Efficient inventory management is vital to business success, yet it remains a common struggle for many companies. The complexity of real-time inventory tracking is prone to human error, causing significant hurdles in maintaining accurate records.

Businesses often face challenges such as stock discrepancies, inaccurate forecasting, and a lack of streamlined inventory-tracking processes. Good software can help address these issues by providing automated inventory tracking with real-time updates and data-driven insights, allowing you to stay on top and reduce costly errors.

This article will break down the importance of ending inventory, highlight the key challenges, and introduce software solutions designed to simplify inventory management.

Key Takeaways

|

What is Ending Inventory?

Ending inventory, also known as closing inventory, represents the value of goods available for sale at the end of an accounting period. It is a crucial figure for businesses to determine net income and assess financial performance.

Calculating the merchandise inventory ending is essential to determine the cost of goods sold (COGS), which directly affects gross profit. Accurate inventory tracking also enables businesses to make informed decisions about production and sales strategies.

Understanding ending inventory helps align operations with market demand. It also supports efficient stock management, improving profitability and reducing the risk of overstocking or understocking. Pairing this knowledge with leading accounting platforms used in the Philippines can further ensure that inventory data integrates seamlessly with financial reporting.

What is Inventory Value?

Inventory value refers to the total dollar value of the goods left for sale at the end of an accounting period. This figure is essential for businesses as it is often reported on financial statements, including the balance sheet.

For example, if you start the month with ₱500 worth of stock and sell ₱300, your ending inventory would be ₱200. This helps businesses understand their remaining assets and accurately calculate the cost of goods sold (COGS).

Businesses aiming to maintain accurate financial records and make informed decisions need to know the role of ending inventory. The way closing inventory is reported affects various aspects of economic performance, including asset management and profitability, which is why many organisations also invest in software built for streamlined financial reporting to ensure these figures are presented accurately.

The Role of Ending Inventory in Financial Statements

Businesses need to understand the role of ending inventory in financial statements if they want to maintain accurate financial records and make informed decisions. The way closing inventory is reported affects various aspects of economic performance, including asset management and profitability.

Let’s dive into how closing inventory affects key financial statements and provides valuable insights into a company’s operations:

- Balance sheet: Ending inventory is recorded as a current asset on the balance sheet, representing the value of unsold goods available for future sales. This helps businesses evaluate their available stock, providing insight into the company’s financial health.

- Income statement: Accurately calculating closing inventory is crucial for determining the cost of goods sold (COGS), which is subtracted from total revenue to calculate gross profit. This, in turn, affects the business’s net income, making it essential for accurate financial reporting.

- Gross margin analysis: Ending inventory plays a significant role in calculating the gross margin, which evaluates the profitability of a company’s operations. By accurately tracking merchandise inventory, businesses can assess how efficiently they are managing inventory and generating profits.

Why Do You Need the Ending Inventory Calculation?

The ending inventory calculation is essential not just at the close of the year, but throughout the entire business cycle. It plays a critical role in various aspects of financial management, from accurate reporting to decision-making.

Below are four reasons why the closing inventory calculation is crucial for businesses, especially in the Philippines.

1. Accurate inventory count

Completing a physical inventory count ensures that your recorded stock matches the actual goods on hand. This process can uncover issues such as operational errors or hidden stock, ensuring that your inventory is accurate and up-to-date.

Many businesses reduce the burden of manual counting by leveraging the operational advantages of using a dedicated tracking system that keeps records aligned automatically.

For example, if your merchandise inventory ending shows discrepancies, it may indicate problems such as theft, return fraud, or mismanagement. A precise count not only helps identify these issues but also assists in managing budgets and avoiding excess stock purchases.

2. Calculate net income

Ending inventory directly impacts net income by affecting the cost of goods sold (COGS). If your closing inventory is higher than expected, you may have more tied up in inventory than in sales, which could potentially hurt profitability.

For instance, if your ending inventory is $25,000 but your net income is only $20,000, it could signal that you’re over-investing in stock. Adjusting your stock orders and negotiating better supplier terms can help improve your net income ratio and reduce excess inventory.

3. Inform future reports

The ending inventory for one year becomes the starting inventory for the next. Accurate ending inventory values set the foundation for the following year’s financial calculations, ensuring that reports are consistent and reliable.

Understanding how to approach building comprehensive stock reports can further support this accuracy and make year-over-year comparisons more meaningful.

If the prior year’s ending inventory is miscalculated, it can lead to ongoing errors, complicating future assessments and planning. Maintaining accuracy in merchandise inventory at the end of the period ensures a smooth transition into the next accounting period and enables better future forecasting.

4. Obtain financing

Lenders often look at ending inventory as an asset when determining whether to approve business loans. Accurate inventory counts provide lenders with a clear picture of your financial health and ability to repay debt.

Using trusted financial management platforms to maintain organized records of inventory values and financial performance can further strengthen your position when seeking funding.

Proper inventory management demonstrates profitability and demand volume, which can help secure more favourable financing terms. For businesses looking to expand or navigate tight financial periods, an accurate closing inventory is crucial for ensuring the necessary funding.

How to Calculate Ending Inventory

To calculate ending inventory, start with the beginning inventory, add any new purchases, and then subtract the cost of goods sold (COGS) to determine the closing inventory. This simple formula helps determine the value of the goods remaining at the end of an accounting period, providing clarity on stock levels and financial decisions.

The formula for ending inventory is as follows:

Ending Inventory = Beginning Inventory + Net Purchases – Cost of Goods Sold (COGS)

In this formula, beginning inventory refers to the value of the stock at the start of the period, which is equal to the closing inventory of the previous period. Net purchases are the cost of items bought during the accounting period, while COGS is the expense of manufacturing or purchasing the goods sold.

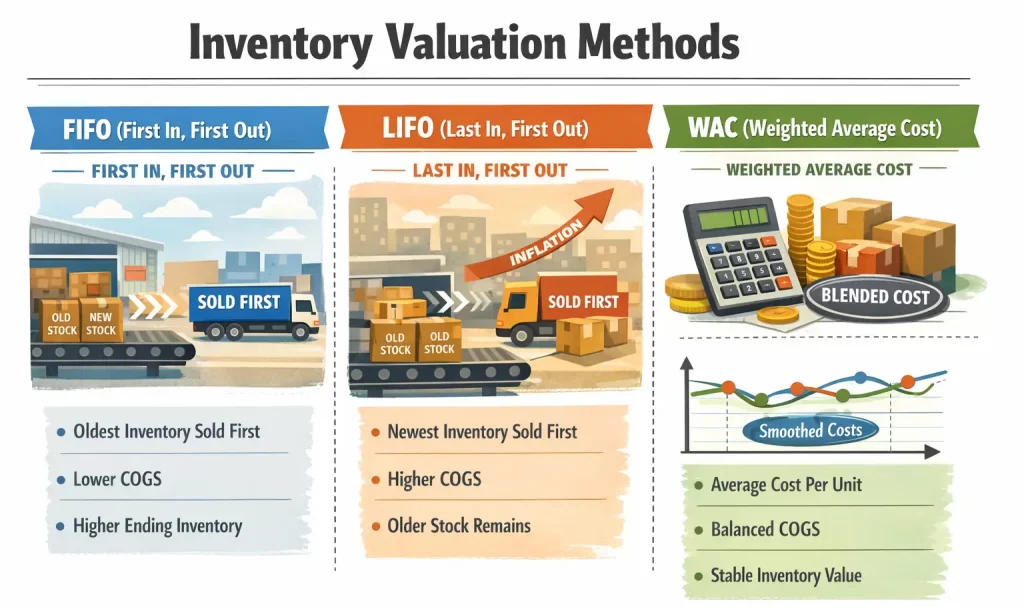

Different Inventory Valuation Methods

Selecting the appropriate inventory valuation method is crucial for ensuring accurate financial reporting and informed business decision-making. Each technique can impact your ending inventory and cost of goods sold (COGS) differently, influencing profitability and financial strategy.

- FIFO (First In, First Out): The FIFO method assumes that the first items purchased or produced are the first to be sold, leaving the most recent inventory in stock. This impacts both the ending inventory and COGS, as older, often cheaper stock is sold first, affecting profitability.

- LIFO (Last In, First Out): In contrast, the LIFO method assumes that the most recent inventory is sold first, leaving older stock on hand. This approach affects the merchandise inventory ending and COGS differently, often resulting in higher COGS during inflationary periods, which may reduce taxable income.

- Weighted Average Method/Weighted Average Cost (WAC): The WAC method calculates the average cost of inventory during the accounting period and uses it to determine the ending inventory and COGS. This method smoothens out fluctuations in cost, providing a balanced approach to valuing inventory across varying purchase prices.

Challenges in Ending Inventory Calculation

Calculating ending inventory can be more complex than it seems, as various challenges can arise during the process. From time-consuming manual inventory counts to issues such as inventory shrinkage, accurate calculations are crucial for maintaining financial integrity.

Let’s take a look at some common hurdles businesses face when calculating closing inventory and how they can affect operations:

- Time-consuming process: Performing physical inventory counts and calculating ending inventory can be a lengthy and labour-intensive process, particularly for businesses with a large inventory. This challenge can cause delays in financial reporting and may lead to inaccuracies in closing inventory if not done correctly.

- Inventory shrinkage: Inaccurate inventory tracking often results in discrepancies between the recorded stock and the actual inventory on hand, leading to inventory shrinkage. This affects the merchandise inventory balance and can result in inflated or understated inventory values, which in turn impact overall profitability. Implementing a structured approach to controlling your stock levels can help minimize these discrepancies and protect margins from unexpected shrinkage losses.

- Real-time inventory management: For e-commerce and retail businesses, maintaining real-time updates of inventory is essential for accurate closing inventory calculations. Without it, enterprises risk errors in stock levels, which can affect the closing inventory and lead to operational inefficiencies.

These challenges highlight the importance of accurate inventory tracking and real-time systems to ensure precise ending inventory calculations. Investing in reliable inventory management systems can help mitigate these issues and improve financial accuracy.

Importance of Accurate Ending Inventory

Accurate ending inventory calculation is essential for making informed business decisions and ensuring smooth operations. Maintaining precise closing inventory levels helps businesses avoid stock-related issues, enhance customer satisfaction, and improve profitability.

Here are the key reasons why an accurate merchandise inventory ending is crucial for business success:

- E-commerce and retail: For e-commerce and retail businesses, accurate tracking of ending inventory is vital to ensure that the products listed are in stock and readily available for customers to prevent missed sales opportunities and help maintain a positive customer experience by providing prompt order fulfillment. Businesses operating online can benefit from exploring tools designed specifically for online retail stock management to keep product listings and actual stock levels in sync.

- Forecasting and demand planning: The value of closing inventory plays a key role in forecasting future demand and planning purchases accordingly. By analysing the closing inventory, businesses can avoid issues like overstocking, which ties up capital, or stockouts, which could lead to missed sales.

- Inventory management software: Utilising advanced inventory management software improves the accuracy and efficiency of tracking ending inventory. This software automates the process of managing merchandise inventory ending, reducing human error, and providing real-time data to support better decision-making.

These points demonstrate the critical importance of accurate ending inventory for businesses to operate efficiently and remain competitive. In the Philippines, leveraging the right tools and methods ensures smoother operations, more accurate forecasting, and improved customer satisfaction.

Examples of Ending Inventory

Accurately calculating ending inventory is essential for businesses to track their remaining stock and assess financial performance. By understanding different scenarios and how each method affects your inventory valuation, you can make more informed decisions to optimise stock levels and profitability.

Here are some examples that illustrate how closing inventory is calculated in various situations:

- After a sale: A clothing store begins the month with 200 shirts at ₱1,120 each (₱20 x 56) and sells 150 shirts. The remaining 50 shirts in their ending inventory would be valued at ₱56,000 (50 shirts x ₱1,120), representing the stock left after sales.

- After buying more stock: A bookstore starts with 100 books at ₱560 each (₱10 x 56) and purchases an additional 100 books at ₱672 each (₱12 x 56). After selling 120 books, their ending inventory is 80 books, calculated using the FIFO method, and valued at ₱46,080 (20 books at ₱672 + 60 books at ₱560).

- After accounting for loss: A grocery store with an initial inventory of ₱560,000 (₱10,000 x 56) adds ₱280,000 worth of goods (₱5,000 x 56), but a ₱28,000 loss (₱500 x 56) due to spoilage reduces their ending inventory to ₱420,000. This highlights how losses affect the final inventory valuation at month-end.

Inventory valuation methods

- FIFO method example: 123 Holdings purchases inventory at varying prices and sells 200 units during the quarter. Using FIFO, the closing inventory is ₱89,600 (₱1,600), reflecting the sale of earlier, lower-cost items first, while leaving higher-priced items in stock.

- LIFO method example: In contrast, using the LIFO method, 123 Holdings sells the items it has purchased most recently first. The ending inventory under LIFO is ₱56,000 (₱1,000), reflecting the sale of higher-cost items and leaving older, cheaper stock in inventory.

- WAC method example: With the WAC method, 123 Holdings calculates an average unit cost of ₱735.52 (₱13.17 x 56) for all inventory. The ending inventory is valued by multiplying the remaining units by this average cost, providing a smooth approach to inventory valuation.

Other methods

- Gross profit method example: Widgets Wholesale Inc. estimates closing inventory using the gross profit method by applying an expected gross profit margin to net sales. This method provides an estimate of closing inventory without requiring a full physical count, which is especially useful after unexpected losses.

- Retail method example: All Cheaper Stuff Inc. employs the retail method to estimate its ending inventory during high-volume sales periods, calculating the amount based on a standard markup and a cost-to-retail ratio. This method helps track merchandise inventory efficiently without detailed physical counting.

Conclusion

Understanding ending inventory is crucial for maintaining accurate financial records and making informed business decisions. By calculating ending inventory correctly, businesses can assess their stock levels, gross profit, and overall financial health with greater confidence.

Beyond the formula itself, the real value lies in applying this knowledge consistently across every accounting period. Accurate ending inventory figures feed directly into financial statements, support better demand forecasting, and provide a solid foundation for year-over-year planning.

Businesses that invest in streamlined, automated tracking systems are better positioned to eliminate manual errors, reduce shrinkage, and maintain reliable records over time.

FAQ for Ending Inventory

How to make ending inventory?

To get the ending inventory you have to calculate it the value of all inventory items remaining at the end of the accounting period. The basic formula:

Ending Inventory= Beginning Inventory + Purchases during the period − Cost of Goods Sold

You can also apply inventory valuation methods like FIFO, LIFO, or Weighted Average Cost to determine the value of remaining stock.

Who is required to file an inventory list in BIR?

Businesses that sell goods and are registered with the Bureau of Internal Revenue (BIR) must file an inventory list if they have inventory as part of their operations. This includes corporations, partnerships, and sole proprietorships with significant inventory levels, as it is required for tax purposes.

Is inventory ending an asset or liability?

Ending inventory is classified as an asset on the balance sheet. It represents the value of goods that the company still owns and can sell in the future, contributing to the company’s current assets.

Should ending inventory be high or low?

Depends on the business context. Generally, higher ending inventory indicates more unsold goods, tying up capital which can be beneficial if the company expects demand to increase. Lower ending inventory might suggest efficient sales or inventory management but can lead to stockouts if demand spikes. The goal is to strike a balance that aligns with the business’s sales cycle and financial strategy.