Free on Board (FOB) has been a concept since people still used sailing vessels. Historically, the term literally meant that the seller’s obligation was fulfilled once the goods were placed “free” (without cost to the buyer) “on board” the vessel designated by the buyer. But in contemporary supply chain operations, FOB is a legally binding agreement embedded in commercial contracts, purchase orders, and letters of credit.

FOB defines who pays freight, who bears transit risk, and when ownership transfers. These terms shape inventory control, financial reporting, and legal responsibility in domestic and international trade. Misunderstanding them can trigger shipment disputes, costly losses, and accounting issues, making FOB essential for supply chain decisions today.

Table of Contents

Key Takeaways

|

Understanding the Fundamentals of Free on Board (FOB)

FOB defines three key aspects: transportation costs, risk allocation, and the transfer of title. It dictates who pays freight, who handles insurance claims, and when ownership transfers. FOB’s interpretation varies by jurisdiction; the Philippine Commercial Code governs domestic trade in the Philippines, while Incoterms applies internationally. Failing to specify the framework can lead to legal disputes.

Domestic and International Legal Considerations

Domestic and international laws are often mistaken for being the same. Businesses must know the fundamental differences between the two.

The Intersection of FOB and Incoterms 2020

Under Incoterms 2020, FOB applies only to sea and inland waterway transport. It dictates risk and ownership transfer when goods are loaded onto the buyer’s designated vessel. The buyer assumes responsibility and costs from that point onward. Misunderstanding this can lead to costly mistakes in international trade.

For containerized shipments, FOB is not ideal. The FCA (Free Carrier) term is recommended since goods are often handed over to the carrier at a terminal before being loaded onto the ship. Using FOB in this scenario creates risk gaps, as the seller may remain liable even after losing physical control of the goods.

Domestic Trade Laws in the Philippines

In the Philippines, FOB terms must be clearly defined in contracts, ensuring alignment with both Incoterms and local laws. The Civil Code of the Philippines (Republic Act No. 386) governs property transfers, specifying that goods remain at the seller’s risk until ownership is transferred, after which risk shifts to the buyer (Article 1524).

For tax compliance, businesses must follow the National Internal Revenue Code and BIR regulations, covering VAT and documentary stamp taxes on goods transfers. Proper documentation is required for the sale, transfer, or exchange of goods, ensuring tax obligations are met.

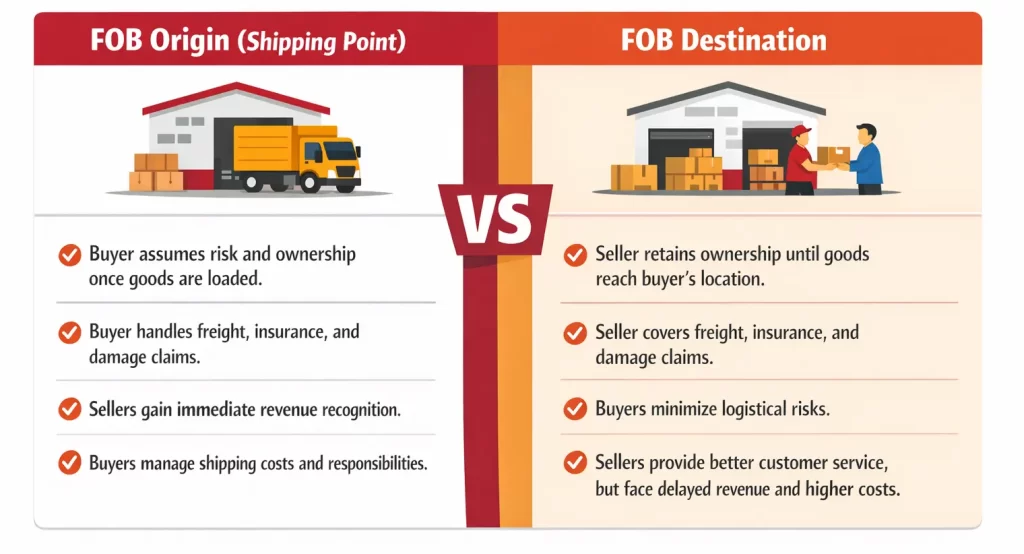

The Critical Distinctions: FOB Origin vs. FOB Destination

In the Philippines, under domestic commercial law, FOB is generally divided into two main categories: FOB Origin (also known as FOB Shipping Point) and FOB Destination.

Understanding the stark contrast between these two variations is essential for effective supply chain risk management and precise financial accounting.

Freight Payment Variations

To add another layer of granularity, both Origin and Destination terms are frequently modified by freight payment conditions. These modifiers explicitly separate the transfer of risk from the payment of freight charges, creating four common hybrid scenarios:

- FOB Origin, Freight Prepaid: The buyer takes ownership and risk at the point of origin, but the seller pays the shipping costs. The seller usually incorporates these costs into the overall price of the goods.

- FOB Origin, Freight Collect: The buyer assumes risk at the origin and is also responsible for paying the freight carrier directly upon delivery.

- FOB Destination, Freight Prepaid: The seller retains risk until delivery and pays the freight charges. This is the most traditional interpretation of FOB Destination.

- FOB Destination, Freight Collect: The seller retains the risk of the goods during transit, but the buyer pays the freight charges upon arrival. The buyer typically deducts this freight cost from the final invoice paid to the seller.

FOB and Shipping Costs

| FOB Term | Seller Responsibility | Buyer Responsibility | Typical Shipping Costs in PHP |

| FOB Origin, Freight Prepaid | Seller pays freight | Buyer assumes risk once goods are shipped | ₱20,000 – ₱50,000 (depending on distance) |

| FOB Origin, Freight Collect | Buyer pays freight directly to the carrier | Buyer assumes risk from the point of origin | ₱15,000 – ₱40,000 |

| FOB Destination, Freight Prepaid | Seller pays freight and retains risk | Buyer assumes ownership only upon delivery | ₱30,000 – ₱60,000 |

| FOB Destination, Freight Collect | Seller retains risk, Buyer pays upon delivery | Buyer assumes risk at the destination point | ₱25,000 – ₱55,000 |

Risk Management and Liability in FOB Agreements

Allocation of risk is the most heavily scrutinized aspect of any shipping agreement. When a catastrophic event, like a container falling overboard, occurs, the FOB terms dictate which party’s insurance policy must respond.

Marine Insurance Considerations

FOB splits liability during transit, so both buyers and sellers need proper cargo insurance. In international FOB shipments, buyers are at risk once the goods are on board the vessel. Therefore, the buyer must secure a marine insurance policy that provides coverage from the port of loading to the final destination, ideally with warehouse-to-warehouse protection. Sellers must cover goods before vessel loading. Without aligned insurance, either party may face major losses when damage or transit issues occur.

The Role of the Bill of Lading

The Bill of Lading (B/L) is a key document in any FOB transaction. It acts as a receipt, proof of carriage, and document of title. Buyers need it to claim goods at their destination. Its consignment terms also affect ownership transfer. Any mismatch between the B/L, invoice, and shipping terms can delay customs clearance.

Analyzing the Financial and Accounting Impact of FOB

Shipping terms exert a profound influence on corporate finance, accounting practices, and working capital management. The precise moment title transfers dictate how transactions are recorded in the general ledger, impacting everything from the cost of goods sold (COGS) to tax liabilities.

Inventory Valuation and Transit Accounting

For buyers, FOB terms determine when buyers record inventory and accounts payable. Under FOB Origin, buyers recognize inventory in transit once goods leave the supplier and include freight in the inventory cost. Under FOB Destination, buyers record inventory only upon delivery. This timing can materially change year-end inventory balances, liabilities, and financial reporting.

Revenue Recognition for Sellers

It is required for sellers to recognize revenue when control of the promised goods is transferred to the customer. It is outlined in ASC 606 (Accounting Standards Codification) by the Financial Accounting Standards Board (FASB). Under FOB Origin, sellers can recognize revenue once goods ship because control transfers at dispatch.

Under FOB Destination, the seller must defer revenue recognition until the goods are delivered. If a shipment takes 30 days to cross the ocean, the seller’s revenue is delayed by a month. Furthermore, the seller must keep the goods on their own balance sheet as inventory during transit. ERP systems help automate these entries, improve accuracy, and prevent reporting errors tied to shipping terms.

Comparing FOB with Other Major Incoterms

To fully grasp the utility of Free on Board, it is helpful to contrast it with other widely used Incoterms. Each term represents a different point on the spectrum of risk and cost allocation between the buyer and the seller.

FOB vs. CIF (Cost, Insurance, and Freight)

| Aspect | FOB | CIF (Cost, Insurance, and Freight) |

| Transport scope | Maritime transport only | Maritime transport only |

| Freight cost | The buyer usually pays freight from the port of origin onward, unless stated otherwise. | Seller pays the cost and freight to the named port of destination |

| Insurance | The buyer usually arranges marine insurance | The seller must arrange marine insurance for the buyer’s transit risk |

| Risk transfer point | Risk transfers when goods are loaded on board at the port of origin | Risk also transfers when goods are loaded on board at the port of origin |

| Seller responsibility | Lower | Higher |

| Buyer convenience | Lower, because the buyer handles more shipping arrangements | Higher, because the seller handles freight and basic insurance |

| Best for | Buyers who want more control over freight and shipping costs | Buyers who want the seller to manage freight and insurance arrangements |

FOB vs. EXW (Ex Works)

| Aspect | FOB | EXW (Ex Works) |

| Seller obligation | Seller delivers the goods on board the vessel and handles export clearance | The seller only makes the goods available at their premises |

| Buyer responsibility | The buyer takes over the risk and costs once the goods are loaded on board | Buyer handles all costs, risks, loading, transport, and export procedures |

| Loading responsibility | Seller handles loading at the port of shipment | Buyer handles loading from the seller’s premises |

| Export clearance | Seller manages export clearance | Buyer manages export clearance |

| Risk transfer point | Risk transfers when goods are loaded on board the vessel | Risk transfers once goods are made available at the seller’s premises |

| Seller responsibility | Moderate | Minimum |

| Best for | Buyers who want some control after shipment, while sellers manage export formalities | Buyers who want full control over the entire shipping and export process |

FOB vs. FCA (Free Carrier)

| Aspect | FOB | FCA (Free Carrier) |

| Transport scope | Primarily used for sea and inland waterway transport | Can be used for any mode of transport, including air, road, rail, and sea |

| Delivery point | Seller delivers goods on board the vessel at the named port of shipment | Seller delivers goods to the buyer’s nominated carrier at the seller’s premises or another named place |

| Export clearance | Seller handles export clearance | The seller also handles export clearance |

| Risk transfer point | Risk transfers when goods are loaded on board the vessel | Risk transfers when goods are handed to the nominated carrier at the named place |

| Flexibility | Less flexible because it is limited to port-based vessel loading | More flexible because it works across multiple transport methods and locations |

| Containerized shipments | Less suitable because it can create a risk gap while goods wait at the terminal | More suitable because it avoids the terminal risk gap in containerized shipping |

| Best for | Traditional bulk or non-containerized sea shipments | Modern multimodal and containerized shipments need clearer risk transfer |

Best Practices for Negotiating FOB Terms

Negotiating shipping terms is a delicate balancing act between cost control, risk appetite, and logistical capabilities. Procurement and sales teams must collaborate closely with their logistics counterparts to determine the most advantageous terms for their organization.

Strategies for Buyers

For buyers with sophisticated, high-volume supply chains, negotiating FOB Origin (or FCA for international containers) is often the optimal strategy. By taking control of the freight, large buyers can leverage their aggregate shipping volumes to negotiate lower rates with ocean carriers and freight forwarders than the seller could offer. This unbundling of product cost and freight cost provides greater transparency, preventing sellers from hiding profit margins within inflated “prepaid” freight charges.

However, buyers must ensure they have the internal infrastructure to manage this complexity. This includes dedicated logistics personnel, robust customs brokerage relationships, and advanced tracking software. Buyers must also be proactive in securing comprehensive cargo insurance, as they are assuming the risk for the longest portion of the journey.

Strategies for Sellers

Sellers must carefully evaluate their willingness to assume transit risk and their ability to manage outbound logistics. Offering FOB Destination can be a strong selling point, particularly when dealing with smaller buyers who lack logistics expertise. It provides the buyer with a seamless, “door-to-door” purchasing experience.

If a seller agrees to FOB Destination, they must accurately calculate the total landed cost, including freight, insurance, and potential tariffs, and bake these costs into the final product price to protect their margins. Sellers should also negotiate aggressively with their outbound carriers to secure favorable rates and ensure that their transit insurance policies are bulletproof, as they retain the risk of loss for the entire journey.

Industry-Specific Use Cases for FOB Terms

While the fundamental definition of Free on Board remains consistent, its practical application varies widely across different sectors. Understanding how specific industries leverage FOB terms provides valuable insight into strategic supply chain management and risk mitigation.

Strategic Implementation Steps for FOB Contracts

Transitioning to a new FOB strategy or standardizing terms across a global enterprise requires meticulous planning. Companies must ensure that their legal, logistical, and financial departments are perfectly aligned. Here are the critical steps for successful implementation:

- Step 1: Conduct a Comprehensive Risk and Capability Assessment. Before drafting contracts, evaluate your organization’s logistics infrastructure. Does your company have the volume to negotiate better freight rates than your suppliers? If so, purchasing FOB Origin might be cost-effective. If your logistics network is limited, FOB Destination is safer.

- Step 2: Explicitly Define the Named Place. Never use generic terms like “FOB China” or “FOB New York.” Precision is paramount. Contracts must specify the exact location, such as “FOB Pier 40, Port of Seattle” or “FOB Supplier Warehouse, Dock 3, Munich.” This eliminates ambiguity regarding exactly where the risk transfers.

- Step 3: Align ERP and Accounting Systems. Financial software must be configured to recognize inventory and revenue in accordance with the specific FOB terms. For FOB Origin, the ERP should trigger a title transfer and accounts payable entry the moment the carrier issues the bill of lading.

- Step 4: Synchronize Insurance Policies. Ensure there are no coverage gaps. Buyers purchasing under FOB Origin must verify that their marine or transit insurance activates the exact moment the goods are loaded, while sellers must maintain coverage right up to that precise point.

Common Pitfalls and How to Avoid Them

Despite the ubiquity of FOB in commercial contracts, costly mistakes are frequent. Avoiding these pitfalls requires rigorous contract management and continuous education of procurement and sales teams.

- Confusing Domestic and International Terms: Using the UCC definition of FOB Origin for an international ocean shipment is a recipe for disaster. Contracts must explicitly state which framework applies (e.g., “FOB Shanghai, Incoterms 2020”).

- Using FOB for Containerized Freight: As emphasized by the ICC, using FOB for containers creates a risk gap at the terminal. Organizations should transition their standard contracts to FCA for all containerized shipments.

- Assuming Title and Risk Always Transfer Together: While risk and title often transfer simultaneously under FOB, this is not a universal law. Specific contract clauses, retention of title clauses, or the method of payment (like Letters of Credit) can separate the transfer of risk from the transfer of legal ownership.

- Inadequate Insurance Coverage: Relying on the carrier’s limited liability coverage instead of purchasing dedicated cargo insurance is a massive financial risk. Carriers are typically only liable for a fraction of the cargo’s value under international maritime law (such as the Carriage of Goods by Sea Act).

The Role of Technology in Managing FOB Transactions

The sheer volume of data generated by global supply chains makes manual tracking of shipping terms, risk transfer points, and freight accounting nearly impossible. Modern enterprises rely heavily on technology to maintain visibility and control over their FOB shipments.

Supply Chain Visibility and Tracking

Real-time visibility platforms help businesses track goods through API connections with carriers, ports, and freight forwarders. Under FOB Origin, buyers need exact vessel departure data because liability starts at that point. Automated alerts for departures, arrivals, and delays also help supply chain teams adjust inventory plans and production schedules faster.

Automated Freight Accounting and ERP Integration

ERP software helps businesses manage FOB accounting more accurately by tracking inventory in transit and capitalizing freight costs. Under FOB Origin, the system can automatically record inventory and related liabilities once goods are loaded. This reduces manual errors, supports accounting compliance, and gives finance teams real-time visibility into working capital and shipment-related entries.

Utilizing AI Management to Manage Supply

AI-powered supply management helps businesses forecast demand, detect shipment risks, and respond faster to supply chain disruptions. In FOB transactions, AI can analyze carrier performance, transit times, and delay patterns to improve planning. This allows teams to reduce stock issues, optimize purchasing decisions, and maintain better control over supply movement.

Conclusion

FOB is crucial not only for logistics but also for legal and financial operations. Whether following Incoterms 2020 or the Philippine Commercial Code, businesses must clearly understand when risk and ownership transfer to avoid costly mistakes. Proper application of FOB Origin or FOB Destination ensures better control over freight costs and risk management.

By mastering FOB terms, companies can streamline their supply chains, improve inventory visibility, and align accounting practices with shipping processes. As trade complexity rises, having the best supply chain system to negotiate, execute, and track these terms effectively will be a key factor in optimizing business performance and ensuring operational success.

FAQ for Free On Board

-

What is the difference between Free on board and free alongside ship?

FOB transfers risk once the goods are loaded onto the vessel, while FAS transfers risk when the goods are placed alongside the ship. In FOB, the seller handles loading, but in FAS, the buyer does.

-

What is the difference between FOB and FOD?

FOD transfers risk when goods arrive at the dock, before loading. FOD is more specific about the delivery location compared to FOB.

-

Is FOB only for sea freight?

Yes, FOB is primarily used for sea freight and inland waterway transport. It defines when risk transfers upon loading onto the vessel, and isn’t used for air or land freight, where other terms like FCA apply.

-

Who pays the BL fee for FOB?

The buyer typically pays the Bill of Lading (BL) fee in FOB transactions. The buyer covers costs related to the BL once the goods are loaded onto the vessel, especially under FOB Origin.