While profitability often takes the spotlight, liquidity is what keeps a business stable. Without the ability to meet short term obligations, even profitable companies can face insolvency.

The quick ratio is a key indicator of short-term liquidity, excluding less liquid assets to provide a clear view of a company’s capacity to cover debts. Mastering this metric is crucial for financial stability and resilience.

Key Takeaways

The quick ratio measures a company’s ability to cover short term liabilities with liquid assets, excluding inventory. A high ratio signals stability, while a low one may indicate cash flow issues. It’s crucial for assessing financial readiness in tough situations.

There are two ways to calculate the quick ratio by summing liquid assets and dividing by liabilities, or by subtracting inventory and prepaid expenses from total assets. Both methods assess a company’s ability to cover short-term liabilities with liquid resources.

Relying only on the quick ratio can be misleading. It overlooks cash flow timing, the quality of receivables, and available credit lines, while management may also manipulate it, distorting the true financial picture.

What Is the Quick Ratio and Why It Matters

The quick ratio, or “acid-test ratio,” measures a company’s ability to cover short-term liabilities without relying on inventory or less liquid assets. It excludes inventory and prepaid expenses, focusing on liquid assets like cash and receivables available for immediate use.

This metric helps assess a company’s ability to handle sudden revenue drops. A strong quick ratio indicates financial stability, while a weak one signals potential cash flow issues or the need for restructuring. Financial analysts use it to evaluate a company’s readiness for worst case scenarios.

How to Calculate the Quick Ratio (Simple Formula)

Calculating this liquidity metric requires precise data extraction from a company’s balance sheet. There are two primary ways to calculate the metric, both of which yield the same result provided the balance sheet is accurately categorized. Understanding both methods provides a more holistic view of asset classification.

Calculating this liquidity metric requires precise data extraction from a company’s balance sheet. There are two primary ways to calculate the metric, both of which yield the same result provided the balance sheet is accurately categorized. Understanding both methods provides a more holistic view of asset classification.

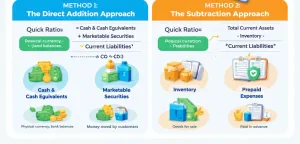

Method 1: The Direct Addition Approach

This method involves manually summing up the most liquid current assets and dividing them by total current liabilities. The formula is structured as follows:

Quick Ratio = (Cash & Cash Equivalents + Marketable Securities + Accounts Receivable) / Current Liabilities

Let us break down each component of this formula in granular detail:

- Cash & Cash Equivalents: Includes physical currency, bank balances, and short-term investments (e.g., Treasury bills) that are immediately available to settle debts.

- Marketable Securities: Liquid financial instruments like stocks and bonds that can be quickly converted to cash within the operating cycle.

- Accounts Receivable: Money owed by customers for credit sales, typically collected within 30 to 90 days, net of doubtful accounts.

- Current Liabilities: Short-term financial obligations due within one year, including accounts payable, short-term debt, and accrued liabilities.

Method 2: The Subtraction Approach

The alternative method starts with the total current assets and subtracts the less liquid components. This is often faster if you are looking at a summarized balance sheet.

Quick Ratio = (Total Current Assets – Inventory – Prepaid Expenses) / Current Liabilities

Prepaid expenses are paid in advance for future goods or services (e.g., insurance premiums). While classified as current assets, they cannot be quickly converted into cash to settle liabilities, so they are excluded from the quick ratio calculation.

Companies can automate these calculations using an accounting software to ensure real time financial insights.

Limitations and Pitfalls of Relying Solely on the Quick Ratio

While the quick ratio is a formidable tool for financial diagnosis, relying on it in isolation can lead to dangerous analytical blind spots. Financial metrics are only as reliable as the data feeding them, and they represent a static snapshot of a moving target. Analysts must be acutely aware of the following limitations:

| Category | Key Elements | Why It Matters |

| The Timing of Cash Flows | Accounts receivable and payable, cash flow timelines | The quick ratio overlooks when cash flows occur, potentially misleading liquidity assessment. |

| The Quality of Accounts Receivable | Allowance for doubtful accounts, aging receivables | The quick ratio assumes all receivables are collected, which may not be the case in times of economic stress. |

| “Window Dressing” by Management | Manipulating payment schedules, boosting cash balances | Companies may artificially inflate liquidity metrics to meet short-term goals, distorting the ratio. |

| Ignoring Revolving Credit Facilities | Untapped lines of credit, credit facilities | The quick ratio fails to account for available credit, which can significantly improve a company’s liquidity. |

Strategic Best Practices for Improving Your Company’s Liquidity

For financial controllers, CFOs, and business owners, actively managing and optimizing liquidity is a daily operational imperative. If a company finds its quick ratio slipping into dangerous territory, proactive strategies must be deployed to stabilize the balance sheet. Improving this metric generally requires a two pronged approach: accelerating cash inflows and strategically managing liability outflows.

For financial controllers, CFOs, and business owners, actively managing and optimizing liquidity is a daily operational imperative. If a company finds its quick ratio slipping into dangerous territory, proactive strategies must be deployed to stabilize the balance sheet. Improving this metric generally requires a two pronged approach: accelerating cash inflows and strategically managing liability outflows.

Accelerating Accounts Receivable Collection

Since accounts receivable form a massive portion of the numerator in our formula, converting them to cash faster directly improves liquidity.

- Implement Dynamic Discounting: Offer a 2/10 Net 30 discount for early payments to improve liquidity.

- Tighten Credit Policies: Implement stricter credit checks and switch slow-payers to COD or upfront deposits.

- Utilize Invoice Factoring: Sell receivables to third-party factors for immediate cash, improving liquidity at a higher cost.

Optimizing Current Liabilities

Managing the denominator of the equation is equally critical. Reducing current liabilities or extending their maturity dates will mathematically improve the ratio.

- Renegotiate Supplier Terms: Extend accounts payable terms from 30 to 45 or 60 days, keeping cash longer and improving liquidity.

- Refinance Short Term Debt: Refinance short term loans into long-term debt to reduce current liabilities and improve liquidity.

- Sweep Accounts and Cash Management: Use automated zero-balance and sweep accounts to move excess cash into interest bearing investments.

Future Trends: Technology and Liquidity Analysis in 2026

In 2026, financial analysis and liquidity management are being reshaped by AI and automation, allowing businesses to monitor cash flows, receivables, and liabilities in real time. AI tools predict liquidity needs, adjusting for market shifts and disruptions, providing more accurate insights for decision-making.

Real time data integration into ERP systems allows companies to access up-to-date financial reports for quicker, informed decisions. Automation handles tasks like invoicing and credit management, reducing errors. As a result, traditional metrics like the quick ratio are being replaced by more dynamic models, improving business agility in an unpredictable financial environment.

Industry Specific Applications: How the Quick Ratio Varies by Sector

While a ratio of 1.0 is historically touted as the gold standard of liquidity, applying a universal benchmark across all sectors is a fundamental error in financial analysis. The quick ratio is highly contextual and is heavily influenced by an industry’s underlying operational model, capital requirements, and working capital dynamics.

| Sector | Quick Ratio Range | Explanation |

| Retail and E-Commerce | 0.2 – 0.5 | Retailers maintain low quick ratios due to fast inventory turnover and immediate cash collection from sales. |

| Software as a Service (SaaS) and Technology | >2.0 | SaaS companies have high ratios, holding little inventory and relying on cash, investments, and receivables. |

| Manufacturing and Heavy Industry | Around 1.0 | Manufacturers aim for a balanced ratio to ensure liquidity even when production stalls or inventories become illiquid. |

How to Monitor Your Quick Ratio Effectively

Calculating this metric once a quarter for an earnings report or annual review is entirely insufficient for proactive financial management. To leverage the acid-test as a true operational compass, corporate finance teams must implement systematic, continuous monitoring processes.

Calculating this metric once a quarter for an earnings report or annual review is entirely insufficient for proactive financial management. To leverage the acid-test as a true operational compass, corporate finance teams must implement systematic, continuous monitoring processes.

- Standardize Asset Categorization: Ensure accurate asset classification by excluding prepaid expenses and restricted cash from quick assets.

- Automate Real Time Tracking via ERP Integration: Use ERP systems for live liquidity tracking, enabling CFOs to monitor fluctuations daily or weekly.

- Establish Contextual Baselines and Alerts: Set historical baselines and automated alerts to notify executives when the ratio falls below critical thresholds.

- Align Cross Departmental Operations: Educate sales and collections teams on how their actions impact the quick ratio, preventing uncollectible debt.

The Hidden Traps of the Quick Ratio You Should Watch Out For

The quick ratio can be misleading, especially if a large portion of accounts receivable is overdue or tied to risky clients. Without checking an Accounts Receivable Aging Report, it’s easy to misjudge liquidity.

It also ignores the timing of liabilities. A company may have a healthy ratio, but if most liabilities are due soon, a liquidity issue can arise. Additionally, “window dressing” tactics like delaying purchases or pushing for early payments can temporarily inflate the ratio, hiding the true liquidity situation.

Advanced Practices in Next Level Liquidity Management

Advanced analysts run the quick ratio through various stress test scenarios, such as customer defaults or supply chain disruptions, to evaluate worst case liquidity. By applying “haircuts” to receivables and cash, they assess a company’s true financial resilience.

Seasonal businesses can smooth out volatility by using rolling averages, offering a clearer view of long term liquidity. Combining the quick ratio with the Cash Conversion Cycle (CCC) is also crucial, as companies with fast CCCs may be more agile financially, even with a lower quick ratio.

Conclusion

While the quick ratio is an important liquidity metric, it can be misleading if not considered alongside other factors, such as the quality of receivables or timing of liabilities. Relying solely on it can mask underlying issues.

Businesses that want to explore the right accounting tools to track these factors more accurately can start with this guide on the best accounting software in the Philippines

FAQ About Quick Ratio in the Philippines

The quick ratio can overstate liquidity if a large portion of accounts receivable is overdue. It’s essential to monitor receivables aging reports to avoid this issue.

The quick ratio includes current liabilities without considering their due dates. Where cash flow timing is affected by delayed payments, this can result in an inaccurate liquidity assessment.

“Window dressing” actions, such as pushing for early payments or delaying purchases, can artificially inflate the quick ratio, masking the true financial situation.

Philippine companies can simulate worst-case scenarios like large customer defaults or supply chain disruptions to stress-test their liquidity. This helps in better understanding their true financial resilience in challenging situations.

Retail businesses in the Philippines face seasonal fluctuations, especially during holidays and special events. Using rolling averages can smooth out these cycles and offer a clearer picture of long-term liquidity.