Businesses in the Philippines are often very cautious when borrowing for expansion. From start-ups in Makati to manufacturers in Laguna, many want to search for capital to scale without giving up ownership. Still, business loans require more than access to funds. To get access to loans and use them to grow wisely, they must understand BSP rules and local tax obligations.

Great debt management involves the art of balancing. Interest costs, repayment risks, and BIR tax benefits must all be accounted for and managed well. With the right use of liabilities, business owners can improve returns without sacrificing ownership of the business. Used poorly, it can strain cash flow, damage creditor relationships, and put the business at risk under Philippine rules. This guide explains the essentials of borrowing capital for businesses operating under Philippine regulations.

Table of Contents

Key Takeaways

|

What is Debt Financing for Pinoy Businesses?

Debt financing lets Philippine businesses raise capital through loans or bonds without giving up ownership. In the Philippines, this usually means taking out a loan from a bank like BDO or BPI, or issuing corporate bonds to the public. Companies repay the principal plus interest under agreed terms, making it a structured funding option for expansion and cash flow needs. Still, debt remains a fixed liability, so lenders assess credit history, collateral, and repayment capacity before approval.

How Borrowing Money Works in the Philippines

Debt management requires a deep understanding of how loans actually work. You have to not only understand the legal terms but also understand how it affects cash flow. Additionally, lenders often determine loans by how much you ask, repayment, interest, and whether you have security or a guarantor. These factors determine how much you can borrow and how expensive that borrowing becomes over time.

1. Principal amount

The principal is the amount your business receives from the lender. For example, a trading company in Cebu may borrow ₱5,000,000 to buy delivery vehicles or warehouse equipment. The business must repay that full amount, regardless of whether the expansion immediately improves sales. Lenders usually size the principal based on your income, cash flow, and the value of any collateral you can offer.

2. Interest rates and BSP signals

The interest rate is the cost of using borrowed money. Bank pricing often moves in the same direction as BSP policy signals. However, your actual loan rate can still be much higher than the BSP benchmark. As of 10 April 2026, the BSP target RRP rate stood at 4.25%, while actual bank lending rates for all maturities averaged 9.1862% for the week of 19–25 March 2026. That gap matters when you estimate your real borrowing cost.

For example, if your business borrows ₱5,000,000 for 36 months at 10% interest, the monthly amortization is about ₱161,336. If the rate rises to 11%, the monthly payment increases to about ₱163,694. Even a one-point increase can add pressure to your monthly cash flow.

3. Loan term and maturity date

The maturity date is the point when the loan must be fully settled. Short-term working capital loans may run for only a few months, while term loans can stretch from one to five years, and project finance may follow project cash flow. A longer term usually lowers the monthly payment, but it can also increase the total interest paid over the life of the loan.

4. Repayment method

Your repayment schedule shows how the business will pay the loan back. Some facilities use fixed monthly amortization, where each payment includes both principal and interest. Others may allow interest-heavy payments early on, with a larger balance due later. In practice, some lenders still use post-dated checks for certain facilities, while others deduct payments through an Automatic Debit Arrangement (ADA). Do not assume every bank uses the same collection method.

5. Collateral and personal guarantee

Many Philippine business loans require security. This may include real estate, equipment, inventory, or other assets. Some applications also include a continuing suretyship, which can make the owner or another guarantor personally liable if the company defaults. For example, a Manila wholesaler may pledge its warehouse inventory and delivery truck as collateral, while the owner signs as surety to strengthen the loan application.

Before signing, always check what the lender can enforce if the business misses payments, what fees apply, and whether insurance, appraisal, or documentary requirements will add to the total cost of borrowing.

Types of Debt Financing Available for Local Companies

Philippine businesses have several options when it comes to borrowing. The right choice depends on how much you need and what you plan to do with the money:

| Key Feature | Term Loans from Commercial Banks | Corporate Bonds | Credit Lines for Working Capital | SME Loans and Government Programs |

| Best for / Typical use | Large purchases, branch expansion, capital expenditure | Large-scale fundraising from investors | Inventory, supplier payments, receivables, seasonal cash gaps | MSME growth, working capital, and small expansion |

| Funding structure / Loan size | Lump sum, usually medium to large | Raised from investors, usually very large | Reusable facility based on the approved limit | Program-based facility, usually smaller to mid-sized |

| Repayment style / Term | Fixed monthly installments over a set term | Interest payments until maturity, then principal repayment | Borrow and repay as needed within the credit line term | Depends on the program and lender terms |

| Approval requirements | ITR, financial statements, cash flow review, and often collateral | SEC registration and formal offering process | Credit review and working capital assessment | Program eligibility and borrower or business requirements |

| Collateral / Security | Often required | Depends on the issuance structure | May or may not be required | Often more flexible than bank loans |

| Ideal borrower / Flexibility | Established businesses, low to moderate flexibility | Large corporations, low flexibility | Businesses with recurring cash needs, high flexibility | MSMEs need more accessible funding and moderate flexibility |

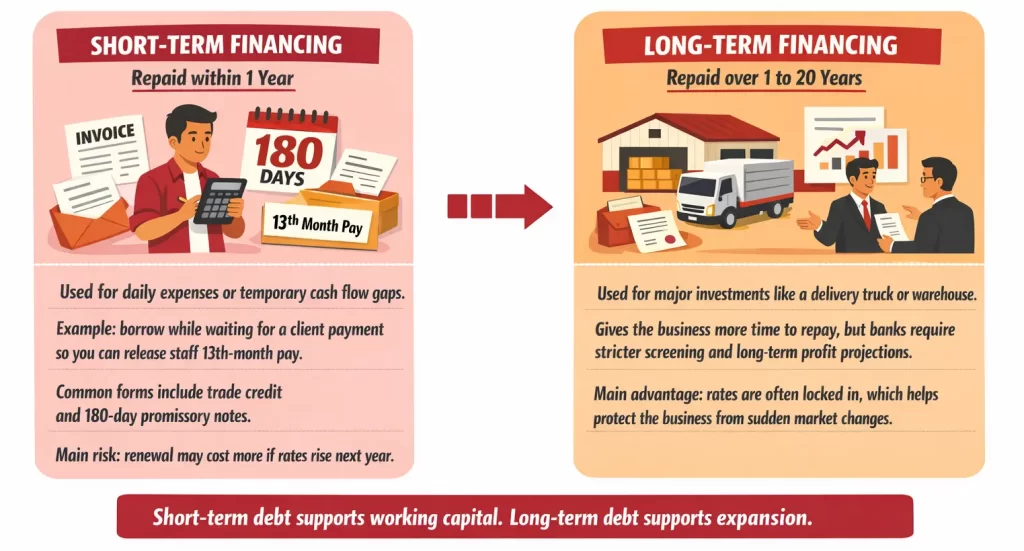

Choosing Between Short and Long-Term Debt

A common mistake for Pinoy business owners is using the wrong kind of loan for a specific need. Following the “matching principle” helps keep your finances stable. You should use short-term debt for things that bring in cash quickly and long-term debt for assets that last a long time:

The Benefits and Costs of Debt

Borrowing can help a Philippine business grow faster, but it also adds fixed obligations that not all businesses can repay. A loan can fund expansion without giving away ownership, yet it can also expose the business to collateral risk, stricter lender conditions, and repayment pressure if sales slow down.

| Benefits of Debt | Risks of Debt |

| Debt gives businesses access to capital for expansion, equipment, or working capital without immediately diluting ownership. | Debt creates fixed repayment obligations, so the business must keep paying even when sales slow down or collections are delayed. |

| You keep control of the business because the lender does not become a shareholder. | If the loan is secured, the lender may enforce collateral such as real estate, vehicles, equipment, or other pledged assets. |

| Interest expense may reduce taxable income, subject to current BIR rules and allowable deductions. | Some lenders also require a continuing suretyship or guarantee, which can expose the owner or another guarantor to personal liability. |

| For some businesses, debt can cost less than giving up equity to an investor who will share in future profits. | Loan conditions may also limit flexibility through documentation requirements, compliance obligations, or lender-imposed restrictions. |

How to Assess If Your Business Can Afford a Loan

With the pros and cons, how can businesses determine whether to borrow? They can start by checking whether it can realistically afford the repayments and whether it meets the standards banks use to assess debt capacity. Two of the most common measures are the Debt-to-Equity (D/E) Ratio and the Debt Service Coverage Ratio (DSCR).

Even profitable businesses can lose loan approval if they cannot prove repayment capacity. Banks check audited financial statements, tax returns, and CIC records. Weak bookkeeping, late payments, or poor credit can hurt the application. Lenders also assess industry risk, so businesses need clean reports, stable cash flow, and a realistic repayment plan.

Below is a sample calculation of the true cost of a business loan in the Philippines, including tax benefits:

Below is a sample calculation of the true cost of a business loan in the Philippines, including tax benefits:

| Item | Amount (PHP) | Notes |

| Loan Principal | 1,000,000 | Amount borrowed |

| Assumed Interest Rate | 10% | Sample annual rate only |

| Loan Structure | — | Assumes a 1-year, interest-only example to keep the math simple |

| Annual Interest Cost | 100,000 | 10% of ₱1,000,000 |

| Documentary Stamp Tax (DST) | 7,500 | Based on ₱1.50 for every ₱200 of issue price; full rate shown for a term of at least 1 year |

| Assumed Lender Fee | 10,000 | Sample 1% fee for illustration only; actual bank fees vary |

| Total Year-1 Financing Cost Before Tax | 117,500 | Interest + DST + assumed lender fee |

| Illustrative Tax Saving on Interest | (Up to 25,000) | Only if the borrower is taxed at 25% and can claim the full interest deduction, actual BIR treatment may differ. |

| Illustrative Net Year-1 Financing Cost | As low as 92,500 | Before principal repayment |

Once these numbers are clear, a finance manager can judge whether the project funded by the loan can generate returns above the loan’s effective cost. If it can, borrowing may support growth. If not, taking on debt may only add pressure to cash flow.

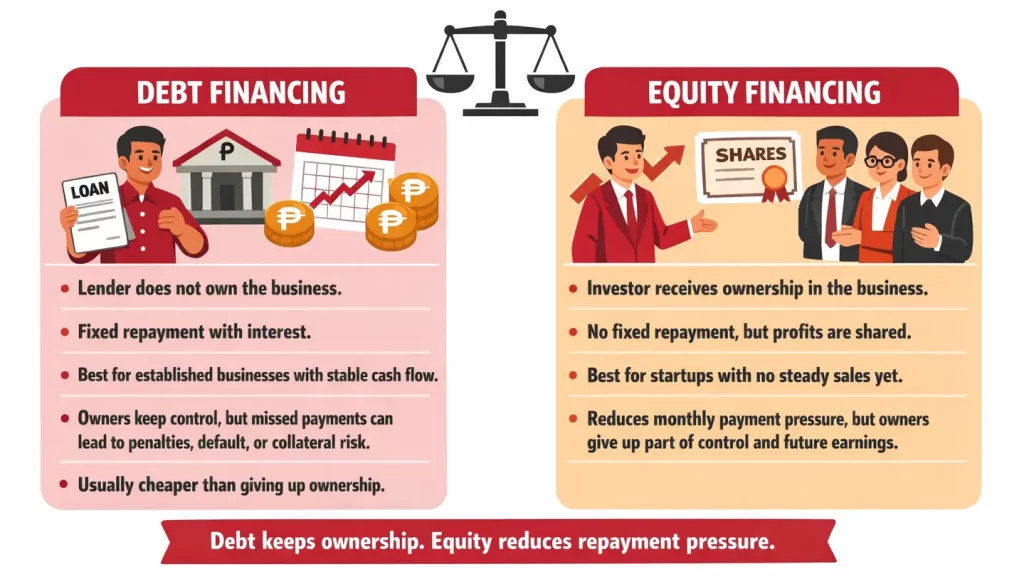

The Difference Between Debt and Equity Financing

The right funding option depends on your business stage and risk capacity. Debt works better for established companies with stable income because it keeps ownership intact and usually costs less than equity. Equity suits start-ups with no steady sales yet, since it removes fixed monthly repayments and gives the business more room to grow.

Most Philippine companies benefit from a balanced capital structure that combines debt and equity. This mix, often measured through WACC, can lower overall funding costs because interest may provide tax benefits. However, businesses still need enough equity to meet bank requirements, absorb risk, and protect operations during slower or more difficult periods.

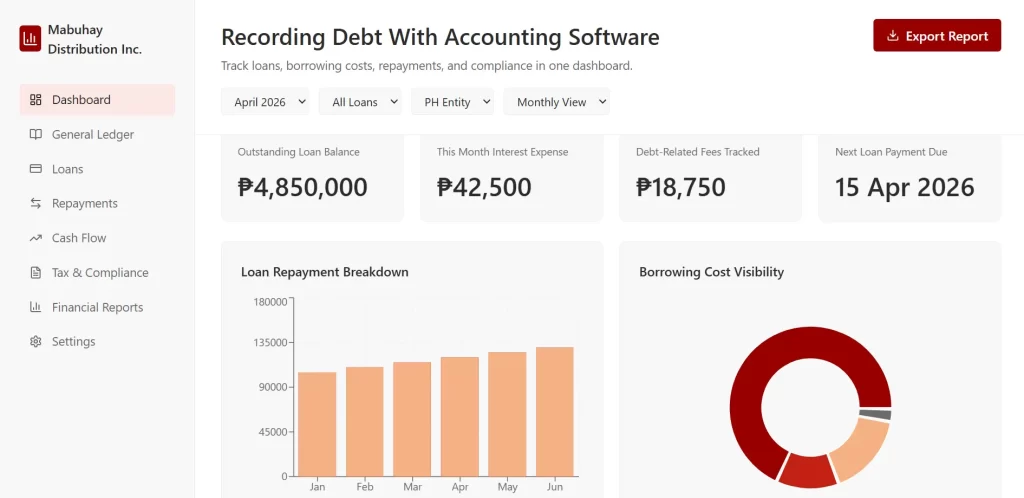

Recording Debt With Accounting Software

Accounting software helps businesses record debt correctly, stay compliant with Philippine reporting rules, and see the full cost of borrowing. In the Philippines, debt costs more than the quoted interest rate because DST, processing fees, and collateral-related charges can push the real cost above the nominal rate. Businesses that need tighter control can use an accounting software in the Philippines to track debt in one place

The benefits of accounting software include:

- Accurate loan entries: Records cash received and loan balances correctly from day one.

- Proper repayment breakdown: Splits each payment into interest expense and principal reduction automatically.

- Better cost visibility: Tracks DST, processing fees, and collateral-related charges in one place.

- Stronger compliance: Supports cleaner records for tax filing, audits, and financial reporting.

- Clearer cash flow monitoring: Shows how repayments affect liquidity and profitability over time.

Manual spreadsheets often combine principal, interest, and extra charges into one entry. This creates reporting errors and weak visibility. Accounting software fixes that by automating loan records, reducing mistakes, and giving finance teams a clearer view of liabilities, repayment schedules, and how debt affects cash flow and profitability over time.

Conclusion

Debt Financing is one of the most commonly used methods to expand business in the Philippines. It helps companies raise capital without giving up ownership, but it also creates fixed obligations that can strain cash flow. Businesses need to understand loan costs, repayment terms, and lender requirements before borrowing.

Businesses must record liabilities accurately to use them wisely, which is difficult if done with pen and paper. That is why many companies look for the best Philippine accounting software, which can improve visibility, support compliance, and reduce manual errors in debt management.

FAQ for Debt Financing

-

Is debt interest tax-deductible in the Philippines?

Yes, under the National Internal Revenue Code, interest expense is generally deductible from gross income, though it may be subject to a reduction if the company has interest income taxed at a final rate.

-

What is the typical interest rate for business loans in 2026?

In 2026, rates vary based on BSP benchmarks, but small businesses often see rates between 7% and 12% depending on credit risk and collateral.

-

Do I need collateral for all business loans in the PH?

Not all loans require collateral; while traditional bank loans usually do, venture debt and certain SEC-registered lending platforms offer unsecured options based on cash flow.

-

What are the three sources of debt financing?

The three common sources of debt financing are term loans from banks, credit lines or revolving facilities, and bonds or debt securities issued to investors.