Table of Contents

Every year, businesses lose billions to undetected fraud, duplicate payments, and regulatory penalties, often because their financial records were never properly verified. Behind most of these failures is the same root cause: a broken or neglected reconciliation process.

Finance teams today manage a fragmented ecosystem of payment gateways, digital wallets, multiple bank accounts, and disconnected enterprise systems. Without a structured way to verify that all of these moving parts agree with each other, even a well run business can be operating on flawed data without knowing it.

This article covers everything you need to know about transaction reconciliation: what it is, the different types, common challenges, a step by step process, and how modern tools are changing the way finance teams work.

Key Takeaways

|

What Is Transaction Reconciliation?

Transaction reconciliation compares two sets of financial records to ensure they align. It confirms that outgoing funds reflect actual spending and that incoming payments correspond to revenue the business has truly earned.

Beyond improving accuracy, reconciliation builds a clear audit trail that regulators and external auditors expect under standards such as SOX (Sarbanes-Oxley Act) and IFRS (International Financial Reporting Standards). More importantly, it gives finance leaders a dependable and current view of the company’s cash position.

Many organizations still face the pressure of a month-end close bottleneck, where finance teams spend long hours reconciling weeks of accumulated transactions. Increasingly, companies are shifting toward continuous accounting, allowing reconciliation to occur daily or even in real time. This transition calls for a solid understanding of the reconciliation lifecycle, common sources of discrepancies, and the right technology to manage the process efficiently at scale.

Deep Dive: Definitions and Core Concepts

To master transaction reconciliation, one must understand the fundamental mechanics that drive the process. It is not simply about checking off numbers, it is about verifying the integrity of the financial data supply chain.

1. Two-Way Match Concept

The two-way match is the most basic form of reconciliation. It compares an internal record, usually the General Ledger (GL), against an external source such as a bank statement. The objective is to confirm that every entry in one record has a corresponding entry in the other, and that the values agree.

When they do not match, the gap is usually caused by timing. For example, a check issued on the last day of the month may not appear on the bank statement until early the following month.

2. Three-Way Match Concept

that three documents align: the Purchase Order (PO), which outlines what the company ordered; the Goods Receipt Note (GRN), which confirms what the company actually received; and the Vendor Invoice, which states what the supplier is charging.

When the invoice amount matches the PO but the quantity differs from the GRN, the system immediately flags the discrepancy and places the payment on hold until the team resolves the issue. Many organizations embed this control directly into their accounts payable workflow to reduce the risk of overpayment and strengthen financial oversight.

3. Reconciliation Items

When two sets of data do not match, the resulting difference is called a “reconciliation item” or an “exception.” These items generally fall into three categories:

-

- Timing Differences: Transactions recorded in one period by the company but in a different period by the bank. For example, a check written on the 31st of January might not clear the bank until the 3rd of February.

- Permanent Differences: These are legitimate charges or credits that the company was unaware of until the statement arrived, such as bank service fees, interest earned, or penalties for insufficient funds. These require an adjusting journal entry to bring the GL into agreement with the bank.

- Errors: Mistakes on either side, such as entering $540 instead of $450, or posting a transaction twice. These require investigation and correction before the reconciliation can be closed.

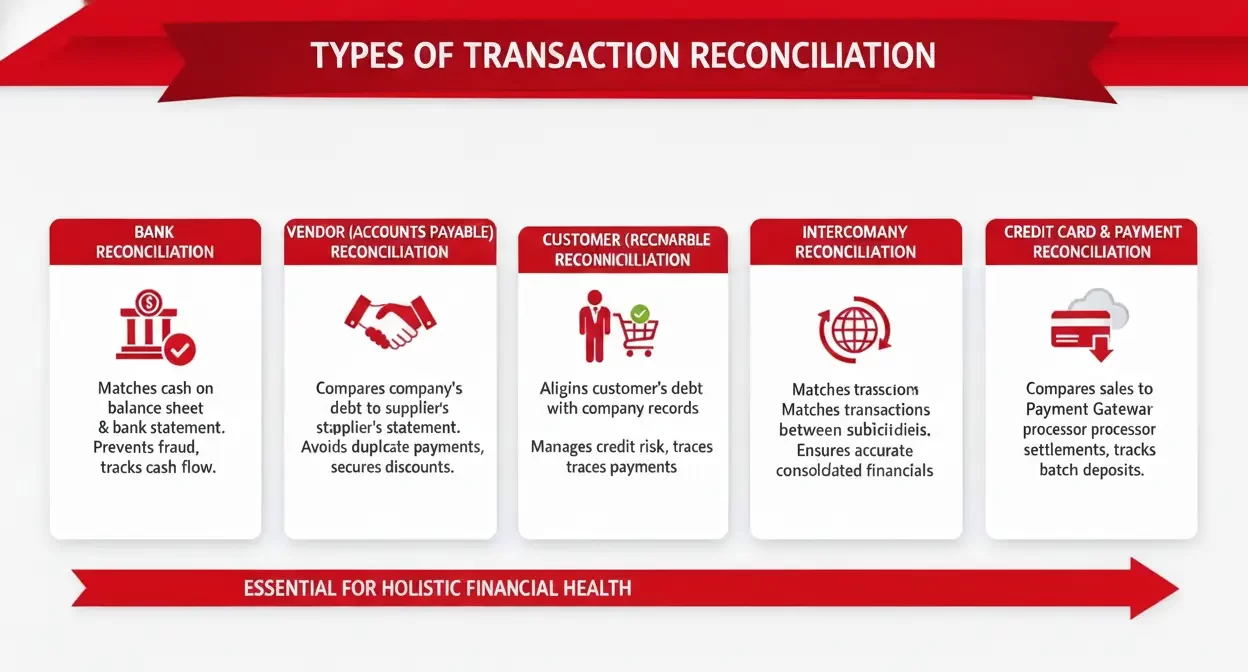

Types of Transaction Reconciliation

While bank reconciliation is the most well known, businesses must perform various types of reconciliation to ensure holistic financial health. Each type addresses a specific area of risk and operational flow.

1. Bank Reconciliation

This is the foundational process of matching cash balances on the balance sheet to the corresponding amount on the bank statement. Given that cash is the most liquid asset and the one most susceptible to fraud, high frequency bank reconciliation is essential. It identifies unauthorized withdrawals, ensures all deposits are credited, and highlights cash flow issues immediately.

2. Vendor (Accounts Payable) Reconciliation

Vendor reconciliation compares what the company believes it owes a supplier against what the supplier’s statement shows. Gaps often arise from missing invoices, credit notes that were not applied, or disputes about goods received. Running this regularly helps avoid duplicate payments and ensures the company does not miss early payment discounts.

This process is closely connected to broader vendor management practices that govern how supplier relationships are maintained.

3. Customer (Accounts Receivable) Reconciliation

On the revenue side, companies need to reconcile what they believe customers owe against what those customers believe they owe. If a customer insists they paid an invoice the company still shows as outstanding, reconciliation traces where the payment went. It may have been applied to the wrong account, or the customer may be mistaken.

Keeping AR records accurate is essential for calculating bad debt reserves and managing credit risk. It is also a core part of sound accounts receivable management.

4. Intercompany Reconciliation

For multinational corporations or entities with multiple subsidiaries, intercompany reconciliation is a massive undertaking. It ensures that transactions between two branches of the same parent company match. For instance, if Subsidiary A records a sale to Subsidiary B, Subsidiary B must record a corresponding purchase. If these do not eliminate each other during financial consolidation, the parent company’s financial statements will be inaccurate. Currency exchange rate fluctuations often add a layer of complexity to this process.

5. Credit Card and Payment Gateway Reconciliation

For retailers and e-commerce businesses, this type is often the most time-consuming. Sales records from the point-of-sale system or online storefront need to be matched against the settlement reports from payment processors such as Stripe, PayPal, or merchant banks.

The complication is that processors typically deposit funds in daily or weekly batches, after deducting their fees, rather than passing through individual transaction amounts. Matching those batch deposits back to individual sales requires careful logic to separate gross revenue from processing costs.

Quantifiable Benefits of Robust Reconciliation

A well run reconciliation process does more than keep the books accurate. It has direct, measurable effects on a company’s financial health and day to day operations.

1. Earlier Fraud Detection

According to the Association of Certified Fraud Examiners, organizations lose an estimated 5% of their annual revenue to fraud. A strong reconciliation process serves as one of the most effective controls for detecting fraud early. When finance teams regularly compare internal records with external statements, they can spot unusual activity such as duplicate payments, transactions involving unfamiliar vendors, or unauthorized transfers before losses escalate. The sooner teams identify a discrepancy, the higher the likelihood of recovering the funds.

2. Stronger Compliance and Audit Readiness

Companies operating in regulated industries or listed on public exchanges must demonstrate the accuracy of their financial records and the strength of their internal controls. A well-maintained reconciliation history provides clear evidence that teams have reviewed account balances and thoroughly investigated exceptions. This documentation not only supports compliance but also streamlines the audit process and reduces the risk of findings or financial penalties.

For teams managing the financial close, maintaining accurate and up-to-date reconciliation records throughout the reporting period significantly eases month-end and year-end pressure. Instead of scrambling to resolve accumulated discrepancies, they can focus on analysis and reporting with greater confidence.

3. Optimized Cash Flow Management

Without reconciliation, a company only knows its “book balance,” meaning what its own records show. That figure can differ meaningfully from what is actually in the bank, because of outstanding checks, pending deposits, or unrecorded charges.

Reconciling regularly closes that gap. The treasury team knows exactly what has cleared and what is still in transit, which allows for more confident decisions about payment timing, short-term investments, and cash reserves.

4. Improved Supplier and Customer Relationships

Billing errors and payment disputes put strain on business relationships. A supplier who repeatedly receives late or incorrect payments will eventually offer less favorable terms. A customer who is chased for an invoice they already paid loses confidence in the company’s operations.

Regular reconciliation keeps the accounts payable and accounts receivable ledgers current, which means problems are caught and corrected before they reach the point of a difficult conversation.

Challenges in the Reconciliation Process

Despite its importance, transaction reconciliation remains a pain point for many finance departments. Several structural and operational hurdles make the process difficult to execute efficiently.

1. Data Stored Across Multiple Systems

A typical enterprise runs on several different platforms at once. Sales data lives in the CRM, the general ledger is in the ERP, payroll is in an HR system, and cash data is spread across multiple bank portals. These systems rarely share data in a compatible format.

Finance teams often have to export files from each source separately, reformat them, and piece them together manually before any matching can begin. This fragmentation is one of the main reasons companies invest in ERP system integration.

2. Volume and Velocity of Transactions

A process that works at 100 transactions per month will not work at 10,000. As businesses grow, the volume and speed of incoming transactions often outpaces the team’s ability to reconcile them manually. By the time a manual reconciliation run is finished, new transactions have already arrived, making it impossible to maintain an accurate, real time view.

3. Timing Gaps Between Records

Records from different sources do not always capture the same transaction at the same time. A payment made on the 30th of the month may not appear on the bank statement until the 2nd of the following month. At year-end or quarter-end, these timing gaps become especially problematic, because accountants must determine whether an unmatched item is a genuine error or simply a transaction that has not settled yet.

4. Human Error in Manual Processes

Spreadsheet-based reconciliation is inherently error-prone. Research suggests that nearly 90% of spreadsheets contain at least one mistake. In reconciliation, a single transposed digit or a broken formula can take hours to track down.

There is also a knowledge risk. When the team member who understands how a particular vendor account works leaves the company, that knowledge often leaves with them, and the reconciliation for that account can stall.

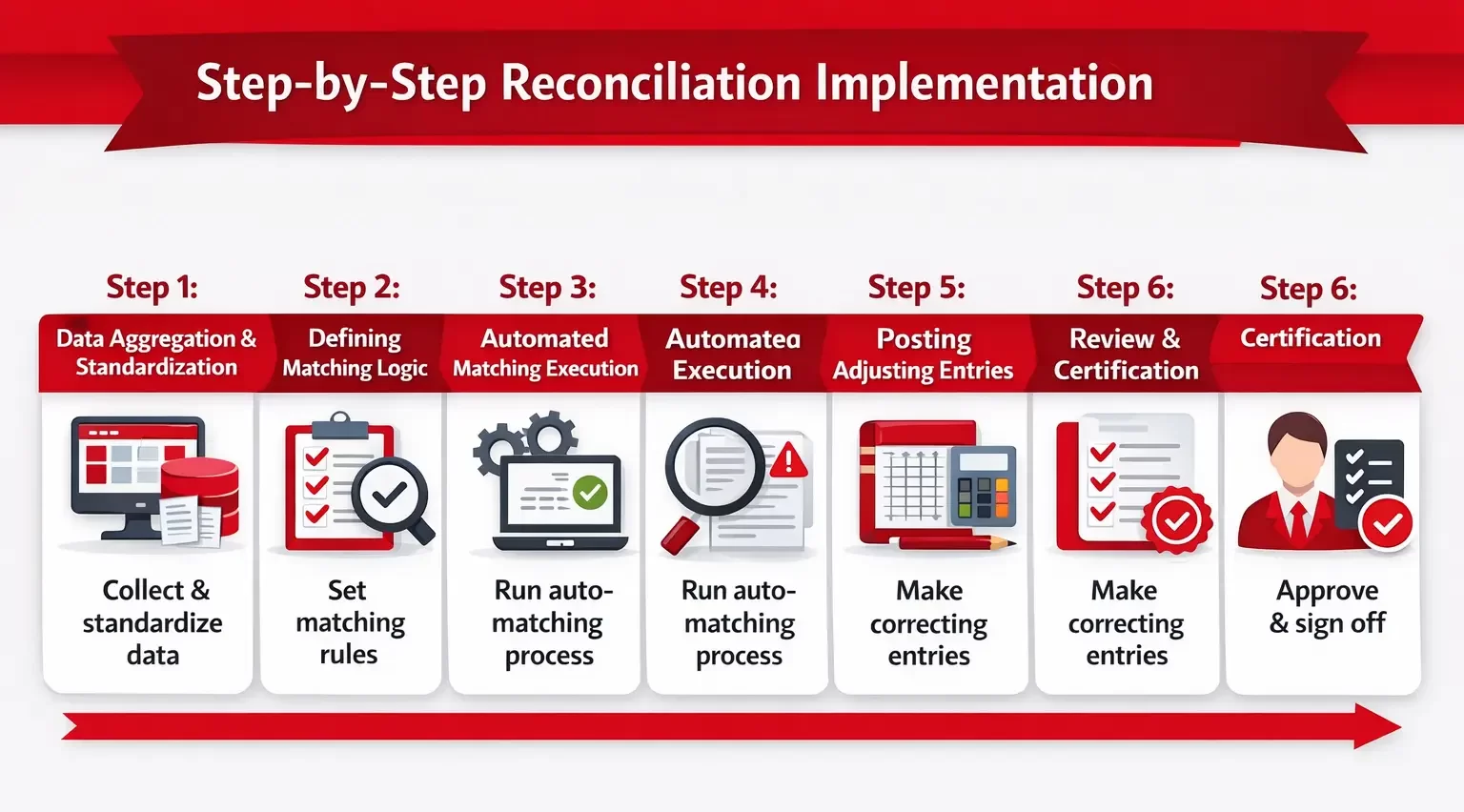

Step-by-Step Implementation Guide

Establishing a world class reconciliation framework requires a structured approach that combines policy, process, and technology. Here is a guide to implementing an effective transaction reconciliation system.

Step 1: Data Aggregation and Standardization

The first step is to gather data from all relevant sources. This includes internal ledgers and external statements. The challenge lies in standardization. Dates may be formatted differently (MM/DD/YYYY vs DD/MM/YYYY) and descriptions may vary. Implementing a data transformation layer or using software that can parse various file formats is essential to ensure that “apples are being compared to apples.”

Step 2: Defining Matching Logic

Finance teams must establish the rules for matching.

- Perfect Match: Reference number and amount match exactly.

- Tolerances: Allow matches where the amount differs by a small threshold—e.g., less than $0.05—to account for rounding errors.

- One-to-Many: Matching one bank deposit to multiple invoices.

- Many-to-One: Matching multiple credit card swipes to a single batch settlement.

Defining these rules upfront allows for automation to handle the bulk of the volume.

Step 3: Automated Matching Execution

With the rules in place, run the matching process. In a manual workflow, this means comparing line items one by one in a spreadsheet. In an automated system, the software applies the rules to both data sets simultaneously.

A well configured system typically auto-matches between 80% and 90% of transactions, leaving only exceptions for human review.

Step 4: Investigate Exceptions

Unmatched items must be investigated. The discrepancy could stem from a bank fee, a missing invoice, or even a fraudulent charge. Each exception requires careful review to determine the root cause and appropriate corrective action. The investigation process should be documented, with comments and attachments added to the reconciliation record to support the resolution.

Step 5: Posting Adjusting Entries

Once the cause of a discrepancy is identified, the general ledger must be updated. If the bank shows a service charge that is not in the books, a journal entry must be posted to expense that charge and reduce the cash account. This step ensures that the GL reflects the true financial position.

Step 6: Review and Certification

The final step is the governance layer. A controller or manager must review the reconciliation, ensure that all significant exceptions have been resolved or explained, and sign off on the account. This certification is crucial for internal controls and audit purposes.

Industry-Specific Use Cases

While the principles of reconciliation are universal, the application varies significantly across different sectors.

1. Retail and E-commerce

The main challenge for retailers is volume. A single day of trading can generate thousands of individual transactions across multiple payment methods and sales channels. Each payment method, whether it is a credit card, digital wallet, or buy-now-pay-later service, settles at a different time and at a different net amount after fees are deducted.

Reconciliation tools designed for retail apply “gross-to-net” logic. They take the raw settlement file from the payment processor, subtract the processor’s fees, and match the net figure against what arrived in the bank.

Returns, chargebacks, and gift card redemptions each require separate handling, adding further layers to the process.

2. Manufacturing and Logistics

In manufacturing, reconciliation closely connects to supply chain operations. Finance and procurement teams rely heavily on the three-way match (PO, Receipt, and Invoice) to maintain control over payments and inventory. Discrepancies often occur when vendors deliver only part of an order but invoice the full amount, or when goods sustain damage during transit.

Logistics companies also face complex reconciliation regarding fuel surcharges and freight rates, which often fluctuate between the time of booking and the time of billing.

3. SaaS and Subscription Businesses

Subscription businesses must manage recurring billing alongside revenue recognition requirements under ASC 606. For example, a customer may pay $1,200 upfront for an annual subscription. Although the company receives the cash immediately, it must recognize the revenue gradually at $100 per month over the contract period.

In this model, finance teams must match the cash receipt to the deferred revenue account and monitor the revenue recognition schedule to ensure accuracy over time. Failed renewals and involuntary churn, such as payments declined due to expired credit cards, add further complexity and increase the volume of reconciliation exceptions.

Manual vs. Automated Reconciliation: Which Is Right for You?

| Aspect | Manual Spreadsheet | Native ERP | Dedicated Software |

| Best For | Low volume | Growing firms | High complexity |

| Automation | Manual | Partial | Advanced |

| Error Risk | High | Moderate | Low |

| Scalability | Limited | Moderate | High |

The best approach depends on transaction volume, the number of data sources involved, and the level of risk the organization is willing to accept from manual errors. As transaction complexity increases, businesses must carefully evaluate whether manual processes can still provide the speed and control they require.

1. Manual Spreadsheet

Spreadsheets are a reasonable starting point for small businesses with straightforward banking and low transaction volumes. They are inexpensive, familiar to most finance staff, and flexible enough to handle simple matching tasks.

The limitations become apparent as the business grows. Spreadsheets have no built-in version control, no audit trail, and no way to automatically import data from external sources. A single broken formula or accidental overwrite can introduce errors that are difficult to find and time-consuming to correct.

2. Native ERP Modules

Most ERP systems include a reconciliation module as part of the standard package. Because these tools connect directly to the General Ledger, they eliminate the need to export and re-import internal data. They are a meaningful step up from spreadsheets for businesses already running on an ERP.

The limitation is integration. Native modules often struggle to connect cleanly with external data sources such as third-party payment processors or banks that use formats the ERP does not support. When that happens, teams typically fill the gap with manual exports, which reintroduces many of the same risks as spreadsheet-based work.

3. Dedicated Reconciliation Software

Specialized reconciliation tools handle complexity at scale. These systems import data from virtually any format, apply advanced matching logic to address inconsistencies in transaction descriptions, and automatically post journal entries once they confirm a valid match. By reducing manual intervention, they allow finance teams to focus on exception handling and analysis rather than routine matching.

The upfront investment is higher, but the return comes through faster closes, lower staffing costs, and fewer errors. A broader accounting software comparison can help identify the right fit for the organization’s size and industry.

Future Trends: The Evolution of Reconciliation (2026 Onwards)

The field of accounting is undergoing a technological renaissance, and reconciliation is at the forefront of this change.

1. From Periodic to Continuous Accounting

The traditional “month-end close” is disappearing. Future-ready finance teams are moving toward a continuous close model, where reconciliation happens automatically as transactions occur. This eliminates the end-of-month crunch and provides real-time financial intelligence.

2. Artificial Intelligence and Machine Learning

AI is transforming how finance teams perform transaction matching. Traditional rules based systems often struggle when data lacks consistency. For example, a ledger may record a vendor as “FedEx,” while the bank statement lists “Federal Express Services.” A rigid rule may fail to connect the two.

Machine learning models analyze historical human decisions and recognize patterns in how teams resolve discrepancies. Over time, the system improves its ability to match transactions accurately, even when descriptions vary. In addition, AI can identify seasonal trends and predict when specific reconciliation items are likely to appear, allowing teams to address potential issues proactively.

3. Blockchain and Immutable Ledgers

Blockchain technology promises to reduce the need for reconciliation significantly. If two companies share a distributed ledger, a transaction recorded by one is instantly and immutably recorded by the other. While widespread adoption is still years away, the concept of a “single shared source of truth” could eventually render intercompany and vendor reconciliation obsolete.

Common Pitfalls and Mitigation Strategies

Even with powerful ERP software, reconciliation projects can fail. Understanding common pitfalls allows project leaders to proactively mitigate risks.

1. The “Garbage In, Garbage Out” Paradigm

The most common cause of reconciliation failure is poor data quality. If the reference numbers entered by the Accounts Payable team do not match the reference numbers on the bank statement, the system cannot match them.

Mitigation: Enforce strict data entry standards. Use input masks on ERP fields to ensure invoice numbers follow a specific format. Implement “OCR (Optical Character Recognition)” technology to scan vendor invoices, reducing manual data entry errors.

2. Over-Automation and False Positives

In their effort to automate as much as possible, teams sometimes design matching rules that are too broad. For instance, relying only on the “Amount” field without validating the “Date” or “Reference” can create false positives. In such cases, the system may match a payment for Vendor A with an invoice for Vendor B simply because the amounts are identical. While automation improves speed, poorly designed rules can undermine accuracy.

Mitigation: Implement multi factor matching logic. A match should only occur if at least two or three criteria align (e.g., Amount AND Date AND Vendor Name). Regularly audit auto-matched transactions to ensure accuracy.

3. Ignoring the Human Element

Automation handles routine transactions effectively, but it cannot interpret every anomaly. Organizations that fail to equip their staff with the skills to investigate and resolve exceptions often see their “unmatched” queue grow over time. As unresolved items accumulate, they slow down the financial close and increase operational risk.

Mitigation: Shift the role of the finance team from “data entry” to “data analysis.” Provide training on how to trace transactions through the ERP, how to access bank portals for detailed transaction descriptions, and how to communicate effectively with vendors regarding discrepancies.

Conclusion

Transaction reconciliation is one of the most important processes in finance, precisely because it sits underneath everything else. When it works well, financial statements are reliable, audits are manageable, and decisions are based on accurate data. When it breaks down, the effects show up across the entire finance function.

The good news is that the tools available today make accurate, timely reconciliation achievable at any scale. Moving away from manual processes is no longer a question of whether it is possible, but of choosing the right approach for the organization’s size and complexity.

For organizations evaluating where to start, exploring the best accounting software options available in the Philippines can provide a practical foundation for selecting tools that support reconciliation at scale.

FAQ

-

What is the difference between reconciliation and matching?

Matching is the specific action of comparing two individual transaction lines to see if they correspond. Reconciliation is the broader process that includes matching, investigating discrepancies, making adjusting entries, and validating the final account balance.

-

How often should transaction reconciliation be performed?

Ideally, finance teams should perform bank reconciliation daily to maintain real time visibility over cash and detect potential fraud early. For lower volume accounts or less critical sub ledgers, teams typically adopt a weekly or monthly schedule based on materiality and risk.

-

What happens if the adjusted bank balance does not equal the adjusted book balance?

If the balances do not match after adjustments, it indicates an unresolved error. The finance team must investigate further to identify discrepancies such as transposition errors, missing transactions, or duplicate entries.