ESG reporting is the process of measuring, documenting, and disclosing a company’s environmental, social, and governance performance. It helps businesses communicate sustainability risks, ethical practices, climate impact, and governance standards through structured and measurable non-financial data used by investors, regulators, and stakeholders.

ESG reporting in Australia is the process of disclosing environmental, social, and governance performance data to the public. It covers emissions, workforce practices, board oversight, and climate risk in one report.

Australian businesses prepare ESG reports by collecting data across operations, applying standards such as AASB S1, AASB S2, and GRI, and publishing results alongside financial statements.

From FY2025, mandatory climate disclosures apply to the largest Australian companies. Therefore, this blog will cover all ESG reporting obligations, frameworks, and data requirements that are vital to understand.

Key Takeaways

ESG reporting discloses environmental, social, and governance performance using measurable and audit-ready data.

What Is ESG Reporting?

ESG reporting is the disclosure of a company’s environmental, social, and governance performance. It translates sustainability activities into measurable data that stakeholders can use for decisions.

As the name suggests, ESG stands for Environmental, Social, and Governance. The environmental pillar covers GHG emissions (Scope 1, 2, and 3), energy use, water consumption, waste management, and climate change risks. The social pillar covers workforce diversity, human rights, labour practices, workplace health and safety, and data security. The governance pillar covers board composition and diversity, executive compensation, shareholder rights, anti-corruption policies, and risk management accountability.

In Australia, ESG reporting has shifted from voluntary communication to regulated disclosures, often supported by ERP for sustainability to centralise and manage data. Australia’s sustainability disclosure regime is being introduced in phases from FY2025, making climate-related reporting increasingly important for larger organisations.

"ESG reporting is, at its core, the translation of non-financial performance into auditable data. Every figure, every target, and every forward-looking statement must withstand the same scrutiny as a line item in the financial statements."

Is ESG Reporting Mandatory in Australia?

Reporting group |

Starts |

Threshold |

What businesses should prepare |

| Group 1 | FY2025 | 2 of: 500+ employees, $1B revenue, $1B assets | Climate governance, Scope 1 & 2 emissions, risk assessment, scenario analysis |

| Group 2 | FY2026 | 2 of: 250+ employees, $200M revenue, $500M assets | ESG data collection processes and climate disclosure preparation |

| Group 3 | FY2027 | 2 of: 100+ employees, $50M revenue, $25M assets | Governance oversight and material climate reporting processes |

Yes. The Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 introduces mandatory climate-related financial disclosures for eligible Australian entities, phased in between FY2025 and FY2027.

The regime applies in three phased groups based on size and listing status.

1. Group 1 (FY2025): large listed and large unlisted companies

Group 1 includes entities meeting two of the following thresholds: 500+ employees, $1 billion in revenue, or $1 billion in gross assets. Reporting applies to financial years starting from 1 January 2025.

These businesses must prepare climate-related disclosures covering governance, climate risks, emissions, and scenario analysis, with Scope 3 reporting phased in later.

2. Group 2 (FY2026): medium listed and unlisted companies

Group 2 applies to entities meeting two of: 250+ employees, $200 million in revenue, or $500 million in gross assets. Reporting begins from 1 July 2026.

Businesses should begin building data collection and reporting processes well before commencement to support climate-related disclosures and future assurance requirements.

3. Group 3 (FY2027): smaller listed and financial institutions

Group 3 covers entities meeting two of: 100+ employees, $50 million in revenue, or $25 million in gross assets, as well as certain asset owners. Reporting starts from 1 July 2027.

Although reporting obligations are more proportionate, businesses still need documented governance, risk management, and climate-related disclosures.

4. Voluntary ESG reporting: who should start now even if not yet required

Businesses outside mandatory thresholds may still receive ESG information requests from lenders, investors, customers, and supply-chain partners.

Starting voluntary reporting early helps improve data quality, prepare for future requirements, and support contract and financing opportunities.

Need a starting point? Download the free ESG report template pack below, then use the guide later in this article to align it with Australian reporting requirements.

Free ESG Report Templates

The following eight templates cover the most common ESG reporting formats used by Australian businesses. Each is structured to align with AASB S1, AASB S2, GRI Standards, and Safe Work Australia data requirements.

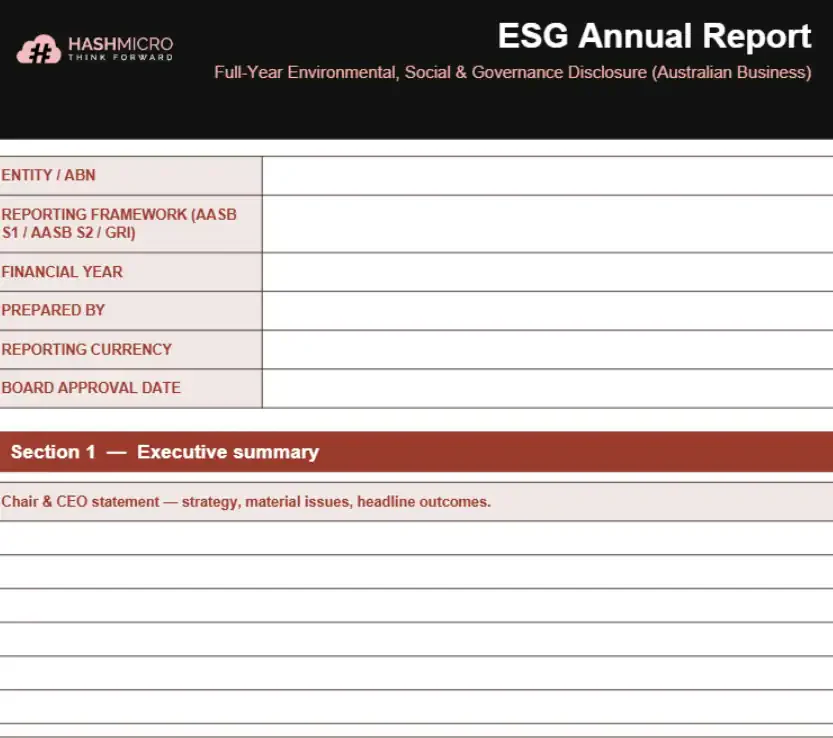

1. ESG annual report template (GRI-aligned)

This template provides the full narrative structure: CEO statement, company profile, materiality outcomes, stakeholder summary, environmental section, social section, governance section, and forward targets.

GRI Universal, Sector, and Topic Standards mapping is embedded, so each section references the disclosure code. It suits ASX-listed entities and mid-market businesses publishing a first sustainability report.

ESG annual report template

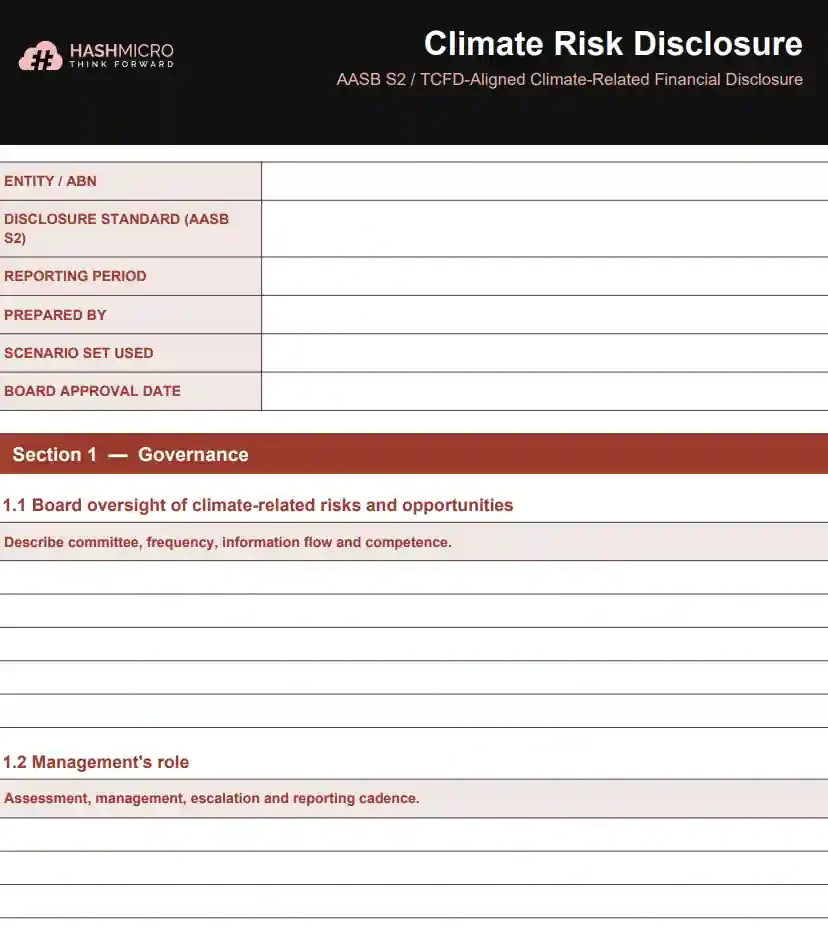

2. Climate risk disclosure template (AASB S2 / TCFD-aligned)

Structured around the four AASB S2 pillars: governance, strategy, risk management, and metrics. It includes pre-formatted sections for scenario analysis, risk registers, and climate-related financial impact.

Director sign-off blocks, assurance provider fields, and restatement tables are included. Mandatory reporters in Groups 1, 2, and 3 can use it as the primary climate statement in the annual financial report.

Climate risk disclosure template

3. GHG emissions report template

Covers Scope 1, 2, and 3 calculations using the GHG Protocol Corporate Standard. Activity data fields include fuel type, electricity source, refrigerants, business travel, freight, and purchased goods.

Built-in NGER emission factors support Australian reporters, with a section for market-based Scope 2 where renewable energy certificates apply. A dashboard aggregates totals in tonnes CO2-equivalent.

GHG emissions report template

4. Environmental KPI report template

Covers non-emissions environmental metrics: water withdrawal, discharge, recycled water, waste generated, waste diverted, land disturbed, biodiversity plans, and air emissions like NOx, SOx, and particulates.

Quarterly tracking tabs allow operations teams to monitor trends and flag variances. Suits resources, manufacturing, and utilities sectors where state licence conditions require regular environmental disclosure.

Environmental KPI report template

5. Social and workforce report template

Contains sections for headcount demographics, WGEA gender pay gap data, Safe Work Australia injury metrics, training statistics, community investment, and Modern Slavery Act due diligence.

Built-in fields calculate lost-time injury frequency rate, total recordable injury rate, turnover, and training hours per FTE. Aligns with GRI 400-series standards and AASB S1 workforce disclosures.

Social and workforce report template

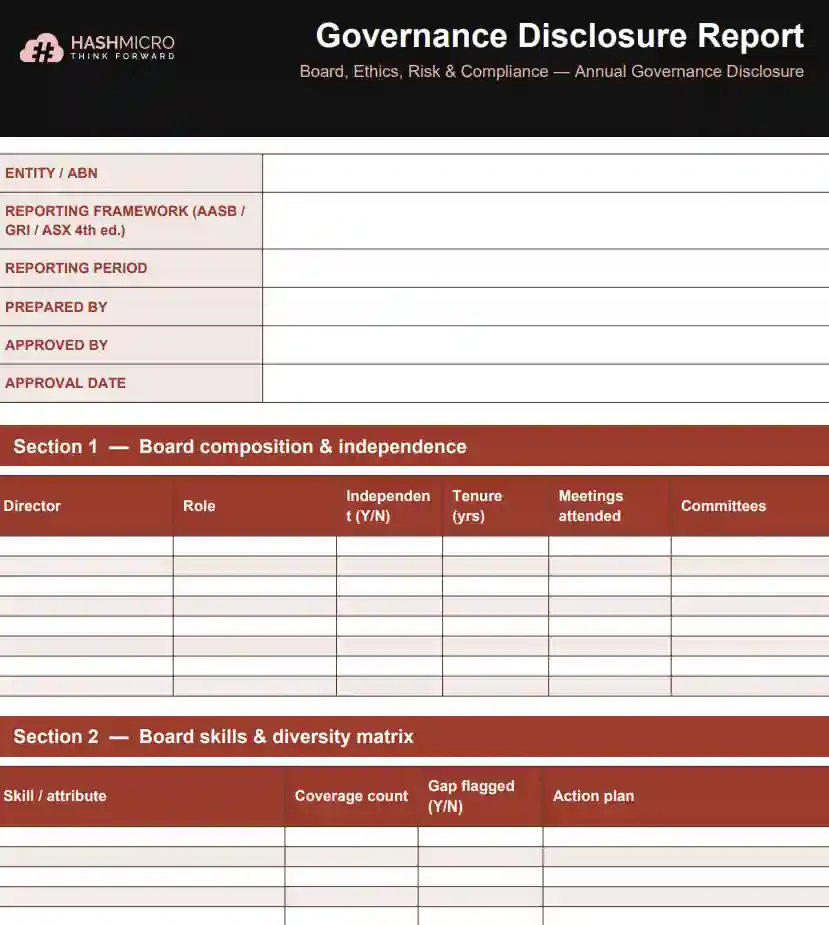

6. Governance disclosure report template

Covers board composition, independence ratios, diversity, tenure, committee structures, executive remuneration, ethics and whistleblower policies, and material compliance breach registers.

Aligned with AASB S1 governance requirements and ASX Corporate Governance Principles. Private companies, not-for-profits, and mid-market businesses can adopt the same structure for lender readiness.

EOFY Financial Analysis Report Template

7. ESG KPI dashboard template (quarterly tracking)

A single-page dashboard tracking up to 20 ESG KPIs across environmental, social, and governance pillars. Each KPI has a target, current value, variance, owner, and RAG status for board reporting.

Designed for quarterly use, with trend sparklines and rolling 12-month views. Teams with sustainability-linked loans or bonds can configure covenant thresholds to trigger alerts when KPIs near breach.

ESG KPI dashboard template

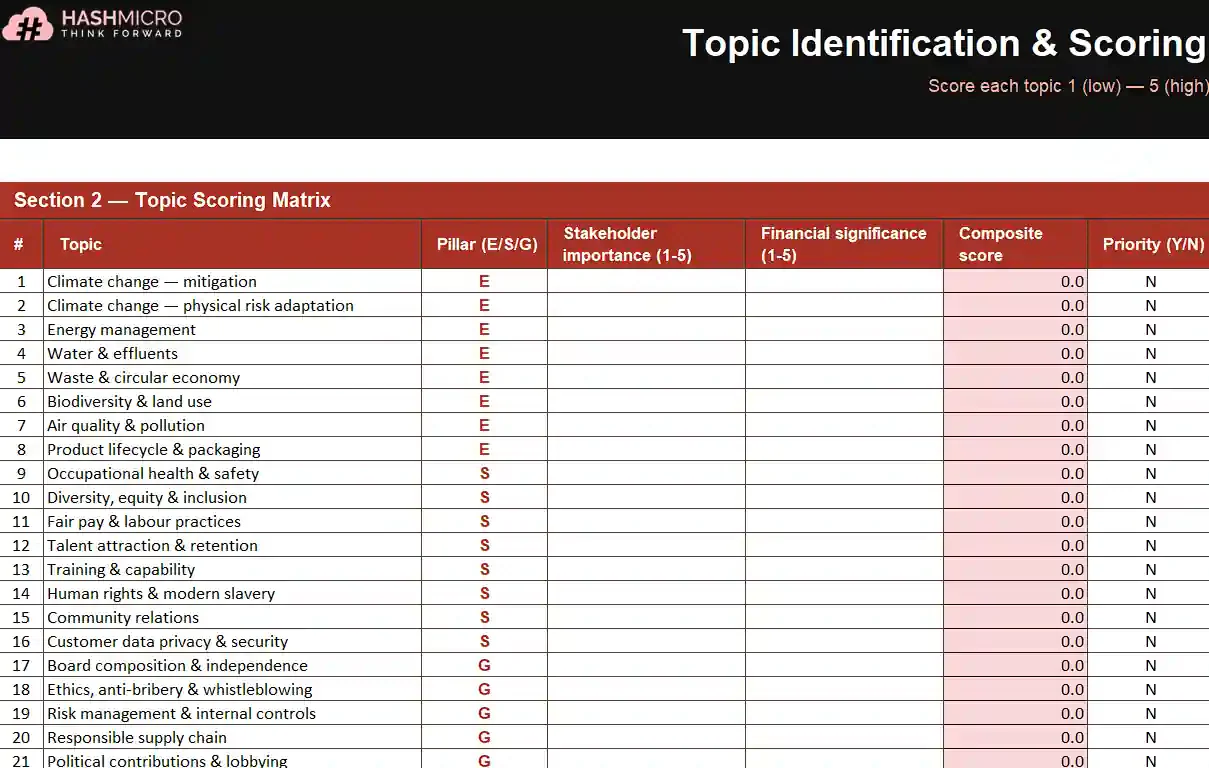

8. Materiality assessment matrix template

Guides the materiality process from stakeholder identification to final priority shortlist. Includes survey templates, scoring rubrics, and a visual matrix plotting financial impact against stakeholder concern.

Outputs feed directly into AASB S2 climate risk analysis and GRI-aligned reporting. Refresh every two years to capture regulatory changes, new business activities, or emerging stakeholder expectations.

Materiality assessment matrix template

While templates provide a reporting structure, ongoing ESG compliance depends on accurate data collection, audit trails, and cross-department visibility. If you’re considering a more scalable approach, the pricing guide below outlines the costs and capabilities of ESG reporting software.

Why ESG Reporting Matters for Australian Businesses

ESG reporting is no longer a marketing exercise. It now carries legal, commercial, and reputational consequences that affect access to capital, contracts, and insurance. Three drivers explain the shift.

1. Meeting ASIC obligations and avoiding greenwashing risk

ASIC holds active enforcement powers against misleading sustainability claims. Since 2023, it has issued infringement notices and commenced Federal Court actions against superannuation funds and listed companies.

Accurate ESG reporting, backed by documented sources and methods, is therefore the primary defence. Vague net-zero pledges, statements without evidence, or selective disclosure all attract regulator scrutiny.

2. Responding to investor, lender, and supply chain demands

The Big Four Australian banks now embed ESG data into credit assessments and sustainability-linked loans. Large investors like AustralianSuper and Aware Super also require AASB S2-aligned disclosures.

Large buyers such as Woolworths, BHP, and Telstra also cascade ESG questionnaires down supply chains. Consequently, suppliers without structured data risk losing tenders, pricing, or preferred-vendor status.

3. Building long-term business resilience and reputation

Climate risk, workforce turnover, and governance failures erode enterprise value over time. ESG reporting forces structured measurement, giving boards early warning of issues financial statements cannot surface.

Transparent reporting strengthens trust and supports an eco-friendly business platform that aligns operations with sustainability goals. For example, Australian companies publishing audited emissions data often outperform peers on retention and loyalty metrics.

4. Operational efficiency

ESG reporting helps businesses identify waste, energy inefficiencies, supplier risks, and process gaps that often increase operating costs. As a result, finance and operations teams can use ESG data to improve resource planning, reduce unnecessary spending, and support more sustainable business performance.

ESG Reporting Frameworks Used in Australia

Australian businesses typically combine a mandatory standard with voluntary frameworks.

The mandatory layer covers compliance, while voluntary frameworks address investor expectations and global comparability.

1. Australia’s mandatory sustainability reporting standards

AASB S1 sets general sustainability disclosure requirements across governance, strategy, risk, and metrics. AASB S2 focuses on climate disclosures, including physical risk, transition risk, and scenario analysis.

Both standards align with the ISSB baseline. Australian entities in Groups 1, 2, and 3 apply AASB S2 from their commencement dates, with AASB S1 following as the framework matures.

2. GRI (Global Reporting Initiative): the most widely used voluntary framework

The GRI Standards remain the dominant voluntary framework for full ESG reporting in Australia. They cover universal, sector, and topic-specific disclosures across environmental, social, and governance pillars.

GRI suits companies wanting stakeholder reporting beyond climate. For example, ASX-listed miners pair AASB S2 climate statements with a GRI-aligned report covering tailings, community, and workforce topics.

3. TCFD: the climate framework now incorporated into AASB S2

The Task Force on Climate-related Financial Disclosures (TCFD) framework introduced the four-pillar structure now embedded in AASB S2: governance, strategy, risk management, and metrics and targets.

Australian entities reporting under TCFD, such as APRA-regulated banks under CPG 229, can transition to AASB S2 with limited rework. The disclosure logic stays the same, though required metrics become more specific.

4. ISSB / IFRS S1 and S2: the global standards behind Australia’s AASB S1/S2

The International Sustainability Standards Board issued IFRS S1 and IFRS S2 in June 2023. The AASB then adopted these with minor Australian modifications, producing AASB S1 and AASB S2 for local use.

For multinationals, this alignment means one global ESG data set can satisfy Australian, UK, Japanese, and Singaporean regimes, subject to differences in scope, timing, and assurance.

5. CDP and UN SDGs: supplementary voluntary disclosure channels

CDP runs an annual questionnaire covering climate, water, and forests. Many Australian listed companies respond because institutional investors use the scores in engagement and voting decisions.

The UN Sustainable Development Goals provide a high-level outcome framework. Businesses typically map ESG initiatives to relevant SDGs inside a GRI report, rather than producing a standalone SDG disclosure.

Types of ESG Reports

Australian businesses rarely produce a single all-encompassing document. Instead, ESG reporting has split into distinct report types, each serving specific stakeholders, frameworks, and assurance needs.

1. ESG annual / sustainability report (GRI-aligned)

This is the flagship narrative report, published alongside the annual financial report. It covers all three ESG pillars, materiality outcomes, stakeholder engagement, and progress against prior commitments.

Length ranges from 40 to 120 pages for ASX 200 companies. Investor relations, sustainability, and communications teams jointly own the content, with external assurance often applied to Scope 1 and 2 emissions.

2. Climate risk disclosure report (AASB S2 / TCFD)

This report satisfies mandatory AASB S2 and focuses exclusively on climate-related financial risks and opportunities. It covers governance, strategy, scenario analysis, risk processes, and quantified metrics.

Unlike a GRI sustainability report, the climate disclosure sits inside or alongside financial statements. Therefore, it falls under director sign-off and auditor assurance, with legal weight equal to financial data.

3. GHG emissions report (Scope 1, 2, and 3)

A greenhouse gas inventory report quantifies emissions across operational boundaries. Scope 1 covers direct emissions, Scope 2 covers purchased energy, and Scope 3 spans value chain emissions in 15 categories.

Australian entities generally follow the GHG Protocol Corporate Standard, supplemented by NGER Act methods for regulated facilities. It often feeds AASB S2 climate statements and GRI-aligned disclosures.

4. Environmental performance report

This report extends beyond emissions to cover water, effluent, waste, recycling rates, land use, biodiversity, and air pollutants. It is common in resources, utilities, manufacturing, and agriculture.

Australian mining and energy firms typically publish an environmental performance report to meet state licence conditions, NGER reporting, and community expectations. It also feeds GRI and AASB S2 disclosures.

5. Social and workforce report

The social report covers demographics, gender pay gap, injury rates, training hours, turnover, community investment, and modern slavery due diligence. It targets regulators, unions, investors, and communities.

Data sources include HR systems, Safe Work Australia incident logs, WGEA submissions, and Modern Slavery Act statements. A social report often consolidates information already produced for regulatory lodgements.

6. Governance disclosure report (AASB S1)

The governance report covers board composition, independence, diversity, committee structures, executive pay, ethics policies, and cyber-risk oversight. AASB S1 formalises sustainability-related governance disclosure.

ASX-listed companies usually integrate governance disclosures into the corporate governance statement. However, private companies preparing voluntary ESG reports can adopt the same structure for lender readiness.

7. ESG KPI progress report (quarterly / annual)

This is an internal or investor-facing update tracking ESG KPIs against targets. Common metrics include emissions intensity, renewable energy share, lost-time injury frequency rate, and board diversity.

Quarterly cadence suits companies with sustainability-linked loans or bonds where covenants reference KPI thresholds. Annual cadence is standard for most Australian businesses outside regulated finance.

8. Materiality assessment report

A materiality report documents which ESG topics are financially significant and most important to stakeholders. It sets the scope and priorities for all subsequent ESG reporting and target-setting activity.

The process combines stakeholder surveys, peer benchmarking, regulatory review, and risk data. Outputs typically include a materiality matrix, a priority topic shortlist, and linkages to GRI, AASB S2, and ISSB.

What to Include in an ESG Report

A robust ESG report combines quantitative metrics, qualitative narrative, and forward-looking targets. The following five components form the minimum content set expected by regulators, investors, and auditors in Australia.

1. Environmental metrics: GHG emissions (Scope 1, 2, 3), energy, water, waste

Report Scope 1 and 2 emissions in tonnes of CO2-equivalent using NGER or GHG Protocol methods. Scope 3 should cover material categories such as purchased goods, business travel, and downstream product use.

Include energy consumption split by renewable and non-renewable sources, water withdrawal and discharge, and total waste with diversion-from-landfill rates. Use the prior reporting year as a baseline.

2. Social metrics: workforce, health & safety (Safe Work AU), community, modern slavery

Disclose headcount by gender, employment type, and location, alongside voluntary turnover rates and the WGEA-reported gender pay gap. Include training hours per employee and apprenticeship intake numbers.

Report lost-time injury frequency rate, total recordable injury rate, and fatalities under Safe Work Australia methodology. A modern slavery statement is required for entities with revenue above $100 million annually.

3. Governance metrics: board composition, executive pay, risk management, ethics

Disclose board size, independent director ratio, gender split, average tenure, and attendance rates. Provide the charter and membership of audit, risk, remuneration, and sustainability committees.

Summarise the executive remuneration framework, including the share linked to ESG KPIs. List ethics, whistleblower, anti-bribery, and conflict-of-interest policies, plus any material breaches in the year.

4. Materiality assessment and stakeholder engagement process

Document how you identified material ESG topics. Describe the stakeholder groups consulted, engagement methods used, and the scoring system applied to rank financial significance against stakeholder importance.

Present the outcome as a materiality matrix, then cross-reference each priority topic to the relevant AASB, GRI, or ISSB disclosures. Refresh the assessment at least every two years.

5. Climate scenario analysis and forward-looking targets (AASB S2)

AASB S2 requires scenario analysis under at least two pathways, including one consistent with the Paris 1.5°C goal. Describe time horizons, physical risks, transition risks, and quantified impacts.

Forward-looking targets should include absolute or intensity emissions reductions, interim milestones, and the base year. Explain assumptions and dependencies, especially where Scope 3 reductions rely on suppliers.

Real ESG Report Examples from Australian Businesses

Many Australian companies already publish detailed ESG and climate disclosures aligned with AASB S2, GRI, TCFD, and ISSB frameworks. Reviewing real reports helps businesses understand reporting structure, KPI presentation, materiality disclosures, and assurance expectations.

1. BHP

BHP publishes detailed climate risk, emissions, water management, biodiversity, and workforce disclosures aligned with TCFD and ISSB principles. Its reports also include operational decarbonisation targets and scenario analysis.

2. Rio Tinto

Rio Tinto combines ESG reporting with environmental performance, community engagement, modern slavery disclosures, and governance oversight across global mining operations.

3. Telstra

Telstra’s ESG reports focus heavily on emissions reduction, renewable energy transition, cybersecurity governance, employee wellbeing, and digital inclusion initiatives.

4. Commonwealth Bank

Commonwealth Bank publishes climate-related financial disclosures covering financed emissions, sustainable lending exposure, governance frameworks, and transition risk management.

5. Wesfarmers

Wesfarmers integrates ESG reporting across retail, industrial, and chemicals divisions, including workplace safety, waste reduction, emissions intensity, and supply chain governance.

6. Woolworths Group

Woolworths reports on food waste reduction, renewable electricity usage, sustainable sourcing, packaging targets, and supplier ESG engagement across retail operations.

7. ANZ

ANZ focuses on climate governance, sustainable finance commitments, financed emissions, and ESG risk integration within lending and investment decisions.

How to Start ESG Reporting

Starting ESG reporting follows a repeatable six-stage process. Treating it as a structured project, with defined owners and deliverables, prevents late-cycle rework and reduces the assurance burden in year one.

1. Determine your reporting obligations (mandatory group or voluntary)

Check whether your entity meets Group 1, 2, or 3 thresholds under AASB S2. Confirm your commencement date, first reporting period, and Scope 3 relief window, then document the conclusion in a board paper.

If you fall outside mandatory groups, review lender, investor, and customer data requests from the past 12 months. Where requests are frequent, voluntary AASB S2-aligned reporting is the practical start point.

2. Conduct a materiality assessment

Identify ESG topics that are financially significant and important to key stakeholders. Combine internal risk data, peer disclosures, regulatory scans, and stakeholder surveys to build a balanced topic list.

Plot topics on a two-axis matrix, then shortlist 8 to 12 priorities. This shortlist defines the scope of your first report, the KPIs you collect, and the narrative sections the final document requires.

3. Choose your ESG framework(s)

Select a mandatory framework where applicable (AASB S1 / S2) and one voluntary framework, typically GRI. Add sector frameworks where relevant, such as SASB for financial services or ICMM for mining.

Map the chosen frameworks to your material topics. Each disclosure should appear once, in the report section where it fits most naturally. This prevents duplication and reduces data collection workload.

4. Collect, verify, and organise ESG data

ESG data comes from HR, finance, operations, procurement, and facilities systems, making an ERP for ESG reporting essential to centralise and manage data accurately. Build a central repository with owners, source documents, calculation methods, and version control for every metric.

Internal verification should happen before external assurance. Reconcile totals to underlying systems, check unit conversions, document estimates, and retain supporting evidence for at least seven years.

When source records sit across different teams, even a complete ESG metric can be difficult to verify and defend during assurance.

Hashy AI helps connect those records, surface missing evidence, and prepare a structured summary for review, as mapped in the banner below.

5. Write, structure, and design your ESG report

Draft in plain English, lead with material topics, and include both narrative and data tables. Aligning section order with the framework index helps assurance providers locate evidence efficiently.

Design should reinforce readability, not decoration. Use consistent charts for trend data, include year-on-year comparisons, footnote methods, and publish a data appendix for machine-readable tables.

6. Get assurance and publish

Mandatory AASB S2 reporters must obtain reasonable assurance on the climate statement by the phase-in date. Voluntary reporters typically seek limited assurance on selected metrics such as Scope 1 and 2.

Publish on the corporate website, lodge with ASIC where required, and file with ASX for listed entities. A press release summarising key metrics supports investor relations, media, and internal communications.

How Much Does ESG Reporting Cost in Australia?

ESG reporting costs in Australia vary based on business size, reporting scope, data maturity, and assurance requirements. Mandatory AASB S2 reporters generally face higher implementation and audit costs during the first reporting cycle.

| Business type | Estimated ESG reporting cost | Main cost drivers |

| Small voluntary reporters | AUD $30,000–$80,000 | Basic consulting, emissions calculations, report preparation |

| Mid-sized mandatory reporters | AUD $150,000–$600,000 | Data systems, assurance, advisory, framework implementation |

| Large listed enterprises | AUD $1M+ | Complex Scope 3 modelling, assurance, scenario analysis, software integration |

Major ESG reporting costs include data collection, assurance, consulting, and software implementation. Integrated ERP systems help reduce reporting effort and compliance costs.

Australian ESG Reporting Requirements in 2025–2027

Australian ESG reporting obligations are shaped by disclosure standards, regulatory oversight, and supporting legislation. Businesses should understand how these requirements interact when preparing for compliance between FY2025 and FY2027.

1. AASB S1 and AASB S2

Australia’s mandatory sustainability disclosure regime is built around AASB S1 and AASB S2. Businesses should focus on understanding commencement dates, reporting obligations, and assurance requirements relevant to their reporting group.

2. ASIC enforcement and the real risk of greenwashing claims

ASIC continues to treat greenwashing as an enforcement priority and has taken action against organisations for misleading sustainability claims.

Any ESG statement, target, or marketing claim should be supported by documented evidence and consistent reporting practices.

3. NGER Act, APRA CPG 229, and the Modern Slavery Act

The NGER Act supports emissions reporting, APRA CPG 229 guides climate risk management, and the Modern Slavery Act requires annual disclosures from eligible entities.

ESG Reporting Best Practices for Australian Businesses

Australian businesses that treat ESG reporting as an operational discipline achieve better data quality, lower assurance costs, and stronger stakeholder outcomes. Four practices separate leaders from laggards.

1. Start with Scope 1 and 2 emissions before tackling Scope 3

Scope 1 and 2 rely on data you already control: fuel records, fleet logs, and electricity invoices. Mature these calculations, reconcile to financial systems, and obtain assurance before tackling Scope 3.

Scope 3 requires supplier engagement, activity factors, and often estimation. Tackling it in year two lets you build supplier data portals, define boundaries, and avoid the risk of material restatements.

2. Align with AASB S2 even if not yet in a mandatory group

Entities outside current thresholds will face obligations as customer and lender pressure rises. Voluntary adoption of AASB S2 structure prevents costly rework when thresholds shift or buyer demands accelerate.

The AASB S2 four-pillar structure also forces board-level engagement with climate risk. Therefore, even businesses reporting only a few metrics in year one benefit from the governance discipline it enforces.

3. Build external assurance readiness into year-one processes

Assurance providers assess documentation quality, not just the numbers. Therefore, maintain source evidence, calculation memos, and version-controlled approvals for every disclosure.

Early engagement with assurance firms during the data collection phase surfaces gaps before they become findings. This lowers second-year fees and reduces the risk of qualified opinions on sustainability statements.

How ERP Software Simplifies ESG Reporting for Australian Businesses

ESG reporting requires data from finance, HR, procurement, operations, facilities, and supply chain systems. A centralised ESG platform helps businesses consolidate this information and reduce manual reporting processes.

- Automatically consolidates ESG data across finance, HR, procurement, and operations.

- Applies standardised emission factors and calculation methods across reporting periods.

- Creates audit-ready trails for AASB S2 assurance and compliance reviews.

- Tracks ESG KPIs, targets, variances, and reporting deadlines in real time.

- Improves Scope 1, Scope 2, and Scope 3 emissions visibility across business units.

- Reduces spreadsheet dependency and manual reconciliation work.

- Supports board reporting through automated dashboards and sustainability analytics.

Integrated ERP and ESG systems help businesses improve reporting accuracy, shorten reporting cycles, and reduce assurance preparation effort across annual disclosures.

Conclusion

ESG reporting has moved from voluntary communications to a core compliance, finance, and risk function for Australian businesses. AASB S1 and AASB S2 set the baseline, phased from FY2025 through FY2027.

Matching framework choice to obligations and investing in centralised data systems reduces assurance risk. Businesses treating ESG reporting as a discipline, backed by the right software and internal ownership, achieve compliance with ease.

If you want to implement ESG compliance effectively, you can schedule a consultation with our experts to get the right guidance.

Frequently Asked Question

ESG reporting focuses on financially material environmental, social, and governance disclosures relevant to investors and regulators. Sustainability reporting is broader and may also include operational, community, and brand-related initiatives beyond financial materiality.

First-year mandatory AASB S2 reporting typically costs between AUD $150,000 and $600,000 for mid-sized entities, covering consulting, software, assurance, and data preparation. Smaller voluntary reporters may spend between AUD $30,000 and $80,000.

Under AASB S2, directors are legally responsible for approving climate-related disclosures. In practice, sustainability, finance, risk, and audit teams prepare the report before final board sign-off.

Small businesses are not currently included in mandatory reporting groups, however, many still face ESG data requests from customers, lenders, insurers, and procurement partners.

Most Australian businesses publish ESG reports annually alongside financial reporting cycles. Larger organisations may also release quarterly ESG KPI updates or climate-related progress disclosures.

Scope 1 emissions are direct emissions from owned operations, Scope 2 covers purchased electricity or energy, and Scope 3 includes indirect value chain emissions such as suppliers, freight, travel, and product use.

A materiality assessment identifies which ESG topics are most financially significant to the business and most important to stakeholders. The process helps define reporting priorities, KPIs, and disclosure scope.

Failure to meet AASB S2 obligations may expose businesses to regulatory action, assurance findings, investor scrutiny, reputational damage, and potential greenwashing claims if disclosures are inaccurate or misleading.