NFC payments have changed the way people pay for goods and services; walk into any modern store and you will likely see customers tapping their smartphones or smartwatches against a terminal to complete a transaction in under a second.

Consumer expectations have evolved, mobile wallet adoption has surpassed 52% globally as of 2024, and that figure is projected to grow by another 15.3% through 2029. In an increasingly cashless world, your business must be able to let go of its paper money and embrace electronic money.

This article will guide you on how to integrate NFC with your POS system and how to stay alive and prosper with it.

Table of Contents

Key Takeaways

|

What Is NFC Payment?

NFC stands for Near-Field Communication, a set of communication protocols that enable two electronic devices to exchange data when brought within approximately four centimeters (roughly 1.5 inches) of each other. NFC allows a customer’s device, like a smartphone, to communicate wirelessly with a merchant’s payment terminal to authorize a financial transaction.

In other words, NFC payments transfer payment credentials from a consumer’s device to a point-of-sale terminal through a brief proximity tap that typically takes under half a second. While all NFC payments are contactless, not all contactless payments use NFC.

QR codes and BLE are alternatives that use different kinds of contactless payment. NFC’s short range, high speed, and tokenization-based security make it the leading contactless payment standard in physical retail.

How NFC Works in POS Systems: The Step-by-Step Process

The mechanics behind an NFC transaction may seem almost magical, but understanding its step-by-step process will demystify what happens during those fractions of a second between tap and approval. In sum, it involves multiple parties and several layers of technology working in concert.

The Hardware Components

An NFC payment transaction involves two primary hardware components: the NFC reader embedded in the POS terminal and the NFC-capable device held by the customer. Major manufacturers build their Modern POS with NFC antennas, which are typically certified by major card networks (Visa, Mastercard, Discover, American Express) to ensure interoperability.

On the consumer side, NFC chips are embedded in most smartphones manufactured after 2015, as well as in smartwatches and fitness trackers. In the Philippines, many consumers also use contactless debit cards issued by banks such as BDO, BPI, or Metrobank, which allow them to simply tap their card on the terminal to complete a payment.

Step 1: Device Detection and Field Activation

When a customer brings their NFC-enabled device within range of the terminal, the terminal’s NFC antenna generates a small electromagnetic field. This field powers the NFC chip in the customer’s device (or card), even if the card has no battery of its own, through a process called inductive coupling. The two devices then establish a radio-frequency link.

Step 2: Tokenization and Credential Exchange

Rather than transmitting the customer’s actual card number (Primary Account Number or PAN), modern NFC payment systems use tokenization. A unique, transaction-specific token is generated by the device’s secure element: a tamper-resistant microchip that stores payment credentials, or through a cloud-based token service. This token and a dynamic cryptogram are transmitted to the terminal. Even if this data were intercepted, it would be useless for any other transaction.

Step 3: Transmission to the Payment Processor

The POS terminal packages the token and cryptogram into a standard payment message and sends it through the merchant’s payment processor to the relevant card network. The card network then routes the detokenized request to the issuing bank for authorization.

Step 4: Authorization and Confirmation

The issuing bank validates the transaction against the customer’s account. They check for sufficient funds, fraud signals, other risk parameters, and send an approval or decline message back through the same chain. The entire round trip, from tap to confirmation displayed on the terminal, typically takes between one and three seconds. If it was approved, the customer may see a green light, hear a beep, or see a checkmark on their device screen.

Step 5: Receipt and Settlement

The merchant’s POS system records the authorized transaction, and batch settlement typically occurs at the end of the day. The funds are transferred to the merchant’s account within one to two business days, depending on the acquiring bank’s policies.

NFC vs Other Payment Methods: A Detailed Comparison

To appreciate what NFC payment brings to the table, it is useful to compare it against the primary alternatives available to merchants today.

NFC vs Magnetic Stripe (Swipe)

Magnetic stripe technology dates to the 1960s and works by storing card data on a magnetic band that is read when swiped through a reader. The fundamental weakness of magnetic stripe is that the sensitive data are transmitted in static, unencrypted form during each transaction, making it highly vulnerable to skimming attacks.

NFC payment, by contrast, transmits dynamic, tokenized credentials that change with every transaction, rendering skimmed data worthless. Most developed markets are actively phasing out magnetic stripe, with Mastercard having announced a full global phase-out by 2033.

NFC vs EMV Chip (Dip)

EMV chip technology, which became the global standard in the 2010s, addressed many of the security vulnerabilities of magnetic stripe by generating a unique cryptogram for each transaction. However, chip transactions require physical insertion of the card into the terminal and a dwell time of several seconds while authentication completes.

NFC payment offers equivalent or superior security while being significantly faster. Where a chip transaction might take 5–10 seconds, an NFC tap takes under one second. Many contactless payment cards are now dual-interface, supporting both EMV chip and NFC.

NFC vs QR Code Payments

QR code payments work by scanning a merchant’s QR code with a smartphone camera or displaying a customer’s QR code for the merchant to scan. It is popular in markets like China, India, and Southeast Asia due to its extremely low infrastructure costs, a printed QR code costs essentially nothing, but they are slower, depend on good lighting and camera quality, and can be vulnerable to QR code substitution fraud.

NFC is faster, more consistent, and integrates more seamlessly with modern POS infrastructure. The downside is that in markets with lower smartphone NFC penetration, QR codes remain an important option.

NFC vs Bluetooth/BLE Payments

Bluetooth Low Energy payments can operate at ranges of up to 10 meters, making it a good payment method for some proximity marketing, like drive-through ordering or table-side payments. However, it introduces security concerns as a malicious reader could theoretically initiate a transaction from a distance without the customer’s awareness.

NFC’s four-centimeter range is a deliberate security feature, as the customer must consciously bring their device close to the terminal, ensuring that for payment to process, the customer must truly consent to it.

Benefits of NFC Payment for Businesses

Beyond the convenience narrative, NFC payment delivers concrete, measurable benefits for merchants across multiple dimensions of business operations.

- Faster Transaction Times and Reduced Queue Length: NFC contactless transactions are completed roughly 30–40% faster than EMV chip transactions. The one-tap payment has significantly shortened queues and increased checkout throughput. For high-traffic businesses such as supermarkets, quick-service restaurants, and transit systems, that efficiency translates to higher revenue and better customer exeriences.

- Lower Cash Handling Costs: Factors like counting reconciliation, bank transportation, storing, losses from errors, and theft are estimated to cause 0.5% to 1.5% of cash revenue to be lost. Many of these operational overheads would be solved by enabling NFC payments and shifting transactions to digital methods.

- Increased Average Transaction Value: Friction of payment affects spending behavior; easier, faster payment methods reduce friction, which encourages slightly higher spending per transaction. Contactless transactions yielded higher average values compared to cash across several categories, supporting the commercial case for NFC adoption.

- Improved Hygiene and Customer Confidence: Hygiene was a priority during the covid pandemic. It has significantly accelerated contactless payment adoption, and the hygiene preferences formed during that period have largely persisted. Offering NFC payments signals to customers that your business is modern and attentive to their wellbeing, which is a tangible, if subtle, brand advantage.

- Reduced Chargebacks on Fraudulent Transactions: When merchants process NFC payments through certified terminals, liability for fraudulent chargebacks shifts from the merchant to the card issuer. This framework, originally introduced with EMV chip adoption, meaningfully reduces merchants’ financial exposure to fraud-related disputes.

- Richer Data and Integration Possibilities: NFC-enabled POS systems capture transaction data that integrates with inventory management, loyalty programs, and analytics platforms. When customers pay via linked wallets or loyalty cards, businesses can associate transactions with customer profiles, enabling personalized marketing and more accurate demand forecasting.

Security and Risk Management in NFC Payments

Security is often the first concern raised by merchants or consumers who are new to NFC payment. The good news is that NFC payment technology incorporates multiple overlapping security mechanisms that make it among the most secure payment methods available for in-person transactions.

1. Tokenization (The Core Security Layer)

As mentioned in the process description, tokenization replaces the customer’s real card number with a surrogate value that is meaningless outside the specific transaction context. Tokens are generated by network-level tokenization services operated by Visa (Visa Token Service), Mastercard (Mastercard Digital Enablement Service), and American Express. Even if a fraudster were to intercept the NFC transmission, they would receive only a single-use token that cannot be replayed or reused.

2. Dynamic Cryptograms

Each NFC transaction includes a dynamic cryptogram, essentially a mathematically complex and transaction-unique code generated using keys stored in the device’s secure element. This cryptogram is validated by the card network and issuing bank during authorization. Unlike the static data on a magnetic stripe, this cryptogram is different for every transaction, making replay attacks impossible.

3. Device Authentication

Mobile wallet NFC payments add a layer of security through device-level authentication. Before the wallet app allows a payment to proceed, the customer must authenticate using a PIN, password, fingerprint scan, or facial recognition. This means that even if a customer’s device is stolen, the thief cannot make NFC payments without passing biometric or PIN authentication.

4. Short-Range Communication as a Security Feature

The physical constraint of NFC provides an inherent defense against eavesdropping and relay attacks. A malicious actor would need to be extremely close to both the customer and the terminal simultaneously to intercept and relay a transaction, a scenario that is practically very difficult to execute without detection.

5. PCI DSS Compliance

NFC-capable POS terminals that are certified by the Payment Card Industry Security Standards Council (PCI SSC) and compliant with PCI DSS (Data Security Standard) requirements provide the merchant-side assurance that payment data is being handled appropriately. Merchants should always verify that their NFC terminals carry current PCI PTS (PIN Transaction Security) certification.

6. Remaining Risk Areas

While NFC payment is highly secure, it is not entirely without risk. Social engineering attacks targeting merchant staff, compromised POS terminals (through malicious software rather than NFC vulnerabilities), and account takeover fraud targeting customer wallets represent the primary risk vectors. These risks are best mitigated through staff training, regular terminal software updates, physical terminal security measures, and customer education about protecting their wallet credentials.

Types of NFC Payment Methods

NFC is not just a single product but a technology standard implemented across a range of payment methods and platforms. Understanding the primary NFC payment types helps merchants ensure they support the options their customers prefer.

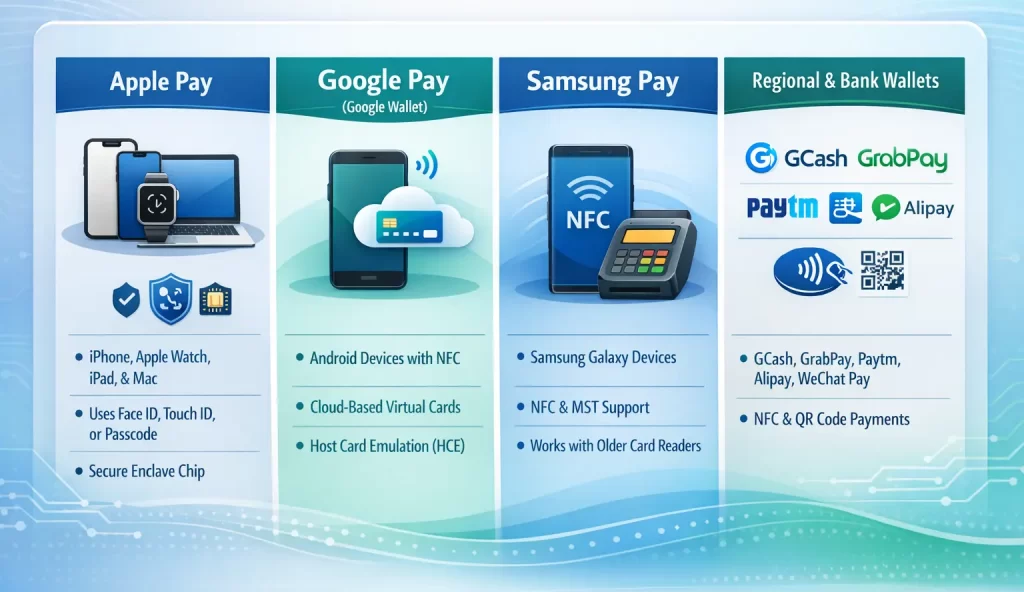

Mobile Wallets

Mobile wallets are the most prominent implementation of NFC payment for consumers. They allow users to store payment card credentials on their smartphones and pay by tapping the phone against an NFC terminal.

Contactless Payment Cards

Dual-interface payment cards (supporting both EMV chip and NFC contactless) have become the default card type issued by most banks in developed markets. These cards contain an NFC antenna embedded in the card body.

Unlike mobile wallet payments, contactless card transactions typically do not require any customer authentication for transactions below a certain threshold (which varies by country and card network, but is commonly in the range of $50–$100 USD equivalent). Above the threshold, PIN entry or other verification may be required.

Wearable Payment Devices

NFC payment is increasingly available on wearable devices beyond smartphones. Smartwatches (Apple Watch, Fitbit, Garmin Pay, Samsung Galaxy Watch) allow users to pay with a tap of the wrist, which is particularly convenient if the user is doing a physical activity or is at a place where carrying a phone is impractical. NFC-enabled rings, wristbands, and even stickers represent the frontier of wearable payment devices, often used in event and theme park environments for seamless, cashless experiences.

NFC-Enabled Loyalty and Transit Cards

Many transit systems (London’s Oyster card, Tokyo’s Suica, Hong Kong’s Octopus card) use NFC technology for fare payment, though these typically operate on proprietary systems rather than open banking networks. Some merchants issue NFC-enabled loyalty cards that also function as payment vehicles, combining identification and payment in a single tap.

Implementing NFC Payment in Your POS System

Rolling out NFC payment capability is a practical, achievable project for businesses of virtually any size. The following framework outlines the key steps and considerations.

- Assess current POS hardware to check if existing terminals support NFC, as many post-2018 models do, but may need activation or a software update. Older hardware may require new terminals or add-on NFC readers.

- Choose NFC-certified terminals and prioritize hardware with PCI PTS, EMVCo Level 1 and 2, and network-specific contactless certifications. Selection should align with your transaction volume, mobility needs, and POS software compatibility.

- Work with your payment processor to confirm your acquiring bank or processor supports contactless transactions and that your merchant account is enabled for NFC acceptance. Verify whether any incremental fees apply for contactless processing.

- Configure contactless transaction limits to set cardholder verification method (CVM) limits per card network requirements and local regulations, ensuring your terminal software enforces PIN entry for transactions above the applicable threshold.

- Train your staff so that your cashiers understand how to prompt contactless payments, handle failed transactions, identify potential terminal tampering, and troubleshoot common NFC payment issues.

- Communicate to customers through universal display of contactless symbols prominently at checkout, and update your website and social media to reflect NFC acceptance. Brief in-store messaging can help encourage adoption in less familiar markets.

- Monitor and optimize NFC transaction mix, error rates, declines, and fraud incidents through POS reporting. Use this data to refine terminal placement, staffing, and payment flow over time.

Integration with POS Software

Businesses using a full POS software platform should seamlessly integrate NFC payment data with inventory, CRM, and reporting modules. Many POS systems are designed to work with NFC-capable payment terminals as part of a broader operational management ecosystem, helping businesses consolidate payment data with sales analytics and inventory tracking in real time.

Common Challenges of NFC Payment Adoption and How to Overcome Them

While the business case for NFC is strong, the path to adoption is not without obstacles. Understanding these challenges in advance allows you to address them proactively.

| Challenges | Solutions |

| Upfront Hardware Investment — NFC terminals cost more than legacy readers, posing a barrier for smaller businesses. | Explore processor leasing programs, subsidized hardware, or payment-as-a-service models that spread costs over a contract period. |

| Connectivity & Technical Reliability — NFC payments rely on internet connectivity, making network outages disruptive. | Use redundant internet connections with a cellular backup, consider offline transaction queuing, and maintain a clear downtime procedure. |

| Consumer Unfamiliarity — In less established markets, customers may hesitate or incorrectly use NFC payment. | Invest in clear in-store signage, staff coaching, and point-of-sale messaging. Awareness campaigns can further accelerate customer adoption. |

| Inconsistent Device Compatibility — Older or budget devices may not support NFC tap-to-pay. | Offer NFC alongside chip, magnetic stripe, and manual entry fallbacks to ensure no sale is lost due to device incompatibility. |

| Legacy POS Integration Complexity — Older POS software may not integrate cleanly with NFC terminals, causing data silos or manual reconciliation. | Check if your POS provider offers NFC-integrated modules or API connections, or consider a broader POS system upgrade to fully realize NFC’s benefits. |

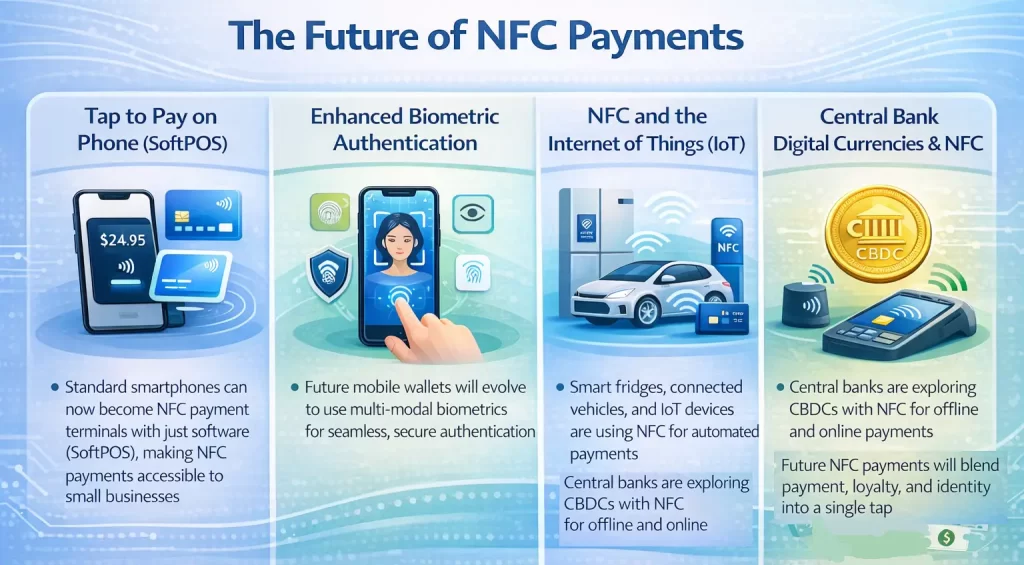

The Future of NFC Payment Technology

NFC payment is evolving rapidly, and the next five to ten years promise significant advances that will further expand its role in commerce and everyday life.

NFC payment penetration is already high in markets like the United Kingdom, Australia, Canada, and parts of Asia, and it will keep growing bigger and enter other markets, including the United States, India, Brazil, and much of Southeast Asia and Africa.

Infrastructure investment, smartphone penetration growth, and regulatory support for digital payments are driving rapid expansion in these markets, suggesting that global NFC payment volume will continue its strong compound annual growth trajectory for years to come.

NFC Payment Standards, Regulations, and Industry Bodies

For merchants and technology teams who need to navigate the technical and compliance landscape, understanding the key standards and regulatory frameworks governing NFC payments is important.

EMVCo

EMVCo is the technical body jointly owned by American Express, Discover, JCB, Mastercard, UnionPay, and Visa that manages the EMV standards family, including the contactless EMV specifications that underpin most NFC payment transactions. EMVCo’s Level 1 and Level 2 terminal certification processes ensure that NFC terminals meet minimum interoperability and security requirements before deployment.

NFC Forum

The NFC Forum is a non-profit industry association that defines and promotes NFC standards. It maintains the core NFC protocol specifications and runs a certification program for NFC devices and tags. While the NFC Forum focuses on the underlying communication technology rather than payment-specific implementations, its standards form the foundation on which payment-specific protocols are built.

PCI Security Standards Council

The PCI SSC publishes and manages the Payment Card Industry Data Security Standard (PCI DSS) and the PIN Transaction Security (PCI PTS) standard. Merchants accepting card payments, including NFC payments, must maintain PCI DSS compliance, and the terminals they use must be PCI PTS certified. PCI SSC has also published specific guidance on contactless payments and mobile payment acceptance through its PCI MPoC (Modular Payments on COTS) standard, which governs SoftPOS solutions.

Regional Regulations

Contactless payment limits, authentication requirements, and consumer protection rules vary significantly by country and region. The European Union’s Payment Services Directive 2 (PSD2) introduced Strong Customer Authentication (SCA) requirements that affect when additional verification is needed for contactless transactions. In Australia, the Reserve Bank of Australia has been active in regulating contactless payment fees and practices. Merchants operating in multiple geographies must be compliant with the specific rules in each market they serve.

Choosing the Right NFC-Enabled POS System for Your Business

Not all POS systems are created equal when it comes to NFC payment support. When evaluating options, businesses should consider the following dimensions.

- Hardware Compatibility and Certification: Confirm that the POS system supports certified NFC terminal hardware and that the terminal has current PCI PTS certification and network contactless certifications. Ask specifically about which mobile wallets are supported (Apple Pay, Google Pay, Samsung Pay) and whether the system supports contactless-only cards in addition to mobile wallets.

- Software Integration Depth: The best NFC payment implementations go beyond simple transaction processing. Look for POS systems where NFC payment data integrates with inventory management (to automatically decrement stock), customer relationship management (to link purchases to customer profiles), and business analytics (to provide real-time revenue and payment method mix reporting).

- Multi-Channel Support: If your business operates across both physical stores and e-commerce channels, evaluate whether the POS system unifies NFC in-store payment data with online payment data in a single reporting environment. Unified commerce capabilities are increasingly the standard against which enterprise-grade POS platforms are evaluated.

- Scalability: Consider your growth trajectory. A POS system that works well for a single store should also be capable of scaling to multiple locations, with centralized NFC terminal management, consistent configuration, and consolidated reporting.

Conclusion

NFC payment is a game changing technology that has made every day payment as easy as tapping a card on a POS hardware. Not only is it efficient, it is also much more safe and secure compare to alternative payment methods. It is not surprising how it became a popular method of payment that is still growing.

A business owner now have to implement NFC payment as many consumers prefer that method. To implement it they must do a number of things, from training staff to checking their POS system, and understand the challengers of NFC adoption. With this in mind, it is recommended for you to use an ERP system that can integrate NFC payment.

FAQ for NFC Payment

-

What is the NFC payment?

NFC payment is a contactless transaction method that uses near-field communication technology to transfer payment credentials from a consumer’s device or card to a POS terminal.

-

Is GCash NFC?

No, while GCash supports NFC-based payments through its integration with mobile wallets like Google Pay and Apple Pay, GCash itself is an app that does not natively have NFC.

-

What is the purpose of NFC in mobile phones?

NFC in mobile phones enables contactless payments, data sharing, and device pairing at close range. For payments specifically, it allows users to store card credentials securely and complete transactions by tapping their phone on a compatible terminal.

-

How to know if a card has NFC?

Look for a four curved lines resembling a Wi-Fi icon on its side. This indicates NFC or contactless capability. You can also check with your issuing bank or review your card’s product details online to confirm whether tap-to-pay is supported.

-

Are there spending limit?

Yes, spending limits may apply, and they vary by issuer and transaction setup. For example, BPI Debit Mastercard allows tap payments up to ₱5,000, while BDO says purchases below ₱2,000 can go through without a PIN or signature.