")

At the end of the month, many business owners find that their accounting records do not match their bank statement. This is a common issue for businesses of all sizes, from small shops to larger companies with many transactions. These differences are usually not serious, but they show that something needs to be reviewed and corrected.

Bank reconciliation is the process of comparing your financial records with your bank statement to identify and explain any differences. Its goal is to ensure your cash balance is accurate and reliable. When done regularly, it helps prevent errors, spot missing or duplicate transactions, and strengthen financial control. When ignored, small mistakes can grow into larger financial problems.

Key Takeaways

|

Breaking Down the Basics of Reconciling Your Bank

Bank reconciliation compares your accounting records with your bank statement to make sure they reflect the same cash balance. Differences happen because your books record transactions immediately, while the bank records them when they clear.

Bank reconciliation compares your accounting records with your bank statement to make sure they reflect the same cash balance. Differences happen because your books record transactions immediately, while the bank records them when they clear.

The process involves matching transactions and explaining any gaps. Some differences are normal, such as outstanding checks or deposits in transit. Others, like unknown charges, must be investigated and corrected.

Reconciliation is about understanding and fixing differences, not forcing numbers to match. The result is a reconciliation statement that shows an accurate cash balance you can trust for reporting and decision-making.

How It Differs from Other Financial Reconciliations

Bank reconciliation is one type of financial reconciliation, alongside accounts receivable, accounts payable, and balance sheet reconciliations. Each compares records to ensure balances are correct, but they serve different purposes and focus on different accounts.

What makes bank reconciliation unique is that it uses an independent third-party record: the bank statement. Because the bank’s records are separate from your own system, this comparison is especially useful for finding errors and detecting possible fraud. Internal reconciliations do not provide the same level of independent verification.

Bank reconciliation is also more time-sensitive than most other reconciliations. Since cash is the most easily misused asset, best practices require it to be checked more often usually monthly at minimum, and more frequently for businesses with many transactions.

Your First Line of Defense Against Financial Fraud

Bank reconciliation is one of the most important tools for preventing fraud, even though many business owners see it as just a routine bookkeeping task. In reality, it is a strong internal control that makes a business much harder to exploit. Companies that reconcile their bank accounts regularly are far less likely to miss suspicious or unauthorized transactions.

Bank reconciliation is one of the most important tools for preventing fraud, even though many business owners see it as just a routine bookkeeping task. In reality, it is a strong internal control that makes a business much harder to exploit. Companies that reconcile their bank accounts regularly are far less likely to miss suspicious or unauthorized transactions.

Most financial fraud relies on weak oversight and a lack of regular review. Bank reconciliation creates a consistent check between your records and the bank’s independent data. When done regularly and reviewed by the right person, it becomes difficult for fraudulent activity to go unnoticed for long.

1. Catching Suspicious Transactions Before It’s Too Late

Bank reconciliation only works as a fraud control if it is done carefully. Simply checking the final balance is not enough. A line by line comparison is what reveals suspicious activity that would otherwise go unnoticed.

Common issues caught through reconciliation include duplicate payments, unauthorized transfers, and fake vendors or employees. Duplicate payments show up when the same expense appears twice in your books but only once should appear on the bank statement. Unauthorized transfers are flagged when money leaves the bank account without a matching entry in your records.

Timing is critical. The faster a suspicious transaction is found, the more likely it can be disputed and recovered. Businesses that reconcile frequently detect fraud sooner and limit potential losses.

2. Warning Signs You Shouldn’t Ignore

Not every discrepancy you find during reconciliation indicates fraud, but certain patterns deserve particular attention. If you encounter any of the following, it warrants investigation beyond simple bookkeeping correction:

- Transactions with round numbers.

Fraudulent entries often involve round numbers because they are easier to fabricate quickly. A charge of exactly $5,000 or $10,000 with no clear corresponding purchase order or invoice should raise a flag.

- Frequent small charges from unfamiliar vendors.

Fraudsters sometimes prefer to make repeated small charges rather than one large one, betting that smaller amounts will attract less scrutiny. If you notice regular small debits from a vendor name you do not recognize, investigate the relationship between that vendor and whoever manages your accounts payable.

- Transactions just below approval thresholds.

Many organizations require additional authorization for expenditures above a certain amount. Transactions that cluster just below that threshold say, repeated charges of $4,950 in an organization where purchases above $5,000 require a second signoff are a classic red flag for internal control evasion.

- Unusual timing patterns.

Transactions processed on weekends, holidays, or late Friday afternoons can indicate that someone is taking advantage of reduced oversight during periods when management is less likely to be watching.

- Missing or voided checks in sequence.

If your check sequence shows gaps checks numbered 1045, 1046, 1047, then jumping to 1052 the missing checks deserve an explanation. This is particularly important for businesses that still use physical checks.

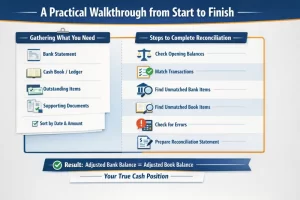

A Practical Walkthrough from Start to Finish

Understanding bank reconciliation conceptually is one thing; executing it reliably is another. The following walkthrough describes the process in practical terms, from gathering your materials to producing a completed reconciliation statement.

Understanding bank reconciliation conceptually is one thing; executing it reliably is another. The following walkthrough describes the process in practical terms, from gathering your materials to producing a completed reconciliation statement.

1. Gathering What You Need Before You Begin

Effective bank reconciliation starts with having the right materials in front of you. Trying to reconcile with incomplete records is one of the main reasons people find the process frustrating you end up chasing down missing information mid-process instead of working through a clean comparison.

Before you start, gather the following:

- Your bank statement for the period being reconciled.

This should cover a clearly defined date range — typically a calendar month — and show the opening balance, all transactions (deposits, withdrawals, fees, interest), and the closing balance. Most banks make statements available digitally within a day or two of the period end.

- Your cash book or general ledger cash account.

This is your internal record of all cash transactions for the same period. It should show the same opening balance as your previous reconciliation’s ending balance, plus all transactions recorded during the period.

- Any outstanding items from your previous reconciliation.

Outstanding checks, deposits in transit, and other items that were unresolved at the end of last period need to be brought forward and checked against this period’s bank statement to confirm whether they have now cleared.

- Supporting documents for any unusual transactions.

Check registers, wire transfer confirmations, receipt records, and bank deposit slips can all be useful for verifying specific entries during the reconciliation process.

One practical preparation step that many experienced accountants recommend is to sort your transactions in a consistent order before starting typically by date, then by amount within each date. This makes it much easier to match entries between the two records and spot items that appear on one side but not the other.

2. Following the Process Without Getting Lost

With your materials in hand, the reconciliation process itself follows a logical sequence. Here is a step-by-step approach that works for most business situations:

Step 1: Confirm opening balances. Your bank statement’s opening balance should match the closing balance from your previous period’s reconciliation. Your cash book’s opening balance should match as well. If either does not, something from the previous period was left unresolved and needs to be addressed before you proceed.

Step 2: Tick off matching transactions. Go through your bank statement and your cash book simultaneously, marking off transactions that appear in both records. A check you wrote for $1,200 that also appears as a $1,200 debit on your bank statement same date, same amount gets marked as matched on both sides. Work through the entire period this way.

Step 3: Identify unmatched items on the bank statement side. Transactions on your bank statement that have no corresponding entry in your books represent things your books are missing. These commonly include bank service fees, interest earned, direct debit payments you forgot to record, returned check fees, and electronic payments processed by the bank on your behalf. For each unmatched bank statement item, you will need to create a corresponding entry in your accounting records.

Step 4: Identify unmatched items on the books side. Transactions in your cash book that have no corresponding bank statement entry are typically timing differences. Outstanding checks issued but not yet cleared are the most common example. Deposits in transit funds you recorded when received but that had not yet posted to the bank account by the statement date are another. These do not require any adjustment to your records; they simply need to be listed on your reconciliation statement as reconciling items.

Step 5: Check for errors on both sides. As you work through the matching process, watch for transposed digits (recording $812 instead of $182), missing or extra zeros, and incorrect account coding. Errors in your books need to be corrected. If you believe the bank has made an error on their statement, that needs to be noted and reported to your bank promptly.

Step 6: Prepare the reconciliation statement. With all items accounted for, you can now prepare the formal reconciliation statement. This document brings both sides to an adjusted balance and confirms that those adjusted balances agree.

When the reconciliation is complete, the adjusted bank balance and the adjusted book balance should be identical. That matching figure is your true cash position as of the statement date.

The Hidden Mistakes That Break Your Bank Reconciliation

Even people who understand bank reconciliation in principle run into consistent trouble when they sit down to actually do it. Many of the most common problems fall into one of two categories: timing issues that look like errors but are not, and genuine mistakes that keep recurring because their root cause is never addressed.

Even people who understand bank reconciliation in principle run into consistent trouble when they sit down to actually do it. Many of the most common problems fall into one of two categories: timing issues that look like errors but are not, and genuine mistakes that keep recurring because their root cause is never addressed.

1. Timing Issues That Aren’t Actually Errors

Timing differences happen because your books record transactions immediately, while banks record them only after they clear. This is normal and does not mean something is wrong.

The most common examples are outstanding checks and deposits in transit. Checks may take days or weeks to clear after being recorded, and deposits made late in the day may appear on the bank statement the next business day. These items should be listed on the reconciliation, not removed from your records.

Problems arise when timing differences are ignored for too long or adjusted incorrectly. Any item still outstanding after 30 to 60 days should be reviewed, and items older than 90 days should be investigated and corrected if necessary.

2. The Slip-Ups That Keep Recurring

Beyond timing differences, certain categories of genuine errors tend to recur with remarkable consistency across organizations of all sizes. Recognizing these patterns can help you address their root causes rather than simply correcting each instance as it appears.

- Transposition errors

occur when digits are recorded in the wrong order (for example, 812 instead of 182). A common way to detect them is to divide the difference between balances by 9. If the result is a whole number, a transposition error is likely.

- Duplicate entries

happen when the same transaction is recorded twice, often due to both manual entry and bank feed imports. The fix is to remove the duplicate and prevent it by setting clear rules about who records transactions and when.

- Missed entries

are transactions that appear on the bank statement but were never recorded in the books. These usually include bank fees, interest income, wire charges, and returned item fees. Reviewing these categories helps ensure nothing is overlooked.

- Incorrectly classified transactions

do not affect the reconciliation balance but can distort financial reports and tax calculations. Examples include recording loan repayments or owner withdrawals as expenses. Reconciliation is the ideal time to find and correct these mistakes.

Finding the Right Frequency for Your Business

Monthly bank reconciliation is the minimum standard for most businesses because bank statements are issued monthly and it helps catch errors or suspicious activity within a reasonable time. For many small to mid-sized businesses, this schedule is sufficient and manageable.

Monthly bank reconciliation is the minimum standard for most businesses because bank statements are issued monthly and it helps catch errors or suspicious activity within a reasonable time. For many small to mid-sized businesses, this schedule is sufficient and manageable.

However, businesses with high transaction volumes may need to reconcile more often. Weekly reconciliation works well for operations like retail, restaurants, and e-commerce, where many transactions happen daily. It reduces the risk of problems going unnoticed for too long while keeping the workload reasonable.

Daily reconciliation is best for very high-volume or cash intensive businesses where fraud risk is higher and cash decisions are made daily. The right frequency depends on balancing the cost of staff time against the risk of undetected errors or fraud.

Conclusion

Bank reconciliation is a simple but powerful habit that keeps your finances accurate and secure. By regularly comparing your records with your bank statement, you can catch errors early, spot fraud before it grows, and always know your true cash position.

Whether you do it daily, weekly, or monthly depends on your business size but the key is doing it consistently. A few hours of careful review each period can save you from much bigger problems down the road.

FAQ About Bank Reconciliation

-

What is bank reconciliation and why is it important?

Bank reconciliation compares your accounting records with your bank statement to explain differences. It is important because it confirms your true cash balance and helps detect errors and fraud.

-

How often should a business perform bank reconciliation?

Monthly reconciliation is the minimum standard. Businesses with higher transaction volumes may need weekly or daily reconciliation to reduce the risk of undetected errors or fraud.

-

What is the difference between a deposit in transit and an outstanding check?

A deposit in transit is money recorded in your books but not yet shown on the bank statement. An outstanding check is a check recorded in your books but not yet cleared by the bank. Both are normal timing differences.

-

What should I do if my bank reconciliation doesn’t balance?

Recheck your calculations and look for transposition errors, duplicate entries, or missing transactions. Review outstanding items and compare records line by line if needed.

-

Who should be responsible for performing bank reconciliation?

The task should be done by someone knowledgeable in accounting and independent from daily cash handling and payment processing.

-

Can bank reconciliation be automated?

Yes. Accounting software can import bank data and match transactions automatically, but human review is still needed for unusual or unmatched items.

-

How long should bank reconciliation records be kept?

Records should generally be kept for five to seven years, depending on local tax and financial regulations.