Managing accounting in the construction industry can be challenging due to unique project costs, timelines, and contract requirements. Accurate tracking of labor, materials, and overhead is essential for maintaining control and profitability.

A construction-specific financial system streamlines these processes, providing automated cost tracking, real-time reporting, and compliance management. This helps contractors optimize budgeting, manage expenses, and improve cash flow efficiently.

But how exactly does a construction-focused accounting system enhance spending, cash flow, and overall profitability? Let’s explore how these tools support smarter financial management in construction projects.

Key Takeaways

Efficient construction accounting tracks costs, manages budgets, ensures compliance, monitors profitability, and supports informed financial decisions.

Construction accounting improves financial accuracy, enables real-time cost monitoring, simplifies multi-project management, and ensures tax compliance.

Contractors should track costs precisely, choose the right accounting method, optimize tax strategy, and use software for efficient financial management.

What is Construction Accounting?

Construction accounting involves tracking project costs, managing budgets, and maintaining cash flow to ensure smooth operations. Using a specialized tool like Construction Accounting Software allows firms to efficiently handle multiple contracts while monitoring expenses in real time.

This system helps construction companies assess project profitability, control costs, and make informed financial decisions. By centralizing project-specific financial data, companies can optimize resource allocation and minimize financial risks.

Moreover, maintaining accurate accounting records ensures compliance with industry regulations and enhances transparency for stakeholders. A proactive accounting approach not only safeguards profits but also supports long-term business growth.

Why is Construction Accounting Important?

Effective construction accounting is crucial for the success of any construction business. It goes beyond basic bookkeeping, providing specialized insights tailored to the industry’s unique challenges. Here are the key reasons why construction accounting is essential

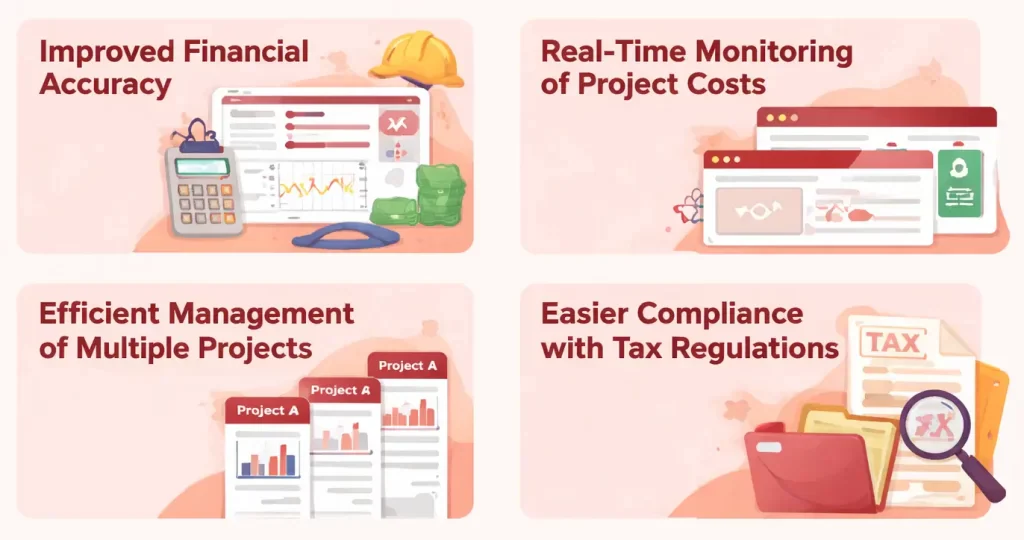

1. Improved Financial Accuracy – Construction project accounting software records and tracks project costs in detail, minimizing errors, and when integrated with estimating and budgeting tools, it ensures accurate and transparent financial reporting.

2. Real-Time Monitoring of Project Costs – Accounting software allows companies to monitor expenses in real time, helping control budgets and prevent cost overruns, while pairing it with scheduling software further streamlines project timelines.

3. More Efficient Management of Multiple Projects – The system organizes financial reports from multiple projects separately, simplifying oversight and enabling companies to track each project’s financial performance without confusion.

4. Easier Compliance with Tax Regulations – Construction accounting systems help maintain organized and complete records for audits and tax purposes, reducing the risk of penalties from reporting or tax errors.

Construction Accounting vs Regular Accounting: What’s the Difference?

Construction accounting and regular accounting share the same fundamental principles, but they differ significantly in their application due to the unique needs of the construction industry. The following table highlights the key differences between the two:

| Aspect | Construction Accounting | Regular Accounting |

| Cost and Revenue Management | Manages project-based costs and revenues tied to timelines | Records periodic transactions without project focus |

| Budget Complexity | Tracks materials, labor, equipment, and changes in detail | Uses simpler, more predictable budgeting |

| Contract Recording | Maintains detailed records of project-specific contracts | Focuses on broader company contracts |

| Revenue Recognition | Applies methods like percentage of completion or completed contract | Recognizes revenue within standard periods |

| Operational Environment | Handles decentralized, site-specific operations with varying regulations | Operates in centralized, stable environments |

Construction Accounting Concept

To better understand the financial aspects of the construction industry, it is essential to grasp the core principles of construction project accounting, which are crucial for managing project costs, budgeting, and financial reporting, including the role of bonds in construction.

Construction Accounting Core Concepts

1. Job Costing – Job costing tracks costs like materials, labor, and equipment for each project, with construction accounting programs monitoring these in real time for accurate budgeting and decision-making.

2. Progress Billing – Projects often use progress billing, invoicing clients at various stages to maintain steady cash flow and align payments with project schedules.

3. Retention Accounting – Retention withholds a percentage of payment until project standards are met, and accounting systems ensure proper recording and timely release.

4. Revenue Recognition – Long-term projects require methods like percentage-of-completion or completed-contract to ensure financial statements reflect true progress.

5. Change Orders Management – Change orders modify scope, timeline, or costs, and accurate accounting keeps budgets realistic and clients billed correctly.

6. Equipment and Asset Management – Tracking depreciation, maintenance, and usage ensures construction equipment is efficiently utilized and accurately reported.

7. Overhead Allocation – Overhead costs, including rent, insurance, and admin salaries, must be allocated properly to reveal each project’s true cost and profitability.

8. Compliance and Tax Considerations – Construction accounting maintains compliance with labor laws, payroll taxes, and industry regulations while optimizing tax strategies and ensuring accurate reporting.

Types of Accounting Used in Construction

Understanding the types of accounting used in construction is essential for ensuring accurate financial management and maintaining control over complex projects. Each approach serves a specific purpose tailored to the unique demands of the industry:

- Job cost accounting: This type of accounting focuses on tracking all costs related to individual construction projects. It helps contractors manage project budgets, monitor spending, and ensure profitability for each job.

- Cash basis accounting: Cash basis accounting records revenue when cash is received and expenses when they are paid. This simple method is often used by smaller construction companies for its straightforward approach.

- Accrual basis accounting: Accrual accounting recognizes revenue and expenses when they are earned or incurred, regardless of when cash is exchanged. This method provides a more accurate financial picture for larger construction companies.

- Percentage-of-completion accounting: Common in long-term construction projects, this method recognizes revenue and expenses proportionally as the project progresses. It ensures that income is recorded throughout the project, providing a more consistent financial overview.

- Cost allocation accounting: This type focuses on distributing indirect costs, such as overhead and administrative expenses, across multiple projects. It ensures accurate job costing and profitability analysis.

Key Aspects of Accounting Software for Construction

Construction accounting differs from regular accounting primarily in revenue recognition. Revenue is recorded based on the percentage of project completion, allowing companies to match income with project progress rather than waiting for full completion.

It also emphasizes individual project management, tracking budgets, expenses, and revenues separately for each project. This ensures more detailed and accurate financial oversight tailored to the unique demands of construction work.

Financial reporting in construction accounting often includes specialized project-based reports. These reports, such as project cost statements, enable managers to monitor financial health in real time and make informed decisions.

"Construction accounting aligns revenue recognition with project progress, providing a more accurate reflection of income as work advances. By tracking each project's budgets, expenses, and revenues individually, it ensures detailed financial oversight and informed decision-making."

Construction Accounting Difficulties and How to Overcome Them

Although accounting for construction companies can indeed make it easier for management to manage finances, implementing construction project accounting cannot be said to be easy. What are the difficulties that will be faced to make accounting for construction companies difficult to do?

Here are the difficulties of implementing accounting for construction and tips on how to overcome them:

1. Fluctuating income

Construction projects often have volatile revenues since payments are made in stages, making cash flow difficult to predict.

Solutions – Companies should plan cash flow carefully, using monthly estimates based on payment milestones to anticipate revenue timing and prepare backup funds.

2. Changes in project demand and specifications

Mid-project changes, such as redesigns or material updates, can disrupt budgets and schedules, complicating financial reporting.

Solutions – Stay flexible with budgets and record every change accurately, ideally with a system that updates financial statements automatically.

3. Difficulty in recording projects by stages

Work is often carried out in multiple stages, requiring financial records to reflect progress, revenue, and costs for each stage.

Solutions – The percentage of completion method allows companies to record revenue and costs based on actual progress, ensuring accurate statements.

4. Constraints in managing construction tax

Construction projects involve complex tax obligations beyond income tax, including materials and subcontractor taxes.

Solutions – Finance teams should understand construction-related tax rules and consult tax experts regularly to remain compliant.

5. Complex project cost management

Managing costs in construction is challenging due to materials, labor, equipment, and overheads, especially with varying project durations and scales.

Solutions – Use a structured, detailed cost recording system to monitor budgets and track expenses in real time.

The accounting system offers flexible, multi-level analytical tools for construction accounting, enabling real-time tracking of financial transactions by category (e.g., materials, operational costs, salaries). It provides accurate insights to help management make informed decisions. A free demo allows businesses to evaluate the system’s suitability before implementation.

Common Mistakes in Construction Accounting

Errors in construction accounting can lead to financial losses, project delays, and damaged relationships with clients and stakeholders.

1. Disorganization – Lack of proper organization in accounting records can result in misplaced invoices, untracked expenses, and incomplete financial data, causing budgeting errors, compliance issues, and difficulties in tracking project profitability; implementing a systematic record-keeping process and using accounting software helps maintain order and accuracy.

2. Poor Cost Estimation – Inaccurate cost estimation during planning can lead to unexpected expenses and reduced profits, often caused by inadequate data, overlooked variables, or failure to account for risks; detailed analysis, historical data, and contingency planning create reliable job cost estimates.

3. Inaccurate Recognition of Joint Ventures – Improperly accounting for shared costs, revenues, and responsibilities in joint ventures can cause financial disputes and compliance issues; using construction project management software helps standardize cost allocation, track shared expenses in real time, and maintain transparency.

4. Incorrect Overhead Calculations – Miscalculating overhead costs like administrative expenses and equipment depreciation can distort project profitability and pricing strategies; regularly reviewing and updating allocations ensures accurate financial reporting.

5. Mishandled Change Orders – Poorly tracked change orders can lead to unbilled work and client disputes; establishing a clear process for approving, tracking, and billing change orders prevents financial discrepancies.

6. Unreasonable Contract Terms – Agreeing to unclear or unfavorable contract terms can expose businesses to financial and legal risks, including payment delays and unexpected liabilities; thoroughly reviewing and negotiating fair terms protects cash flow and operational stability.

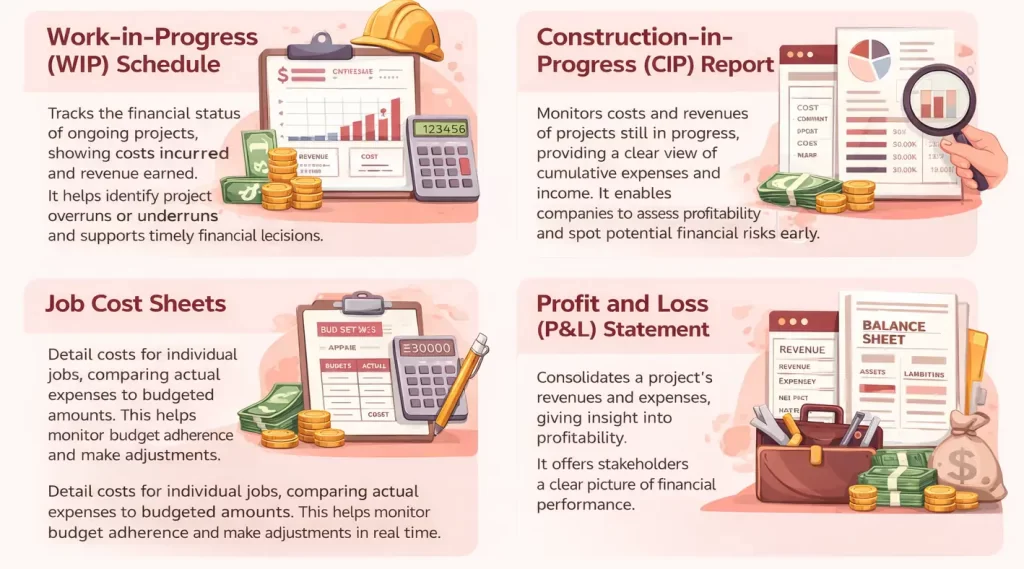

Financial Statements Specific to Construction Accounting

In construction project accounting, certain financial statements are tailored to address the industry’s unique complexities. These specialized reports are designed to provide accurate, actionable data that reflects the dynamic nature of construction projects.

Below are key financial statements that are essential for construction businesses to track progress and make informed decisions:

These financial statements in construction project accounting are not only vital for tracking financial health but also crucial for informed strategic decisions, enabling construction companies to stay on top of their financial performance and achieve sustainable growth.

4 Construction Accounting Best Practices for Contractors

1. Emphasize Precise Job Costing – Contractors should track all project-related costs, including labor, materials, and indirect expenses. Job costing statements or construction accounting tools help compare actual costs with budgets and identify opportunities for improvement.

2. Select the Appropriate Accounting Approach – Choosing the right method is key, with cash basis suitable for smaller projects and accrual basis providing detailed financial insights. Large projects often use the percentage-of-completion method, while residential projects may prefer the completed-contract method to defer revenue recognition.

3. Identify the Optimal Tax Strategy – Tax obligations vary based on revenue recognition, project type, and business structure. Contractors can align accounting methods with project types and entity structures to optimize tax outcomes.

4. Invest in Construction Accounting Software – Modern accounting tools automate job costing, streamline financial oversight, and ensure tax compliance. Features like project monitoring, real-time analytics, and flexible revenue recognition support efficient management of construction finances.

Case Study: Construction Accounting Challenges and Solutions in the Philippines

A medium‑sized construction firm in Metro Manila struggled with cash flow management and cost control due to long project cycles and fluctuating expenses, leading to frequent budget overruns and delayed payments from clients. These issues made it difficult for the company to maintain clear financial visibility across multiple projects and disrupted their ability to forecast profitability accurately.

After realizing the limitations of manual bookkeeping and fragmented spreadsheets, the finance team implemented a dedicated construction accounting system to automate cost tracking, monitor project budgets in real time, and manage complex revenue recognition methods like percentage‑of‑completion. With these tools, the firm improved financial accuracy, streamlined tax compliance, and gained better insight into project‑specific performance, ultimately strengthening its operational planning and decision‑making.

Encouraged by these results, leadership began evaluating pricing schemes and scalable software options tailored for the Philippine construction market, weighing subscription levels and feature sets that would support continued growth while balancing budget constraints.

Conclusion

Construction accounting requires specialized processes to manage the unique financial aspects of building projects. Unlike general accounting, it deals with industry-specific variables that demand careful tracking and management. The right system simplifies project finance complexities, offering visibility, accuracy, and control, while aligning financial management with operations.

By combining specialized practices with the proper tools, construction companies can improve efficiency and project outcomes. To see how this approach can work for your business, consider consulting with a specialist to identify the most effective system setup for your needs.

FAQ About Construction Accounting

FAQ

Construction companies often use job costing, percentage-of-completion, and completed-contract methods. These approaches are designed to suit the distinct characteristics of construction projects, enabling businesses to track project expenses, recognize revenue over time or at project completion, and handle long-term contracts efficiently.

Accounting for construction involves several specialized practices. These include tracking project-specific costs (job costing), managing revenue recognition based on the stage of completion or contract terms, and preparing detailed financial reports such as work-in-progress (WIP) schedules. Proper accounting ensures accurate budgeting, cash flow management, and compliance with industry regulations.

Construction costs are typically categorized into three main groups: labor, materials, and overhead. Within these categories, companies often use cost codes to track specific expenses, such as different types of materials, and assign each cost to a particular construction project. When allocating overhead expenses, most businesses first determine their total overhead and then distribute it as a percentage of the project’s labor and material costs.

Construction in progress (CIP) accounting is a method used to track costs related to ongoing construction projects before they are completed and classified as fixed assets. This approach ensures that expenses such as labor, materials, and overhead are properly recorded until the project is finalized and transferred to the appropriate asset account.

In accounting, a building refers to a tangible asset that a company owns and uses for business operations. It is classified under property, plant, and equipment (PPE) and depreciated over its useful life to reflect its decreasing value.

Construction bookkeeping involves tracking project-specific costs, progress billing, and job costing, which differ from traditional bookkeeping. It requires detailed financial records for each project to ensure accurate cost allocation, budgeting, and profitability analysis.

A key formula in construction accounting, particularly for the percentage-of-completion method, is:

– Job cost = Direct costs + Indirect costs + Overhead allocation

– Gross profit margin = (Revenue – Cost of goods sold) / Revenue

– Percentage of completion = (Costs incurred to date / Total estimated project costs) x 100