The Tax Reform for Acceleration and Inclusion (TRAIN) Act, or Republic Act No. 10963, is a major milestone in the evolution of the Philippine tax system. Enacted in 2017, the TRAIN law was designed to streamline taxation and improve fairness.

For business owners and decision-makers, the TRAIN Law goes beyond regulatory compliance. It directly influences payroll structures, pricing strategies, cash flow management, and overall financial planning.

Understanding the TRAIN Law in the context of 2026 is essential for maintaining operational efficiency and financial resilience. By clearly grasping its key provisions and business implications, companies can better align their strategies with current tax regulations.

Table of Contents

Key Takeaways

|

Quick Summary of Key TRAIN Law Changes

Before going into the objectives behind the TRAIN Law, it helps to scan the major changes first. This quick comparison highlights the provisions that most directly affect payroll, pricing, tax compliance, and financial planning.

| Component | Before TRAIN Law | After TRAIN Law |

|---|---|---|

| Personal income tax | Old graduated tax rates applied, with personal and additional exemptions. | The first ₱250,000 became tax-free, and the new graduated rates were simplified. |

| VAT threshold | Businesses generally became liable to VAT once annual gross sales or receipts exceeded ₱1,919,500. | The VAT threshold increased to ₱3,000,000, giving many SMEs more room to stay non-VAT. |

| Estate tax | Estate tax followed a graduated rate structure ranging from 5% to 20%. | Estate tax shifted to a flat 6% rate on the net estate. |

| Donor’s tax | Donor’s tax used a graduated rate structure ranging from 2% to 15%. | Donor’s tax shifted to a flat 6% on net gifts above ₱250,000 per year. |

| Excise tax on fuel (BBM) | Diesel had a zero excise tax rate, while fuel taxation was generally lower. | TRAIN imposed phased increases, including diesel at ₱2.50, ₱4.50, and ₱6.00 per liter, and gasoline at ₱7, ₱9, and ₱10 per liter. |

| Excise tax on sweetened beverages | No dedicated excise tax applied to sweetened beverages. | TRAIN introduced a specific excise tax, generally ₱6 or ₱12 per liter depending on the sweetener used. |

| Tax option for self-employed individuals | No 8% income tax option was available in lieu of graduated rates and percentage tax. | Qualified self-employed individuals and professionals below the VAT threshold may opt for an 8% tax on gross sales or receipts in excess of ₱250,000. |

The Core Objectives Behind the TRAIN Law (RA 10963)

The implementation of the TRAIN Law was driven by a clear set of national objectives aimed at fostering economic growth and improving public services. It was not merely a revision of tax rates but a foundational part of the government’s broader socioeconomic agenda.

The reform was designed to generate revenue to fund the nation’s ambitious infrastructure projects under the “Build, Build, Build” program and to increase the budget for essential services like education and healthcare.

By restructuring the tax system, the government also aimed to unburden the majority of taxpayers, particularly low-income earners, thereby increasing their disposable income and stimulating domestic consumption.

For businesses, these objectives signal a long-term shift in the country’s economic priorities and regulatory environment. Understanding the reason behind the law is the first step in navigating its complexities and aligning your business strategy accordingly.

The following sections will delve deeper into the specific goals that shaped this landmark legislation and what they mean for the future of commerce in the Philippines, helping you understand the strategic context of these significant fiscal changes.

A. To create a simpler and fairer tax system

The TRAIN Law simplifies the tax system, reducing personal income tax rates and eliminating complex loopholes. For businesses, this means clearer tax brackets and a more predictable fiscal environment, making compliance easier. By shifting focus to consumption taxes, it also encourages formal economic participation and investment.

B. To generate revenue for public infrastructure and services

The TRAIN Law generates funds for critical infrastructure projects, such as roads and public transportation. These projects reduce business costs by improving connectivity and reducing traffic. The reform’s excise taxes on fuel and goods like sweetened beverages contribute to revenue that supports business efficiency across the Philippines.

Key Features of the TRAIN Law Affecting Businesses

The TRAIN Law introduced major changes that reshaped how businesses operate in the Philippines. Beyond personal income tax cuts, updates to VAT, new excise taxes, and simplified estate and donor taxes have had a direct impact on corporate finances.

Understanding these changes is essential for effective business management. Failure to adjust to new VAT thresholds or excise taxes can lead to compliance risks, reduced margins, and inaccurate pricing.

According to the official text of the law, these provisions were designed to work together to support the government’s fiscal objectives. The following overview highlights the most important changes and their immediate implications for businesses.

A. Overhaul of the Personal Income Tax (PIT) System

One of the key features of the TRAIN Law is the restructuring of personal income tax brackets, which directly affects employees’ take-home pay. Individuals earning up to ₱250,000 annually are now exempt from income tax, providing broad relief to workers.

For higher income levels, the law introduced simpler and generally lower tax rates. This requires HR and payroll teams to update withholding calculations and adjust compensation and benefits strategies accordingly.

Freelancers and self-employed individuals earning below the ₱3 million VAT threshold may also choose an 8% tax on gross income instead of the graduated income tax rates and percentage tax.

B. Updates to the Value-Added Tax (VAT) System

The TRAIN Law introduced major updates to the VAT system, including raising the VAT exemption threshold from ₱1,919,500 to ₱3,000,000 in annual gross sales or receipts. This change benefited many SMEs by reducing the need to register for and manage VAT compliance.

At the same time, the law removed VAT exemptions from several sectors and goods. As a result, businesses must reassess their VAT status, evaluate potential new tax costs in their supply chains, and ensure their accounting systems support accurate compliance.

C. Introduction of New and Increased Excise Taxes

A major revenue-generating component of the TRAIN Law was the imposition of new and increased excise taxes on specific goods, which has had a ripple effect across various industries.

The TRAIN Law introduced excise taxes on sugar-sweetened beverages, affecting food and beverage manufacturers, goods suppliers, and retailers. It also raised excise taxes on petroleum products, increasing costs for logistics, transportation, and manufacturing.

D. Simplification of Estate Tax and Donor’s Tax

To simplify and encourage compliance in wealth transfer, the TRAIN Law streamlined both estate tax and donor’s tax. It replaced the complex, tiered tax structures with a single, flat rate of 6% for both.

For estate tax, this rate is applied to the net estate value exceeding ₱5 million, with increased standard deductions. For donor’s tax, the 6% rate applies to net donations exceeding ₱250,000 annually.

This simplification makes estate planning and wealth transfer more straightforward for business owners and high-net-worth individuals, reducing the administrative burden and potentially encouraging the legal declaration of assets.

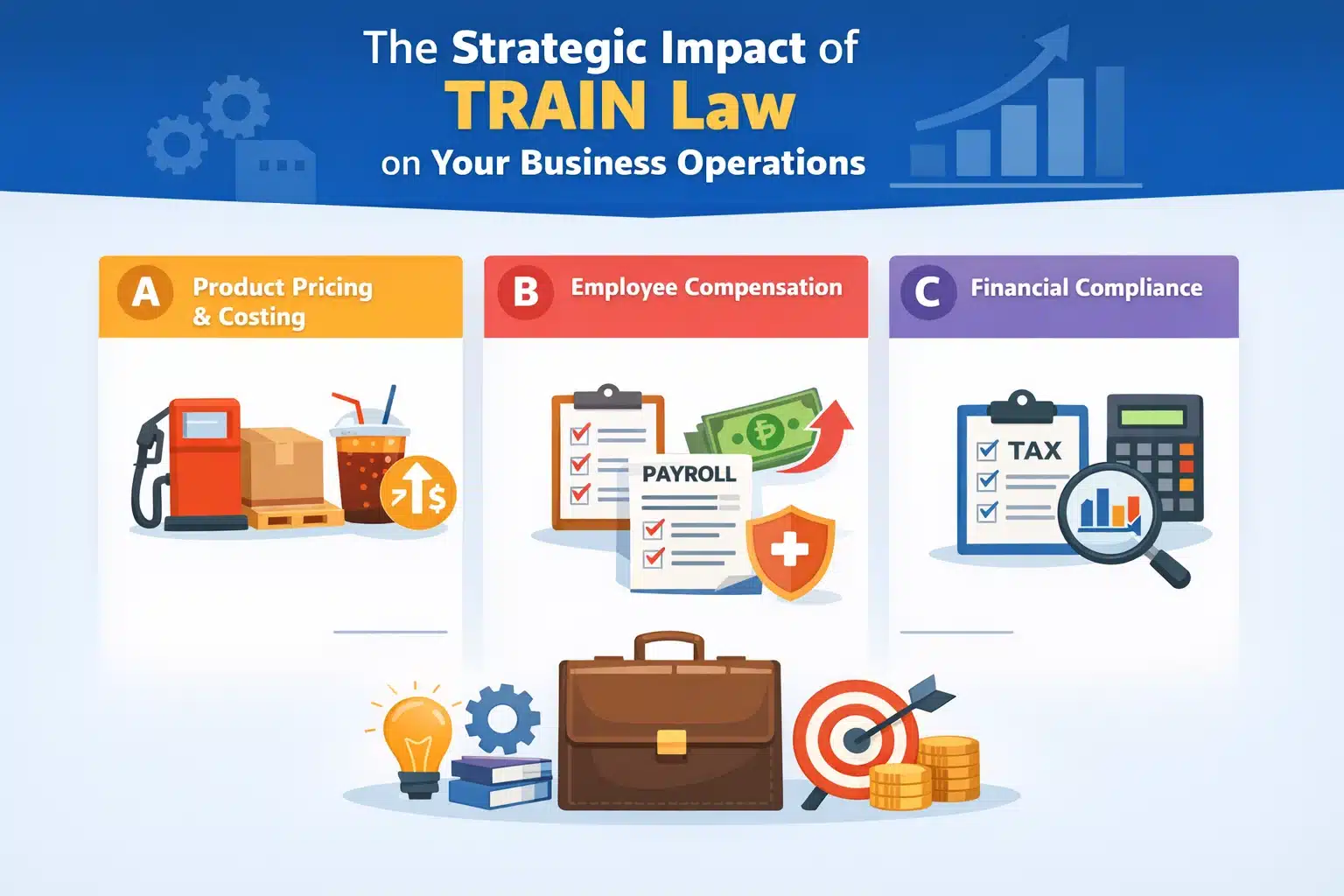

The Strategic Impact of TRAIN Law on Your Business Operations

The TRAIN Law goes beyond compliance and directly influences pricing, budgeting, HR, and investment decisions. Adapting to these changes requires a holistic review of business processes to reduce risks and capture new opportunities.

From adjusting prices due to excise taxes to restructuring compensation after income tax reforms, businesses must take a forward-looking approach. The higher VAT threshold also gives SMEs a chance to streamline operations and improve cash flow.

A. Who Is Most Impacted by the TRAIN Law Changes?

The TRAIN Law has distinct impacts across different sectors:

- F&B Industry (Excise on Sweetened Beverages): Companies in the food and beverage sector, especially those dealing with sweetened beverages, face increased costs due to excise taxes. They must decide whether to absorb these costs or pass them on to consumers, which could affect pricing and demand.

- Logistics and Manufacturing (Fuel Excise): Logistics and manufacturing sectors are directly impacted by higher fuel excise taxes, which increase transportation and production costs. This could disrupt supply chain pricing and force businesses to reassess operational costs.

- Retail and SMEs (VAT Threshold Changes): SMEs and retailers with annual revenues of less than ₱3 million can benefit from the higher VAT threshold, allowing for improved cash flow and simplified operations. However, those exceeding the threshold need to adapt to the new financial compliance standards.

B. Impact on product pricing and overall costing

The new excise taxes on fuel, sweetened beverages, and other goods have a direct impact on the cost of production and distribution, forcing many businesses to re-evaluate their pricing strategies.

Higher fuel costs affect logistics, manufacturing, and retail across the entire supply chain, from sourcing to delivery. Meanwhile, taxes on sweetened beverages force F&B businesses to absorb costs or raise prices, potentially impacting demand.

C. Changes in employee compensation and payroll management

The personal income tax overhaul increases employees’ take-home pay, which can improve morale and productivity, but it also requires updated payroll calculations under the new income tax rate table Philippines. It allows businesses to review compensation and optimize allowances.

D. Navigating new financial compliance and reporting standards

The TRAIN Law has intensified the need for meticulous record-keeping and accurate financial reporting to ensure compliance with the Bureau of Internal Revenue (BIR). With changes in VAT thresholds, the risk of errors and penalties has increased.

This environment underscores the importance of robust financial systems that can handle complex calculations and generate precise reports. Businesses must ensure their accounting teams are well-versed in the new regulations and that their processes.

How to Ensure Your Business is Compliant and Competitive Post-TRAIN

Adapting to the TRAIN Law is an ongoing process that goes beyond basic compliance. Businesses must integrate tax changes into core operations to stay efficient and competitive.

This shift has exposed the limits of manual and outdated processes. Using the right tools and strategies helps automate compliance, improve accuracy, and gain clearer financial visibility.

A. Conduct a comprehensive review of your financial processes

- Check if your annual sales have exceeded the ₱3 million VAT threshold. If so, you must comply with the new VAT reporting rules.

- Review the pricing of products affected by new excise taxes (e.g., sweetened beverages). Ensure pricing adjustments align with increased costs.

- Audit supply chain costs and verify that your pricing reflects the new tax regulations to ensure no hidden expenses are left unchecked.

B. Modernize your payroll and accounting systems

- Update payroll brackets according to the latest income tax tables. Ensure payroll systems can calculate new tax deductions automatically.

- Automate accounting processes to streamline VAT and excise tax management, reducing the risk of human error. Utilize accounting software to handle complex tax calculations directly in your financial workflows.

- Review payroll entries to ensure the correct withholding taxes are applied for each employee based on updated tax brackets.

C. Leverage technology for automated and accurate tax management

- Implement an integrated accounting system (like HashMicro’s Accounting Software) to handle automated VAT and excise tax calculations directly within your financial digital workflow management.

- Ensure all transactions are recorded accurately according to the latest BIR regulations using a centralized platform that simplifies tax management.

- Use ERP software to generate compliant reports automatically and manage your financial data, including payables, receivables, and general ledger management.

Conclusion

The TRAIN Law has reshaped the Philippine business environment by affecting taxation, costs, pricing, payroll, and financial compliance. For businesses, understanding the core provisions is essential to managing risk and making informed strategic decisions.

Adapting to the TRAIN Law requires a proactive approach that goes beyond meeting minimum compliance requirements. By aligning financial processes and payroll management with updated tax regulations, companies can improve efficiency while maintaining competitiveness.

To navigate these changes effectively, businesses should leverage modern financial tools that improve accuracy and control. Seeking expert guidance through a free consultation can also help organizations assess readiness and strengthen long-term financial resilience.

Frequently Asked Questions

-

What is the main goal of the TRAIN Law?

The primary goal of the TRAIN Law is to create a simpler, fairer, and more efficient tax system in the Philippines. It aims to generate revenue for government infrastructure and social services while providing tax relief to most Filipino taxpayers to boost their purchasing power.

-

Who benefits most from the TRAIN Law’s income tax changes?

Individuals earning an annual taxable income of ₱250,000 or less benefit the most, as they are now fully exempt from personal income tax. Middle-income earners also generally see higher take-home pay due to the restructured, lower tax rates.

-

Is the TRAIN Law still in effect today?

Yes, the TRAIN Law (RA 10963) is still in effect in 2026. It was designed with staggered implementation for certain components, like fuel excise taxes, and it continues to be the foundational tax code for personal income, VAT, and various excise taxes in the Philippines.