Do you know that businesses managing inventory manually often face expensive mistakes each year? Many of these errors can be avoided by using effective methods like the First-In, First-Out (FIFO) method. Whether you run a small shop in Manila or manage a large distribution center in Cebu, applying FIFO principles can make a big difference.

Using inventory management software that supports FIFO can further enhance this process. These tools automate inventory management, ensuring FIFO is applied consistently. This improves accuracy, reduces waste, and boosts efficiency, ultimately impacting your bottom line and helping you stay competitive.

To learn more about how FIFO works and how you can apply it effectively in your business, read our next section on “What is the FIFO Method.”

Key Takeaways

The FIFO (First-In, First-Out) method helps businesses reduce waste and improve profitability by ensuring that the oldest inventory items are sold first.

FIFO is especially beneficial for industries with perishable goods, such as food and beverages, as well as sectors like electronics and fashion, where product relevance is key.

FIFO inventory valuation aligns the cost of goods sold with the oldest inventory costs, offering a more accurate reflection of the current market value. It offers versatility across various industries.

What is the FIFO Method?

The FIFO (First-In, First-Out) method actively manages the control of inventory by selling or using the first items added to inventory first. This technique ensures that goods purchased or produced earlier are utilized or sold before newer inventory.

FIFO effectively aligns inventory costs with current sales prices, giving companies a more accurate assessment of their inventory value. By selling older items first, businesses base their cost of goods sold (COGS) on the cost of earlier purchases, often reflecting lower prices.

This method also prevents discrepancies between current market prices and the inventory recorded in financial statements, providing businesses with a clear and consistent view of profitability.

How FIFO is Applied in Inventory Management

In inventory management, the FIFO method is crucial for industries where product freshness, relevance, or expiration is a concern. For example, in the food and beverage sector, FIFO ensures that older stock is sold before newer inventory, minimizing waste and avoiding aging in inventory.

This method also benefits industries such as fashion, electronics, and pharmaceuticals, where products can lose value or become obsolete over time. By applying FIFO, companies keep inventory fresh, maintain product relevance, and ensure customers receive up-to-date goods. FIFO also simplifies inventory tracking and reporting because it closely follows the actual flow of goods, which makes stock management and audits easier.

How the FIFO Method Works

To understand FIFO more clearly, you need to see how it applies to both inventory valuation and cost calculation. This method follows a simple principle: businesses sell or use their oldest inventory first. As a result, FIFO affects how companies record the cost of goods sold and value their remaining stock.

FIFO Inventory Valuation Explained

FIFO inventory valuation is straightforward: the cost of goods sold (COGS) is based on the cost of the earliest inventory purchases. This means that during periods of inflation, where prices rise over time, the COGS will reflect the older, lower costs.

As a result, the ending inventory is valued at the most recent, higher costs, providing a more accurate representation of the current market value.

The FIFO Calculation Process

Calculating FIFO is a simple process that involves matching the oldest inventory costs with the latest sales. For each sale, the cost is assigned based on the order of purchase, starting with the earliest inventory.

This process continues until all inventory from that period is depleted, then the next oldest inventory is used, and so on.

FIFO Formula & Calculation Example

The FIFO formula does not subtract the oldest inventory cost from revenue. Instead, it calculates the cost of goods sold (COGS) by assigning the cost of the oldest inventory units to the units sold first.

It is expressed as:

FIFO COGS = (Units sold from oldest batch × oldest unit cost) + (Units sold from next batch × next unit cost) + …

This formula helps businesses calculate COGS accurately because it uses the earliest inventory costs first. As a result, the ending inventory reflects the value of the most recently purchased units.

Step-by-Step Calculation

- Identify the oldest inventory batch and its unit cost.

- Match the units sold with that batch first.

- Multiply the number of units sold by the unit cost of that batch.

- If the sale exceeds the first batch, continue with the next oldest batch.

- Add the costs from each batch to get the total FIFO COGS.

Real-Life Example and Walkthrough

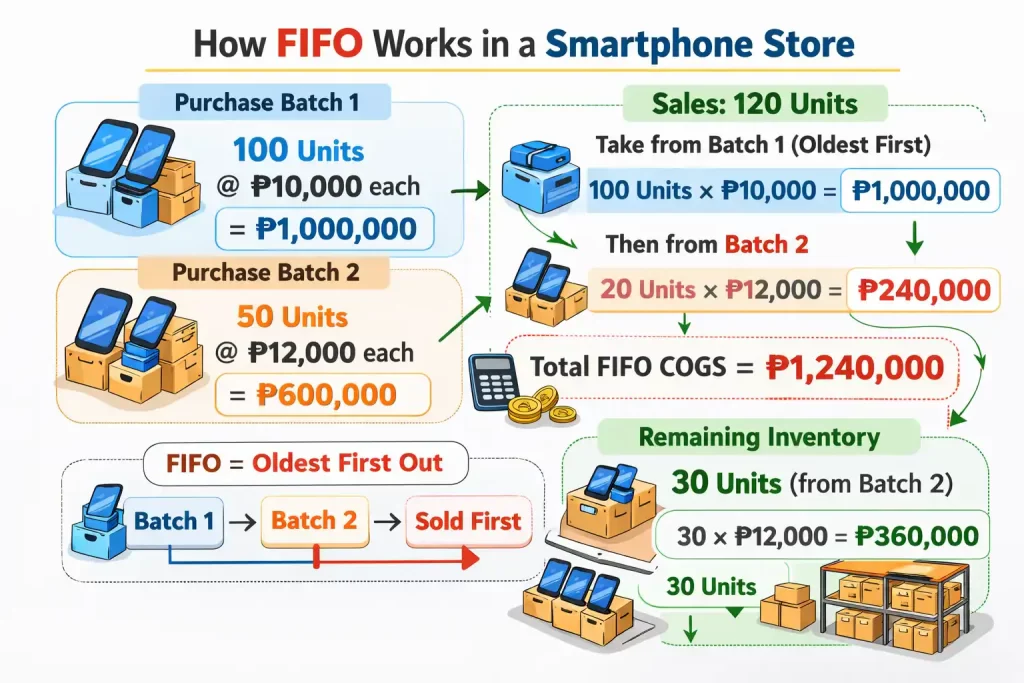

Suppose an electronics store purchased 100 smartphone units at ₱10,000 each and later purchased 50 more units at ₱12,000 each.

If the store sold 120 units, FIFO assigns the cost of the first 100 units to the oldest batch:

100 × ₱10,000 = ₱1,000,000

The remaining 20 units come from the second batch:

20 × ₱12,000 = ₱240,000

So, the total FIFO COGS = ₱1,240,000

The remaining inventory is 30 units from the second batch, valued at:

30 × ₱12,000 = ₱360,000

This method ensures that the business records the oldest inventory costs first, while the remaining inventory reflects more recent purchase costs.

Pros and Cons of the FIFO Method

The FIFO method, like any other inventory management method, has its own benefits and downsides. These key pros and cons will show you if your business needs to apply the FIFO method:

Advantages

- Higher Valuation for Ending Inventory: FIFO results in a higher valuation for ending inventory, as it accounts for the most recent costs.

- Increased Net Income: By using older, lower-cost inventory first, businesses can show higher profits during inflationary periods.

- Reflects Actual Inventory Movement: FIFO accurately represents the physical flow of inventory, especially for perishable goods.

Disadvantages

- Potential Discrepancies with Spikes in COGS: During periods of rapid price increases, FIFO may lead to discrepancies in COGS, affecting profit margins.

- Higher Taxes Due to Increased Income: Higher reported income can lead to higher tax liabilities, a significant consideration for businesses.

FIFO vs. Other Inventory Methods

Businesses use several inventory valuation methods, but each one affects cost calculations, inventory value, and financial reporting differently. To understand why many companies choose FIFO, it helps to compare it with other common methods such as LIFO, Average Cost, and Specific Identification. This comparison shows how each method works and which approach fits different business needs better.

FIFO vs. LIFO

While FIFO focuses on selling the oldest inventory first, the Last-In, First-Out (LIFO) method does the opposite, selling the most recently acquired inventory first. LIFO can result in lower taxes during inflation, but might not reflect the actual inventory flow, making FIFO a more realistic approach.

FIFO vs. Average Cost Method

The Average Cost Method averages the cost of all inventory items and applies this average to each sale. While simpler, it may not provide as accurate a reflection of inventory value as FIFO does, especially in industries with fluctuating costs.

FIFO vs. Specific Identification Method

The Specific Identification Method tracks each inventory item individually, assigning the exact cost to each sale. While precise, it is more complex and less practical for businesses with large volumes of inventory, making FIFO a more efficient choice.

Choosing the Right Inventory Method for Your Business

When selecting an inventory method, consider factors like the nature of your products, market conditions, and tax implications. For Filipino businesses, where market dynamics can change rapidly, choosing the right method is crucial to maintaining profitability and compliance.

How to Decide Between FIFO and Other Methods

To decide between FIFO and other methods, assess your business’s specific needs. FIFO is ideal for businesses dealing with perishable goods or where inventory valuation accuracy is paramount. However, consult with a financial expert to ensure the chosen method aligns with your long-term business goals.

Why FIFO is a Popular Choice

FIFO is a popular choice because it offers versatility across various industries. Whether you’re in retail, manufacturing, or food service, FIFO ensures your inventory is managed efficiently, increasing turnover, reducing waste, and maximizing profits.

In the Philippines, where businesses often face challenges related to inventory spoilage and obsolescence, FIFO aligns perfectly with the need for efficiency and cost-effectiveness. Your businesses can benefit from FIFO by ensuring that older stock is always sold first, reducing the risk of waste, and ensuring product freshness.

Conclusion

Wrapping up, it’s clear that the right inventory management approach can really impact your business’s success. The FIFO method, with its simple yet effective strategy, helps keep your inventory organized, reduce waste, and ensure you’re always selling the oldest stock first.

Keeping track of inventory can be challenging, no matter how great your method is. That’s where the right inventory management system comes to the rescue. It’s designed to make your life easier, giving you real-time insights and reports that help you stay on top of your stock without the stress.

FAQ About FIFO Method

The FIFO method is crucial because it ensures that the oldest inventory is sold first, reducing waste, preventing obsolescence, and providing a more accurate reflection of inventory costs, especially in industries with perishable goods or fluctuating prices.

FIFO is better because it reduces waste by selling older stock first, reflects actual inventory movement, and provides accurate financial reporting during inflation by aligning costs with the oldest inventory.

To solve FIFO, track inventory costs from the oldest to the newest. Match the oldest costs to sales first, then continue with the next oldest until all units sold are accounted for.

FEFO is better when products have expiration dates, such as food, medicine, and cosmetics. FIFO works well for general inventory, but FEFO helps businesses reduce spoilage and sell items before they expire.>

Yes, because LIFO often feels less intuitive and may not match the actual physical flow of inventory.>