Deducting wages to pay income tax should be an easy task; the intricacies of the BIR withholding tax system require a profound understanding, despite being one of the most critical components. Businesses in the Philippines have a duty to the Bureau of Internal Revenue (BIR) to be a withholding agent; failure to comprehend and execute these responsibilities accurately can lead to severe financial repercussions.

The withholding tax system helps the government secure steady revenue through tax deductions remitted to the BIR. For businesses, compliance gets complex because ATCs, rates, deadlines, and documents keep changing. The EOPT Act adds new rules, so companies need organized processes and close attention. Read more to see how your team can stay compliant with less confusion.

Table of Contents

Key Takeaways

|

Understanding the Fundamentals of BIR Withholding Tax

The BIR withholding tax system is a method of collecting income tax in advance from the payee of the income. It is not a separate or new type of tax. Rather, it is simply a mechanism for the advance collection of the income tax, percentage tax, or value-added tax (VAT) that the payee will eventually owe to the government. The system operates on a fundamental triad: the government (represented by the BIR), the withholding agent (the payor), and the taxpayer (the payee).

When a withholding tax transaction occurs, the payor serves as the government’s collection agent. The payor deducts the required amount, remits it to the BIR, and issues a withholding tax certificate to the payee. The payee then uses that certificate as a tax credit when filing quarterly or annual taxes. This system helps the government secure steady revenue, reduce tax evasion, and streamline collection. It also helps the BIR match reported expenses with declared income, which is why companies need accurate records, consistent workflows, and complete documentation to stay compliant.

The Core Mechanics: How the Withholding Tax System Works

Applying the BIR withholding tax system correctly starts with understanding the roles of the government, the withholding agent, and the payee. Under the Ease of Paying Taxes Act, withheld taxes are treated as trust funds, so businesses must keep them in a separate account. The obligation to withhold arises once income becomes payable, meaning it is already due, demandable, or legally enforceable, or once it is accrued, recorded, or supported by an issued invoice.

Once withholding applies, the withholding agent must identify the correct ATC, confirm the tax base, calculate the tax, and record the transaction properly. For many common VATable EWT transactions, businesses use the gross income payment exclusive of VAT, but they should still verify the rule for each case. The withholding agent must also issue the proper certificate, such as BIR Form 2307, to support the payee’s tax credit claim within the required deadline or earlier upon request.

Major Classifications of BIR Withholding Tax

The Philippine withholding tax system is not monolithic; it is divided into several distinct categories, each with its own set of rules, rates, and reporting requirements. Understanding these classifications is essential for accurate tax mapping and compliance.

Withholding Tax on Compensation (WTC)

Withholding Tax on Compensation (WTC) is the tax withheld from individuals receiving compensation income arising from an employer-employee relationship. WTC is perhaps the most universally recognized form of withholding tax, as it affects almost every formally employed individual in the country.

The employee’s salary tax deduction is based on the graduated income tax rates prescribed by the Tax Reform for Acceleration and Inclusion (TRAIN) Law, and subsequently the Corporate Recovery and Tax Incentives for Enterprises (CREATE) Act. The calculation of WTC is highly dynamic. It requires the employer to determine the employee’s gross taxable compensation by excluding non-taxable items such as statutory contributions (SSS, PhilHealth, Pag-IBIG), de minimis benefits (up to their prescribed limits), and the 13th-month pay and other benefits up to the maximum threshold of PHP 90,000.

The remaining taxable income is then subjected to the withholding tax table, which dictates the amount to be deducted per payroll period (daily, weekly, semi-monthly, or monthly). At the end of the year, employers are required to perform an annualization process to ensure that the total tax withheld matches the exact tax due for the entire year, refunding any excess or deducting any deficit from the final paycheck.

Expanded Withholding Tax (EWT) / Creditable Withholding Tax (CWT)

Expanded Withholding Tax or Creditable Withholding Tax is the most complex category for businesses to manage. It applies to specific types of income payments made by a resident to another resident. The tax withheld is creditable, meaning the payee can use it to offset their quarterly and annual income tax liabilities. The complexity of EWT lies in the sheer volume of transactions it covers and the varying rates assigned to different Alphanumeric Tax Codes (ATCs). Common EWT rates include:

Final Withholding Tax (FWT)

Final Withholding Tax (FWT) serves as the full and final income tax on specific types of passive income. Once the withholding agent deducts and remits it, the taxpayer no longer reports that income annually. FWT usually applies to interest, royalties, prizes, winnings, some dividends, deposit substitutes, trust funds, and similar arrangements (typically subject to 20%). Because the tax is final, the withholding agent carries full responsibility for collecting and remitting the correct amount.

Fringe Benefits Tax (FBT)

Fringe Benefits Tax is a final withholding tax on benefits given to managerial or supervisory employees. It does not usually apply to rank-and-file employees under regular compensation tax. Employers compute FBT by grossing up the benefit’s value, applying the 35% rate, and paying the tax as a deductible business expense. If a company misclassifies, undervalues, or fails to remit FBT, it can face major BIR audit assessments.

Withholding of Value-Added Tax (WVAT) and Percentage Taxes

In certain cases, the government withholds business taxes (VAT or Percentage Tax) on top of income taxes. The most common instance of WVAT involves transactions with the government. Government agencies must withhold 5% Final VAT when purchasing from VAT-registered suppliers. Non-VAT entities under the 3% percentage tax face similar withholding rules. Proper invoicing and reconciliation are essential. Taxpayers must account for withheld VAT in monthly and quarterly declarations to avoid double taxation.

Essential BIR Forms and Certificates Every Business Must Know

Compliance with the BIR withholding tax system is intrinsically tied to the accurate preparation and timely filing of numerous tax forms. The BIR relies heavily on these standardized documents to track remittances, cross-reference data, and execute tax audits. Understanding the purpose and workflow of each form is non-negotiable for any finance department.

Monthly and Quarterly Remittance Returns

The primary vehicles for remitting withheld taxes to the government are the remittance returns. Historically filed monthly, the BIR has shifted some of these to a quarterly basis to ease the burden on taxpayers, although monthly remittances are still required in many cases, depending on the type of withholding tax involved. Under the current rules, taxpayers generally file tax returns electronically, while payments may be made electronically or manually through authorized channels.

| BIR Form | Purpose | Remittance / Filing Rule | Deadline |

|---|---|---|---|

| 1601-C | Used by employers to remit taxes withheld from employees’ salaries. | Filed monthly. Taxpayers enrolled in eFPS must follow the applicable BIR filing and payment schedule. | For January to November, due on or before the 10th day of the following month. For December, due on or before January 15 of the following year. |

| 1601-EQ | Used to report and remit expanded withholding taxes deducted from suppliers of goods and services. | Filed quarterly. Taxpayers must still remit withholding tax for the first two months of each calendar quarter using BIR Form 0619-E. | Due not later than the last day of the month following the close of the quarter. |

| 1601-FQ | Used to report and remit final withholding taxes for the quarter. | Filed quarterly. Taxpayers remit withholding tax for the first two months of each calendar quarter using BIR Form 0619-F. | Due not later than the last day of the month following the close of the quarter. |

Annual Information Returns and the Alphalist

Remitting the tax is only part of withholding tax compliance. The BIR also requires withholding agents to report detailed information about the employees or payees from whom tax was withheld through the Annual Information Returns and their accompanying alphalists. These alphalists follow BIR-prescribed formats and usually include key data such as the payee’s Tax Identification Number (TIN), name, nature of income payment, amount paid, and amount of tax withheld. The alphalist should reconcile with the corresponding remittance returns, certificates, and supporting records.

| BIR Form | What It Covers | Deadline | Key Notes |

|---|---|---|---|

| 1604-C | Summarizes compensation paid and taxes withheld for the year. | On or before January 31 of the following year. | Should reconcile with monthly 1601-C remittances, employee records, and year-end alphalist data. |

| 1604-E | Consolidates annual EWT data and income payments exempt from withholding tax. | On or before March 1 of the following year. | Its annual alphalist supports BIR verification of payments and tax credits. The related alphalist is filed through eSubmission regardless of the number of payees. |

| 1604-F | Summarizes income payments subject to final withholding tax. | On or before January 31 of the following year. | Attachments include alphalists for payees subject to final withholding tax, fringe benefits, and income payments exempt from withholding tax but still subject to income tax. |

In practice, BIR filing mechanics still distinguish between platforms. Under RMC No. 18-2021, mandated eFPS users may still use 1604-CF in eFPS, while offline eBIRForms or manual filers use 1604-C and 1604-F. Late filing may trigger a penalty of ₱1,000 per failure, up to ₱25,000 per year, unless reasonable cause applies.

Certificates of Tax Withheld

Certificates of tax withheld are key documentary proof of a withholding tax transaction and are especially important for the income recipient. Depending on the transaction and current BIR rules, these certificates may be issued and transmitted in physical or digital form, subject to BIR validation requirements.

| BIR Form | Purpose | Issuance Timing | Key Notes |

|---|---|---|---|

| 2316 | Certificate of Compensation Payment/Tax Withheld for employees. | Issued on or before January 31 of the succeeding year, or on the day of the last compensation payment if employment ends earlier. | Shows total compensation and tax withheld. For qualified employees, it supports substituted filing, so they are not required to file BIR Form 1700. |

| 2307 | Certificate of Creditable Tax Withheld at Source for creditable withholding tax. | Furnished within 20 days from the close of the quarter. | Supports the payee’s tax credit claim, not a deduction claim. It may be transmitted digitally, and the BIR validates it against SAWT and the withholding agent’s alphalists. |

| 2306 | Certificate of Final Tax Withheld at Source for final withholding tax transactions. | Issued for transactions subject to final withholding tax. | This remains the proper certificate for final withholding tax transactions. However, for certain real estate cases involving BIR Form 1606, Form 1606 with proof of payment serves as the supporting proof instead of Form 2307. |

The Newest Tax Table (2026)

As of 2026, the latest official BIR tax tables for compensation income still follow the rates effective January 1, 2023, onwards. Below are the updated annual and monthly withholding tax tables used for year-end tax computation and payroll withholding.

Revised Annual Tax Table

| Taxable Income | Tax Due |

|---|---|

| Not over ₱250,000 | 0% |

| Over ₱250,000 but not over ₱400,000 | 15% of the excess over ₱250,000 |

| Over ₱400,000 but not over ₱800,000 | ₱22,500 + 20% of the excess over ₱400,000 |

| Over ₱800,000 but not over ₱2,000,000 | ₱102,500 + 25% of the excess over ₱800,000 |

| Over ₱2,000,000 but not over ₱8,000,000 | ₱402,500 + 30% of the excess over ₱2,000,000 |

| Over ₱8,000,000 | ₱2,202,500 + 35% of the excess over ₱8,000,000 |

Revised Withholding Tax Table

| Monthly Taxable Compensation | Withholding Tax |

|---|---|

| Not over ₱20,833 | ₱0 |

| Over ₱20,833 but not over ₱33,332 | 15% of the excess over ₱20,833 |

| Over ₱33,333 but not over ₱66,666 | ₱1,875 + 20% of the excess over ₱33,333 |

| Over ₱66,667 but not over ₱166,666 | ₱8,541.80 + 25% of the excess over ₱66,667 |

| Over ₱166,667 but not over ₱666,666 | ₱33,541.80 + 30% of the excess over ₱166,667 |

| Over ₱666,667 | ₱183,541.80 + 35% of the excess over ₱666,667 |

The Impact of the Ease of Paying Taxes (EOPT) Act on Withholding

One of the biggest changes of the Ease of Paying Taxes (EOPT) Act is the updating of the time of withholding. The current BIR rules on withholding tax provide that the obligation to withhold arises once the income is payable, which is equivalent to due and demandable or enforceable by law. The same is also true if the income is already accrued or recorded in the payor’s books of accounts or if the income is already supported by a sales invoice issued by the seller. Therefore, it is important for businesses to realize that withholding is not a cash-based rule.

The EOPT Act also categorized taxpayers based on the size of the businesses and provided a more responsive approach for micro and small taxpayers. The new law also provided that withheld taxes are trust funds and should not be commingled with other company funds. The new law also provided that filing and payment of taxes are made easier by providing different filing and payment options for taxpayers.

Step-by-Step Guide to Calculating BIR Withholding Tax

Calculating BIR withholding tax correctly requires more than applying a percentage to an invoice. Businesses need to confirm when withholding applies, identify the correct Alphanumeric Tax Code (ATC), use the proper tax base, and record the transaction accurately. A structured process helps reduce errors, avoid vendor disputes, and support smoother tax compliance.

Step 1: Confirm the Nature of the Transaction and the Correct ATC

Before making any calculation, identify what the payment is for and determine whether it is subject to withholding tax under current BIR rules. For example, is the payment for rent, professional services, or janitorial services? Once you confirm the nature of the transaction, check the latest BIR ATC schedule for the correct code and rate. For certain rental payments, BIR still reflects WI100 for individuals and WC100 for corporations at a 5% rate. Because BIR may later modify or create ATCs through new issuances, businesses should always verify the current code before processing the payment.

Step 2: Confirm When the Withholding Obligation Arises

Under current EOPT rules, the obligation to withhold arises when the income has become payable. In BIR regulations, “payable” means the obligation is already due, demandable, or legally enforceable. The same rule also states that withholding may arise when the income payment is accrued or recorded as an expense or asset in the payor’s books, or when the seller issues the sales invoice or other adequate supporting document, whichever comes first. Because of this, businesses should avoid describing the rule as purely a cash basis.

Step 3: Establish the Correct Tax Base

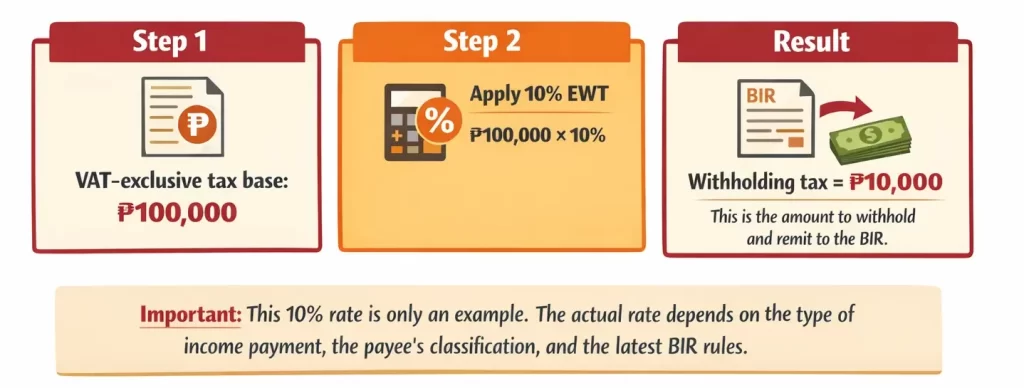

After confirming that withholding applies, determine the proper tax base. For many common VATable EWT transactions, the withholding tax is computed on the gross income payment exclusive of VAT. If the supplier issues a VAT-inclusive invoice, remove the VAT first before applying the withholding tax rate.

Example: If the invoice for professional services is ₱112,000 VAT-inclusive, divide the total by 1.12 to get the VAT-exclusive amount of ₱100,000. The VAT portion is ₱12,000. Businesses should still verify the specific rule for the transaction involved because not all withholding situations follow the same base.

Step 4: Apply the Withholding Tax Rate

Once you establish the correct tax base, apply the corresponding ATC rate.

Illustration:

Step 5: Compute the Net Amount Payable to the Supplier

After calculating the withholding tax, subtract it from the total invoice amount to determine how much cash you will actually release to the supplier.

Example:

₱112,000 – ₱10,000 = ₱102,000

In this case, the business pays the supplier ₱102,000 and remits ₱10,000 to the BIR. The payor should also issue the proper withholding tax certificate, such as BIR Form 2307, in line with BIR timing rules. As a rule, the withholding tax statement is furnished within 20 days from the close of the quarter, or simultaneously with payment upon the payee’s request.

Step 6: Record the Journal Entry Properly

Proper accounting supports accurate reporting, reconciliation, and alphalist preparation. Using the same example, the journal entry would be:

Debit: Professional Fees Expense — ₱100,000

Debit: Input VAT — ₱12,000

Credit: Expanded Withholding Tax Payable — ₱10,000

Credit: Cash in Bank / Accounts Payable — ₱102,000

Recording the transaction this way helps the general ledger reconcile with the related invoice, withholding tax return, and supporting certificate.

Common Pitfalls and Compliance Risks to Avoid

Even with established processes, businesses frequently fall into traps that trigger BIR audits and penalties. Recognizing these pitfalls is the first line of defence against tax liabilities.

- Timing Differences in Withholding: Historically, businesses struggled with the “accrual vs. payment” rule. While the EOPT Act has clarified that the obligation to withhold arises at the time the income has become payable, many businesses still mistakenly wait until actual cash disbursement to record the withholding tax, leading to late remittance penalties.

- Failure to Issue BIR Form 2307 Promptly: Withholding agents often delay the issuance of Form 2307 until the end of the quarter. This creates immense friction with suppliers who need these certificates to claim tax credits on their own quarterly income tax returns. Failure to provide this form can result in vendor disputes and administrative complaints.

- Mismatched Alphalist Data: The BIR uses the Quarterly Alphalist of Payees (QAP) to cross-check the withholding taxes you remitted against the tax credits claimed by your suppliers. Typographical errors in Tax Identification Numbers (TINs) or discrepancies in the reported amounts will immediately flag your company in the BIR’s computerized matching system.

- Applying the Wrong Tax Base: A frequent error among junior accountants is computing the withholding tax based on the gross invoice amount, inclusive of VAT. It must always be calculated on the net-of-VAT amount.

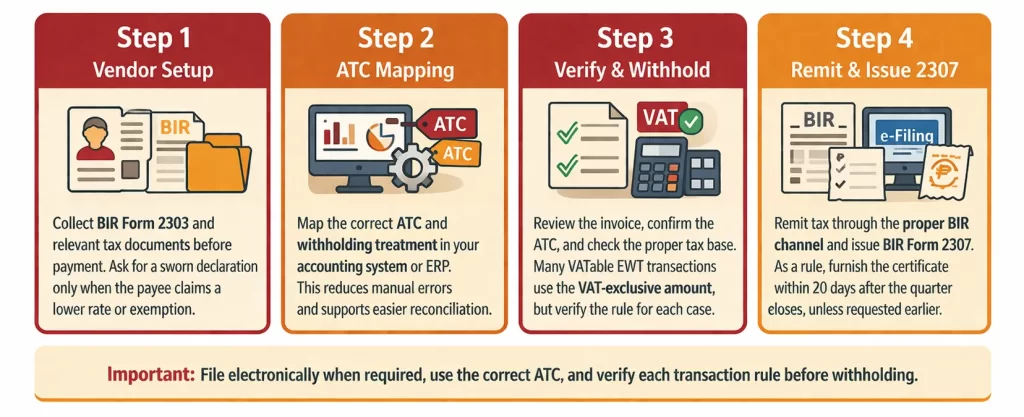

Step-by-Step Implementation Guide for Businesses

Transitioning from a theoretical understanding of withholding taxes to flawless execution requires a structured operational workflow. Here is a definitive implementation guide to ensure your business remains fully compliant as a withholding agent.

Industry-Specific Use Cases for BIR Withholding Tax

While the foundational rules of the BIR withholding tax system apply universally across all registered businesses, its practical application varies significantly depending on the industry. Different sectors encounter unique transaction types, requiring specialized knowledge of Alphanumeric Tax Codes (ATCs) and specific withholding tax rates.

| Industry | Common Transactions | Typical Withholding Tax Treatment | Key Compliance Challenge |

|---|---|---|---|

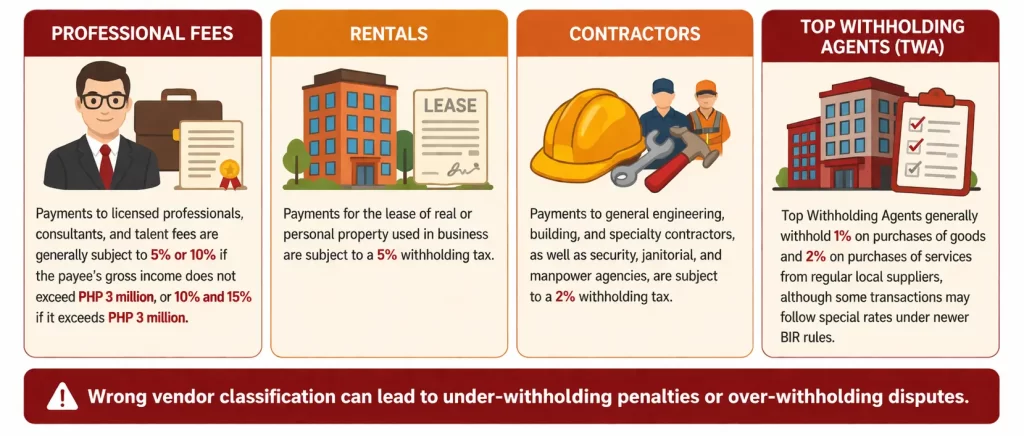

| Real Estate and Construction | Payments to prime contractors, subcontractors, and sales of real property by developers. | Local contractors are generally subject to 2% EWT. Progress billings require a deduction from the net amount, excluding VAT. Sales of real property may be subject to 1.5%, 3%, or 5% CWT depending on selling price and registration status. | Businesses need to handle progress billings, retention payables, and the correct CWT tier for property sales. |

| BPOs and Professional Services | Payments to consultants, IT specialists, freelancers, and other independent professionals. | Professional fees are typically subject to 5% or 10% for individuals and 10% or 15% for corporate consultants, depending on income thresholds. | Companies must track cumulative income to determine when a payee crosses the PHP 3 million threshold and becomes subject to the higher rate. |

| E-commerce and Retail Marketplaces | Gross remittances made by e-commerce platforms and digital financial service providers to online merchants. | Under RR No. 16-2023, platforms impose 1% creditable withholding tax on one-half of the gross remittances made to online merchants. | Platforms need payment systems that can automatically compute, deduct, and remit the tax before releasing funds to merchants. |

Conclusion

FAQ for BIR Withholding Tax

-

How much is withholding tax in the Philippines?

The Philippines does not apply one fixed withholding tax rate. The rate changes based on the type of income and transaction. For example, compensation withholding follows the current BIR withholding table, while some expanded withholding taxes apply rates such as 5% on certain rent, 2% on certain contractors, and 1% on one-half of certain e-marketplace remittances.

-

Who pays withholding tax, buyer or seller?

The payor usually withholds and remits the tax to the BIR. The income recipient usually bears the tax because the payor deducts it from the payment. In practice, the buyer or payor acts as the withholding agent, while the seller or payee receives the net amount.

-

Can you get withholding tax back?

Yes, taxpayers can recover excess creditable withholding tax through a tax credit or refund, if they properly report the income and prove the withholding. The law allows refunds when the withheld amount exceeds the tax due. Final withholding tax usually does not work the same way, unless an overpayment or error happened.

-

When must withholding tax be paid?

The deadline depends on the form. Employers generally file 1601-C on or before the 10th day of the following month for January to November, and on or before January 15 for December. Taxpayers generally remit 0619-E and 0619-F on or before the 10th day of the following month, then file 1601-EQ or 1601-FQ by the last day of the month after the quarter closes.