Adjusting entries are essential updates made at the end of a period, yet many businesses still overlook them, resulting in confusing financial statements. Those discrepancies often stem from incomplete or disorganized adjustments that distort overall accounting accuracy.

A study by the University of the Philippines revealed that 60% of companies experience financial statement errors due to improper adjusting entries. This highlights how crucial it is to get these adjustments right to maintain reliable reporting.

Key Takeaways

Adjusting entries improves financial accuracy by aligning revenues and expenses with the correct period and minimizing discrepancies.

Missing or incorrect adjustments can throw off your reported income and put you at risk of BIR compliance issues — especially during quarterly and annual filing in the Philippines.

A reliable accounting system with automation features can cut the time you spend on period-end adjustments and reduce manual errors.

What Are Adjusting Journal Entries?

Adjusting journal entries are corrections you make at the end of an accounting period to ensure your books reflect what actually happened — not just when cash moved. They convert your records to an accrual basis, so every transaction sits in the right period.

They help businesses track real account balances by updating revenues and expenses to the correct periods, regardless of when cash changes hands. Common examples include accrued revenues, deferred expenses, and depreciation adjustments that align records with actual activity.

Once you understand how adjusting and reversing entries work together, keeping your general journal accurate gets much easier. For Philippine businesses filing under BIR regulations, this is especially important — your books need to be defensible during audits.

Under Revenue Regulations No. 11-2024 and the TRAIN Law, the BIR expects businesses using accrual accounting to record revenues and expenses in the period they occur, not when payment is received. Adjusting entries are how you meet that requirement.

What Do Adjusting Entries Actually Do?

Adjusting entries align your recorded revenue and expenses with the actual amounts for each period. Without them, your income statement might show earnings you haven’t really received yet, or miss expenses you’ve already incurred.

For example, if your company paid six months of office rent upfront in January, you’d adjust each month to record only one month’s worth as an expense. That way your monthly financials stay honest.

Knowing how to make these entries also helps you comply with Philippine Accounting Standards (PAS) and Philippine Financial Reporting Standards (PFRS), which follow IFRS guidelines. If you’re also working with closing entries, adjusting entries are the step right before.

9 Types of Adjusting Journal Entries

Here are nine types of adjusting entries you’ll encounter. Each one addresses a different timing gap between when something happens financially and when it’s recorded.

Here are nine types of adjusting entries you’ll encounter. Each one addresses a different timing gap between when something happens financially and when it’s recorded.

-

Equipment

This covers small consumable or reusable assets — think office supplies, tools, or cleaning materials. At period-end, you adjust the supplies account to reflect what’s actually been used up versus what’s still on hand.

-

Revenue receivables

When you’ve delivered a service or product but haven’t billed the client yet, you record it as accrued revenue. This is common for Philippine BPO firms and service providers who bill monthly but deliver work continuously.

-

Accrued expenses (expense debt)

These are costs you’ve already incurred but haven’t paid yet — like utility bills, employee salaries for the last few days of the month, or SSS/PhilHealth/Pag-IBIG employer contributions that are due next month.

-

Accrued revenues

Similar to revenue receivables, but this covers situations where you’ve earned income that hasn’t been invoiced at all. A consulting firm that finished a project in March but won’t invoice until April would record an accrued revenue adjustment in March.

-

Deferred revenues (prepaid income)

You’ve collected cash, but you haven’t done the work yet. Think annual subscriptions or tuition fees collected at the start of a semester. Each period, you recognize only the portion of revenue you’ve actually earned.

-

Prepaid expenses (deferred expenses)

Prepaid rent, insurance premiums, or advance payments to suppliers — these were initially recorded as assets. Each month, you adjust to move the used portion into expenses. For example, if you paid ₱120,000 for a year of fire insurance, you’d expense ₱10,000 per month.

-

Depreciation expenses

Fixed assets like vehicles, machinery, and office equipment lose value over time. Depreciation entries spread that cost over the asset’s useful life. Under BIR rules, the straight-line method is most commonly accepted, with useful life periods specified per asset type (e.g., 5 years for office equipment, 10 years for buildings).

-

Provisions (Allowance for Bad Debts)

Not every customer pays. Provisions estimate how much of your accounts receivable might go uncollected. Philippine MSMEs with credit-based sales should regularly review their receivable aging and book a provision — this avoids a sudden hit to your income statement when bad debts are finally written off.

-

Inventory Shrinkage

Shrinkage captures the difference between your recorded inventory and what’s physically there — whether from theft, damage, spoilage, or counting errors. Retail and food businesses in the Philippines deal with this constantly. A physical count at period-end, compared against your book balance, tells you how much to adjust.

Cash Accounting vs. Accrual Accounting: Why It Matters

Cash accounting records income and expenses only when money changes hands. It’s simpler and works for very small businesses, but it can make your income look wildly inconsistent month to month.

Accrual accounting records transactions when they’re earned or incurred, regardless of when payment happens. It gives a clearer view of your financial health and is required for larger businesses under PAS/PFRS and BIR regulations.

In the Philippines, businesses with gross annual sales exceeding ₱3 million are generally required to use accrual-based accounting for BIR reporting purposes. If you’re at that threshold, adjusting entries aren’t optional — they’re a compliance requirement.

How to Prepare Adjusting Entries (Step by Step)

Here’s a practical walkthrough you can follow at the end of each accounting period:

- Step 1: Complete the unadjusted trial balance. Pull your trial balance from the general ledger. This is your starting point — every debit and credit should already be recorded for the period.

- Step 2: Identify accounts that need adjustment. Go through each account and ask: does this balance reflect reality as of the period-end date? Common candidates include prepaid expenses, accrued salaries, unearned revenue, and depreciation.

- Step 3: Record the adjusting entries. For each identified account, create the journal entry with the correct debit and credit. Make sure your supporting documents (contracts, invoices, schedules) are ready — BIR auditors will ask for them.

- Step 4: Prepare the adjusted trial balance. After posting all adjusting entries, generate a new trial balance. This adjusted version feeds directly into your income statement, balance sheet, and cash flow statement.

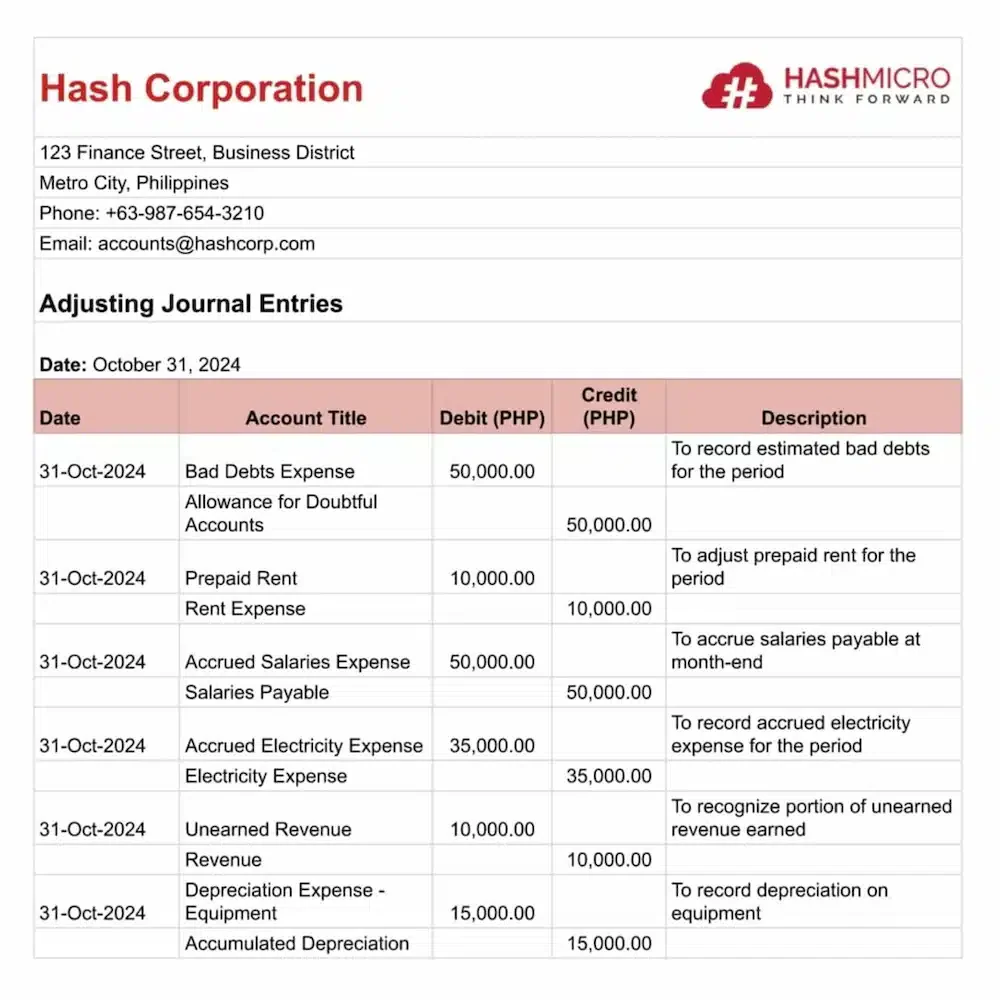

Adjusting Journal Entry Example

To illustrate this concept further, let’s explore an example of an adjusting journal entry that highlights its purpose and importance.

Let’s say your company paid ₱60,000 on January 1 for six months of office rent. Here’s how the adjusting entry would look at the end of January:

- Initial entry (Jan 1): Debit Prepaid Rent ₱60,000 / Credit Cash ₱60,000

- Adjusting entry (Jan 31): Debit Rent Expense ₱10,000 / Credit Prepaid Rent ₱10,000

- This moves one month’s portion (₱60,000 ÷ 6 = ₱10,000) from the asset account to the expense account. You’d repeat this entry at the end of each month through June.

Common Mistakes Philippine Businesses Make with Adjusting Entries

- Forgetting 13th month pay accruals. Under DOLE rules, 13th month pay is mandatory. Many businesses only record it in December, but accruing 1/12 of the estimated amount each month gives a more accurate monthly P&L.

- Not adjusting for withholding tax on services. If you’re paying contractors or professionals, you’re required to withhold creditable tax (typically 2% for contractors, 5%–15% for professionals). The withheld amount needs its own adjusting entry if it hasn’t been recorded at period-end.

- Skipping depreciation on low-value assets. Assets below ₱5,000 might seem insignificant, but if you have hundreds of them (which is common in manufacturing and retail), the cumulative depreciation matters.

- Ignoring FX adjustments for USD-denominated receivables. BPO companies and exporters often invoice in USD. At period-end, you need to revalue those receivables at the BSP closing rate and book the forex gain or loss.

Conclusion

Adjusting entries are a non-negotiable part of the accounting cycle if you want books that hold up under scrutiny — whether from your management team, investors, or the BIR.

They catch revenues and expenses that slipped through during the period, and they convert cash-based records into accrual-based statements that meet PAS/PFRS standards. Getting them wrong — or skipping them — snowballs into bigger problems at year-end.

If you’re still handling adjusting entries manually in spreadsheets, it might be time to look at accounting software options available in the Philippines that automate period-end adjustments and keep an audit trail the BIR can verify.

FAQ About Adjusting Entries

FAQ

The main categories of adjusting entries include accrued revenues, accrued expenses, unearned revenues, prepaid expenses, and depreciation. Each type helps ensure that income and expenses are properly matched to the period in which they occur.

Adjusting entries are posted in a company’s general ledger at the end of an accounting period to capture any transactions that haven’t yet been recognized. These entries are typically made after preparing the unadjusted trial balance and before generating the adjusted trial balance.

The goal of adjusting entries is to produce financial statements that accurately show a business’s true financial condition at period-end. Without these adjustments, reported income, expenses, assets, and liabilities may not reflect the real activity of the period, resulting in misleading financial reporting.