Statutory reporting represents the mandatory submission of financial and non-financial information to government agencies. Every legal business must comply with these specific requirements to maintain its operating license. Failure to adhere to these standards often results in severe financial penalties, reputational damage, and operational disruptions.

With divergent requirements of different regulatory bodies, statutory reporting became a complicated affair. Companies must navigate a labyrinth of local tax laws, securities regulations, and industry-specific mandates. The burden of statutory reporting only gets worse with global expansion. Thus, a robust system is needed to ensure accuracy and timeliness for companies today.

Table of Contents

Key Takeaways

|

Introduction to Statutory Reporting

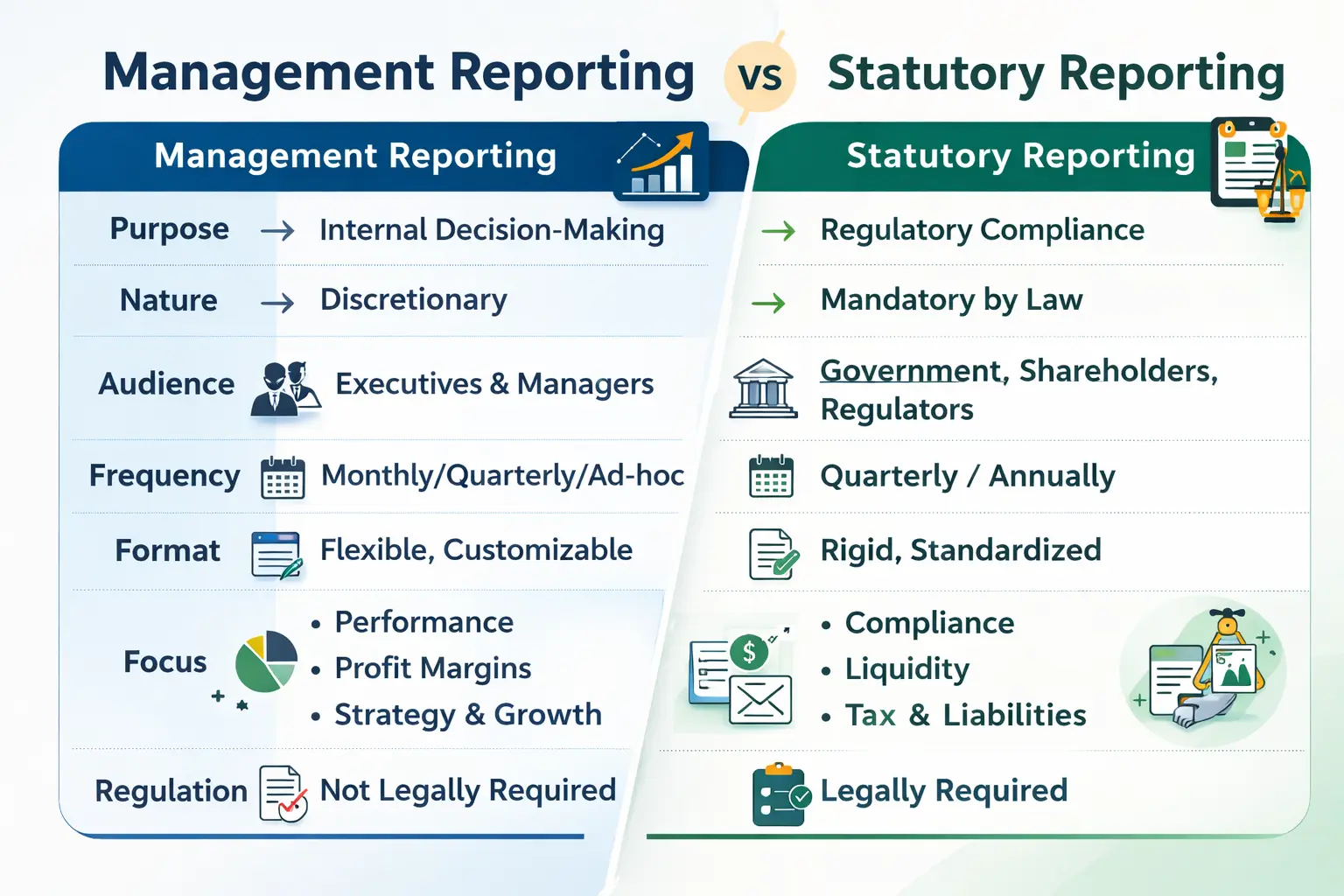

In the modern corporate landscape, transparency is not just a suggestion; it is a legal obligation. Statutory reporting serves as the primary mechanism through which governments and regulatory bodies monitor the financial health and compliance of entities operating within their borders. Statutory reports are strictly defined by laws, while internal reports is designed for strategic decision-making.

Disparate operational and financial data across tools and departments becomes a major hurdle when statutory deadlines hit. Regulators worldwide now use technology to review submissions with far greater precision, leaving little tolerance for inconsistencies. Manual spreadsheets are no longer enough; companies increasingly need integrated financial solutions that centralize data in one unified system for faster, more reliable reporting.

In-depth Definitions & Core Concepts of Statutory Reporting

Understanding statutory reporting requires a clear grasp of the frameworks that govern it. At its core, statutory reporting is the preparation of financial statements and disclosures in accordance with the specific statutes (laws) of the country where the company is registered. These reports are intended for external stakeholders, primarily the government and shareholders.

-

Statutory Reporting vs Management Reporting

It is crucial to distinguish between statutory reporting and management reporting. Management reporting is internal and discretionary. It is designed to help executives make informed decisions about the future of the company. The format, frequency, and content of management reports are determined by the company’s leadership based on what they deem relevant.

Conversely, statutory reporting is external and mandatory. The format is rigid, the frequency is set by law (usually annual or quarterly), and the content is strictly regulated. While management reporting focuses on segment performance and profit margins to drive strategy, statutory reporting focuses on compliance, liquidity, and tax liability to satisfy regulators.

-

GAAP and IFRS

Two primary accounting frameworks dominate the landscape of statutory reporting: Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). GAAP typically refers to the standard framework of guidelines for financial accounting used in any given jurisdiction, most notably US GAAP in the United States.

IFRS, issued by the London-based International Accounting Standards Board (IASB), aims to provide a global common language for business affairs. More than 140 jurisdictions, including the European Union, Australia, and Canada, require IFRS for domestically listed companies. Understanding which framework applies to a specific subsidiary is fundamental to accurate statutory reporting.

-

The “Last Mile” of Finance

In accounting circles, statutory reporting is often referred to as the “Last Mile of Finance.” This metaphor describes the final stage of the financial record-to-report (R2R) process. After the books are closed and the general ledger is finalized, the data must be converted into the specific formats required by regulators. This stage is notoriously labor-intensive and prone to bottlenecks.

-

Legal Entities and Consolidation

Statutory reporting is done at the legal entity level. A multinational corporation may consist of dozens or even hundreds of separate legal entities and each of these entities must file its own statutory accounts in its country of domicile. Furthermore, the parent company must prepare a consolidated statutory report that aggregates the results of all these entities, often requiring complex intercompany eliminations and currency adjustments.

Common Challenges & Solutions

Despite the advancements in financial technology, statutory reporting remains a pain point for many organizations. The challenges are multifaceted, stemming from both external regulatory pressures and internal operational inefficiencies. Identifying these hurdles is the first step toward overcoming them.

Challenge 1: Regulatory Volatility

The regulatory landscape is in a state of constant flux. Tax laws change with political cycles, and accounting standards evolve to address new economic realities. Keeping track of these changes across multiple jurisdictions is a monumental task. A small change in a local tax code can require significant adjustments to the reporting logic.

Solution: To navigate the seas of regulatory volatility, a company must form a formal process of monitoring the changing regulations. With the constant surveillance, a company can assess the impact and update policies before the deadlines. To do so, give clear ownership of responsibilities like monitoring and interpreting changes.

Document the specific accounting rules or tax treatment in a periodic rhythm to do so in a controlled method to keep templates consistent and assumptions the same across entities. Just remember that there are no regulation fire drills; every potential change must be treated with great care.

Challenge 2: Data Silos and Fragmentation

In many organizations, financial data is scattered across disparate systems—CRM for sales, HRIS for payroll, and legacy ERPs for inventory. Consolidating this information for statutory reporting often involves exporting data to spreadsheets, where it is manually manipulated. This process breaks the audit trail and increases the risk of copy-paste errors.

Solution: Be organized; clarify who owns each dataset and how it must be maintained. Standardize the chart of accounts, cost centers, and entity mapping rules across groups. Defined the data quality requirements and established reconciliation routines that happen throughout the month before the issue becomes bigger. When data is consolidated from the start, consolidation becomes faster and requires less manual work.

Challenge 3: The “Excel Hell”

Spreadsheets remain the dominant tool for the “last mile” of reporting. While flexible, they are fragile. Formula errors, broken links, and version control issues plague the spreadsheet-based approach. It is not uncommon for finance teams to spend more time checking formulas than analyzing the actual data.

Solution: Transitioning to dedicated financial close and reporting software is essential. These platforms replace spreadsheets with structured workflows. They offer features like version control, audit logs, and automated roll-forwards. While spreadsheets may still be used for ad-hoc analysis, they should not be the system of record for statutory filings.

Challenge 4: Currency and Language Barriers

Global companies must report in the functional currency of their subsidiaries while also consolidating in the reporting currency of the parent company. Fluctuating exchange rates add a layer of complexity to this translation. Additionally, reports must often be filed in the local language, requiring translation of account descriptions and disclosures.

Solution: Modern multi-currency accounting systems automate the translation process using real-time exchange rates. They can maintain dual ledgers: one in the local currency and one in the group currency. Furthermore, these systems often support multi-language capabilities, allowing the same data to be presented in English for headquarters and the local language for regulators.

How to Automate Statutory Reporting

Transforming the statutory reporting process from a manual struggle to an automated workflow requires a strategic approach. It is not merely a software installation; it is a re-engineering of financial processes. The following steps outline a path to modernization:

Step 1: Audit Current Processes and Risks

Begin by mapping the current reporting cycle and Identify every data source, every spreadsheet, and every manual intervention. Document the time spent on each task to find any bottlenecks. Assess the risk level of each step—where are errors most likely to occur? This is the baseline for improvements.

Step 2: Standardize the Chart of Accounts

Inconsistency is the enemy of automation; for example, if Subsidiary A records “Travel Expenses” under code 5001 and Subsidiary B uses code 6001, automated consolidation becomes impossible. Standardizing the Chart of Accounts (COA) across all entities is a prerequisite for efficient reporting as it ensures that data maps correctly to the statutory templates.

Step 3: Centralize Data Management

Move towards a “Single Source of Truth” by implementing or upgrading to a comprehensive ERP solution. The goal is to minimize the number of interfaces between systems as ideally, the general ledger, sub-ledgers, and reporting tools should reside within a unified ecosystem or be tightly integrated via APIs.

Step 4: Automate Reconciliation and Consolidation

Implement tools that automate the reconciliation of intercompany transactions. Intercompany mismatches are a leading cause of delays in the close process. Automated tools can match transactions in real-time, allowing discrepancies to be resolved during the month rather than at month-end. Similarly, automate the currency translation and consolidation logic.

Step 5: Define Governance and Workflow

Establish clear ownership for every part of the statutory report. Who is responsible for the tax provision? Who signs off on the revenue recognition? Implement workflow software that tracks the progress of these tasks. This provides visibility into the status of the close and ensures that deadlines are met.

Step 6: Continuous Monitoring and Optimization

The implementation does not end with the first successful filing. Regulatory requirements change, and the business evolves, establishing a continuous improvement loop. Regularly review the reporting process to identify new opportunities for automation. Solicit feedback from the finance team regarding pain points and address them proactively.

Industry-Specific Use Cases

While the fundamental requirement to report is universal, the specific data points and regulatory pressures vary significantly across industries. Understanding these nuances is critical for designing an effective reporting framework.

-

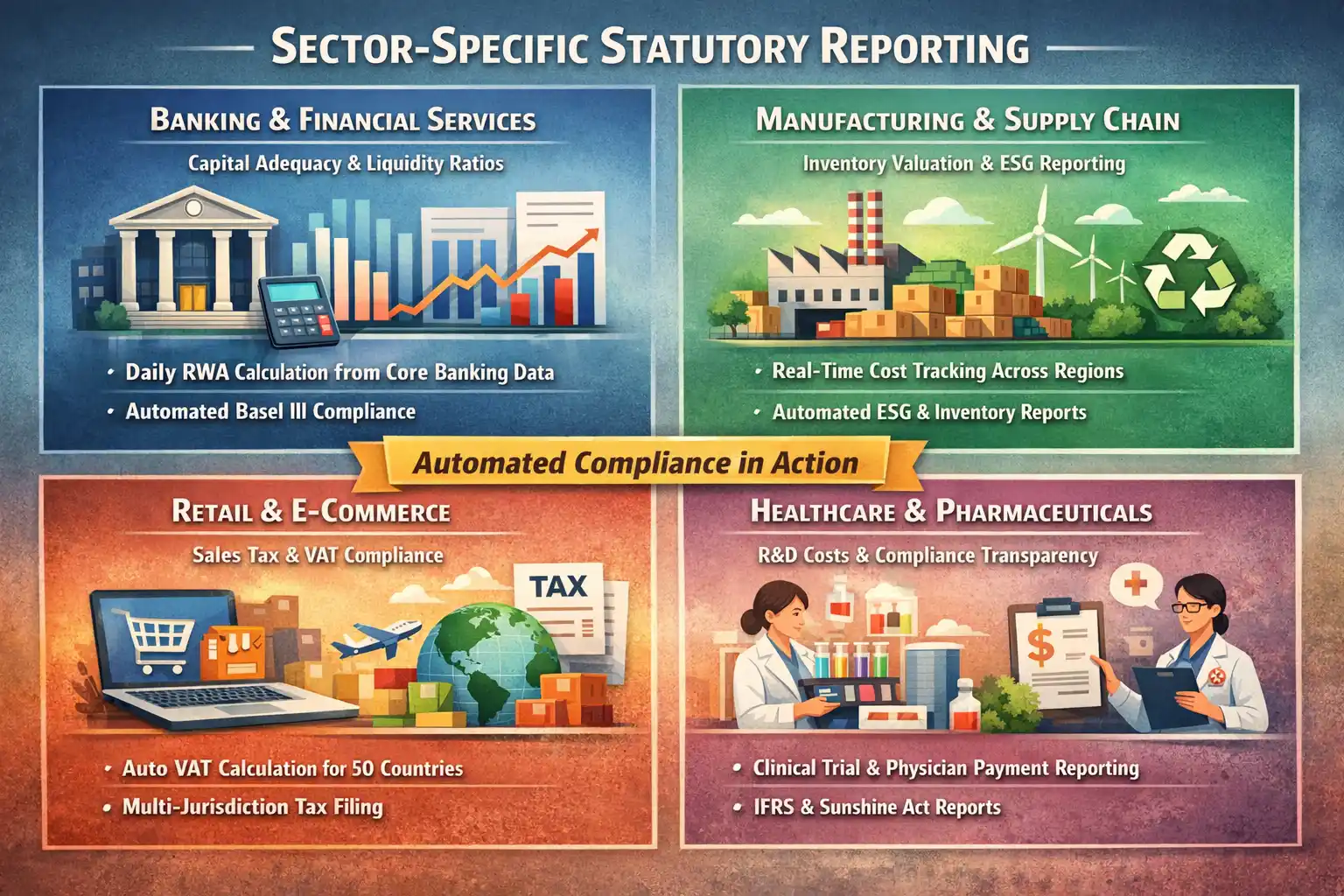

Banking and Financial Services

The financial sector faces the most stringent statutory reporting requirements. Banks must comply with frameworks like Basel III, which mandate detailed reporting on capital adequacy, liquidity ratios, and leverage. These reports require the aggregation of granular data on millions of individual loans and deposits.

Use Case: A commercial bank utilizes an automated reporting engine to calculate its Risk-Weighted Assets (RWA) daily. This system pulls data directly from the core banking platform, applies the complex Basel formulas, and generates the required regulatory templates. This automation ensures that the bank remains compliant with capital reserve requirements without manual intervention.

-

Manufacturing and Supply Chain

For manufacturers, statutory reporting is heavily tied to inventory valuation and cost of goods sold (COGS). Regulations often dictate specific methods for valuing inventory (e.g., FIFO or Weighted Average) and capitalizing overhead costs. Additionally, manufacturers face increasing requirements for environmental reporting.

Use Case: An automotive parts manufacturer operates across three continents. They use a unified ERP to track inventory costs in real-time and the system automatically adjusts inventory values based on local accounting standards for each subsidiary. Simultaneously, it tracks energy consumption and waste metrics, populating the statutory ESG reports required by European regulators.

-

Retail and E-Commerce

Retailers deal with high transaction volumes and complex sales tax/VAT regimes. The rise of e-commerce means that a retailer may trigger tax obligations in jurisdictions where they have no physical presence (economic nexus). Statutory reporting in this sector focuses heavily on accurate revenue recognition and tax remittance.

Use Case: An online fashion retailer sells to customers in 50 countries. Their financial system integrates directly with their e-commerce platform. For every sale, the system automatically calculates the correct VAT or sales tax based on the customer’s location and the product type. At month-end, the system generates the specific tax return formats for each of the 50 jurisdictions.

-

Healthcare and Pharmaceuticals

In addition to standard financial reporting, healthcare companies must report on compliance with strict industry regulations (e.g., HIPAA in the US). Pharmaceutical companies face statutory requirements regarding R&D capitalization and the transparency of payments made to healthcare professionals (Sunshine Acts).

Use Case: A pharmaceutical company uses a specialized reporting module to track all clinical trial expenses. The system segregates costs that can be capitalized as assets from those that must be expensed immediately, according to IFRS standards. It also aggregates all marketing spend on physicians, automatically generating the transparency reports required by government health agencies.

The Three Modes of Statutory Reporting

When approaching statutory reporting, organizations generally choose between three models: In-house Manual, Outsourced, and In-house Automated. Each has distinct profiles regarding cost, control, and risk.

1. In-house Manual (Spreadsheets)

This is the traditional approach where internal finance teams use spreadsheets to compile reports.

| Pros | Cons |

| Low initial software cost | Extremely high risk of error |

| high flexibility to make quick changes | Dependency on key individuals |

| Easy to learn | Time-consuming & difficult to audit |

2. Outourced (Accounting Firms)

Companies hire external accounting firms to prepare their statutory filings.

| Pros | Cons |

| Access to specialized expertise | High recurring costs |

| Reduced burden on internal staff | Loss of control over data |

| Lower risk of non-compliance due to expert oversight | Slower turnaround times |

| Useful external benchmark | Potential disconnect between the firm and the company’s operational reality |

Verdict: Good for entering new markets where local knowledge is lacking, but can become prohibitively expensive for global operations.

3. In-house Automated (Modern ERP/Reporting Software)

The company uses specialized software to automate the reporting process internally.

| Pros | Cons |

| High accuracy | Higher upfront implementation cost |

| Full control and visibility | Requires training and change management |

| Scalability | Temporary production dip during transition |

| Long-term cost efficiency | Dependence on system uptime |

| Real-time data access | Over-standardization |

Verdict: The gold standard for mid-sized to large enterprises. It offers the best balance of control, cost, and compliance.

How ERP System Solves Statutory Reporting

To truly excel in statutory reporting, organizations must move beyond basic compliance and adopt advanced practices that leverage the full power of an ERP system. These practices not only ensure compliance today but prepare the organization for the regulatory landscape of tomorrow.

-

Continuous Compliance Monitoring

Traditional reporting is periodic (monthly, quarterly, annually), so mistakes are only detected in the final monthly reports. A truly advanced organization would practice “Continuous Compliance,” in which the ERP system monitors transactions in real time against regulatory rules.

For example, the system can block a purchase order instantly if the vendor lacks a valid tax ID, rather than flagging the error weeks later during the month-end close. This shift from detective controls (finding errors later) to preventive controls (stopping errors now) drastically reduces compliance risk.

-

Predictive Analytics for Tax Planning

With an ERP system, finance teams can use predictive analytics to forecast future statutory liabilities. By modeling different business scenarios, such as entering a new market or changing a supply chain route, companies can estimate the tax impact before making strategic decisions. This transforms statutory reporting from a reactive obligation into a proactive strategic tool.

-

Automated Reconciliation of Intercompany Transactions

For global entities, intercompany transactions are a major source of statutory reporting errors. One subsidiary records a receivable while the other fails to record the payable, leading to consolidation discrepancies. ERP system automatically match and reconcile intercompany trades at the transaction level.

-

Automatic Regulatory Updates

Regulations change constantly and to handle all those little details manually takes too much time and resource. But with an ERP-backed reporting process any company can stay up to date with the current regulations including tax rates, revised statutory reporting formats, electronic filing standards, audit trail documentation rules, and industry-specific compliance parameters. The result is more consistent compliance, fewer manual interventions, and faster preparation when deadlines approach.

The Future of Statutory Reporting (2026 Onwards)

The field of statutory reporting is undergoing a radical transformation driven by digitalization and shifting societal expectations. Looking ahead to 2026 and beyond, several trends will redefine how companies report to regulators.

Continuous Transaction Controls (CTC)

The era of “post-audit” is ending. Governments are moving toward “pre-audit” or Continuous Transaction Controls. Instead of submitting a report at the end of the month, companies will be required to transmit transaction data (such as invoices) to the tax authority in real-time for approval.

Countries like Brazil, Mexico, and Belgium have already pioneered this. It is likely that by 2030, this will be the standard across Europe and parts of Asia, requiring ERPs to be permanently connected to government servers.

ESG Integration into Statutory Frameworks

Environmental, Social, and Governance (ESG) reporting is moving from voluntary to mandatory. The European Union’s Corporate Sustainability Reporting Directive (CSRD) is a harbinger of global standards. Future statutory reports will integrate financial data with non-financial metrics.

CFOs will be as responsible for reporting carbon emissions as they are for reporting cash flow. This convergence will require systems that can capture operational data (energy usage, diversity stats) alongside financial transactions.

AI and Predictive Compliance

Artificial Intelligence will play a pivotal role in auditing statutory reports before they are filed. AI algorithms will scan draft reports to identify anomalies, variances, or potential non-compliance risks based on historical data and changing regulations.

This “predictive compliance” will allow companies to fix issues before the regulator ever sees them, significantly reducing the risk of audits and penalties.

Standard Business Reporting (SBR) and XBRL

The standardization of data formats will accelerate. eXtensible Business Reporting Language (XBRL) tags financial data so it can be machine-read. Regulators are increasingly mandating XBRL for all filings.

This shift allows regulators to instantly compare company performance across industries. For companies, this means that reporting software must be natively capable of generating XBRL-tagged documents without manual tagging.

E-commerce: Digital Services Taxes and High-Volume Reconciliation

E-commerce platforms deal with high transaction volumes that can overwhelm traditional reporting processes. Statutory reporting in this sector often involves Digital Services Taxes (DST) which are levied on revenue generated from digital services rather than income.

Because these laws vary rapidly by country, manual tracking is almost impossible and it is made worse with the increasing demand for E-commerce statutory reporting. Only with an ERP system can you track the millions of micro-transactions and reconciling them against payment gateway settlements in real-time.

Furthermore, e-commerce businesses must comply with strict data privacy laws like GDPR or CCPA. The ERP system assists in statutory reporting regarding data breaches or consumer data requests by maintaining a centralized, secure database of customer interactions.

Conclusion

Statutory reporting is the bedrock of corporate legitimacy. It is the price of admission for doing business in the global economy. While the obligations are heavy, the evolution of technology has provided the tools to manage this burden effectively. Moving away from disjointed, manual processes toward integrated, automated systems is not a luxury but a way to survive and grow.

The transition to automated statutory reporting offers benefits that ripple through the entire organization. It enhances data integrity, improves strategic decision-making, and builds trust with investors and regulators. By embracing these modern methodologies, finance leaders can transform their departments from back-office compliance centers into strategic partners that drive business value.

As we look toward a future of real-time reporting and integrated ESG mandates, the agility of a company’s reporting infrastructure will become a key competitive differentiator. Organizations that invest in robust financial systems today will be best positioned to navigate the regulatory complexities of tomorrow.

Frequently Asked Questions

-

What is the main difference between statutory and management reporting?

Statutory reporting is mandatory, intended for external stakeholders like the government, and follows strict legal standards (GAAP/IFRS). Management reporting is discretionary, intended for internal decision-making, and focuses on operational performance metrics chosen by company leadership.

-

Why is statutory reporting important for businesses?

It ensures legal compliance, allowing the business to operate without penalties or license revocation. Furthermore, accurate statutory reporting builds trust with investors, banks, and stakeholders, which is essential for securing capital and maintaining corporate reputation.

-

What happens if a company fails to comply with statutory reporting?

Non-compliance can result in severe financial penalties, legal action against directors, and increased scrutiny or audits from regulators. In extreme cases, it can lead to the suspension of trading on stock exchanges or the revocation of business operating licenses.

-

How does software improve the statutory reporting process?

Software automates data collection, consolidation, and formatting, significantly reducing human error and manual workload. It ensures a ‘single source of truth’ for financial data and allows for real-time updates to comply with changing regulations.

-

What are the emerging trends in statutory reporting for 2025?

Key trends include the shift toward Continuous Transaction Controls (real-time reporting to governments), the mandatory integration of ESG (Environmental, Social, and Governance) data into statutory filings, and the use of AI for predictive compliance and auditing.