Down payment is the biggest financial hurdle for any business that wants to expand and buy capital or land. This upfront sum is more than just a prerequisite for a purchase; it is a strategic capital allocation that ripples through the company’s balance sheet for years. A business’s liquidity and financial flexibility depend on how you handle down payments.

Down payment goes beyond wiring cash to a vendor; it also involves analyzing opportunity costs, understanding the impact on working capital, and projecting how that initial outlay influences long-term interest expenses and asset equity. Where cash flow is king, determining the optimal amount to put down versus the amount to finance is a delicate balancing act.

Key Takeaways

|

Table of Contents

Down Payment Comprehensive Definition

A down payment is a partial payment made at the time of purchasing a high-value asset or service. The remaining balance is paid over a specific period through either financing or instalment plans. It serves as a tangible commitment to the seller or lender that the transaction will be honored, so unlike a security deposit, it cannot be refunded, making it permanent.

If a buyer defaults on the subsequent loan payments, the lender has already recouped a portion of the asset’s value, reducing their potential loss. For the buyer, it lowers interest as a portion of the payment has been fulfilled before it is applied. In journal entries, this would trigger: a credit to the cash account (asset decrease) and a debit to the specific asset account (asset increase), while the remaining balance creates a liability.

A down payment differs from a retainer or advance service payment because service advances are recorded as unearned revenue until work is completed, while down payments for capital assets are added to the asset’s cost. Additionally, B2B differs significantly from B2C. In a B2B environment, down payments are often milestone-based, helping suppliers secure working capital and confirm buyer commitment.

Can You Negotiate the Down Payment Amount?

Down payment may seem fixed, but in commercial transactions, it is often negotiable. By demonstrating financial strength, such as a strong credit score, profitability, and cash reserves business can negotiate a lower down payment. Offering collateral, such as a lien on other unencumbered assets, can also open the door to negotiation. In vendor financing, especially with repeat customers or bulk orders, down payments can be reduced further in exchange for a higher price or longer terms, making it a flexible deal.

How to Balance a Down Payment

A down payment immediately reduces a company’s cash flow, limiting liquidity needed for daily operations like salaries and utility bills. Businesses must balance investing in long-term assets with maintaining enough working capital to handle unexpected costs. Paying too much upfront can strain cash reserves, while financing entirely increases debt obligations.

Psychological and operational shifts also occurs after a large down payment; Management becomes more conservative with spending to replenish the cash buffer, which can hinder minor but necessary improvements in the business. Therefore, down payments should be carefully evaluated within a broader cash flow strategy to maintain financial stability.

Why paying too much upfront can be a problem

Paying a larger down payment is not always better, as it can leave a business asset-rich but cash-poor. Tying up too much capital in non-liquid assets increases liquidity risk, especially in industries with slow receivables or unstable revenue.

The opportunity cost is high, since that cash could potentially generate higher returns through marketing, research, hiring, or inventory investments. For example, if the return on investment (ROI) for the new asset is 5%, but investing that same cash into a new marketing channel would yield a 15% return, then the company lost a huge growth potential by maximizing down payment.

A massive upfront payment also reduces financial flexibility. If the equipment breaks or clients delay payments, the company may rely on expensive emergency financing, which can outweigh any interest savings from reducing debt. Preserving a safety net is often more valuable than saving a few percentage points on a long-term loan.

How to plan so your business doesn’t run short.

Preventing a cash crunch requires rigorous forecasting before the check is signed. These are the steps on how to handle your business finance after a down payment:

- First Conduct a cash flow stress test before paying by creating a pro forma cash flow statement to see your financial position after the down payment. Test worst-case scenarios, like a 20% drop in sales or sudden cost increases, so that you can ensure the business can still operate comfortably.

- Time the purchase strategically by scheduling large down payments during peak liquidity periods, such as after strong sales or major receivable collections. Avoid slow revenue months or periods with high tax obligations to reduce pressure on working capital.

- Set up a sinking fund in advance and gradually save for the down payment by allocating a portion of monthly profits into a separate account. This prevents sudden cash strain and ensures the funds used are surplus, not essential operating capital.

- Leverage modern accounting tools for visibility to automate tracking, forecast cash flow impact, and maintain real-time insight into how major outflows affect future financial stability.

Finding the right balance between saving and spending

Balance is often determined by liquidity ratios, specifically the Current Ratio and the Quick Ratio. Ensure that these ratios remain within healthy benchmarks for their industry before committing to a down payment, as a down payment reduces current assets (cash) without immediately reducing current liabilities (unless it pays off a short-term debt), which will lower your liquidity ratios. Lenders and investors watch these ratios closely; a sharp drop could signal financial distress.

To find the balance, calculate the amount of cash you spend monthly to keep the business operational. A general rule of thumb is to maintain a cash buffer equivalent to three to six months of operating expenses after the down payment is made. If the down payment would reduce your reserves below this threshold, then consider financing a larger portion of the purchase even if it means paying more interest over time.

Additionally, consider the lifespan and depreciation of the asset. Don’t put all of your eggs in a rapidly depreciating asset. In such cases, leasing or a lower down payment with a shorter loan term might be more advantageous. The goal is to match the cash outflow with the utility and revenue generation of the asset, ensuring that the asset pays for itself over time rather than draining your resources upfront.

Why the Amount You Put Down Changes Everything

How much you put into your down payment can have a greater effect than just reducing the amount of debt you will have. These are the multiple benefits that go beyond lower interest rates:

Down payment and creditworthiness

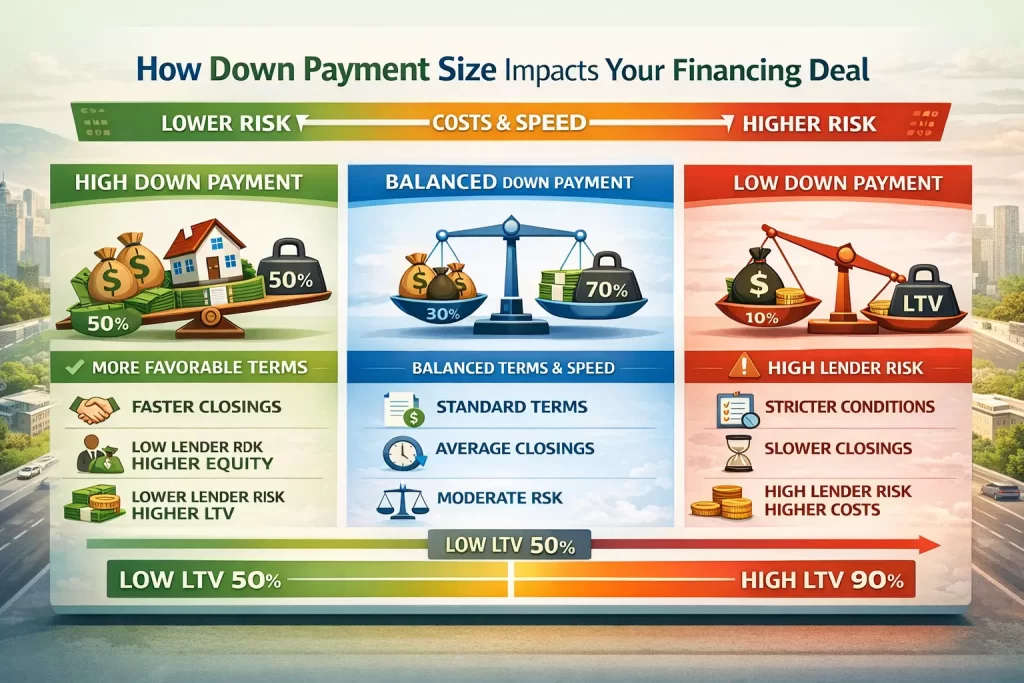

The size of your down payment is a powerful lever that adjusts the mechanics of your financing deal. It is a signal of creditworthiness and a determinant of the loan’s structural integrity. The Loan-to-Value (LTV) ratio is the primary metric lenders use here. A higher down payment results in a lower LTV, which dramatically alters the risk profile of the loan from the lender’s perspective.

The size of your down payment directly influences the loan terms and transaction speed. A smaller down payment shifts the risk to the lender, leading to higher costs and stricter conditions. Meanwhile, a larger down payment puts the risk on the buyer as more equity is at stake, but lenders offer more favorable terms. Larger down payments also enable quicker closings as the underwriting process is less rigorous, providing a competitive advantage in fast-moving markets.

Owning more assets with a down payment

A large down payment allows you to immediately own substantial equity. The bigger the equity, the bigger the net worth, which can improve your solvency ratios. This immediate ownership is particularly valuable if you plan to use the asset as collateral for future financing. For example, if you buy a warehouse with a 40% down payment, you immediately have significant equity that could potentially be leveraged later for a line of credit if the business needs cash.

Immediate equity also provides a buffer against market fluctuations. If the value of the asset drops shortly after purchase, a small down payment could leave you with negative equity. Being underwater limits your options; you cannot sell the asset without bringing extra cash to the table to pay off the loan. A healthy down payment ensures you remain in a positive equity position, giving you the flexibility to sell or trade in the asset if your business needs change.

Banks and lenders will treat you differently.

Lenders operate on risk-based pricing. When a business offers a substantial down payment, they are demonstrating financial stability and commitment. Consequently, lenders often unlock “tier 1” rates and terms for these borrowers. This difference in interest rates can be huge. On a multi-million dollar commercial loan, a difference of 0.5% or 1% in the interest rate translates to tens or hundreds of thousands of dollars in savings over the life of the loan.

A higher down payment can loosen other restrictive covenants, too. Lenders might waive requirements for personal guarantees from the business owners, or they might allow for more flexible repayment schedules, such as seasonal payments that match the business’s revenue cycle. Conversely, a low down payment might trigger a requirement for Private Mortgage Insurance (PMI) in real estate or similar insurance products in equipment financing, adding a monthly expense that provides no value to your business other than securing the loan.

Lowering monthly expense

The most tangible day-to-day benefit of a larger down payment is the reduction in monthly debt service. By lowering the principal amount borrowed, the amortized monthly payments decrease. This improves the business’s Debt Service Coverage Ratio (DSCR), a key metric that lenders look at to determine if a company generates enough income to pay its debts. A healthier DSCR makes it easier to qualify for other financing in the future.

A higher down payment lowers monthly payments, making the asset reach profitability sooner. For example, a lower monthly payment means the machine starts making a profit at a lower production level. This eases pressure on the sales team and provides a cushion during slower times, lowering fixed costs and helping the business stay more resilient.

The Tax Part Most Business Owners Don’t Think About

Taxation is a complex layer in the acquisition of business assets, and the down payment plays a nuanced role. It is crucial to understand that a down payment itself is generally not a tax-deductible business expense. You cannot simply write off the ₱3000 you put down on a truck as an expense in the year you paid it. In the eyes of the BIR and other tax authorities, you only exchanged cash for equity in a vehicle. The net value on your balance sheet hasn’t changed; the composition has.

However, the down payment is part of the “cost basis” of the asset. The cost basis is the total amount you paid for the asset, including the down payment and the amount financed (plus other acquisition costs like installation or delivery). This total cost basis is what you use to calculate depreciation. So, while the down payment isn’t directly deductible, it allows you to capitalize the asset and claim depreciation deductions over the useful life of the item. This is where the tax benefit lies—spread out over years, rather than an immediate deduction.

What you might be able to claim

The interest paid on the financed portion of the asset is usually expensed, unlike the down payment. By putting less money down and financing more, you increase your interest payments, which increases your deductible interest expense. This is a strategy some businesses use to reduce taxable income, though it involves paying more cash to the bank to save a smaller percentage in taxes, so strategize carefully.

Additionally, businesses can deduct the full cost of qualifying equipment and software purchased or financed in the same tax year under the Philippine tax code and BIR regulation. Even with a small down payment, you could potentially deduct the entire asset cost in the first year (within limits). This provides a tax advantage, where the savings might even exceed the down payment, giving a temporary boost to cash flow.

Talk to a tax professional.

Tax laws are fluid and vary significantly by jurisdiction and asset type. Real estate, software, heavy machinery, and passenger vehicles all have different depreciation schedules and deduction limits. A tax professional can model different scenarios for you: “If you put 20% down, here is your tax liability vs. if you put 40% down.” They can help you structure the purchase to maximize tax efficiency.

Down payment timing also matters. Making a purchase and placing an asset in service in the final days of the fiscal year can capture a full year’s worth of certain depreciation benefits (depending on the convention used), effectively reducing your tax bill for the year that is about to close. A CPA can advise on whether it is better to rush the down payment before year-end or delay it to the next fiscal period based on your projected profits and tax bracket.

Ways to Pull Together the Money Without Hurting Your Business

Scraping together a large lump sum for a down payment can be daunting, especially for small to medium-sized enterprises (SMEs). Taking the money directly from operating cash is the default method; smart businesses use creative financing structures to fund the down payment, ensuring that their core operational funds remain untouched for emergencies and daily needs. The goal is to acquire the asset without crippling the company’s liquidity.

In an inflationary environment, the cost of the asset may rise faster than you can save, and you lose the productivity gains the asset would have provided. Therefore, finding alternative sources for that initial capital is often a smarter growth strategy:

- Using a business credit line to pay for a down payment can be useful for short-term capital needs. Drawing from the business line of credit (LOC), you can repay it over a few months as revenue comes in. Be aware, to do this you need discipline and a clear plan to pay your debts in 6 to 12 months, as high interest rates can destroy the purchase value.

- Saving a little each month until you’re ready to pay for a down payment. Save it in higher-yield savings accounts or short-term treasury bills to hedge against inflation, and it also serves as a test if you can afford the projected loan payment amount each month before making the purchase.

- Teaming up with a partner to share the cost so that large acquisitions, like commercial buildings or machinery, can be cheaper to buy as the capital burden is shared. Becareful on who you do this with, for it requries a strong operating agreement to manage usage, maintainance, and exit strategies.

- Programs that help first-time buyers granted by governments and development agencies, like the Small Business Administrations (SBA) or local economic development councils, can help you get a loan or even subsidized financing to reduce your down payment as a first-time buyers. Specific industries may also grant you financial aids for equipment upgrades.

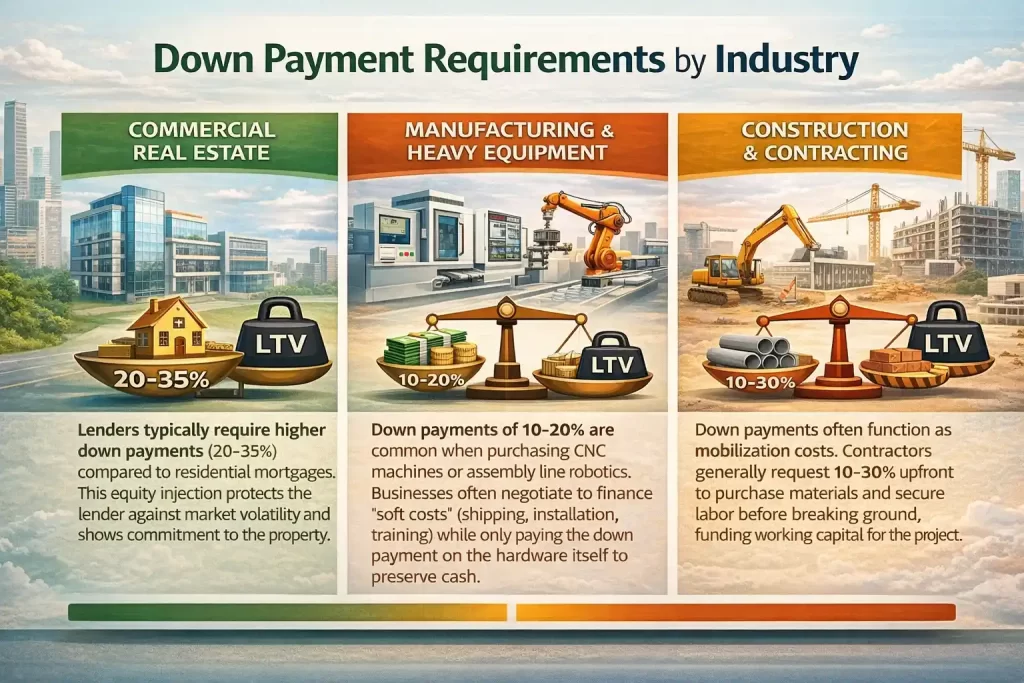

Industry-Specific Use Cases

The application and strategic importance of down payments fluctuate wildly depending on the sector. Understanding these nuances can help businesses benchmark their capital allocation strategies against industry standards.

Advanced Best Practices for Implementation

To optimize the down payment process, sophisticated organizations employ several advanced tactics:

1. Milestone-Based Payments: Instead of a lump-sum down payment, negotiate a milestone structure. This is particularly effective in custom equipment manufacturing or software development. You pay a percentage upon signing, another upon design approval, and the final portion upon delivery. This keeps the vendor motivated and protects your cash flow.

2. Letters of Credit: In international trade or large-scale procurement, businesses can sometimes use a standby letter of credit in place of a cash down payment. This assures the seller of payment without requiring an immediate cash outflow from the buyer.

3. Lease-to-Own Structures: For rapidly depreciating assets, consider a capital lease. These arrangements often require lower upfront payments, sometimes even just the first and last month’s payments, allowing businesses to upgrade technology without a massive initial capital sink.

Conclusion

A down payment goes beyond its use as part of a high-priced purchase made up front. Where, when, why, and how you use a down payment can bring other financial benefits and burdens. It can be used to get tax deductions, secure better deals from lenders, reduce debt service, and acquire many assets quickly.

But maximizing down payment can cause a significant reduction in cash flow, causing missed opportunities in other places. On the other hand, minimizing down payment can result in harsher terms by lenders, and fluctuating interest rates can disrupt expenses wildly swings.

That is why businesses need to know their industries well and consult tax professionals; there are different variables in different places and fields where a down payment could be advisable or a disaster. Apart from that, as a general rule to balance down payment well, a business must recognize its own cash flow, set up a sinking fund in advance, purchase strategically, and use modern digital tools that can make the process of accounting for down payments a piece of cake.

FAQ for Down Payment

-

Is a down payment a business expense?

No, a down payment is not immediately deductible as a business expense. It is considered a capital expenditure that contributes to the cost basis of the asset. The tax benefit is realized over time through depreciation deductions rather than as a one-time write-off.

-

What is a typical down payment percentage for commercial loans?

Commercial loan down payments typically range from 15% to 35%, depending on the asset type, the borrower’s creditworthiness, and the lender’s policies. SBA loans or government-backed programs may allow for lower down payments, sometimes as low as 10%.

-

Can I use a loan to pay a down payment?

Generally, primary lenders do not want you to borrow the down payment because it increases your total debt load and risk. However, businesses often use lines of credit or bridge financing from separate sources to cover these costs, provided their cash flow can support the cumulative debt service.

-

How does a down payment affect monthly payments?

A larger down payment reduces the principal loan amount, which directly lowers the monthly instalment payments and the total interest paid over the life of the loan. It improves cash flow in the long run but requires a larger initial cash outflow.

-

What is the difference between a deposit and a down payment?

A deposit is often a refundable sum held to secure a deal or service, which may be returned if terms aren’t met. A down payment is a non-refundable partial payment applied toward the total purchase price of an asset, representing immediate equity ownership.