Based on official guidelines from the Bureau of Internal Revenue (BIR), individuals and organizations must secure a Certificate of Exemption or BIR ruling to legally claim tax-exempt status under the National Internal Revenue Code and related laws. From an economic perspective, governments utilize tax exemptions to allocate resources more efficiently.

When an entity operates on a not-for-profit basis to serve the community, taxing its revenue would diminish its capacity to deliver essential services, thereby forcing the government to step in and provide those services directly at a higher cost to the taxpayer. Therefore, granting a tax-exempt status is often viewed as a social contract: the organization is relieved of its tax burden in exchange for providing measurable public benefits.

However, achieving and maintaining this specialized status is not a passive endeavor. It requires meticulous record-keeping, strict adherence to evolving legislative frameworks, and a proactive approach to financial management. The stakes are incredibly high; mishandling exempt transactions or failing to meet reporting requirements can result in severe financial penalties, rigorous audits, and the potential revocation of the exempt status itself.

|

Key Takeaways

|

What is Tax Exempt Status?

It refers to specific entities or transactions being relieved from the obligation to pay certain taxes. This includes exemptions from income tax, sales tax, and other levies. For businesses and organizations, this status offers significant financial relief, but it also comes with regulatory requirements. Being granted tax-exempt status is often reserved for specific types of organizations, such as non-profits, religious groups, and government entities

Entities with tax-exempt status do not pay certain taxes on their income or transactions. This means they can allocate more of their funds toward their core activities. However, to maintain this status, they must adhere to certain guidelines set by the government, such as restricting their activities to charitable, religious, or educational purposes. In the Philippines, this status is granted by the Bureau of Internal Revenue (BIR) and requires the submission of relevant documents to prove eligibility.

Types of Tax-Exempt Entities and Organizations

Various organizations in the Philippines may qualify for tax-exempt status, depending on BIR rules and the entity’s legal purpose. Common examples include non-stock, non-profit organizations, religious institutions, educational institutions, and other entities recognized under Philippine tax laws.

| Tax-Exempt Entity | Description | Key Requirements |

| Charitable and Philanthropic Organizations | Organizations formed for religious, educational, scientific, literary, or public safety purposes. | Must ensure profits aren’t distributed to private individuals; restrict political campaigns and lobbying activities. |

| Educational Institutions | Schools, colleges, universities, and other educational bodies that generally qualify for tax exemption. | Revenue from non-educational activities may be subject to tax liabilities. |

| Religious Organizations | Churches, mosques, synagogues, and temples, granted tax-exempt status under the principle of separation of church and state. | Exempt from most taxes, but some reporting requirements may differ from other non-profits. |

| Trade Associations and Chambers of Commerce | Organizations formed to promote the interests of their members rather than the public. | Exempt from income tax on dues but donations to these organizations are typically not tax-deductible as charitable contributions. |

| Government Entities | Federal, state, and local government bodies, including agencies and instrumentalities, are inherently tax-exempt. | Exempt from income taxes, property taxes, and often sales and use taxes. |

How Tax-Exempt Status Affects on Financial Planning

They can reinvest savings from tax exemptions back into their operations, increasing their capacity to serve their mission. However, failing to maintain tax-exempt status due to non-compliance can result in penalties, back taxes, and a loss of credibility. Therefore, continuous compliance with BIR requirements and review from entities preparing formal reports is essential to maintain this status.

1) Structuring the Chart of Accounts

For exempt organizations, the Chart of Accounts (CoA) must be structured to track funds based on donor restrictions rather than just standard revenue and expense categories. Accountants must segregate funds into categories such as:

- Unrestricted Net Assets: Funds that the organization’s board of directors can use at its discretion for any legitimate purpose.

- Temporarily Restricted Net Assets: Funds subject to donor-imposed stipulations that will be met either by actions of the organization or the passage of time.

- Permanently Restricted Net Assets: Funds subject to donor-imposed stipulations that they be maintained permanently by the organization (e.g., endowments).

2) Managing Unrelated Business Income Tax

Even if an organization is broadly tax-exempt, it must pay taxes on income generated from a trade or business that is regularly carried on and is not substantially related to the organization’s exempt purpose. For example, if a university operates a commercial hotel on its campus that is open to the general public, the revenue from that hotel may be subject by BIR.

Accountants must meticulously allocate expenses between exempt activities and unrelated business activities to accurately calculate the other liability. Clear reporting becomes easier when teams understand the difference between square-footage allocations for facility costs or time-tracking allocations for personnel costs.

3) Financial Statement Presentation

The financial statements of a tax-exempt organization differ significantly from those of a for-profit corporation. Instead of an Income Statement, exempt organizations issue a Statement of Activities, which details the changes in net assets. Instead of a Balance Sheet, they issue a Statement of Financial Position. Additionally, they are often required to produce a Statement of Functional Expenses, which breaks down costs by their functional classification (e.g., program services, management and general, and fundraising).

How to Secure and Maintain Tax-Exempt Status

For accounting and legal professionals guiding an organization through this process, a systematic implementation strategy is needed to ensure immediate compliance and long-term financial health.

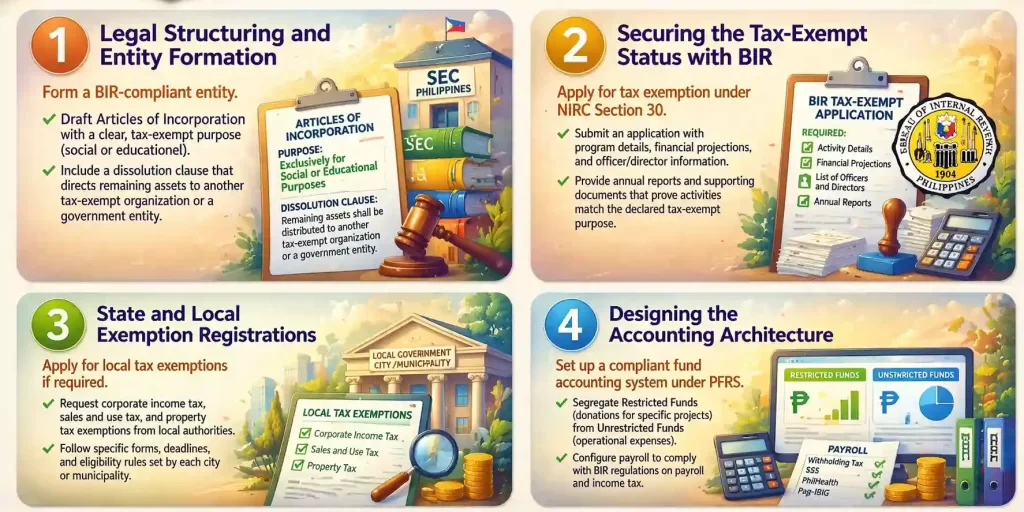

Step 1: Legal Structuring and Entity Formation

Form a legal entity in compliance with BIR (Bureau of Internal Revenue) regulations. This starts with drafting the Articles of Incorporation, which must clearly state the organization’s purpose aligned with tax-exempt activities.

For example, to qualify as a non-profit organization in the Philippines, the document should specify that the entity is formed exclusively for social or educational purposes. A dissolution clause must also be included, specifying that remaining assets will be distributed to another tax-exempt organization or a government entity upon closure.

Step 2: Securing the Tax-Exempt Status with BIR

Next step is to apply for tax-exempt status with the BIR. This involves submitting a comprehensive application that includes details about the organization’s activities, financial projections, as well as information about officers and directors. The organization is also required to submit annual reports and documentation that show its activities are in line with the stated tax-exempt purpose.

This step is crucial to ensure the entity meets the criteria under the National Internal Revenue Code (NIRC), particularly Section 30, which outlines tax exemptions for non-profit organizations.

Step 3: State and Local Exemption Registrations

After receiving approval from BIR, the organization must separately apply for tax exemptions at the local level, if applicable. This includes applying for corporate income tax exemptions, sales and use tax exemptions, and property tax exemptions from local authorities. Each region or city in the Philippines may have its own forms, deadlines, and eligibility criteria that the organization must meet.

Step 4: Designing the Accounting Architecture

Once legal status and tax exemption are granted, the organization must establish a financial system that complies with applicable standards for non-profits. In the Philippines, this follows Philippine Financial Reporting Standards (PFRS), which require organizations to segregate restricted funds (e.g., donations for specific projects) from unrestricted operational funds.

The accounting software solution in the Philippines must be capable of segregating restricted funds (donations for specific projects) from unrestricted operational funds. Additionally, the payroll system must account for tax provisions related to non-profit employees, governed by BIR regulations on payroll and income tax.

Why BIR Can Reject or Question a Tax-Exempt Application

BIR does not look at the label non-profit alone. It checks whether the organization passes both the organizational test and the operational test. Under RMO No. 38-2019, the SEC registration papers, Articles of Incorporation, and by-laws must show that the entity’s primary purposes fall under Section 30 of the NIRC. The entity’s regular activities must also be devoted to those purposes, not to profit-driven operations.

-

Missing or incomplete documents slow the case

BIR uses checklist-based requirements for rulings, including a dedicated checklist for Non-Stock and Non-Profit (Sec. 30) applications. It also validates the accuracy and completeness of documentary requirements during processing. When the file lacks core papers such as SEC registration documents, by-laws, activity details, or financial support, the application can stall before substantive review even starts.

-

Weak purpose clauses can fail the organizational test

A vague purpose clause creates risk immediately. BIR requires the constitutive documents to show that the corporation was organized for a Section 30 purpose, and the dissolution clause must direct remaining assets to one or more entities with similar exempt purposes or to the Philippine government for public purpose. If the papers do not say that clearly, the application becomes vulnerable to rejection or reworking.

-

Mixed-profit activity can break the operational test

BIR can question an application when a substantial part of the organization’s operations consists of activities conducted for profit. The rule is strict: Section 30 entities remain exempt only on income earned in furtherance of their exempt purpose. Income from interest, investments, rentals, or other profit-oriented activity can still be taxable, even after the entity secures exempt status.

-

Documentation gaps raise private-benefit questions

BIR also checks whether earnings or assets benefit insiders. RMO No. 38-2019 lists red flags such as compensation or honoraria to trustees or organizers, unreasonable employee compensation, welfare or financial assistance to members, donations to unrelated parties, and purchases above fair market value from related parties.

When an organization cannot support salaries, grants, purchases, and fund use with clear records, board approvals, and source documents, BIR has reason to question whether the entity is truly operating on a non-profit basis.

Compliance and Reporting Requirements For Philippines Business

Tax exemption offers significant benefits but comes with the responsibility of strict compliance and transparency. Organizations must consistently demonstrate to regulatory authorities that they are operating within the framework of their exempt status.

-

The Initial Application Process

Obtaining tax-exempt status is a detailed and thorough legal and financial process. Organizations must submit comprehensive applications to the relevant tax authorities, providing structural governance details, a narrative of proposed activities, and financial projections. The Articles of Incorporation must include specific language that irrevocably dedicates the organization’s assets to its exempt purposes.

-

Annual Informational Returns

Although tax-exempt organizations do not pay income taxes, they are still required to file extensive annual informational returns. These returns are public records that offer insight into the organization’s financial standing, governance practices, executive compensation, and program accomplishments. Preparing these returns requires close collaboration between internal accounting teams, external auditors, and legal advisors.

-

State and Local Compliance

Compliance extends beyond federal requirements. Organizations with federal tax-exempt status must often apply separately for exemptions at the state level, including income tax exemptions, property tax exemptions, and sales tax exemptions. Each jurisdiction has its own forms, deadlines, and renewal criteria. A decentralized approach to managing these multiple compliance layers can lead to significant errors and unexpected tax assessments.

What Tax-Exempt Entities Still Need to File in the Philippines

BIR still requires exempt corporations under Section 30 to file the proper annual return or annual information return, and the entity remains a withholding agent when it pays compensation or other income subject to withholding tax.

1. Annual BIR return and withholding reports

The BIR maintains Form 1702-EX for corporations, partnerships, and other non-individual taxpayers exempt under the Tax Code, including Section 30 entities. BIR guidance also states that exempt taxpayers are still required to file an annual income tax return/annual information return with Audited Financial Statements. On top of that, tax exemption does not cover withholding obligations on employee compensation or on payments to suppliers and service providers that are subject to withholding rules.

2. SEC filings continue after BIR approval

A non-stock corporation does not stop reporting to the SEC after obtaining tax-exempt status. The SEC’s eFAST guide states that Financial Statements must be filed within 120 calendar days after the end of the fiscal year, while the General Information Sheet (GIS) must be filed within 30 calendar days from the date of the annual meeting. The same guide also shows that non-stock corporations may need the appropriate NSPO attachments, depending on the amount of annual contributions or donations.

3. CTE validity must still be monitored

For many Section 30 entities, a Certificate of Tax Exemption (CTE) issued under RMO No. 38-2019 is valid for three years and may be revalidated under the same procedure. BIR can also revoke the ruling when there are material changes in the entity’s character, purpose, or method of operation that no longer match the basis for exemption.

BIR later clarified that some entity types follow different validity treatment, so organizations should check whether their category falls under a special rule before assuming the three-year cycle applies.

4. Books and proof must stay audit-ready

Under the EOPT rules and RR No. 7-2024, books of accounts and other accounting records must generally be preserved for five years from the due date of the return or the actual filing date, depending on the case. That matters because BIR can review whether the organization’s actual activities, receipts, payroll, restricted-fund use, and disbursements still match the exempt purpose declared in its ruling and constitutive documents.

In practice, that means keeping audited financial statements, ledgers, invoices, payroll records, donor restrictions, grant agreements, and board resolutions organized and accessible.

Conclusion

Tax-exempt status provides organizations with significant financial advantages, but it also comes with a complex array of responsibilities. Organizations must navigate legal structuring, secure federal and state-level exemptions, and adhere to rigorous compliance and reporting standards. This continuous process of maintaining tax-exempt status requires diligence, proper governance, and consistent communication with regulatory authorities.

To explore more about managing financial operations and compliance, check out HashMicro’s Accounting Software Solutions to streamline your business’s tax and financial management processes.

Frequently Asked Questions Around Tax Exempt Status

Who qualifies for tax-exempt status?

Non-profit organizations, educational institutions, religious organizations, and government bodies typically qualify for tax-exempt status.

Is sales tax exempt from all purchases?

Sales tax is only exempt for certain purchases made by qualifying entities; personal purchases typically still incur sales tax.

How do I apply for tax exemption in the Philippines?

You need to submit documents like your Articles of Incorporation, financial statements, and a formal application to the Bureau of Internal Revenue (BIR).

When should a business consider becoming tax-exempt?

A business should consider this if it shifts focus to non-profit activities, such as charitable work or education.