Every business asset inevitably loses value over time. Whether you manage physical manufacturing machinery or intangible software licenses, recording this depreciation accurately keeps your financial health in check. We use Net Book Value (NBV) to track this remaining worth directly under the Property, Plant, and Equipment (PP&E) section on your balance sheet.

Ignoring net book value (NBV) can lead to inaccurate asset reporting, inefficient replacement planning, and potential compliance issues. According to the Malaysian Institute of Accountants (MIA), property, plant, and equipment (PPE) should be properly accounted for under MFRS requirements, including depreciation and carrying amount calculations, to ensure accurate financial reporting and audit readiness.

Just knowing accounting definitions will not protect your cash flow. Let us explore the core formulas, practical calculation methods, and exactly how NBV drives strategic financial decisions for your business in Malaysia.

Key Takeaways

|

Maintaining precise depreciation records and strict MFRS compliance fundamentally relies on a well-structured accounting infrastructure.

What Is Net Book Value (NBV)?

Net Book Value is the net amount at which a fixed capital investment is recorded on a company balance sheet. This figure is derived by subtracting accumulated depreciation and impairment losses from the original cost of the holding. Finance leaders relying on enterprise financial platforms use this metric to track the remaining value of tangible resources and intangible software after accounting for wear and tear over their useful life.

This value differs from market price because it relies strictly on historical cost principles and accrual accounting rules. Maintaining accurate NBV records is essential when preparing for public market entry to ensure full compliance with the Malaysian Financial Reporting Standards (MFRS) so that financial reports transparently reflect the consumption of these resources’ value rather than speculative market fluctuations.

Net Book Value Formula

To find the exact value of an asset on paper, we only need to look at two primary components. The calculation remains straightforward once we establish the initial purchase price and track the total usage over time.

THE NBV FORMULA:

Net Book Value = Original Asset Cost – Accumulated Depreciation

Components of the NBV Formula

Before running the numbers, we must understand the core elements making up this equation:

- Original Asset Cost: This represents the total amount paid to acquire the capital expenditure, which includes shipping, installation, and initial setup fees.

- Accumulated Depreciation: This metric captures the total expense recorded over the life of the holding up to the present day. We must remember that this component broadly covers depreciation for physical items, amortization for intangible resources, and depletion for natural resources.

- Salvage Value: While not explicitly written in the main formula, we absolutely cannot skip this factor. Salvage value is the estimated residual worth of the equipment at the end of its useful life. We subtract this from the original cost to find our depreciable base.

NBV Calculation Example

For a practical scenario, consider a manufacturing company in Malaysia acquiring a new factory machine for RM150,000. The management estimates the equipment has a useful life of 5 years with a projected salvage value of RM30,000 at the end of that period.

Note: The following calculation uses the standard straight-line method as the default projection.

The calculation starts by finding the depreciable base. Subtracting the salvage value from the original cost (RM150,000 minus RM30,000) leaves a total depreciable amount of RM120,000. Dividing this figure by the 5-year useful life results in a consistent annual depreciation expense of RM24,000.

| Year | Original Cost (RM) | Annual Depreciation (RM) | Accumulated Depreciation (RM) | Net Book Value (RM) |

| 0 | 150,000 | 0 | 0 | 150,000 |

| 1 | 150,000 | 24,000 | 24,000 | 126,000 |

| 2 | 150,000 | 24,000 | 48,000 | 102,000 |

| 3 | 150,000 | 24,000 | 72,000 | 78,000 |

| 4 | 150,000 | 24,000 | 96,000 | 54,000 |

| 5 | 150,000 | 24,000 | 120,000 | 30,000 |

Depreciation Methods That Affect NBV

The specific accounting method management selects directly dictates how fast the Net Book Value decreases on the balance sheet year over year. Exploring these four primary approaches ensures full MFRS compliance while accurately aligning the decline in value with actual business operations in Malaysia.

Straight-Line Depreciation

This remains the most straightforward and commonly used method across all industries. The calculation evenly spreads the depreciation expense across the entire useful life of the item.

Formula:(Original Cost – Salvage Value) / Useful Life

When to Use: Ideal for office furniture, standard IT hardware, or equipment that lose value consistently over time.

Example: An RM20,000 office setup, typically processed via standard employee expense claims, with a 4-year lifespan simply loses RM5,000 in value every single year.

Double Declining Balance

This accelerated method records higher depreciation expenses during the early years of the item’s useful life.

Formula: 2 * Straight-Line Rate * Beginning Period Book Value

When to Use: Best suited for technology hardware or commercial vehicles that lose a massive chunk of their market value immediately after purchase.

Example: An RM80,000 delivery van for a Klang Valley logistics firm will see a massive NBV drop in year one to reflect heavy initial wear.

Sum-of-the-Years’ Digits

As another accelerated approach, this method provides a slightly smoother curve compared to the double declining model. It multiplies the depreciable base by a fraction based on the remaining useful life.

Formula: (Remaining Life / Sum of the Years’ Digits) * Depreciable Base

When to Use: Perfect for specialized medical devices or industrial tech that become obsolete quickly but still retain steady late-stage utility.

Example: For a 5-year RM50,000 server, the first-year multiplier relies on a base of 15 (calculated by adding 5+4+3+2+1).

Units of Production

Unlike the other three methods, this approach completely ignores time and focuses purely on actual physical usage.

Formula: (Depreciable Base / Estimated Total Production) * Actual Units Produced

When to Use: Highly relevant for the Malaysian manufacturing sector, such as palm oil processing or semiconductor factories.

Example: An RM300,000 packaging machine depreciates based on the exact number of cartons sealed each month rather than the calendar year.

| Depreciation Method | Best Used For | Key Advantage |

| Straight-Line | Office furniture, standard hardware | Simplest calculation, highly predictable |

| Double Declining | Tech assets, commercial vehicles | Maximizes early tax deductions |

| Sum-of-the-Years’ Digits | Specialized electronics | Smoother accelerated depreciation curve |

| Units of Production | Manufacturing machinery | Ties NBV directly to actual factory output |

What Assets Can (and Cannot) Be Depreciated?

Before calculating any depreciation, we must recognize that not every single business item qualifies for this accounting treatment. Identifying which resources lose value over time prevents massive compliance errors on your balance sheet.

| Assets We Can Depreciate | Assets We Cannot Depreciate |

Tangible Assets:

Intangible Assets:

|

Land:

Financial Items:

Personal Items:

|

For strict local compliance, the Malaysian Financial Reporting Standards (MFRS) 116 specifically dictates these precise classifications. We must follow this standard to accurately separate depreciable equipment from non-depreciable holdings across all operational businesses in the country.

NBV vs. Market Value: What Is the Difference?

Net Book Value relies strictly on historical accounting records, whereas Fair Market Value reflects what external buyers are actually willing to pay in the open market today. While these two financial figures naturally diverge over time, specific market conditions certainly exist where they can closely align.

| Criteria | Net Book Value (NBV) | Fair Market Value |

| Basis of Calculation | Original cost minus accumulated depreciation | Current open market supply and demand |

| Primary Purpose | Internal financial reporting and tax compliance | Buying, selling, or securing business loans |

| Fluctuation | Decreases predictably based on a chosen formula | Highly volatile depending on economic conditions |

| Primary Usage | Balance sheet recording and internal audits | Mergers, acquisitions, and business property liquidations |

For a practical example, consider a logistics company in Johor acquiring an operational delivery truck for RM80,000. After three years of heavy usage, our accounting records might project a remaining book value of RM32,000. However, a sudden regional shortage of commercial vehicles could drive the actual market value up to RM45,000.

Recorded NBV directly dictates accurate tax deductions and standard financial reporting, whereas market value drives strategic hold or sell decisions. When acquiring replacements based on these decisions, maintaining a strategic approach to handling vendor and supplier relationships ensures you secure the best open-market price. A massive gap where the external market price drops.

Where Does NBV Appear on Financial Statements?

Net Book Value primarily sits on the balance sheet specifically under the Property, Plant, and Equipment (PP&E) section. The financial statement structures this area very clearly by listing the original purchase cost first and then subtracting the accumulated depreciation directly below it. The final calculated figure displays the NBV as the net carrying amount.

This metric also links directly to the income statement where the annual value reduction records as a depreciation expense. The cash flow statement then adds this exact depreciation back as a non-cash expense, while the accompanying financial footnotes detail the specific calculation methods applied.

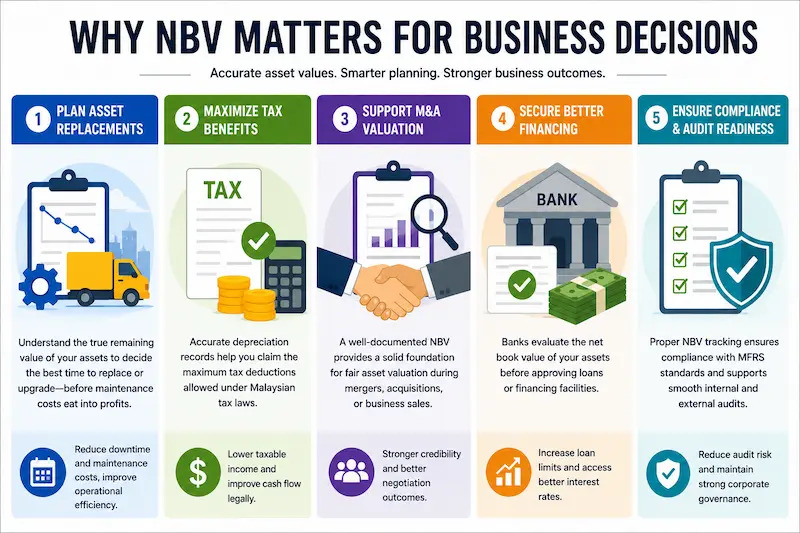

Why NBV Matters for Business Decisions

Tracking depreciation goes far beyond simple bookkeeping routines; it directly drives strategic corporate planning. Relying on accurate valuation figures prevents costly operational mistakes and opens up structural financial advantages.

Replacement Planning: A precise NBV reveals exactly when an aging equipment costs more to maintain than its actual remaining worth. For example, a logistics firm in Kuala Lumpur can use this exact metric to decide the optimal time to sell and replace a deteriorating delivery fleet, which is a crucial part of broader asset and building material sourcing, before maintenance expenses destroy profit margins.

Tax Deduction & Depreciation Claim: Malaysian tax authorities allow depreciation expenses to be claimed as an allowable expense for corporate income tax purposes. Maintaining an updated book value guarantees finance teams can maximize these capital allowances entirely without triggering local compliance audits.

M&A Valuation & Due Diligence: During regional mergers or acquisitions, prospective buyers heavily scrutinize the target company’s balance sheet. A cleanly documented NBV serves as the critical baseline to negotiate fair purchasing prices for physical assets across expanding SME ecosystems.

Loan Collateral Assessment: Local financial institutions actively review the clean carrying value of fixed assets before approving any corporate financing. Presenting a transparent, well-calculated NBV on heavy manufacturing equipment allows businesses to secure much higher loan limits and better interest rates.

Internal Audit & Compliance: Strict adherence to MFRS requires flawlessly documented historical recorded values to pass rigorous internal audits. Managing these precise calculations manually across hundreds of assets invites severe human error, especially when tracking mobile heavy machinery while overseeing various concurrent construction projects in different regions.

Common Mistakes When Calculating NBV

Manual valuation work routinely leads to critical reporting errors. Avoiding these calculation traps prevents major compliance issues.

- Incomplete Accumulated Depreciation

Failing to include software amortization directly causes a massive value overstatement on the balance sheet, which disrupts your core financial reporting balance. Categorizing assets meticulously and applying specific depreciation schedules for intangible items easily prevents this oversight.

2. Ignoring Asset Impairment

Not updating the NBV after a severe factory flood artificially inflates corporate financial health and misleads internal auditors. Conducting immediate impairment tests following any physical damage quickly adjusts the carrying value to its true state.

3. Inconsistent Depreciation Methods

Randomly switching calculation models mid-lifecycle triggers immediate red flags during tax compliance checks. Locking down one consistent MFRS-approved method per category for its entire lifespan ensures absolute reporting stability during public market evaluations.

4. Forgetting the Salvage Value

Calculating depreciation using the full original purchase price incorrectly accelerates the expense timeline and skews tax deductions. Deducting the projected residual worth to find the true depreciable base before calculating annual rates keeps the projection perfectly accurate.

5. Confusing NBV with Market Value

This remains the most common error among non-finance owners, often leading to disastrous liquidation decisions like assuming an RM15,000 operational van holds zero value. Treating NBV strictly as a historical reporting metric while validating external market prices before selling completely eliminates this blind spot.

Implementing reliable accounting software instantly solves these manual tracking risks by standardizing all calculations accurately from day one.

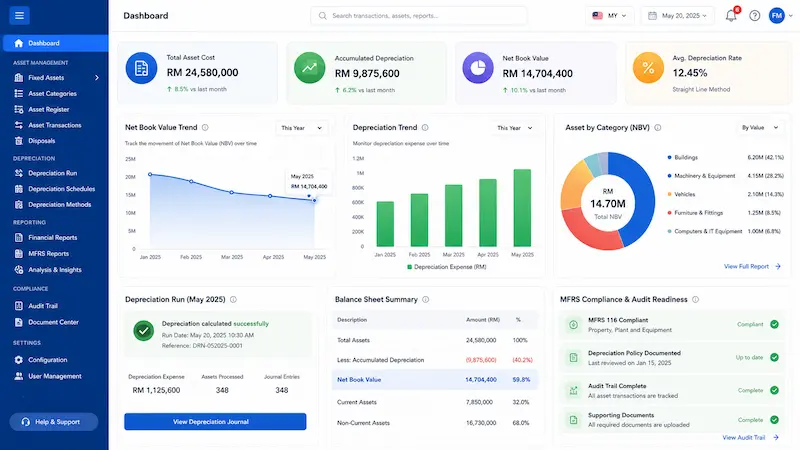

How Accounting Software Helps You Track NBV Accurately

Relying on manual spreadsheet formulas to track depreciation naturally invites critical calculation errors and missing data. These repetitive human oversights easily jeopardize tax compliance and overall reporting accuracy. Modernizing this operational workflow by transitioning to a centralized accounting platform eliminates these risks through three systematic steps:

1. Centralize Your Fixed Asset Management

The system seamlessly replaces vulnerable spreadsheets with a dedicated fixed asset management module. This initial step completely secures your balance sheet integrity and ensures every recorded value managed across your building project operational software remains perfectly updated without requiring constant manual intervention.

2. Automate All Depreciation Calculations

You no longer need to update complex formulas manually every month. This reliable system automatically calculates your Net Book Value across various depreciation methods to instantly eliminate hidden calculation risks.

3. Generate MFRS-Compliant Reporting

The platform effortlessly produces fully MFRS-compliant reporting to support your internal audits and validate your corporate tax claims. To secure your financial data accuracy today, you can explore the best accounting software for multiple businesses to streamline your entire asset valuation process immediately.

Conclusion

Net Book Value serves as a critical indicator of your company’s operational efficiency, moving your perspective beyond simple tax compliance to proactive capital planning. By viewing NBV as a strategic metric rather than just a balance sheet requirement, finance leaders can better identify when equipment and holdings cease to be productive and when capital reinvestment will yield the highest returns.

In the evolving Malaysian market, accuracy in this valuation process is the baseline for institutional credibility. Relying on precise, documented data is what differentiates a business that is merely tracking its past from one that is successfully securing its future financial capacity and audit readiness.

Standardizing this process through an automated workflow removes the risk of human error that often plagues manual calculations. Reviewing a free demo allows your finance team to see how modern accounting architecture handles MFRS-compliant reporting, ensuring that your financial records remains a reliable driver for future corporate decisions.

Frequently Asked Questions About NBV

-

What is the difference between net book value and book value?

Net book value specifically refers to the remaining carrying amount of an individual fixed item after deducting its accumulated depreciation. Meanwhile, book value typically represents the total net business value of an entire company, calculated by subtracting total liabilities from total resources. One measures a single piece of equipment, while the other evaluates the financial standing of the whole business entity.

-

Is NBV the same as the asset selling price?

No, these two figures serve entirely different purposes and rarely match exactly. The net book value is an internal accounting metric based on historical purchase costs and scheduled depreciation rates. The actual selling price depends entirely on current market demand, the item’s condition, and what a buyer is willing to pay at the time of sale.

-

How do you calculate NBV if an asset has experienced impairment?

When equipment or property suffers damage or becomes obsolete, an impairment loss must first be recognized to reduce its carrying amount to the recoverable value. This revised amount then becomes the new depreciable base, and future depreciation expenses are recalculated over its remaining useful life.

-

Does the depreciation method affect NBV?

Yes. The depreciation method directly influences how quickly recorded value decreases over time. Accelerated methods reduce the carrying amount more rapidly in the early years, while the straight-line method spreads depreciation evenly. Although the residual value may remain the same, the yearly NBV figures will differ.

-

Where is NBV recorded in the company financial statements?

Net book value is recorded under the Property, Plant, and Equipment (PPE) section of the balance sheet. It represents the original purchase cost minus accumulated depreciation and impairment losses. Depreciation expenses related to the item are also reflected in the income statement, reducing taxable profits over time.