“Buy now, pay later” (BNPL) would have been unthinkable in the past. Consumers were limited to either using the “buy now, pay more later” method with credit cards or reserving an item and then only getting it when fully paid with layaway programs. BNPL allows consumers to make purchases immediately and pay in interest-free installments. With the growing popularity of BNPL, particularly among Millennials and Gen Z, retail merchants now have to adapt to this new payment method by integrating it into their point-of-sale (POS) systems to enhance the customer experience, boost conversion rates, and stay competitive.

Integrating “Buy Now, Pay Later” (BNPL) into point-of-sale (POS) systems isn’t straightforward. Merchants need to ensure compatibility with their existing systems, select a suitable provider, and train their staff to handle new payment methods efficiently. Read the full article to understand the proper process of integration to provide a seamless shopping experience that enhances customer satisfaction.

|

Key Takeaways

|

Understanding Buy Now Pay Later (BNPL)

At its core, the modern deferred payment model is a form of short-term financing that allows consumers to make purchases and pay for them at a future date, typically through a series of equal installments. The most common structure, “Pay in 4,” divides the total cost into four equal payments. Consumers make the first payment at checkout, with the remaining three payments automatically deducted from their linked debit or credit card every two weeks.

The “Pay in 4” plan offers consumers a manageable, predictable repayment schedule. Unlike traditional credit options with their high interest rates, this model typically involves no interest charges if payments are made on time. It allows consumers to make purchases without the burden of high upfront costs, making it an attractive alternative for those who prioritize budgeting and financial control. Additionally, the seamless integration of BNPL options at checkout ensures a smooth, hassle-free shopping experience.

How BNPL Works for Shoppers, Merchants, and Providers

A BNPL payment looks simple on the surface of a checkout register, but behind its simplicity is a complex ecosystem. For a successful transaction, there has to be instantaneous coordination between three primary stakeholders: the consumer, the merchant, and the financial technology provider. Understanding how these entities interact is essential for businesses looking to implement these solutions effectively.

The Consumer Journey at the Digital and Physical Checkout

For consumers, all they have to do is browse the merchant’s website, add items to their cart, and choose the installment payment option at checkout. After entering minimal personal details, the provider quickly conducts a soft credit check, approves the transaction, and links the payment method, ensuring a smooth, uninterrupted purchase experience. The entire process takes seconds, ensuring that the momentum of the purchase is not interrupted, thereby minimizing cart abandonment.

The Merchant’s Role and Immediate Settlement

For the merchant, the mechanics of an installment transaction are remarkably similar to a traditional credit card purchase, albeit with significantly enhanced benefits. A merchant does not assume any credit risk of a consumer completing a purchase using a deferred payment method. Rather, the financial technology provider takes on the full responsibility of collecting the future installments from the consumer.

The provider pays the merchant the full purchase amount upfront, minus an agreed merchant discount rate (MDR). This immediate payment keeps the merchant’s cash flow intact, allowing them to process orders, ship goods, or hand over merchandise without worrying about consumer defaults or late payments. The higher transaction fees are typically offset by increased conversion rates and average order values.

The Provider’s Underwriting and Risk Management Process

The true technological marvel of the buy now pay later ecosystem lies in the provider’s ability to assess risk and underwrite microloans in real-time. Traditional credit checks can take days and often exclude individuals with thin credit files. Modern installment providers bypass these legacy systems by utilizing sophisticated machine learning algorithms and alternative data points to determine creditworthiness instantly.

These algorithms analyze hundreds of data points in real-time, including the consumer’s purchase history, item types, time of day, device information, and even behavioral biometrics. This enables providers to approve most applicants while maintaining low default rates. Additionally, small loan amounts and short repayment periods significantly reduce the provider’s overall risk compared to traditional unsecured lending.

The Psychology Behind the BNPL Boom

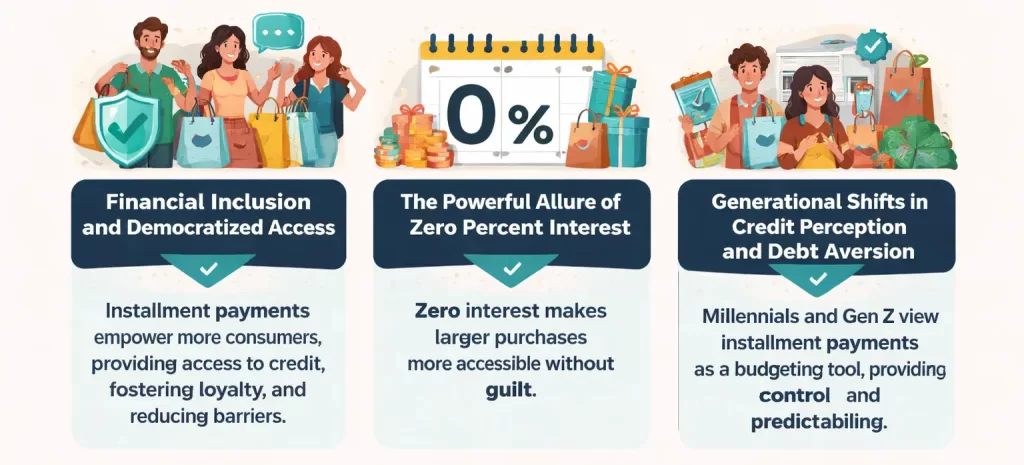

The explosive growth of deferred payment systems cannot be attributed solely to technological advancements; it is equally rooted in deep psychological drivers and shifting consumer mindsets. By understanding the behavioral economics at play, merchants can better tailor their marketing and checkout experiences to align with consumer desires. So here are the reasons why consumers see it as beneficial to use BNPL:

In summary, BNPL provides financial inclusion, fosters loyalty, and encourages larger purchases. Additionally, it is used as a budgeting tool by the younger generation as it offers financial control without the risks of traditional credit.

The Merchant Advantage: Why Retailers are Embracing Flexible Financing

The rapid proliferation of deferred payment options is not only beneficial to consumers, but it is also an advantage for merchants. Despite the higher processing fees associated with these services, the return on investment (ROI) for retailers is exceptionally strong, impacting several key performance indicators across the business.

Driving Exponential Growth in Average Order Value (AOV)

Flexible financing drives a significant increase in Average Order Value (AOV). A $400 shopping cart, which might cause hesitation if paid in a lump sum, suddenly becomes highly attractive when framed as four payments of $100. This psychological shift encourages customers to upgrade or buy more, with AOV increases of 20% to 50%, offsetting higher merchant discount rates.

Significantly Reducing Shopping Cart Abandonment Rates

Shopping cart abandonment is a major challenge in e-commerce, often driven by sticker shock. Displaying installment pricing alongside the full price helps reduce this hesitation. Offering a buy now, pay later option acts as an effective conversion tool, improving checkout conversion rates and capturing revenue that would otherwise be lost to indecision or competitors.

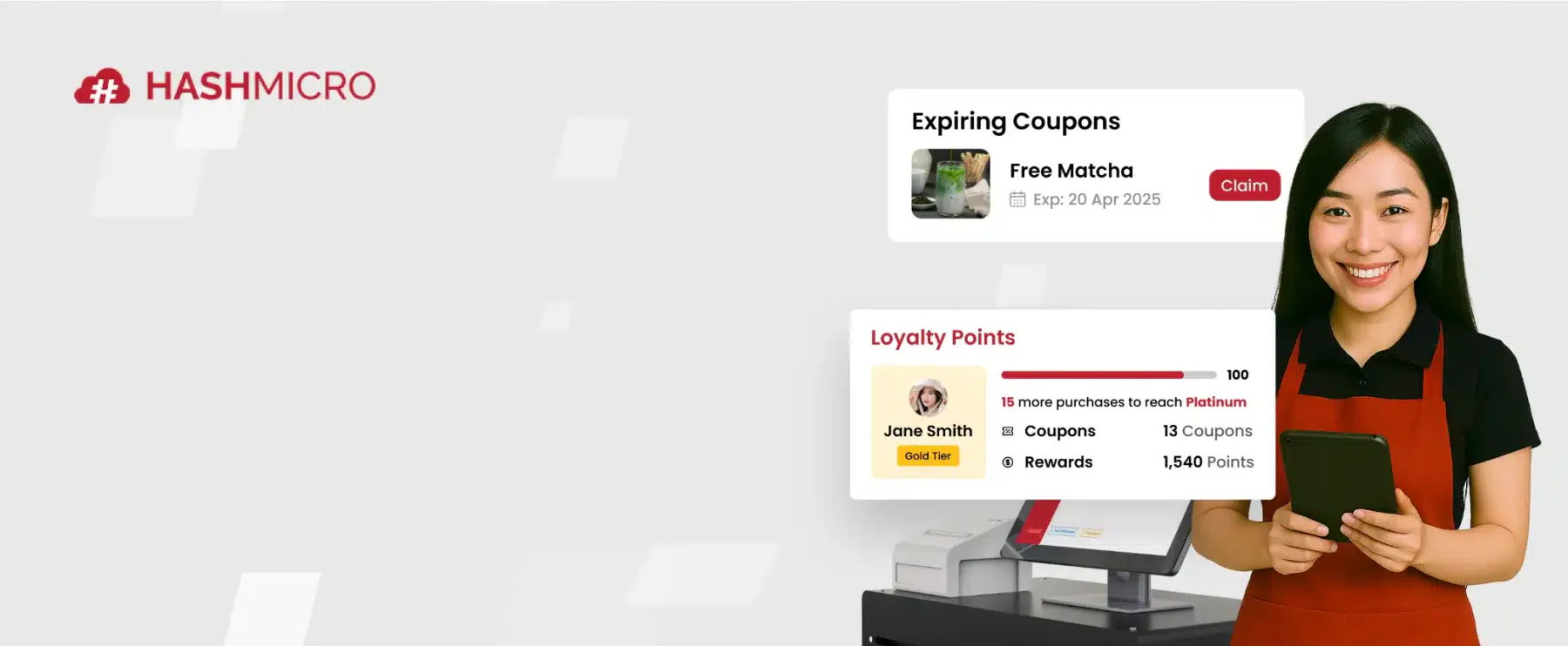

Enhancing Customer Acquisition and Long-Term Brand Loyalty

Alternative financing platforms not only boost transactions but also serve as powerful customer acquisition channels. Partnering with installment providers exposes merchants to a large, engaged audience. Offering flexible payment options fosters loyalty, creating a positive, frictionless checkout experience that encourages repeat purchases, making payment flexibility a strategic tool for both customer acquisition and retention.

How to Strategically Integrate BNPL

Successfully integrating BNPL into your retail infrastructure requires a well-planned approach. Disorganized implementation can cause technical issues and disrupt checkout flows. Merchants must ensure seamless integration across both digital and physical channels.

Here are the key steps to integrate BNPL effectively:

- Vendor Evaluation and Selection: Assess potential partners based on target demographics, terms, and geographic coverage. Evaluate merchant discount rates (MDR), approval rates, and consumer fairness.

- Technical Integration with POS and E-commerce Platforms: Ensure smooth integration with POS systems and e-commerce platforms. Use dynamic pricing and API connections to simplify checkout and facilitate secure credit approval.

- Staff Training and Omnichannel Alignment: Train staff on processing BNPL transactions and positioning payment options as sales tools. Ensure a unified experience across both online and in-store channels.

- Marketing and Consumer Education: Promote BNPL options through website banners, email campaigns, and in-store signage. Educate consumers on terms, benefits, and zero-interest periods to encourage adoption.

- Bridging Online and Offline Data: Ensure transaction data flows into centralized ERP and CRM systems for tracking customer lifetime value and analyzing purchasing trends.

- Simplify Financial Reconciliation: Automate the financial reporting process, distinguishing between traditional credit and alternative financing payments to improve operational efficiency.

By following these steps, you’ll ensure seamless BNPL integration, providing a smooth and unified experience for your customers.

Industry-Specific Use Cases for BNPL

Knowing how to apply BNPL in different industries is needed to unlock new revenue streams for merchants in untapped markets. Here is how BNPL is used in three different industries:

Managing the Risk of BNPL Integration

Despite the overwhelming advantages, the integration of alternative financing is not without its challenges. Merchants must maintain a clear-eyed perspective on the potential operational and financial risks associated with deferred payment models and proactively develop mitigation strategies.

Here are the five common risks and the methods of mitigation:

- Margin Compression and Merchant Fees: BNPL providers charge higher processing fees (2% to 6%) compared to credit card networks. Merchants should model financial projections to ensure increased conversion rates and AOV outweigh the higher fees.

- Return Abuse and Refund Complexities: Handling returns is more complicated with BNPL. Clear return policies and real-time API synchronization between the POS and provider are essential to avoid customer issues.

- Regulatory Scrutiny and Compliance Risks: As BNPL grows, it attracts regulatory attention. Merchants must partner with compliant providers who follow local financial regulations, avoiding reputational and legal risks.

- Managing Increased Merchant Discount Rates: BNPL processing fees can be 4% to 8%. Merchants should track the impact on gross profit and adjust pricing strategies to offset the higher fees.

- The Operational Complexity of Returns and Refunds: Returning BNPL items complicates the refund process. Merchants must use integrated systems to ensure timely and accurate refund processing, minimizing operational disruptions.

Pay attention to these difficulties to avoid any problems from implementing BNPL.

Comparing BNPL Providers in the Philippines

Integrating BNPL does not only involve your POS system, but also the providers. Here are some of the most popularly used BNPL providers in the Philippines:

| Category | Atome | HashMicro | BillEase | Plentina | Cashalo PayLater |

|---|---|---|---|---|---|

| Official Site | Atome Philippines | HashMicro POS | BillEase Official | Plentina Official | Cashalo Official |

| Key Features | Up to ₱200,000 limit, 0% for 40 days, flexible 6-month plans | Supports BNPL-ready POS workflows, centralized transaction tracking | Up to ₱40,000 credit, flexible 30-day to 12-month plans | Easy small-purchase credit via app; simple approval | Integrated BNPL on partner merchants; flexible installment offers |

| Transaction Limits | Up to ₱200,000 spending limit | Depends on the connected BNPL provider and merchant policy | Up to ₱40,000 credit line | Min ₱100 loan, max grows with use | Varies by merchant and plan; not official site detail |

| Repayment Terms | Up to 6 months | Follows the repayment terms of the integrated BNPL provider | 30 days up to 12 months | 14, 30, 60 days (typical) | Depends on lender or partner plan; not official site detail |

| Typical Billing Cycle | 0% interest for the first 40 days | Syncs provider billing schedules with POS records and reporting flows | Weekly or monthly options | Short cycles (14 to 60 days) | Merchant-dependent schedules |

| Best For | High-limit BNPL and larger purchases | Retailers that want BNPL flexibility with POS, inventory, and reporting in one connected system | Longer-term installment flexibility | Everyday small purchases and essentials | General BNPL usage across merchants |

Conclusion

Buy now, pay later (“BNPL”) is gaining traction for young consumers as it provides greater flexibility and financial control. Business owners must catch up and also get the benefits of BNPL, which include higher conversion rates, increased average order values, reduced cart abandonment, and enhanced customer loyalty.

To implement BNPL, merchants must integrate the solution into their POS system, ensuring seamless transactions and training staff on how to offer flexible payment options effectively. That is why you must find the right POS system that is available in the Philippines.

FAQ for Buy Now Pay Later

Who is eligible for pay later?

Consumers with a valid ID, stable income, and good credit history are typically eligible for BNPL. Providers assess each applicant based on their financial profile and the purchase amount.

How do you get approved for buy now, pay later?

To get approved, consumers provide basic personal details, undergo a soft credit check, and link a payment method. Providers quickly assess risk and approve the transaction within seconds.

What do businesses need to integrate BNPL into their POS system?

Businesses need to select a BNPL provider, integrate their API or plugin into the POS system, train staff, and ensure synchronization with inventory and financial systems for seamless transactions.

What should businesses consider when selecting a BNPL provider?

Businesses should consider transaction fees, repayment terms, customer support, integration ease, and the provider’s reputation to ensure a seamless, cost-effective, and customer-friendly BNPL solution.