A payment gateway is the hidden system that is everywhere. To the average shopper, the process of buying goods online is as easy as clicking “Pay now”. But that simplicity is backed by a high-speed digital relay race involving multiple banks, security checks, and data verification. All that important process to maintain a merchant’s cash flow and protection from business fraud took at most three seconds.

This article will further explore payment gateways and showcase how a business can implement them to protect its customers and business.

Table of Contents

Key Takeaways

|

Payment Gateway Definition

A payment gateway is an online service that processes payment transactions between a customer and a business. Functioning like a point-of-sale terminal, it encrypts sensitive data, authorises transactions, and ultimately decides whether revenue enters your account or is rejected at the door.

It ensures that every transaction can be completed globally, securely, and quickly. With this security system, customers can feel safe and trust your business.

What’s Actually Happening Between “Pay Now” and “Payment Confirmed”

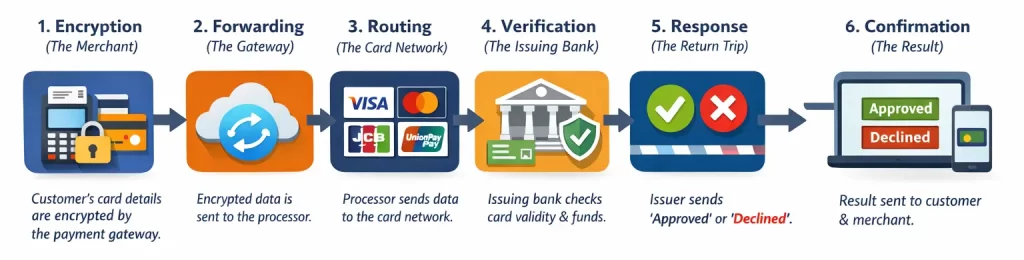

Understanding the journey a transaction takes is vital to improving your checkout experience. On the surface, it seems that money instantly moves from the customer’s bank to yours, but in reality, there are multiple steps in the process.

The process has two distinct phases: Authorization and settlement. The gateway is primarily responsible for authorization, making sure that the customer is legitimate and has funds available for the purchase in real-time. Settlement usually happens at the end of the business day; it is the actual transfer of funds, and it takes place in batches.

The chain of handshakes you never see

In the few seconds the loading spinner is active on your customer’s screen, a sophisticated chain of “digital handshakes” occurs. Whether it is due to technical downtime, security flags, or insufficient funds, if one of the chains fails, then the sale is lost. Here is the breakdown of the invisible relay:

This entire loop covers thousands of miles of digital infrastructure in milliseconds. The efficiency of your gateway determines how fast this loop closes, directly impacting the user experience.

Why a gateway and a processor aren’t the same thing

Gateway is often seen as the processor when it actually has distinct functions. The payment gateway is the interface that accepts the card, reads the chip, and asks for a PIN. In other words, it is a data-gathering tool.

Meanwhile, the payment processor works behind the scenes, taking data from the terminal and running it over the banking network to get the money. It does the heavy lifting of moving financial data between the merchant’s bank (Acquiring Bank) and the customer’s bank (Issuing Bank).

You cannot have one without the other. However, you can sometimes mix and match them. For example, a high-volume enterprise might use a specific gateway for its robust fraud tools but connect it to a different back-end processor that offers lower transaction fees. Understanding this distinction gives you leverage when negotiating contracts.

Types of Payment Gateway

The architecture of a gateway determines the user experience (UX) on your site. A clumsy integration can increase cart abandonment, while a seamless one can boost conversion rates. Generally, gateways fall into three architectural categories, with each serving different business maturities.

- Hosted Gateways (Redirects)

In this setup, when a customer clicks “Buy,” they are redirected away from your website to the payment provider’s secure page to enter their details. Once paid, they are redirected back to your site.

- Pros: The easiest to set up. Security compliance (PCI DSS) is largely handled by the provider because you never touch the data.

- Cons: It adds friction; customers may trust your brand but feel uneasy being sent to a third-party URL they don’t recognize. It breaks the branding experience.

- Self-Hosted Gateways (On-Site Checkouts)

Here, the customer stays on your website. They enter payment details into a form that looks like part of your store. However, the data is usually posted directly to the gateway’s URL in the background, or collected via a secure widget (iFrame).

- Pros: Better user experience. The customer never leaves your ecosystem.

- Cons: You bear more responsibility for security. If your website is hacked, there is a theoretical risk (though iFrames mitigate this significantly).

- API-Based Gateways (Server-to-Server)

This is for merchants who want total control. You build the entire checkout UI from scratch and use the gateway’s API to process payments behind the scenes.

- Pros: Limitless customization. You can design unique checkout flows, one-click upsells, and highly branded experiences.

- Cons: Requires significant development resources and places the highest burden of security compliance on your business.

Set up fits for a one-person store vs a growing brand.

For a solopreneur or a brand-new drop shipping business, a hosted gateway is often the smartest choice. The primary goal in the early stages is validation, not optimization. However, as a brand grows, the redirect method becomes a liability. Data shows that every additional step or URL change in the checkout process drops conversion rates. A growing brand generating consistent revenue should transition to a self-hosted or API-based solution. Customer experience becomes paramount at this stage.

The trade-Off between control and convenience

The central tension in choosing a gateway is control versus convenience. “All-in-one” payment service providers (PSPs) are convenient as you get a gateway, processor, and merchant account in a single signup. The trade-off is control; accounts often freeze because of aggressive fraud algorithm. Unexpected sales spike can cause the automated systems to flag your account and freeze your funds for weeks. Dedicated merchant accounts are harder to set up, but they offer more stability and control over your funds.

Where local options outperform the big global names

A common mistake is assuming that the biggest global gateway is the best choice for every market. In the United States, credit cards dominate. However, in Southeast Asia, QR codes and digital wallets are the standard. Local gateways often outperform global giants in specific regions because they have a greater understanding of local regulations, have better direct integrations with local banks and alternative payment methods (APMs), and have higher authorization rates for domestic cards.

A Step-by-Step Guide to Implementation

Integrating a payment gateway is a pivotal moment for any business as it marks the transition from “concept” to “commerce.” While modern APIs have simplified this process, a structured approach is necessary to ensure security and reliability.

- Select Your Integration Method:

- Hosted Payment Page: The customer is redirected away from your site to a secure page hosted by the gateway. This is the easiest to implement and reduces PCI compliance scope, but offers the least control over branding.

- Direct Post/Drop-in UI: The payment fields appear on your site, but the data is posted directly to the gateway’s servers. This offers a balance of seamless UX and security.

- Server-to-Server (API): You have full control over the UI, and the data passes through your servers before going to the gateway. This offers maximum customization but requires the highest level of PCI compliance (SAQ D) and security infrastructure.

- Obtain Credentials and Configure the Sandbox: Never develop in a live environment. All reputable gateways provide a “Sandbox” or test environment where you can use dummy credit card numbers to simulate successful payments, declines, and errors without moving real money.

- Map Your Error Messages: A common oversight is failing to handle decline codes gracefully. If a transaction fails, your UI should explain why (e.g., “Incorrect Zip Code” vs “Card Declined”) without exposing sensitive security details.

- Validate PCI Compliance: Before you can accept a single real dollar, you must validate your compliance with the Payment Card Industry Data Security Standard (PCI DSS). Depending on your integration method, this may be as simple as filling out a self-assessment questionnaire (SAQ A) or as complex as a third-party audit.

- Go Live and Monitor: Once tested, swap your API keys from “Test” to “Production.” Deeply monitor the first few batches of transactions. Look for “false positives” in fraud detection filters that might be blocking legitimate sales.

The Hidden Pitfalls of Gateway Integration

Even with a robust implementation plan, merchants often stumble into operational traps that hurt conversion rates or lock them into unfavorable contracts. Being aware of these pitfalls can save you from future technical debt.

-

Data Portability and Vendor Lock-in

Becareful when using a gateway’s vault to store customer credit card tokens for recurring billing. Some companies make the process of moving data difficult and costly, making it harder for you to switch providers. Ensure that your contract includes a “Data Portability” or “Token Migration” clause so that you are not held down by one provider.

-

Latency Issues

If your gateway takes more than 3-5 seconds to process a transaction, customers may click the “Pay” button multiple times (causing duplicate charges) or abandon the cart, thinking the site has crashed. Monitor the average response time of your gateway API. If it consistently lags, it may be time to switch providers or optimize your server-side code.

-

Ignoring Mobile Optimization

A gateway interface that works perfectly on a desktop may be unusable on a mobile device. If your customers need to pinch-and-zoom to see your interface, or the number pad doesn’t automatically trigger when the user selects the credit card field, then no one is going to use your mobile conversion. Make sure that the UI components are fully responsive and touch-friendly.

-

Unexpected Friction

Needing an account for doing payment, a lack of options, or a checkout page that doesn’t look secure are all frictions that a customer may not suspect. Many carts have been abandoned because of it. Thus, a modern gateway should address this by applying auto-completion, saving card details for future purchases (tokenization), and mobile-responsive input fields that trigger the correct numerical keyboard on smartphones.

Advanced Gateway Strategies for Scaling Enterprises

A single payment gateway often becomes a bottleneck or a single point of failure as transaction volumes grow. Enterprise-level merchants move beyond simple integration toward sophisticated payment orchestration to adapt.

Payment Orchestration and Smart Routing

Large merchants use a “Payment Orchestration Layer” software that allows the merchant access to multiple gateways. It routes transactions based on specific criteria to optimize success rates and costs; it might route all American Express transactions to Gateway that has better Amex rates and all European transactions to Gateway B, which has local acquiring in Europe. If Gateway A goes down, the system automatically fails over to Gateway B, ensuring 100% uptime.

3D Secure 2.0 Implementation

While security is important, it often reduces sales as windows pop up and customers forget their many passwords. 3D secures 2.0 can make security less of a hassle by sending over 100 data points (device ID, shipping history, etc.) to the issuing bank in the background. If the risk is low, the bank authenticates the user without them ever being bothered by the screen. Implementing this advanced protocol protects you from chargeback liability while maintaining a smooth user experience.

The Real Cost Beyond the Per-Transaction Fee

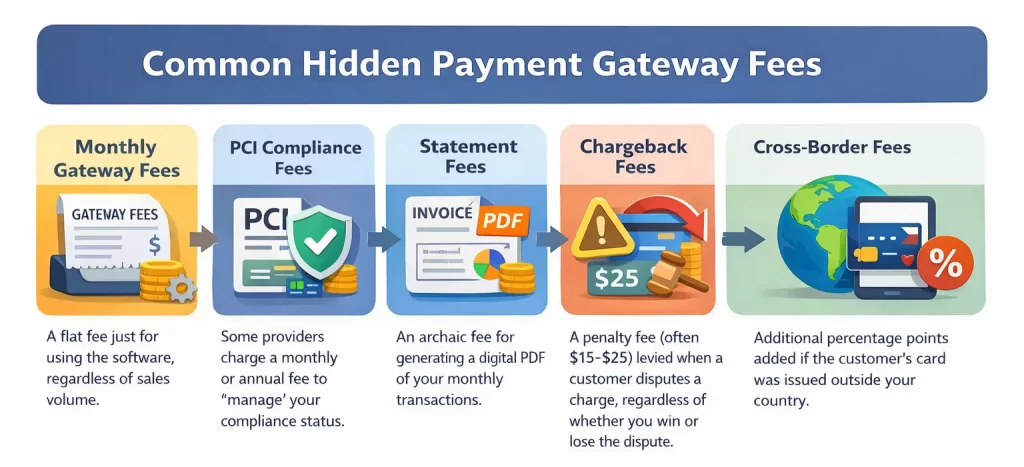

Pricing in the payments industry is notoriously opaque. Most businesses focus on the headline rate, typically something like “2.9% + $0.30”, but this is rarely the full bill. To protect your margins, you must dig deeper into the fee structure.

Setup Fees, monthly charges, and the fine print

Beyond the transactional slice, gateways often carry a variety of supporting fees that can bleed a small business dry if not monitored:

Calculating What You’re Actually Paying Per Sale

To understand your true cost, you need to calculate your “Effective Rate.” Take your total bill for the month (transaction fees + monthly fees + hidden charges) and divide it by your total sales volume.

Example: If you processed $10,000 and paid $350 in total fees, your effective rate is 3.5%.

There are generally two pricing models to consider:

- Flat Rate Pricing: Everyone pays the same percentage (e.g., 2.9%). This is simple and predictable, making it ideal for low-volume businesses.

- Interchange-Plus Pricing: This is the wholesale model. You pay the exact fee the card network charges (Interchange) plus a small markup for the processor. Since interchange rates vary (debit cards are cheaper than premium rewards credit cards), this model is usually cheaper for high-volume businesses. It is more complex to read a statement, but it offers transparency into what you are actually paying for.

Protecting Your Revenue from Chargebacks and Fraud

The dark side of accepting online payments is the risk of fraud. A payment gateway is your first line of defence against bad actors. However, the goal isn’t just to block fraud; it’s to block fraud without rejecting legitimate customers.

Chargebacks dispute

What was once used as a way to protect consumers from identity theft is now used by consumers to commit purchase theft. “Friendly fraud” is not so friendly fraud where legitimate customers make a purchase but later on claim that they didn’t recognize the purchase or just “changed” their mind, but don’t want to return it.

This can be solved by making a robust gateway that allows you to customize the text that appears on the customer’s bank statement. Ensuring it matches your store name exactly is a simple way to reduce friendly fraud significantly.

What PCI Compliance Actually Means for Your Business

PCI DSS (Payment Card Industry Data Security Standard) is a set of rules ensuring that all companies that process, store, or transmit credit card information maintain a secure environment. It is not a law, but a standard mandated by the card networks.

Hosting a gateway will lower your PCI burden (SAQ A) as you never see the card data. However, hosting an API integration will cause the compliance burden to skyrocket (SAQ D) as your servers touch the data. So be careful with what you use; non-compliance can lead to heavy fines and the revocation of your ability to process cards.

This can be bypassed by using modern gateways utilising “Tokenization.” They replace sensitive card data with a unique string of characters (a token). You store the token, and the gateway stores the card, allowing you to offer “one-click” purchasing to returning customers without the liability of storing their actual card numbers.

Tools That Flag Suspicious Transactions Before They Cost You

Modern gateways come equipped with sophisticated fraud filters. You should configure these based on your risk tolerance:

- AVS (Address Verification Service): Checks if the billing address entered matches the address on file with the card issuer. A mismatch is a strong indicator of a stolen card.

- CVV/CVC Checks: Verifies the 3 or 4-digit code on the back of the card. Since this code is prohibited from being stored digitally, a hacker with a stolen database of card numbers usually won’t have the CVV.

- Velocity Checks: Flags multiple transactions coming from the same IP address or using the same card within a short timeframe (e.g., a bot testing card validity).

- 3D Secure 2.0: This is the modern version of “Verified by Visa.” It analyze dozens of data points (device ID, spending history) to authenticate the user silently. If the transaction looks risky, it challenges the user with a biometric prompt or SMS code.

Selling Across Borders Starts With Accepting Local Wallets

Global e-commerce is not just about shipping; it is about settlement. If you restrict your payment methods to USD and major credit cards, you are effectively locking out a vast portion of the global market.

Why International Shoppers Abandon Carts at Checkout

Imagine shopping on a foreign site. You leave the moment you find prices labeled in a currency you don’t know, and the checkout asks for a payment method you don’t have.

This is what we call “Currency Anxiety.” International shoppers don’t know what the final charge will be after their bank applies conversion fees. Furthermore, in markets like Japan (iDEAL) or Brazil (PIX), local payment methods are far more trusted than credit cards. If your gateway doesn’t support these local rails, your conversion rate in those regions will remain near zero.

Supporting Multiple Currencies Without the Operational Nightmare

Advanced gateways offer Multi-Currency Pricing (MCP) and Dynamic Currency Conversion (DCC). MCP allows you to display prices in the customer’s local currency while settling on your own. The gateway handles the daily exchange rate fluctuations. This provides clarity for the customer and stability for the merchant.

Additionally, ensuring your gateway can handle “Local Settlement” is vital. If you have a business entity in Europe, you want your European sales to settle in Euros to a European bank account to avoid double conversion fees. A sophisticated payment stack, potentially integrated with systems like Odoo or HashMicro, can automate the reconciliation of these multi-currency accounts, keeping your books balanced regardless of where the money originated.

Signs It’s Time to Switch Your Provider

Businesses often stick with their first payment gateway long after they have outgrown it. The pain of migration seems too high. However, staying with a legacy provider can cost you significantly in lost conversions and operational inefficiency.

Red Flags That Your Current Setup Is Holding You Back

- Frequent Downtime: It is unforgivable if your gateway goes down on 11.11. Reliability is the baseline requirement.

- Lack of Integration: If your finance team is manually typing transaction data from the gateway into your accounting software, you are wasting valuable time. Your gateway must integrate seamlessly with your ERP or POS system.

- Opaque Rejections: If the gateway is declining transactions with generic error codes, you cannot help your customers fix the issue. You need detailed decline data.

- Slow Settlement: If it takes 5-7 days for funds to hit your account, your cash flow suffers. Modern providers often offer 2-day or even next-day settlement.

Questions to Ask Before Signing With Someone New

Do not rely on the sales pitch. Ask these hard questions:

- “Do you support Level 2 and Level 3 data processing?” (Crucial for B2B merchants to lower interchange rates).

- “What is your chargeback win rate, and do you offer automated dispute management?”

- “Can you provide a dedicated account manager, or will I be stuck in a generic support queue?”

- “Is there a penalty for early termination of the contract?”

How to Test a New Gateway Without Disrupting Live Sales

Never switch your entire volume on day one. Use a routing strategy. Implement the new gateway alongside the old one. You can route 10% of your traffic to the new provider to test authorization rates and user experience.

This is often called A/B testing your payments. If the new gateway performs better (higher conversion, faster load times), you can gradually increase the volume until you are ready to fully decommission the old system.

Tailoring the Gateway: Industry-Specific Use Cases

A generic “out-of-the-box” payment gateway configuration often fails to address the nuanced needs of specific business models. Despite the underlying technology similarity, the application of features varies drastically between a subscription software company and a high-volume retail store. Selecting a gateway that aligns with your specific industry vertical can reduce churn, lower fees, and improve authorization rates.

SaaS and Subscription Models

Involuntary churn happens when a customer’s subscription lapses, not because they wanted to cancel, but because their payment failed. This is a nightmare for businesses relying on recurring revenue. A gateway must offer robust account updater functionality. This feature automatically communicates with card networks to update expired card numbers or new expiration dates without requiring customer intervention.

Furthermore, “dunning management” is essential. This is the automated process of retrying failed transactions at strategic intervals (smart retries) and sending email reminders to customers to update their billing information. A gateway optimized for SaaS handles this logic internally, saving your development team from building complex billing infrastructure.

B2B and Wholesale

Business-to-business transactions differ significantly from B2C due to the sheer size of the transaction values and the types of cards used. Corporate and purchasing cards often carry higher interchange fees. However, gateways that support Level 2 and Level 3 Data Processing can significantly reduce these costs.

By passing additional data fields to the processor, such as line-item details, tax amounts, and customer codes, merchants can qualify for lower interchange rates. For a B2B wholesaler processing millions in volume, switching to a gateway that supports Level 3 processing can save tens of thousands of dollars annually in fees.

International E-Commerce

If you are selling globally, a gateway that only accepts your domestic currency is a conversion killer. Cross-border commerce requires a gateway capable of Multi-Currency Pricing (MCP) and Dynamic Currency Conversion (DCC).

MCP allows customers to browse and pay in their local currency, which builds trust and transparency. The gateway handles the conversion and settles the funds in your preferred currency, shielding you from some volatility while improving the customer experience.

Conclusion

A payment gateway is a vital component for any business that needs to make digital transactions. Through a process of authorization and settlement, a payment gateway provides businesses with a way to make digital transactions safe, easy, and fast for both businesses and consumers.

A payment gateway can take many different forms, each with its benefits and downsides. Some may redirect their customers to a secure host site when making purchases, make it appear as if it were a part of their website, or have full control of the UI.

Apart from the architecture of a payment gateway, there are also other variables like cost, regulations, integration of currency and payment method, providers, and different industry uses. These are all factors that should be considered when implementing a payment gateway, preferably integrated with an ERP systems. The best one is the one most fitting for your needs.

FAQ for Payment Gateway

-

What is the difference between a payment gateway and a merchant account?

A payment gateway is the technology that captures and encrypts card data from the customer (like a digital POS terminal). A merchant account is a specialized bank account that allows you to accept those funds. The gateway sends the data; the merchant account receives the money.

-

Can I use multiple payment gateways on one website?

Yes, many businesses use multiple gateways to provide backup options (redundancy) or to offer different payment methods (e.g., one gateway for credit cards and another for crypto or local wallets). This is often managed through payment orchestration software.

-

How long does it take for a payment gateway to settle funds?

Standard settlement times range from 2 to 7 business days, depending on the provider and your risk profile. However, many modern providers now offer next-day or instant payouts for an additional fee.

-

What is a payment gateway integration?

Integration refers to how the gateway connects to your website or shopping cart. This can be done via a redirect (Hosted), a pre-built plugin (like for WooCommerce or Shopify), or a custom API connection that allows for a fully branded checkout experience.

-

What is the best payment gateway?

The best option depends on your sales channels, target market, preferred payment methods, transaction fees, fraud protection, ease of integration, and whether you need local options like digital wallets or bank transfers. For businesses in the Philippines, the best gateway is usually the one that supports the payment methods your customers already use while keeping checkout secure and smooth.

-

Is it safe to store credit card numbers on my own server?

Generally, no. Storing raw credit card data (PAN) requires a massive security infrastructure to meet PCI DSS Level 1 compliance. It is much safer and cheaper to use