grandparent and grandchild.

This exemption is available only when the transferor is a Malaysian citizen. The recipient takes over the original acquisition date and price, which becomes relevant for any future disposal of the same property.

Other Exemptions

Additional categories outside the main individual exemptions include the following.

- Disposals of residential property valued at RM200,000 or below, where the property has been held for more than six years

- Compulsory acquisitions by government authorities or statutory bodies

- Disposals made pursuant to a court order

- Donations of property to the government, a state authority, or approved charitable bodies

- Property transferred as part of an approved corporate restructuring under Section 15 of the RPGTA

Each of these exemptions requires Form CKHT 3 to be submitted together with CKHT 1A, with the relevant supporting documentation attached.

RPGT Filing, Forms, Deadlines, and Payment

The administrative side of RPGT is where many sellers stumble. Two parties carry filing obligations, not just the seller, and the timeline is tight.

| Form | Filed By | Purpose |

| CKHT 1A | Seller (disposer) | Declares the disposal and computes the RPGT payable |

| CKHT 2A | Buyer (acquirer) | Confirms the acquisition and supports the seller filing |

| CKHT 3 | Disposer claiming exemption | Notifies LHDN of an exemption claim, attached to CKHT 1A |

Many sellers are surprised to learn that the buyer also has a filing obligation. Failure by the buyer to submit CKHT 2A within the deadline can lead to penalties on both parties. The forms must be signed and either submitted online through MyTax or delivered to the nearest LHDN branch office.

Submission Deadline

Both seller and buyer must submit their respective forms within 60 days from the date of disposal, defined as the date of the sale and purchase agreement (SPA). The deadline is not based on the date of payment or the date the documents are stamped.

Late submission carries a penalty of 10% on the RPGT payable, with additional charges if the actual tax payment is also delayed.

The buyer is also required to retain 3% of the purchase consideration, or 7% if the seller is a non-citizen or foreign company, and remit it directly to LHDN as an advance payment against the seller RPGT. This retention rule is usually handled by the buyer solicitor, and it is one of the most overlooked obligations in Malaysian conveyancing.

Payment Methods

LHDN accepts payment of RPGT through several channels.

- The MyTax portal at mytax.hasil.gov.my, which is the primary online channel

- e-PCB and electronic banking services connected to LHDN

- Over-the-counter payment at appointed banks, including Maybank, CIMB Bank, Public Bank, and others designated by LHDN

- Pos Malaysia counters, for sellers who prefer a manual transaction

Receipts from any of these channels should be retained for at least seven years in case of audit or any future query from LHDN. Using accounting software can also help businesses organize RPGT payment records, supporting documents, and financial reports more efficiently.

How Proper Accounting Records Help Reduce Your RPGT Liability?

Many property owners pay higher RPGT because they cannot provide complete records for allowable expenses during assessment. Keeping organized documents such as acquisition costs, renovation receipts, and disposal invoices helps support deductions and reduce the final RPGT payable amount.

Using accounting software also makes RPGT filing easier by keeping property transactions, supporting documents, and expense records in one place. Solutions combine financial reporting and asset management features to help businesses track property-related costs, manage fixed assets, and prepare records required for CKHT filings more efficiently.

Conclusion

understanding Real Property Gains Tax (RPGT) is important for anyone planning to sell property in Malaysia, whether as an individual or a company. The final tax payable depends on several factors, including the holding period, disposer category, allowable expenses, and available exemptions under the RPGTA. Missing important filing deadlines or failing to keep proper supporting documents can also lead to unnecessary penalties and higher tax exposure.

By maintaining organized financial records and using accounting software with financial reporting and asset management features, property owners can prepare CKHT filings more accurately and maximize allowable deductions. With proper planning and documentation, Malaysian property sellers can manage RPGT obligations more efficiently while reducing the overall tax burden.

Discover how accounting software with financial reporting and asset management features can help your business manage property-related taxes and records more efficiently with free demo for today.

FAQ about Real Property Gains Tax (RPGT)

FAQ

Yes. The seller must still file Form CKHT 1A within 60 days, even when the disposal results in a loss with no chargeable gain. The submission documents the no-gain position, prevents LHDN from issuing an estimated assessment, and allows the loss to be carried forward against future RPGT gains.

A Malaysian company that disposes of property after the fifth year still pays 10% under Part II. The zero-rate relief available to Part I individuals does not extend to corporate disposers, which should be built into the financial model whenever a corporate disposal is being considered.

A direct inheritance from a deceased person to a beneficiary is not treated as a disposal under the RPGTA, so no RPGT applies at that moment. The beneficiary inherits the deceased original acquisition date and price, which then becomes the holding-period start when the property is eventually sold.

Stamp duty is paid by the buyer at acquisition, calculated on the purchase price, and tiered between 1% and 4%. RPGT is paid by the seller at disposal, calculated on the chargeable gain after allowable expenses and exemptions. Both must be settled for a property transfer to be legally complete.

{kind=link}