For many Sdn Bhd directors in Malaysia, reporting issues often arise when auditors ask why the company uses one standard instead of another. MPERS vs MFRS becomes an important comparison because each choice affects how goodwill, investment property, borrowing costs, and financial instruments are recorded.

According to the IFRS Foundation, private entities in Malaysia have been able to use the Malaysian Private Entities Reporting Standard (MPERS) or Malaysian Financial Reporting Standards (MFRS) since 1 January 2016, while PERS has been replaced by MPERS.

Understanding the difference helps finance managers and business owners choose a more suitable standard before audit, consolidation, first-time adoption, or accounting system changes.

Key Takeaways

|

Reliable reporting starts with clean accounting data. When MPERS or MFRS affects amortisation, revaluation, consolidation, or transition records, the right accounting software helps finance teams keep those details organised before audit review.

What Are MPERS and MFRS?

MPERS and MFRS are accounting standards and reporting principles issued by the Malaysian Accounting Standards Board (MASB) to guide how Malaysian companies prepare financial statements. Malaysian companies use them to prepare financial statements under the Companies Act 2016, depending on whether the company qualifies as a private entity or has public accountability.

Malaysian Private Entities Reporting Standards (MPERS)

Malaysian Private Entities Reporting Standards (MPERS) is issued by the Malaysian Accounting Standards Board (MASB) for private entities. Effective from 1 January 2016, it replaced Private Entities Reporting Standards (PERS) and contains 35 sections based on IFRS for SMEs, with Malaysia-specific guidance such as MASB 32.

Malaysian Financial Reporting Standards (MFRS)

Malaysian Financial Reporting Standards (MFRS) is used by entities with public accountability, such as listed companies, banks, insurers, takaful operators, Capital Markets and Services Licence holders, and development financial institutions. It is fully aligned with International Financial Reporting Standards issued by the International Accounting Standards Board (IASB).

Who Should Use MPERS and Who Must Use MFRS?

The choice between MPERS and MFRS depends on whether a company qualifies as a private entity or has public accountability. For business owners, the key point is not only whether the company is listed, but also whether it is connected to a group that must follow MFRS.

| Malaysian Private Entities Reporting Standards (MPERS) | Malaysian Financial Reporting Standards (MFRS) |

|

|

The condition that often causes confusion is subsidiary status. A Sdn Bhd may look like a private company on its own, but if it is a subsidiary, associate, or jointly controlled by a listed parent company or another entity regulated by the Securities Commission Malaysia or Bank Negara Malaysia, it may not qualify for MPERS.

This means the company’s group structure matters as much as its own legal status. Before choosing MPERS, business owners should check whether the company is connected to a parent, investor, or regulated entity that already uses MFRS.

Key Differences Between MPERS and MFRS

MPERS and MFRS share the same broad reporting purpose, but they differ in complexity, measurement choices, and disclosure depth. In practice, the difference affects how a company consolidates subsidiaries, recognises goodwill, measures investment property, treats borrowing costs, and classifies financial instruments.

| Area | MPERS | MFRS |

|---|---|---|

| Control of subsidiaries | Based on power to govern financial and operating policies | Uses a 3-element test covering power, exposure to variable returns, and ability to affect returns |

| Goodwill | Amortised over useful life, with a maximum of 10 years | Not amortised, but tested for impairment annually |

| Investments in associates and joint ventures | Allows equity method, cost model, or fair value model | Uses equity method only |

| Financial instruments | Uses 2 measurement models | Uses 4 measurement models |

| Investment property | Fair value model required unless fair value cannot be measured reliably | Choice between fair value model and cost model |

| Borrowing costs | Expensed in profit or loss | Capitalised when directly attributable to a qualifying asset |

| Intangible assets | Finite useful life only, no revaluation, and all research and development costs expensed | May have indefinite useful life, revaluation is permitted, and development costs may be capitalised when criteria are met |

| Recycling of foreign exchange reserve | Not permitted on disposal of foreign operation | Permitted on disposal of foreign operation |

| Leases | No bright-line threshold for classification | Follows MFRS 16 with a right-of-use asset model |

Control of Subsidiaries

MPERS defines control by the power to govern another entity’s financial and operating policies. MFRS uses a broader test covering power, variable returns, and the ability to affect those returns. This can change which entities must be included in consolidated financial statements.

Goodwill Treatment

Under MPERS Section 19, goodwill is amortised over its useful life, with a maximum of 10 years if the period cannot be estimated. Under MFRS, goodwill is not amortised but tested for impairment every year, which can create larger losses when value declines.

Investment Property

MPERS Section 16 generally uses fair value for investment property when it can be measured reliably, with changes going to profit or loss. MFRS allows either fair value or cost model, giving companies more policy choice.

Borrowing Costs

Under MPERS Section 25, borrowing costs are expensed immediately. Under MFRS, borrowing costs linked to qualifying assets can be capitalised, which affects early profit and asset value.

Financial Instruments

MPERS Section 11 and Section 12 use simpler measurement rules for basic receivables, payables, loans, and simple investments. MFRS is more detailed and better suited for complex treasury, hedging, derivatives, or investment portfolios.

MPERS vs PERS: Why the Historical Shift Matters

MPERS replaced the older Private Entities Reporting Standards (PERS), which was based on IAS-era standards and had not been updated since 1 January 2006. The shift made private entity reporting in Malaysia more current through statement of comprehensive income, removal of extraordinary items, and clearer disclosures for judgements and related party transactions.

It also changed key treatments such as non-controlling interest and leases. Non-controlling interest is no longer treated as an expense in profit or loss, while lease classification now depends on the substance of the arrangement instead of fixed 75% or 90% bright-line thresholds.

First-Time Adoption and What Companies Need to Prepare

For first-time adoption under MPERS Section 35, companies need to prepare these key items:

- First-time adopter status: Confirm whether this is the company’s first financial statement that fully complies with Malaysian Private Entities Reporting Standards (MPERS).

- Date of transition: Set the correct transition date before preparing the opening financial position.

- Opening statement: Prepare an opening statement of financial position based on MPERS requirements.

- Transition impact: Explain how the change affects financial position, performance, and cash flows.

- System readiness: Use accounting software in Malaysia to keep transition records, adjustments, and reporting data easier to manage.

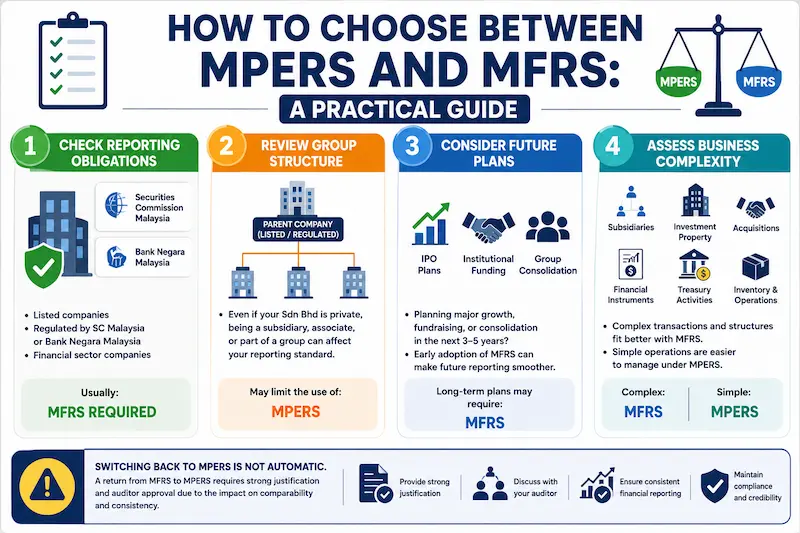

How to Choose Between MPERS and MFRS: A Practical Guide

Check Whether the Company Has Public Accountability

Choosing between MPERS and MFRS starts with the company’s reporting obligation. If the company is listed, regulated by the Securities Commission Malaysia or Bank Negara Malaysia, or operates in a regulated financial sector, MFRS is usually required.

Review the Company’s Group Structure

Check the group structure. A Sdn Bhd may look private, but if it is a subsidiary or associate of a listed or regulated entity, MPERS may not be available because the parent company’s reporting requirements can affect the subsidiary.

Consider Future Funding or IPO Plans

Future plans also matter. Companies planning an IPO, institutional funding, or group consolidation within the next 3 to 5 years may benefit from adopting MFRS earlier. Companies with simpler operations and no such plans may find MPERS more practical.

Match the Standard with Transaction Complexity

Transaction complexity should be reviewed as well. MFRS is more suitable for businesses with subsidiaries, investment properties, acquisitions, complex financial instruments, or treasury activities. MPERS is usually easier for companies with basic receivables, payables, loans, inventory, and standard operations.

A private entity that has adopted MFRS should not assume it can freely return to MPERS. Any switch back usually needs strong justification and auditor agreement because it affects reporting consistency.

The Impact on Your Accounting System

Choosing MPERS or MFRS affects how the accounting system handles amortisation, revaluation, financial instruments, and borrowing costs. MPERS may need goodwill amortisation schedules and fair value updates, while MFRS may require more flexible classification and project-level tracking for qualifying assets.

The selected standard should match the system’s capability. If reporting involves consolidation, revaluation, amortisation, or project-level cost tracking, financial reporting software should help keep records consistent without relying too much on manual adjustments.

Conclusion

Choosing a reporting standard is not only about meeting audit requirements. It also affects how management reads business performance, prepares for growth, and explains financial results to shareholders, lenders, or future investors.

For Malaysian companies, the safer choice is the one that fits both the current company structure and the direction of the business. A standard that feels simple today may create more work later if the company plans to consolidate, raise funding, or handle more complex transactions.

If the decision is still unclear, a free consultation can help finance teams review their reporting needs, system readiness, and audit expectations before committing to MPERS or MFRS.

FAQ About MPERS in Malaysia

-

Is MPERS mandatory for all Sdn Bhd companies in Malaysia?

Malaysian Private Entities Reporting Standards (MPERS) apply to private companies that are not required to lodge financial statements with the Securities Commission Malaysia or Bank Negara Malaysia, and are not subsidiaries of regulated entities. However, a private company may choose Malaysian Financial Reporting Standards (MFRS) voluntarily. The old Private Entities Reporting Standards (PERS) can no longer be used since MPERS became effective.

-

What is the main difference between MPERS and MFRS in simple terms?

Malaysian Private Entities Reporting Standards (MPERS) is a simpler framework for private companies. Malaysian Financial Reporting Standards (MFRS) is the full framework used by public accountability entities. The biggest differences usually appear in goodwill, financial instruments, investment property, and borrowing costs.

-

Can a company switch from MPERS to MFRS?

Yes, a company can switch from Malaysian Private Entities Reporting Standards (MPERS) to Malaysian Financial Reporting Standards (MFRS). Moving back from MFRS to MPERS is much more limited and usually needs strong justification. The company should discuss the change with its auditor because it may affect comparability and restatement of financial statements.

-

When did MPERS become effective in Malaysia?

Malaysian Private Entities Reporting Standards (MPERS) became effective for annual financial statements beginning on or after 1 January 2016. Earlier application was also permitted.

-

Does MPERS apply to sole proprietors or partnerships?

No. Malaysian Private Entities Reporting Standards (MPERS) apply to private companies incorporated under the Companies Act 2016. Sole proprietors and partnerships follow different reporting requirements based on their business structure.

-

How many sections are in MPERS?

Malaysian Private Entities Reporting Standards (MPERS) contains 35 sections. These sections cover key areas of financial reporting for private entities, including financial statements, revenue, property, plant and equipment, financial instruments, related party transactions, and other accounting treatments.

-

What happens if a private company applies the wrong accounting standard?

Using the wrong accounting framework can create audit issues and may affect whether the financial statements are considered properly prepared. It can also affect credit assessment, investor due diligence, and compliance under the Companies Act 2016. If the company is part of a listed or regulated group, the mistake may also affect consolidation at parent company level.