Effective cash outflow tracking is just as vital as monitoring revenue within a complex corporate finance ecosystem. As organizations scale, many businesses struggle to distinguish between key financial terms like disbursement vs reimbursement due to overlapping transaction types. While both processes involve payments, they require fundamentally different accounting treatments, operational workflows, and tax implications to maintain financial accuracy.

Distinguishing between these two payment methods is essential for ensuring regulatory compliance and precise financial reporting. Proper classification prevents skewed profit and loss statements and avoids costly complications during tax audits, specifically regarding Value Added Tax (VAT) or Goods and Services Tax (GST) treatments.

This guide provides a comprehensive framework to manage corporate outflows by understanding their unique accounting entries and structural differences.

Key Takeaways

|

Understanding the Core Concepts of Cash Outflows

To establish a solid foundation, it is essential to define what each term means within the strict context of corporate accounting. Both terms represent a transfer of funds from a corporate entity to another party, but the nature of the underlying obligation dictates how the transaction is classified.

What is a Disbursement?

A disbursement is the direct transfer of funds from a company’s account to a specific recipient. In business, this process is used to settle debts, purchase assets, or distribute profits to stakeholders. It serves as the primary way company deploy cash reserves to maintain daily operations and fund strategic growth.

The defining characteristic of a disbursement is that the company is the principal entity initiating the payment for its own direct benefit or obligation. The funds are moving outward to satisfy a corporate liability. Common examples of corporate disbursements include:

- Vendor Payments: Settling invoices for raw materials, SaaS subscriptions, or professional services.

- Payroll: The distribution of salaries, wages, and bonuses to the workforce.

- Dividend Payments: The distribution of a portion of the company’s earnings to its shareholders.

- Loan Drawdowns: The release of funds from a lender to a borrower.

- Capital Expenditures (CapEx): CapEx purchasing fixed assets such as machinery, real estate, or company vehicles.

In each of these scenarios, the company is directly liable for the expense. The disbursement simply represents the mechanical transfer of cash to extinguish that liability.

What is a Reimbursement?

A reimbursement is a specific payment process used to compensate individuals for out-of-pocket expenses incurred for business purposes. This transaction restores personal funds, ensuring that anyone who uses their own resources on behalf of the company is fully repaid. Efficiently managing these claims helps organizations maintain financial accuracy while tracking indirect corporate spending.

The defining characteristic of a reimbursement is the presence of an intermediary who acts on behalf of the company. The initial transaction occurs between the employee (or agent) and a third-party vendor. The subsequent transaction occurs between the company and the employee. Common examples of corporate reimbursements include:

- Travel and Entertainment (T&E): Repaying an employee for flights, hotel accommodations, and meals incurred during a business trip.

- Office Supplies: Compensating an office manager who used a personal credit card to buy emergency printer ink.

- Mileage: Paying an employee a standard rate per mile driven in their personal vehicle for business purposes.

- Medical Reimbursments: Specialized corporate health plans where employees pay for medical services upfront and submit claims to the employer.

In a reimbursement scenario, the company did not directly transact with the hotel or the airline, it is transacting with the employee to cover the legitimate business expense that the employee facilitated.

Disbursement vs Reimbursement: The Fundamental Differences

While the end result of both processes is a reduction in corporate cash, the journey of those funds and the legal relationships involved vary significantly. Finance teams must recognize these differences to ensure accurate financial modeling and compliance.

1. The Principal-Agent Relationship

The most crucial distinction lies in the legal relationship between the parties involved. In a standard disbursement, the company acts as the principal. It enters into a direct contract with a supplier, receives an invoice in its own name, and pays that invoice directly. There is no middleman.

In a reimbursement, an employee acts as a company agent by paying third parties directly using personal funds. Before issuing repayment, the business must verify that these out-of-pocket expenses align with corporate policy and authorized spending.

2. Timing of the Cash Outflow

The timing of the financial obligation also differs. Disbursements are typically proactive or scheduled based on agreed-upon credit terms (e.g., Net 30, Net 60). The company knows about the liability in advance, records it in the Accounts Payable ledger, and schedules the disbursement to optimize working capital.

Reimbursements are inherently reactive. The company only becomes aware of the specific cash outflow requirement after the employee has incurred the expense and submitted an expense report. This reactive nature makes reimbursements harder to forecast with precision, requiring finance teams to rely on historical data and strict budgetary caps to manage liquidity.

3. Documentation and Verification Requirements

Because disbursements involve direct relationships with established vendors, the documentation is usually standardized. The finance team relies on the three-way matching process: verifying the purchase order, the receiving report, and the supplier’s invoice before authorizing the disbursement.

Reimbursements require a more nuanced verification process. Finance teams must collect fragmented documentation, such as physical receipts, digital boarding passes, and credit card statements from various employees. Furthermore, the verification process for reimbursements involves checking the expense against subjective corporate policies.

Accounting Entries and General Ledger Impact

Accurate bookkeeping is the bedrock of corporate finance. The way a transaction is recorded dictates how it will appear on the balance sheet and income statement. Understanding the fundamental accounting principles is essential when differentiating the journal entries for these two types of outflows.

Recording Disbursements Properly

When a company makes a disbursement, it is typically clearing a liability that has already been recognized. Let us examine a standard vendor payment for office equipment.

Step 1: Recognizing the Expense and Liability (Accrual)

When the invoice is received, the company records the expense and the corresponding liability.

- Debit: Office Equipment Expense

- Credit: Accounts Payable

Step 2: Executing the Disbursement

When the payment is actually made to the vendor, the liability is cleared, and cash is reduced.

- Debit: Accounts Payable

- Credit: Cash/Bank

This straightforward process ensures that expenses are matched to the period in which they are incurred, independent of when the actual cash disbursement takes place.

Managing Reimbursement Journal Entries

Reimbursements follow a slightly different path because the expense is incurred by the employee before the company officially recognizes the liability in its system. Let us look at an employee submitting an expense report for a business flight.

Step 1: Employee Submits Expense Report

Once the expense report is approved, the company must recognize the travel expense and the liability owed to the employee.

- Debit: Travel Expense

- Credit: Accrued Expenses/Employee Reimbursements Payable

Step 2: Executing the Reimbursement Payment

When the company transfers the funds to the employee’s bank account (often processed alongside payroll), the entry is:

- Debit: Accrued Expenses/Employee Reimbursements Payable

- Credit: Cash/Bank

Notice that in both scenarios, the ultimate result is a Debit to an Expense account and a Credit to Cash. However, the intermediary liability accounts (Accounts Payable vs. Employee Reimbursements Payable) provide necessary granularity for financial analysis and auditing.

Tax Implications and VAT/GST Treatments

Distinguishing between disbursement vs reimbursement matters for tax compliance, specifically regarding Value Added Tax (VAT) and Goods and Services Tax (GST). Misclassifying these transactions can lead to denied tax claims and costly financial penalties.

Tax Rules for Disbursements (Agency Context)

In tax terminology, a “disbursement” often has a very specific meaning related to acting as an agent. If a company pays a cost on behalf of a client and passes that exact cost onto the client, it may be treated as a disbursement for VAT purposes. In this scenario, the payment is outside the scope of VAT.

For a transaction to qualify as a tax-exempt disbursement, stringent criteria must usually be met:

- The company must act merely as an agent for the client.

- The client must be the recipient of the goods or services.

- The client must be responsible for paying the third party.

- The client must authorize the company to make the payment on their behalf.

- The company must pass on the exact cost without any markup.

Example:

A law firm paying a government court fee on behalf of a client. The court fee is a disbursement. The law firm does not add VAT to this specific fee when invoicing the client, as they are simply passing the exact cost through.

Tax Rules for Reimbursements (Principal Context)

If a company incurs expenses while providing its own services to a client, and then attempts to recover those costs from the client, this is considered a reimbursement for tax purposes. Because the company consumed the goods or services to deliver its final product, the recovered costs are treated as part of the total service provided.

Therefore, these reimbursements are subject to VAT at the same rate as the main service. Even if the original expense had zero VAT, when the company recharges it to the client as a reimbursement, it must apply standard VAT.

Example:

A management consultant who travels to a client’s office buys a flight and a hotel room. These are the consultant’s own expenses incurred to fulfill the contract. When the consultant invoices the client for “Consulting Fees + Travel Reimbursement,” the entire invoice amount, including the travel costs, is subject to VAT.

Why Misclassification Can Lead to Penalties?

Incorrectly treating a taxable reimbursement as a non-taxable disbursement causes businesses to miss required VAT charges. During a tax audit, authorities will demand the unpaid tax, forcing the company to cover the costs along with interest and non-compliance penalties.

Conversely, charging VAT on a true disbursement unnecessarily inflates costs for the client. This error complicates the client’s tax recovery process and can damage the professional relationship due to financial inaccuracy.

Common Scenarios in Business Operations

To further contextualize the disbursement vs reimbursement debate, there are examine how these concepts play out across different operational departments.

1. Legal and Professional Services

Professional service firms like accountants, lawyers, and architects frequently manage both transactions simultaneously. For example, an architect may pay a structural engineer for a consultation, which is a direct disbursement. Later, they might invoice the client for design fees plus blueprint printing costs, which is a reimbursement subject to VAT.

2. Employee Travel and Entertainment Expenses

HR and Finance departments spend significant time managing Travel and Expense (T&E) claims, but the process changes when switching from personal to corporate cards. Swiping a corporate card makes the company directly liable to the issuer. Consequently, paying the monthly statement is a disbursement rather than a reimbursement because the employee never incurred an out-of-pocket expense.

3. Inventory and Supply Chain Adjustments

Managing cash flows in supply chain management matters when handling returned goods or damaged inventory. If a company returns defective materials, they must handle the purchase return process to receive a credit memo or cash refund. Accurately tracking the original disbursement alongside these returns ensures precise inventory valuations and supplier balances.

The Impact on Cash Flow and Financial Health

The distinction between these two types of payments extends beyond accounting entries. It deeply impacts how a company manages its liquidity and forecasts its financial future.

Cash Flow Forecasting

Disbursements are generally predictable. Because they are tied to purchase orders, vendor contracts, and established payroll schedules, financial analysts can accurately plot these outflows on a cash flow forecast. This predictability allows the company to optimize its treasury management, ensuring that cash is held in interest-bearing accounts until the exact moment a disbursement is due.

Reimbursements often introduce financial unpredictability when employees submit large, delayed expense reports at the end of a quarter. To prevent these sudden cash outflow spikes, companies should enforce strict submission deadlines and clear expense policies. Implementing these controls allows finance teams to transform erratic claims into manageable and forecastable data points.

Working Capital Management

Working capital is the lifeblood of any organization. Strategic management of disbursements, such as negotiating longer payment terms with suppliers can significantly improve a company’s working capital position. It keeps cash in the business longer.

Delaying reimbursements technically preserves corporate cash, but it damages employee morale and trust. Employees who are forced to carry corporate expenses on their personal accounts for extended periods may experience personal financial strain. Therefore, best-in-class organizations aim to process employee reimbursements as swiftly as possible, often within a few days of approval.

Best Practices for Managing Corporate Outflows

To maintain financial integrity and operational efficiency, company must implement robust frameworks for handling both disbursements and reimbursements. Without strict controls, companies expose themselves to duplicate payments, expense fraud, and cash flow bottlenecks.

Establishing Clear Expense Policies

A comprehensive and accessible corporate expense policy serves as the primary defense against financial inaccuracies. This document must clearly define legitimate business expenses, set spending limits, and outline the exact process for submitting claims. By removing ambiguity, a well-structured policy empowers managers to confidently reject non-compliant reimbursement requests and maintain financial integrity.

Document Collection and Verification

Maintaining a centralized vendor master file is critical for managing disbursements and preventing invoice fraud or misdirected funds. Finance teams must verify banking details to protect against risks like Business Email Compromise (BEC) attacks. For reimbursements, collecting itemized receipts is a non-negotiable requirement to ensure that specific purchases are allowable and separate from personal expenses.

Regular Audits and Compliance Checks

Continuous monitoring is essential to catch financial anomalies and ensure policy compliance through random audits. Finance teams must reconcile bank statements against the general ledger monthly to guarantee all disbursements and reimbursements are recorded accurately. Using the best account reconciliation system can automate this process, instantly flagging discrepancies, duplicate payments, or unrecorded claims.

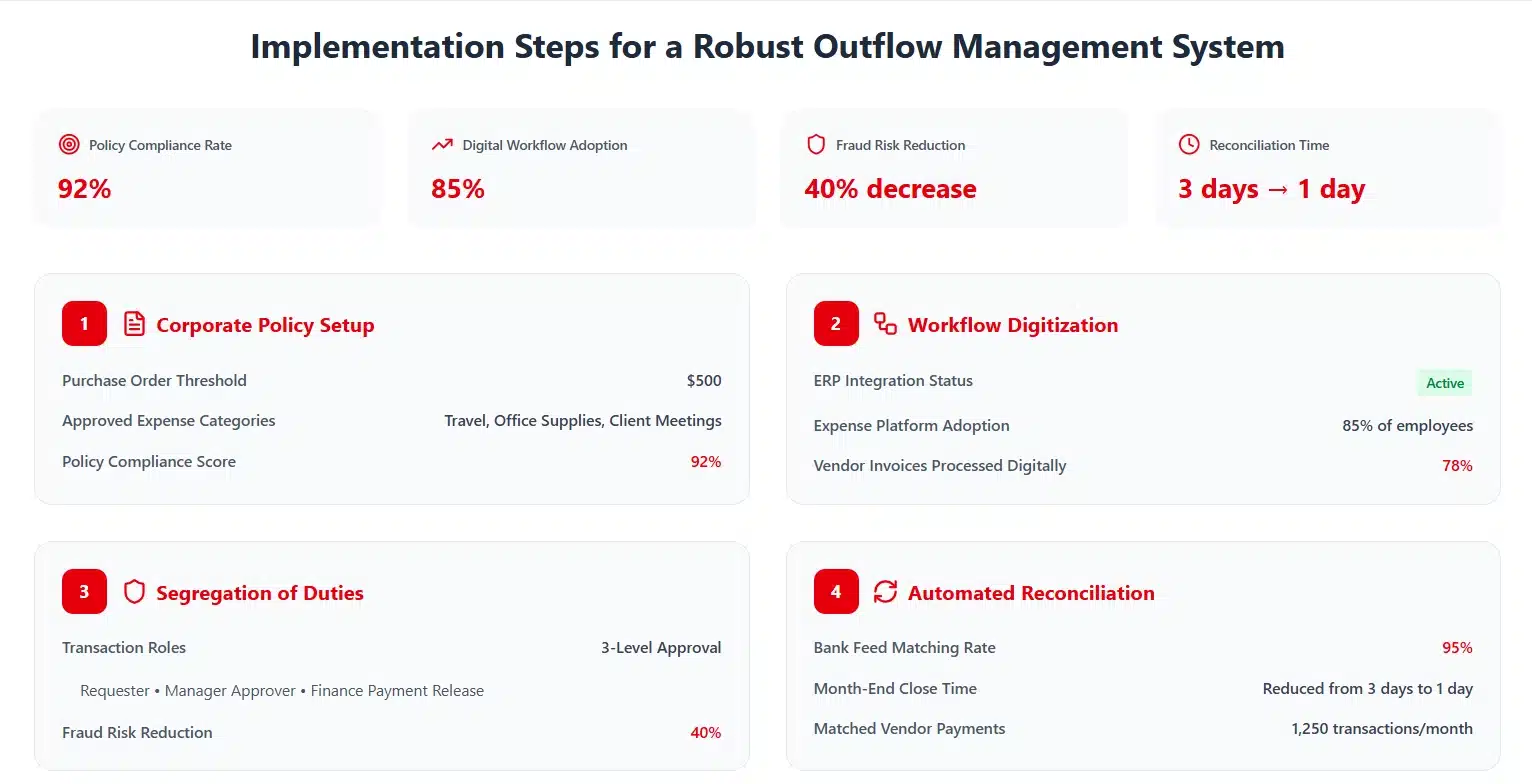

Implementation Steps for a Robust Outflow Management System

Transitioning from a disorganized cash management environment to a compliant system requires a strategic approach. Organizations must build an infrastructure that manages both direct corporate disbursements and employee reimbursements with equal precision.

Step 1: Establish Comprehensive Corporate Policies

Building a solid financial foundation requires clear, distinct rules for procurement and employee expenses. Your policy must explicitly define which purchases require a formal Purchase Order (PO) and which minor costs are acceptable for out-of-pocket spending. Setting strict monetary thresholds, such as mandating formal disbursements for any amount over $500, effectively prevents policy circumvention.

Step 2: Digitize and Centralize Workflows

Relying on paper invoices and email-based expense reports is a recipe for lost documents and delayed payments. Implement a robust Enterprise Resource Planning (ERP) system integrated with a dedicated expense management platform. This allows the accounts payable (AP) team to manage vendor disbursements in one module, while HR and finance manage employee reimbursements in another, all feeding into a centralized general ledger.

Step 3: Enforce Segregation of Duties

To prevent internal fraud and accounting errors, the person approving a transaction should never be the same individual initiating the payment. For disbursements, ensure that the employee requesting the service, the manager approving the invoice, and the staff releasing the funds are three different people. For reimbursements, require a multi-level review to verify the business purpose and tax compliance before any funds are released.

Step 4: Automate Reconciliation and Reporting

Leverage modern financial software to automate the matching of bank feeds with internal records. These tools can automatically link a corporate disbursement to its corresponding vendor invoice or match bulk reimbursement payouts to approved expense reports. This approach significantly reduces the month-end close cycle and ensures that cash flow statements accurately reflect all company outflows.

Advanced Practices in Cash Outflow Management

As organizations mature, they must move beyond basic compliance and look toward strategic optimization. Leading finance teams are adopting advanced practices to optimize working capital, enhance security, and improve the employee experience.

Transitioning to a Zero-Reimbursement Environment

Many forward-thinking companies are now working to eliminate the traditional reimbursement model entirely. By issuing smart corporate cards or single-use virtual cards, businesses shift transactions from delayed reimbursements to direct corporate disbursements. This approach provides finance teams with real-time spending visibility while removing the administrative burden of processing manual expense reports.

Optimizing Days Payable Outstanding (DPO)

Managing the timing of cash outflows is a critical component of effective working capital management and optimizing the payable formula. Advanced finance teams strategically delay vendor disbursements to the limit of negotiated payment terms to keep cash in the bank longer. Conversely, they often accelerate employee reimbursements to maintain high morale and build internal trust within the organization.

Integrating AI and Machine Learning for Spend Auditing

Manual auditing of disbursements and reimbursements is nearly impossible to manage at a large scale. Modern organizations now deploy AI-driven software to audit 100% of their cash outflows and detect financial anomalies instantly. These AI machine learning algorithms can identify duplicate invoices, flag out-of-policy spending, and alert teams to suspicious vendor billing patterns.

Holistic Spend Analytics

Best-in-class finance departments aggregate both disbursement and reimbursement data into unified spend dashboards for better oversight. Analyzing these total outflows holistically allows procurement teams to identify hidden trends and negotiate superior vendor rates. This data-driven strategy ensures that every dollar spent, whether through direct payments or employee claims, is used as leverage for future corporate discounts.

Conclusion

Effective financial management requires a clear understanding of the difference between disbursement and reimbursement in corporate finance. While both transactions involve money leaving the company, they serve distinct purposes and should not be treated as interchangeable processes.

Disbursements refer to direct payments made to vendors through structured accounts payable procedures, whereas reimbursements return funds to employees who temporarily cover business expenses. Understanding disbursement vs reimbursement helps finance teams maintain accurate accounting records, proper tax treatment, and well-organized financial workflows.

Clear policies, proper documentation, and reliable financial systems ensure that every payment leaving the organization is authorized and traceable. As business operations grow more complex, mastering the fundamentals of disbursements and reimbursements becomes increasingly important for maintaining financial control.

Experience the benefits of automated spend management firsthand by booking a free demo today.

FAQ about Accounting Disbursement vs Reimbursement

-

What is the main difference between a disbursement and a reimbursement?

The main difference lies in the relationship and timing. A disbursement is a direct payment made by a company to a vendor or third party to settle a corporate liability. A reimbursement is a repayment made to an employee or agent who has already paid for a business expense out of their own pocket.

-

Are reimbursements subject to VAT or GST?

Yes, typically. If a company incurs an expense in the course of delivering its services and recharges that cost to a client, it is considered a reimbursement and is usually subject to standard VAT or GST. This is different from a tax-exempt disbursement where the company acts merely as an agent passing on an exact cost.

-

Can paying a corporate credit card bill be considered a reimbursement?

No. When a company pays the balance of a corporate credit card, it is making a disbursement directly to the credit card issuer to settle a corporate liability. A reimbursement only occurs when an employee uses their personal funds or personal credit card and requires repayment from the company.