Many businesses face challenges in differentiating between inventory that still holds value and items that should be removed from their financial records. Without a solid understanding of inventory write-offs, issues like overstated assets, poor financial accuracy, and inefficient stock management can arise.

Inventory write-off refers to the process of removing items from inventory records when they are no longer sellable due to damage, expiration, or obsolescence. Managing write-offs correctly helps maintain accurate accounting, supports smarter purchasing decisions, and minimizes unnecessary losses.

Discover how recognizing and addressing inventory write-offs promptly can strengthen business resilience.

Key Takeaways

|

Table of Contents

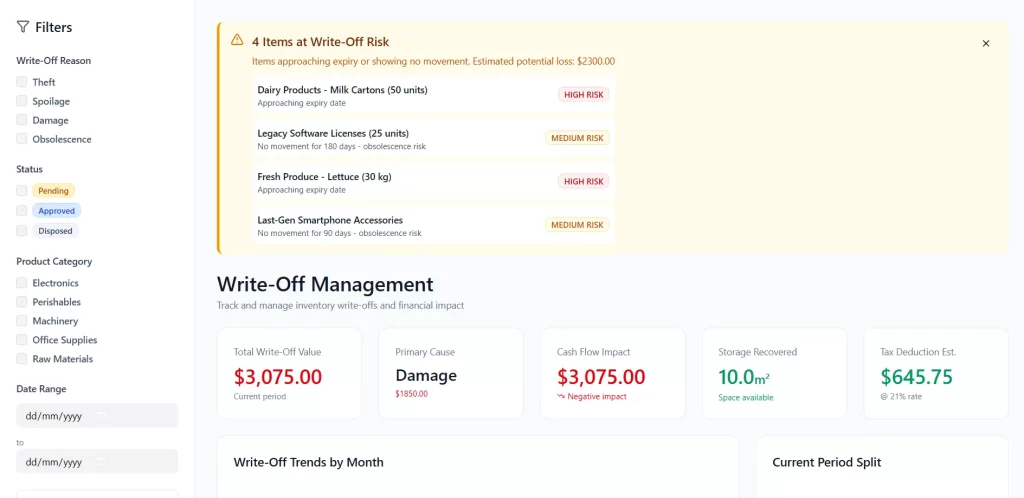

What is an Inventory Write-Off?

An inventory write-off is a financial process used to eliminate unsellable goods from a company’s inventory records. It typically occurs when products are damaged, past their expiration date, or no longer usable due to obsolescence.

By writing off these items, businesses acknowledge that the affected inventory holds no recoverable value. This adjustment helps maintain accurate financial statements and ensures that inventory figures reflect only items with genuine business value.

Types of Inventory Write-Offs

Inventory write-offs occur for various reasons, each with distinct implications for your business operations and financial accuracy. Understanding the causes behind these adjustments is crucial to maintaining precise inventory records.

Below are some of the most frequent types of inventory write-offs:

1. Theft or loss

Theft or loss occurs when stock disappears due to internal theft, shoplifting, or errors such as misplaced inventory. Since these items can no longer be located, they must be written off to maintain accurate inventory records.

This process also helps businesses track shrinkage patterns and assess the effectiveness of their loss-prevention efforts.

2. Spoilage (for perishable goods)

Spoilage typically affects industries that handle food, drinks, or medical products. If goods expire or are improperly stored and become unusable, they lose their commercial value and need to be removed from inventory through a write-off.

3. Damaged goods

Product damage can occur through various means, including mishandling, transportation issues, or exposure to harsh conditions such as moisture or extreme temperatures. Items like soaked electronics or ripped garments become unsellable and must be removed from inventory.

Writing them off helps maintain accurate stock valuation and ensures your financial reports present a realistic picture of your assets.

4. Obsolete inventory

These are products that have lost their market value due to being outdated or falling out of demand. Common examples include seasonal merchandise that is no longer in season or older electronics that newer versions have replaced.

Obsolete inventory not only occupies storage space but also locks in the capital that could otherwise support higher demand or more profitable stock.

Why is it Important to Manage Write-Offs?

Proper inventory management plays a key role in ensuring your business’s financial records remain accurate and reliable. By handling inventory write-offs correctly, you can gain clearer insights into operational performance.

Below are some key reasons why effectively managing write-offs is vital for your business:

1. More accurate forecasting

Keeping precise inventory records, especially when it comes to write-offs, helps improve forecasting and inventory planning.

Recognizing and analyzing inventory losses enables companies to make more informed decisions regarding restocking and inventory management.

When managed properly, it ensures that financial data remains reliable and supports sound decision-making grounded in actual operational performance.

2. Better cash flow

Proper inventory control, particularly through timely write-offs, is essential for maintaining a strong cash flow. Removing non-sellable stock also helps reduce surplus inventory and unlock tied-up capital.

By maintaining accurate inventory data, companies can also allocate resources more effectively to items that drive revenue and enhance overall profitability.

3. Improve operational efficiency

Properly managing inventory write-offs is crucial for maintaining accurate financial records that accurately reflect the actual value of your stock. A proactive approach not only prevents operational inefficiencies but also frees up valuable storage space and capital.

It also enables your team to focus on high-performing inventory that directly contributes to profitability and long-term business growth.

4. Keep accurate inventory records for accounting and tax purposes

Accurate inventory records are vital for both financial audits and tax reporting. If outdated or unsellable items aren’t properly written off, it can inflate asset values and raise red flags during audits.

Inventory write-offs are treated as losses and can reduce taxable income, but proper documentation and compliance with tax rules are essential.

Many businesses also use the allowance method to anticipate potential losses from obsolete stock, helping them manage tax deductions more effectively.

5. Assess your financial health

Improper handling of excess inventory write-offs can distort your company’s financial position. Keeping damaged or obsolete items on the books inflates inventory value and creates a misleading impression of economic health.

This overstatement may lead to poor decisions, such as under-ordering or missing opportunities to restock with better-selling items. Write-offs also affect COGS and net income, offering a clearer view of profitability.

Since they reduce retained earnings, write-offs directly impact shareholders’ equity, underscoring the importance of accurate inventory management.

How to Write-Off Inventory in 5 Steps

Following the proper procedure for writing off obsolete inventory through a journal entry is crucial to maintaining the integrity of your financial statements and supporting informed business decisions. Below is a step-by-step overview of how to write off inventory correctly.

1. Evaluate the remaining value

First, assess whether the inventory still holds any recoverable market value. If some value remains, it may qualify for a write-down instead of a complete write-off. However, if the items are completely worthless, proceed with the write-off procedure.

2. Assess the materiality of the loss

If the financial impact of the loss is minor, it can be recorded as part of the cost of goods sold (COGS). But if the value is substantial, it should be logged separately in an inventory write-off account to ensure transparency and avoid skewing gross margin calculations.

3. Record a journal entry

According to GAAP, an inventory write-off journal entry must be recorded immediately to ensure that financial statements reflect accurate asset values and comply with the matching principle.

4. Choose a disposal method

Once written off, inventory doesn’t need to be disposed of immediately; however, any disposal must comply with IRS-approved procedures, which may include donation, liquidation, or destruction.

5. Keep detailed documentation

Regardless of the disposal route, thorough records, including receipts, photos, and written logs, must be maintained. These serve as evidence for tax reporting or future audits to justify the write-off.

Inventory Write-Off Example

A seafood distributor in Cebu stores premium tiger prawns and lobsters in a specialized cold storage facility. Due to a sudden power outage and delayed generator backup, one of the storage units malfunctions, leading to the spoilage of several trays of shellfish. As these products are no longer viable for sale, they must be written off in their entirety.

If the loss is relatively minor, such as ₱28,000 worth of shellfish from just one unit, it can be treated as a regular adjustment. Losses of less than 5% of total inventory are typically considered immaterial and don’t require special reporting.

However, if the issue affects multiple cold storage units, resulting in a much larger loss, such as ₱280,000 worth of premium seafood, it would be classified as material.

In this case, instead of debiting Cost of Goods Sold (COGS), which could skew financial metrics, the company should record the loss in a separate inventory write-off account to maintain clear and accurate financial reporting.

To calculate the COGS, follow this formula:

COGS = Beginning Inventory + Purchases – Ending Inventory

Conclusion

Inventory write-offs are an unavoidable part of running a product-based business, but how a company handles them makes a significant difference to its financial accuracy and operational health. Recognizing write-offs promptly, documenting them correctly, and distinguishing between a write-off and a write-down ensures that financial statements remain reliable and that tax reporting stays compliant.

Whether the cause is spoilage, theft, damage, or obsolescence, treating each write-off as a signal rather than just a loss helps businesses identify patterns, tighten procurement decisions, and reduce future exposure. For businesses looking to build stronger stock controls around these processes, reviewing the best inventory management software options available today is a practical starting point.

Frequently Asked Questions

-

Can you sell inventory that has been written off?

You can indeed write off inventory and then sell it, but it’s essential to follow the correct accounting practices. Writing off inventory usually happens when items become unsellable or out of date.

-

What is a write-off in simple terms?

A write-off is an accounting practice that recognizes expenses or losses deemed unrecoverable. It removes the asset or debt from the balance sheet and records the loss on the income statement, ensuring accurate financial reporting.

-

What is the difference between a write-down and a write-off?

A write-down reduces the value of an asset for tax and accounting purposes, but the asset still retains some value. A write-off reduces the value of an asset to zero and negates any future value.