Every time a business pays its employees or settles a vendor invoice, an EFT payment is working in the background. Short for Electronic Funds Transfer, it is the digital movement of money between bank accounts and it has become the standard for modern financial operations.

The numbers speak for themselves. According to Bank Negara Malaysia’s Annual Report 2024, e-payment transactions grew 19% to reach 409 transactions per capita translating to at least one e-payment per Malaysian per day. HSBC Amanah For businesses, this is a clear signal: clients, vendors, and employees expect payments to be fast, digital, and traceable.

For accounting professionals, treasury managers, and business owners, understanding how EFTs work is no longer a nice-to-have. As financial systems grow more automated and interconnected, the ability to manage, track, and reconcile electronic payments is a core operational competency. This article breaks down exactly what an EFT payment is, how it functions, and what businesses need to know to use it effectively.

Key Takeaways

Table of Content

|

What is EFT Payment Actually?

An EFT payment is the digital exchange of money between two bank accounts either within the same financial institution or across different banks without requiring physical currency or manual bank staff involvement. It is a broad category that covers a wide range of transaction types, from direct payroll deposits to corporate wire transfers to everyday card purchases.

Today, however, the EFT ecosystem is a sophisticated network of banks, clearing houses, and regulatory bodies operating through encrypted digital messaging systems. What these systems all share is their reliance on electronic data interchange to move capital securely and efficiently.

In corporate finance, the term EFT is often used as a shorthand for any non-paper payment. While this is broadly accurate, finance professionals should be aware that different sub-types of electronic transfers carry distinct implications for processing speed, cost, and reconciliation procedures.

How Does an EFT Payment Work?

To fully appreciate the efficiency of an EFT payment, there is a precise sequence of steps happening behind the scenes. Understanding these stages matters for accountants who need to track cash flow status at any given point.

The Four Stages of an Electronic Transfer

1. Authorization: The process starts when the payer formally approves the transaction. In a business context, this typically happens through an ERP system or treasury management portal, where the user inputs the recipient’s routing number, account number, transfer amount, and execution date. For consumer transactions, this step often involves a PIN entry or mobile app authentication.

2. Transmission: Once authorized, the payer’s bank known as the Originating Depository Financial Institution (ODFI) compiles the payment instructions into a standardized electronic file. In many countries, these files are batched together at set intervals rather than sent one by one. The ODFI then transmits this file to a central clearing facility. The ODFI then transmits this batch file to a central clearing facility.

3. Clearing: The clearing house receives the batched files and acts as an intermediary. It sorts transactions by destination bank, verifies routing information, and forwards payment instructions to each Receiving Depository Financial Institution (RDFI). In the US, this role is filled by networks such as the Federal Reserve or The Clearing House.

4. Settlement: Settlement is where the actual transfer of money between institutions occurs. The clearing house calculates net positions across all participating banks, and the central bank adjusts reserve accounts accordingly. Once the RDFI receives its credit, it posts the funds to the individual payee’s account. Depending on the EFT type used, this entire process can take days, hours, or seconds.

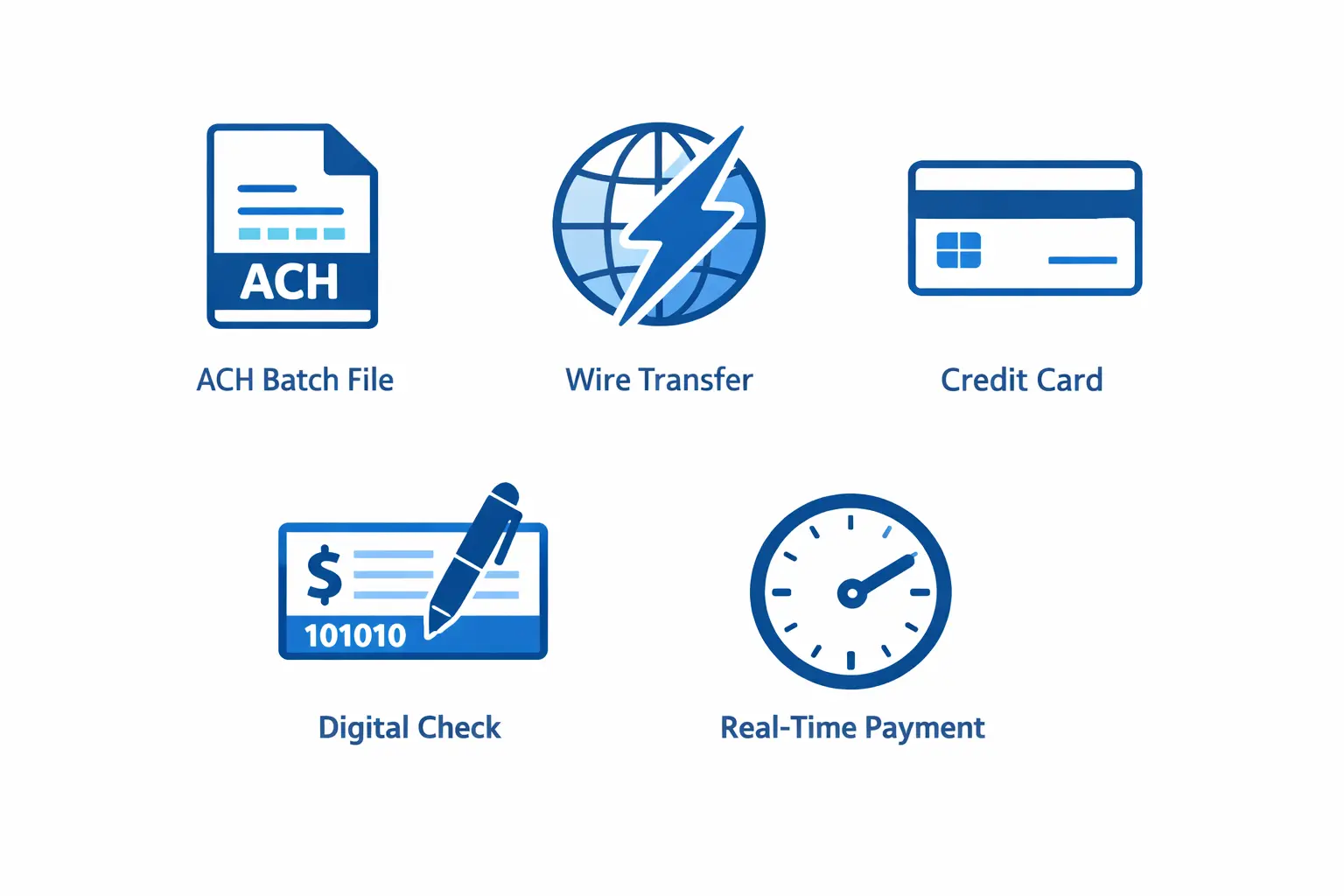

Types of EFT Payments Every Business Should Know

EFT is an umbrella term. Below that, there are several distinct payment rails, each designed for different scenarios. Choosing the right type based on transaction size, urgency, and destination is a key decision for any finance team.

Automated Clearing House (ACH) Transfers

The Automated Clearing House (ACH) network processes high volumes of transactions in batches, making it one of the most cost-efficient options available. ACH credits push funds from payer to payee (such as payroll direct deposits), while ACH debits pull funds from a payer’s account (such as automatic bill payments). Traditional ACH settles within one to three business days, though Same-Day ACH has significantly compressed this window.

Wire Transfers

Wire transfers move funds individually and in real time, making them the preferred choice for high-value, time-sensitive transactions including real estate deals, mergers and acquisitions funding, and critical international supplier payments. Domestic wires are processed through central bank systems like Fedwire; international wires rely on the SWIFT network. The trade-off is cost: wire transfer fees are substantially higher than ACH.

Card Transactions (Credit and Debit)

Every corporate purchasing card swipe or consumer debit transaction is an EFT. Card networks like Visa and Mastercard handle real-time authorization, though actual settlement to the merchant’s bank typically takes one to two business days. This type is fundamental to retail, e-commerce, and everyday corporate expense management.

Electronic Checks (eChecks)

An eCheck is a digital version of a paper check that uses the same routing and account number information but processes through the ACH network. It is widely used in B2B billing where vendors want the familiarity of check-based payment without the physical handling delays.

Real-Time Payments (RTP) and Instant Transfers

RTP networks represent the most significant recent development in the EFT space. Unlike ACH, which operates on a batch schedule, RTP systems work 24/7/365 and settle funds within seconds. In the US, both the RTP network and the Federal Reserve’s FedNow service provide this capability, making them increasingly important for payroll emergencies, urgent vendor settlements, and instant consumer disbursements.

How EFT Payments Transform Accounting Operations

The transition from analog payment methods to digital EFT systems has fundamentally altered the daily operations, strategic capabilities, and overall efficiency of corporate accounting departments. The impact of electronic funds transfers extends far beyond the mere act of moving money, it reshapes how financial data is recorded, verified, and utilized for strategic decision-making.

Streamlining Accounts Payable and Receivable

Traditional AP workflows required printing, signing, mailing, and manually tracking paper checks a slow, opaque process where cash movements were difficult to predict. EFT payments automate this entirely. AP teams can schedule payments to execute on exact due dates, optimizing days payable outstanding (DPO) and capturing early payment discounts consistently.

On the AR side, electronic payments reduce days sales outstanding (DSO) by elimin

ating postal delays and providing faster access to working capital.

Automating the Core Financial Records

One of the most operationally significant benefits of EFTs is their compatibility with accounting automation. When an electronic transfer is initiated or received, modern accounting systems can capture the accompanying remittance data and auto-post the corresponding journal entries. This keeps the general ledger current without manual data entry, giving CFOs and controllers an accurate, real-time picture of the company’s financial position.

Faster & More Accurate Bank Reconciliation

Bank reconciliation has historically been one of the most time-consuming tasks in accounting. Paper checks introduced float, data entry errors, and the occasional lost-in-the-mail mystery. EFT payments arrive with standardized digital metadata precise timestamps, unique transaction IDs, and exact amounts that enables algorithmic matching between bank feeds and internal ledgers.

Modern systems can achieve near-100% auto-reconciliation rates, freeing accounting teams to focus on analysis rather than manual ticking and tying.

Benefits of Using EFT Payments For Business

The near-universal adoption of electronic funds transfers by modern enterprises is not merely a matter of following technological trends; it is driven by highly quantifiable operational and financial advantages. Businesses that optimize their use of EFTs gain a significant competitive edge in treasury management and operational efficiency.

Speed and Cash Flow Predictability

EFTs eliminate the geographic and logistical delays of physical payment methods. An international wire transfer can reach its destination within hours an ACH batch executes on a predetermined date. For treasury managers, this predictability enables accurate cash flow forecasting and tighter liquidity management capabilities that are simply not achievable with

Lower Transaction Costs

The true cost of a paper check factoring in check stock, postage, labor to print, sign, and mail typically ranges from $4 to $10 per transaction. An ACH transfer often costs less than $0.50. For businesses processing hundreds or thousands of vendor payments each month, the shift to electronic transfers produces immediate and substantial savings.

Clear Digital Audit Trail

Every EFT generates an immutable digital record that logs each stage of the transaction from authorization to settlement. When a vendor questions a payment, the accounts payable team can produce instant, verifiable proof without searching physical archives. This transparency also supports internal audits, tax compliance, and regulatory reporting all areas where paper-based systems introduce risk and administrative overhead.

Environmental Sustainability

Beyond the financial and operational metrics, transitioning to a fully electronic payment ecosystem aligns with corporate environmental, social, and governance (ESG) goals. By eliminating paper checks, envelopes, and the physical transportation required to move paper documents between offices, post offices, and banks, businesses can significantly reduce their carbon footprint and contribute to broader sustainability initiatives.

EFT vs. Traditional Payment Methods

To truly grasp the value proposition of the EFT payment, it is helpful to contrast it directly with the traditional payment modalities it has largely replaced: cash and paper checks.

| Criteria | ETF Payment | Paper Check | Physical Cash |

| Processing Speed | Minutes to 3 business days | 3–10+ business days | Immediate |

| Transaction Cost | < $0.50 (ACH) | $4–$10 per check | Storage/security costs |

| Audit Trail | Full digital record | Limited, manual | None |

| Fraud Risk | Low (encrypted) | High (check washing) | High (anonymous) |

| Reconciliation | Automated | Manual/time-consuming | Manual only |

| International Use | Yes (SWIFT/wire) | Complex, slow | Impractical |

Security Protocols and Regulatory Framework

Because electronic funds transfers move trillions of dollars daily, they are prime targets for cybercriminals and fraudulent actors. Consequently, the EFT ecosystem is heavily regulated by government entities and secured by sophisticated, multi-layered cryptographic protocols. For accounting and finance professionals, understanding this compliance and security landscape is vital for protecting corporate assets.

The Regulatory Framework

In the United States, consumer EFT transactions are primarily governed by the Electronic Fund Transfer Act (EFTA), implemented through Regulation E. The EFTA establishes disclosure requirements, error resolution procedures, and consumer liability limits for unauthorized transactions.

For corporate transactions, the regulatory focus shifts to Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements. Financial institutions must monitor EFT traffic for suspicious activity and screen international wire transfers against global watchlists maintained by bodies such as the Office of Foreign Assets Control (OFAC). Non-compliance can result in frozen funds, significant financial penalties, and potential criminal liability.

Security Measures That Protect EFT Transactions

Three layers of protection form the backbone of EFT security:

- End-to-end encryption scrambles payment data including account and routing numbers into unreadable ciphertext as it travels across networks.

- Tokenization replaces sensitive account details with randomly generated token strings. Even if intercepted, a token has no usable value outside the specific transaction it was created for.

- Multi-Factor Authentication (MFA) requires users to verify their identity through multiple independent credentials before initiating or approving a payment, reducing the risk of unauthorized access.

Common Pitfalls and How to Avoid Them

Despite the inherent security and efficiency of electronic transfers, organizations can still fall victim to operational errors and sophisticated fraud if proper safeguards are not established. Recognizing these pitfalls is the first step in mitigating financial risk.

Business Email Compromise (BEC) and Fraud

BEC is one of the most financially damaging threats to EFT integrity. Attackers impersonate vendors or executives via email, requesting that payment routing details be updated to a fraudulent account. Because wire transfers are typically irreversible, losses from successful BEC attacks can be catastrophic.

The mitigation is straightforward: any request to change payment details must be verified by a phone call to a known, trusted contact never via a reply to the suspicious email itself.

Data Entry Errors

A single typo in a routing or account number can cause a failed transaction or, in the worst case, deposit funds into an unintended account. Recovering misdirected funds is time-consuming and can damage vendor relationships.

Using automated vendor portals where suppliers manage their own banking information combined with pre-note verification before sending large sums to new accounts significantly reduces this risk.

Reconciliation Bottlenecks

When large batches of EFTs appear on a bank statement as a single lump sum, accounting teams can struggle to match that total to the individual invoices it covers.

Ensuring your payment processor supports rich remittance data formats (such as EDI 820) and that your accounting software can parse those formats for automatic matching prevents this from becoming a recurring bottleneck.

How to Implement EFT Payments in Your Business

Transitioning to a fully electronic payment environment requires a structured approach. Here are the core steps most organizations follow:

- Conduct a Payment Infrastructure Audit: Analyze transaction volumes, average payment sizes, and vendor preferences. This helps determine the right mix of EFT types for your operation

- Select the Right Technology Partner: Evaluate payment gateways and treasury management systems. Assess API capabilities, security certifications, and fee structures. Confirm compatibility with your banking partners.

- ERP and Accounting Integration: Connect your accounting software to your payment platform. Initiated payments should automatically mark invoices as paid in the general ledger. This typically requires SFTP or API connections with your bank.

- Testing and Vendor Onboarding: Run test transactions to verify routing and account details. Onboard vendors by collecting their banking information through secure digital portals.

Conclusion

EFT payments have moved from a technology upgrade to a business necessity. The combination of faster settlement, lower transaction costs, automated reconciliation, and a clear digital audit trail makes electronic funds transfers measurably superior to paper-based alternatives across virtually every dimension that matters to finance and operations teams.

Understanding how each EFT type works from ACH batches to real-time wire transfers gives businesses the tools to match the right payment method to the right situation. And paired with the right treasury management or ERP system, it creates a payment infrastructure that supports both day-to-day efficiency and long-term financial visibility.

FAQ About EFT Payments

-

How long does an EFT payment take to process?

It depends on the type. Standard ACH takes one to three business days. Same-Day ACH settles within the same business day. Domestic wire transfers typically complete on the same day. International wires take one to two business days. RTP networks and FedNow settle within seconds, around the clock.

-

Are EFT payments safe?

Yes, EFTs are generally very secure. They use end-to-end encryption, tokenization, and multi-factor authentication. The primary risks such as BEC fraud are procedural, not technical. They can be mitigated with proper verification protocols.

-

Can EFT payments be reversed?

ACH transfers can sometimes be reversed within a limited window if an error occurs. Wire transfers, however, are typically irrevocable once processed. This makes it essential to verify all payment details before initiating a wire, and to have strong fraud controls in place.

-

What is the difference between a wire transfer and an EFT?

Payroll software in Malaysia incorporates several security measures to protect sensitive employee and company data. Specifically, these include SSL encryption, secure cloud hosting, and compliance with data protection laws such as the Personal Data Protection Act (PDPA). Additionally, many systems provide secure login features and regular updates to safeguard against security threats.

-

How do i track my EFT Payment?

Most banks provide a unique trace number or reference ID for every EFT transaction. You can use this to check the payment status directly through your bank’s online portal. For businesses processing high volumes, an ERP with a finance module gives full visibility across all incoming and outgoing EFTs in one centralized dashboard.