Many founders fail the transition to public ownership by overlooking the demand for strict financial reporting and transparency. This lack of readiness creates regulatory friction and kills investor trust before the first share is sold.

Preparation is the primary factor for success in the local capital market. Research regarding listings on Bursa Malaysia suggests that companies starting prep 24 months in advance achieve higher valuation stability. High quality disclosure can also cut the cost of equity by 30 percent as public investors prioritize proven transparency.

Mastering the compliance roadmap is the only way to avoid costly mistakes. Read this guide until the end to ensure your company is truly ready for a successful Initial Public Offering and sustainable growth in the Malaysian market 2026.

Key Takeaways

|

Digital systems provide the clarity needed for efficient operations. Accurate data supports growth and stability

Understanding the Concept of an Initial Public Offering

An initial public offering is the first time a private company offers its shares to the public through a stock exchange. Prior to this event, a company is typically owned by a relatively small group of individuals or entities, which may include the original founders, family members, angel investors, and venture capital or private equity firms.

Since the shares of a private company are not traded on a public exchange, they are not easy to buy or sell. Once the IPO takes place, the company becomes publicly listed, which means public investors can start trading its shares in the market. In simple terms, an IPO is the point where a private company officially becomes a public company.

The Structure of the Offering

An initial public offering typically consists of two main components: the primary offering and the secondary offering. In a primary offering, the company issues new shares to public investors.

The capital raised from the sale of these new shares goes directly to the company’s balance sheet, providing an influx of cash that can be used for various corporate purposes, such as funding research and development, expanding into new markets, or paying down existing debt.

Conversely, a secondary offering involves the sale of existing shares held by current owners, such as founders or early investors. The proceeds from a secondary offering go directly to these selling shareholders, not to the company itself. Many IPOs include both types of offering, so the company can raise fresh capital while early investors also get the chance to realise returns.

The Strategic Motivations Behind an IPO

The decision to pursue an initial public offering is rarely made lightly. The process is expensive, time consuming, and subjects the company to intense public scrutiny.

Therefore, the strategic motivations driving a company to go public must be compelling enough to outweigh these significant burdens. In many cases, companies decide to move forward because the long term benefits are considered worth the added pressure and compliance demands.

Raising Substantial Capital for Expansion

The most obvious and frequently cited reason for conducting an initial public offering is to raise a massive amount of capital. While private markets have grown increasingly robust in recent years, allowing companies to raise hundreds of millions of dollars without going public, the public equity markets still offer the deepest and most liquid pool of capital available globally.

By tapping into the public markets, a company can secure the substantial funding required to finance aggressive expansion plans, build new manufacturing facilities, acquire competitors, or invest heavily in cutting edge technology. Furthermore, once a company is public, it can more easily return to the market to raise additional capital through follow on offerings if needed.

Enhancing Corporate Image and Market Presence

Going public is widely perceived as a mark of success, stability, and maturity. The rigorous vetting process required to complete an initial public offering, including extensive audits, regulatory reviews, and public disclosures, signals to the market that a company has achieved a significant level of operational and financial sophistication.

This enhanced corporate image can yield numerous tangible business benefits. It can increase brand awareness among consumers, instill greater confidence in suppliers and business partners, and make it easier to secure favorable terms from lenders.

For many B2B companies, public status can be a crucial differentiator when competing for massive, multi year enterprise contracts, as prospective clients often prefer to partner with transparent, publicly traded entities. In Malaysia, this stronger image can also help build investor confidence, especially for companies preparing to meet listing and disclosure expectations under Bursa Malaysia.

Creating a Liquid Currency for Mergers and Acquisitions

For companies with aggressive growth strategies, an initial public offering provides a powerful tool for executing mergers and acquisitions or M&A.

When a company is private, using its stock to acquire other businesses is challenging because the value of the private stock is subjective and highly illiquid. Target companies are often reluctant to accept private shares as compensation because they cannot easily convert those shares into cash.

However, once a company is public, its stock has a clearly defined, publicly verifiable market value and can be readily sold on the open market. This makes the company’s shares more useful as an acquisition currency and allows the business to preserve cash for other operational needs.

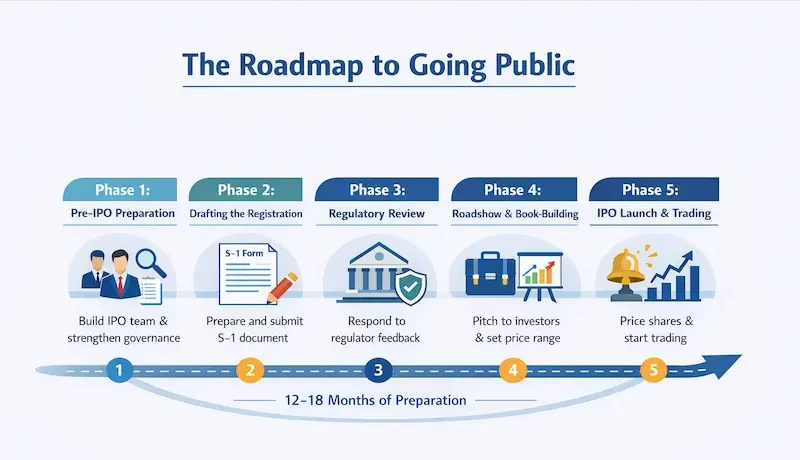

Implementation Steps: The Roadmap to Going Public

Going public usually takes 12 to 18 months of serious preparation. The process is often divided into several key phases so the company can manage it more clearly.

Phase 1: Pre-IPO Readiness and Team Assembly

Before filing anything, the company needs to build its IPO working group. This includes hiring investment banks or underwriters to manage the offering, specialized legal counsel to navigate securities law, and independent auditors to upgrade financial statements to Public Company Accounting Oversight Board or PCAOB standards.

Internally, the company also needs stronger investor relations capability and more formal governance, including an independent board and audit committee.

Phase 2: Drafting the Form S-1 Registration Statement

The Form S-1 is the core IPO document. Drafting this document is an exhaustive process that requires the company to disclose its financial history, business model, competitive landscape, and capital structure.

Two of the most important sections are the MD&A, which explains the financial results, and the Risk Factors section, which outlines the main threats to the business. Additionally, the company must meticulously outline Risk Factors, disclosing every conceivable threat to the business to protect against future shareholder litigation.

Phase 3: SEC Review and the Quiet Period

After the S-1 is filed, the regulator reviews it and usually sends comments that must be addressed before the offering can move forward. The company and its legal team must respond to these comments, amending the S-1 until the SEC declares it effective.

During this period, the company also enters the quiet period, which limits what executives can say publicly about the offering. This rule is meant to prevent the company from promoting the stock too aggressively before the prospectus is officially available.

Phase 4: The Roadshow and Book-Building

Once the filing is nearly ready, the executive team begins the roadshow to present the company to institutional investors. The goal is to pitch the company’s growth story and gauge investment interest.

Based on investor feedback, underwriters then run the book building process to estimate demand and support final pricing decisions.

Phase 5: Pricing, Allocation, and Trading

In the final phase, the company and underwriters agree on the IPO price and share allocation. Shares are allocated to institutional investors, and the following morning, the executives ring the exchange bell.

After that, the stock begins trading publicly and its market value starts moving based on investor demand.

Providing Liquidity and Retaining Talent

An initial public offering is the ultimate liquidity event for a company’s early stakeholders. Founders who have dedicated years to building the business, angel investors who took a risk in the earliest stages, and venture capitalists who provided growth funding all look to the IPO as the primary mechanism for realizing a return on their investment.

Beyond rewarding early investors, going public is also a critical strategy for attracting and retaining top tier talent. High growth private companies frequently use equity based compensation, such as stock options or restricted stock units or RSUs, to attract skilled employees.

However, this equity holds little practical value until a liquidity event occurs. An IPO can turn that paper value into something more tangible, which may improve retention and make the company more attractive to strong talent.

The Complex Mechanics of the IPO Process

The IPO process is a structured journey that takes a company from private ownership to public listing. The process of executing an initial public offering typically spans six to twelve months, though the preparatory phase can begin years in advance. It also requires close coordination between management, underwriters, legal counsel, and auditors.

1. Pre-IPO Preparation and the Bake-Off

Before launching an IPO, the company needs to make sure it is ready to operate as a public entity. This involves strengthening the management team, particularly by hiring a highly experienced Chief Financial Officer (CFO) and a seasoned General Counsel.

Once the internal team is ready, the company enters the bake off stage, where investment banks compete to lead the offering. They usually present valuation estimates, marketing plans, and their track record in similar IPOs. Based on these presentations, the company selects one or more lead underwriters (also known as bookrunners) to manage the offering, as well as a syndicate of co-managers to assist in distributing the shares.

2. The Organizational Meeting and Drafting the Registration Statement

The formal process begins with an organisational meeting involving executives, underwriters, legal teams, and auditors. This meeting sets the timeline, divides responsibilities, and starts the drafting of the registration statement.

In the United States, this document is known as the Form S-1. The S-1 is the main document investors use to understand the company before the IPO. It covers the business model, key risks, leadership structure, and audited financial statements.

3. The SEC Review Process

After the first draft is ready, the company submits it to the regulator for review. In the U.S., this is the Securities and Exchange Commission (SEC).

The regulator checks whether the disclosures are complete and whether the financial information is presented fairly. In most cases, the company will receive comments that require clarification, revisions, or added disclosures. The filing must then be updated and resubmitted until the regulator is satisfied.

For companies planning to list in Malaysia, this stage also needs to align with the review and disclosure requirements of the Securities Commission Malaysia and Bursa Malaysia.

4. The Roadshow and Book Building

While the review is ongoing, the company usually starts the roadshow. The roadshow is an intensive, multi-city (and sometimes international) marketing tour designed to pitch the initial public offering to institutional investors, such as mutual fund managers and hedge funds.

During these meetings, the CEO and CFO explain the company story, growth plans, and investment potential. At the same time, underwriters collect investor interest through book building to measure demand and pricing appetite.

5. Pricing the Offering and the First Day of Trading

The final step is setting the IPO price and deciding how many shares will be sold. Based on the demand generated during the roadshow and recorded in the order book, the company’s management and the lead underwriters meet to determine the final IPO price and the exact number of shares to be sold.

If the price is too high, the stock may perform poorly on its first day. If it is too low, the company may raise less capital than expected. That is why pricing needs to balance market demand and long term confidence.

Once the price is finalised, the shares are allocated and the stock begins trading on the market.

The Critical Role of Accounting in an IPO

Accounting is critical in an IPO because the finance team needs to raise reporting quality, fix complex issues, and prepare for closer audit and regulatory review. One of the most common hurdles is revenue recognition, since contracts must be reviewed carefully to apply the right accounting treatment. The team also needs to strengthen controls by mapping every significant financial process and making sure those controls can support public company standards.

Operational Readiness for Public Company Status

An initial public offering is not just a financial event. It also changes how the company operates every day. A business cannot wait until listing day to start acting like a public company.

Operational readiness needs to be built early, long before the registration statement is filed. That usually means upgrading systems, improving governance, and preparing teams to handle public company responsibilities.

Upgrading IT Infrastructure and ERP Systems

The systems used by a private company are often not strong enough for public company demands. Public companies require enterprise grade technology to ensure the accuracy, security, and timeliness of their financial data.

Basic spreadsheets and entry level accounting tools usually need to be replaced with integrated ERP systems. These systems help centralise financial data, automate key processes, and support stronger access control.

Using integrated enterprise software, such as solutions provided by HashMicro, can help make this transition smoother by improving data visibility and supporting more reliable financial reporting. A connected system also helps align business operations across departments, from procurement to human resources, so reporting becomes more consistent and easier to manage.

Transforming Corporate Governance

Going public also requires stronger corporate governance. Public investors demand a high level of oversight and accountability, which necessitates a complete overhaul of the company’s corporate governance structure.

Private company boards are often dominated by founders and early investors, but public companies are expected to have stronger independent oversight. In contrast, public companies are required by exchange listing rules to have a board of directors composed of a majority of independent directors, individuals who have no material relationship with the company other than their board seat.

They also need formal committees such as an audit committee, a compensation committee, and a nominating and corporate governance committee. Among them, the audit committee plays a key role in overseeing financial reporting, external audits, and internal control effectiveness.

Building an Investor Relations Department

After the IPO is completed, the company needs to communicate consistently with analysts, institutional investors, and public shareholders. To manage this crucial function, the company must establish an Investor Relations or IR department.

The IR team becomes the main link between the company and the market. They are responsible for drafting quarterly earnings releases, organizing earnings conference calls, participating in investor conferences, and ensuring that the company’s messaging is consistent, transparent, and compliant with fair disclosure regulations such as Regulation FD.

A strong IR function can support valuation by helping the market understand the company’s strategy and trust its communication.

The Costs and Risks of Going Public

Although an initial public offering offers major benefits, it also comes with high costs and added pressure. The company must be ready for higher compliance costs, tighter scrutiny, and new strategic risks after listing.

The Costs and Risks of Going Public

| Key Area | Description |

|---|---|

| Higher Compliance Costs | Public companies must meet stricter regulatory requirements, including financial reporting, audits, and governance standards, which significantly increase operational costs. |

| Increased Scrutiny | Companies face continuous oversight from regulators, investors, and the public, requiring higher transparency and consistent performance reporting. |

| Strategic Pressure | Management must balance long-term strategy with short-term market expectations, often under pressure to meet quarterly targets. |

| Market Volatility Risk | Share prices can fluctuate due to external factors beyond company control, impacting valuation and investor confidence. |

| Disclosure Obligations | Sensitive business information must be disclosed publicly, which may reduce competitive advantage. |

Industry Use Cases: How Different Sectors Approach the IPO

The IPO framework may follow the same general rules, but each industry approaches it differently. That is because every sector uses public funding to solve different growth, capital, and operational needs.

Technology and Software as a Service (SaaS)

For technology and SaaS companies, an IPO is often used to fund rapid growth. For technology and SaaS companies, an IPO is often viewed as a mechanism to fund aggressive customer acquisition and continuous research and development.

Many of these companies go public before becoming profitable, so investors pay close attention to metrics such as ARR, NRR, and CAC. A notable trend in tech IPOs is the implementation of dual class share structures, which allow founders to retain voting control and protect long term vision from the short term pressures of public market activists.

Biotechnology and Pharmaceuticals

Biotech companies often approach IPOs very differently from other sectors. Many biotech firms go public pre revenue and sometimes even before entering clinical trials.

For these businesses, the IPO often serves as a funding source for expensive research and regulatory development. Investors usually focus less on current revenue and more on drug approval potential, clinical progress, and the strength of the intellectual property pipeline.

Consumer Goods and Retail

Consumer brands often use the IPO as both a funding strategy and a visibility boost. Going public increases brand visibility and consumer trust.

For retail businesses, the funds raised are often used to expand store networks, improve supply chain performance, or support international growth. These companies may also attract strong retail investor interest because customers already know and use the brand.

Implementation Steps: The Roadmap to Going Public

Going public usually takes 12 to 18 months of serious preparation. The process is often divided into several key phases so the company can manage it more clearly.

Phase 1: Pre-IPO Readiness and Team Assembly

Before filing anything, the company needs to build its IPO working group. This includes hiring investment banks or underwriters to manage the offering, specialized legal counsel to navigate securities law, and independent auditors to upgrade financial statements to Public Company Accounting Oversight Board or PCAOB standards.

Internally, the company also needs stronger investor relations capability and more formal governance, including an independent board and audit committee.

Phase 2: Drafting the Form S-1 Registration Statement

The Form S-1 is the core IPO document. Drafting this document is an exhaustive process that requires the company to disclose its financial history, business model, competitive landscape, and capital structure.

Two of the most important sections are the MD&A, which explains the financial results, and the Risk Factors section, which outlines the main threats to the business. Additionally, the company must meticulously outline Risk Factors, disclosing every conceivable threat to the business to protect against future shareholder litigation.

Phase 3: SEC Review and the Quiet Period

After the S-1 is filed, the regulator reviews it and usually sends comments that must be addressed before the offering can move forward. The company and its legal team must respond to these comments, amending the S-1 until the SEC declares it effective.

During this period, the company also enters the quiet period, which limits what executives can say publicly about the offering. This rule is meant to prevent the company from promoting the stock too aggressively before the prospectus is officially available.

Phase 4: The Roadshow and Book-Building

Once the filing is nearly ready, the executive team begins the roadshow to present the company to institutional investors. The goal is to pitch the company’s growth story and gauge investment interest.

Based on investor feedback, underwriters then run the book building process to estimate demand and support final pricing decisions.

Phase 5: Pricing, Allocation, and Trading

In the final phase, the company and underwriters agree on the IPO price and share allocation. Shares are allocated to institutional investors, and the following morning, the executives ring the exchange bell.

After that, the stock begins trading publicly and its market value starts moving based on investor demand.

Conclusion

Taking a company public is a major step that can create long term opportunities, but it also brings greater pressure in reporting, governance, and daily operations. An IPO is not only about raising capital, because it also reflects whether the business is ready to meet higher standards in a more transparent market environment.

That is why IPO readiness should be built early and approached with a clear strategy. Strong financial reporting, reliable internal controls, and well prepared operations can make a significant difference when your company starts facing public scrutiny. The better your preparation is before listing, the easier it becomes to manage both the process and the expectations that follow.

If your business is working toward stronger reporting, better visibility across departments, and more structured financial processes, using the right system can help support that transition. You can explore a free demo to see how a more integrated system may help your company improve operational readiness before moving into a more demanding stage of growth.

Frequently Asked Questions About IPO

-

How long does IPO preparation usually take?

IPO preparation often starts well before the official filing stage. In many cases, companies need 12 to 24 months to strengthen reporting, governance, internal controls, and operational readiness before entering the public market.

-

What changes most after a company goes public?

The biggest change is the level of scrutiny. Once listed, a company must deal with stricter disclosure requirements, tighter reporting timelines, stronger governance expectations, and more frequent communication with investors and analysts.

-

Why are internal controls important before an IPO?

Internal controls help ensure financial reporting is accurate, consistent, and reliable. Before an IPO, strong controls are essential because public companies are expected to meet higher compliance standards and show that their reporting processes can withstand external review.

-

Is a traditional IPO the only way to enter the public market?

No. Companies can also explore alternatives such as direct listings and SPAC mergers. Each route comes with different advantages, costs, and risks, so the right choice depends on the company’s goals, capital needs, and readiness.