Every business ends up with assets that reach the end of their useful life. A production machine becomes too expensive to maintain, office laptops slow down, or a vehicle no longer fits your routes. That part is normal.

What often creates headaches is the exit. If an asset leaves your floor but stays in your books, your numbers start drifting. And once your numbers drift, audits get uncomfortable.

So here’s the real question: when you retire an asset, can you prove what happened, who approved it, and how you recorded it?

Key Takeaways

|

What Is Asset Disposal and Why Is It Important for Business?

Asset disposal is how you remove a fixed asset from your accounting records after it leaves your operations. You might sell it, scrap it, trade it in, or donate it. Either way, you are not only dealing with the physical item. You are also closing the asset’s financial story.

When you dispose of an asset, your finance team needs to remove the asset’s cost and accumulated depreciation from the balance sheet, then record any gain or loss on the income statement. If you skip that, you create “ghost assets”, meaning the asset no longer exists, but it still shows up in your books. Do you really want to discover that during an audit?

If you operate in Malaysia, disposal also touches compliance. If you claimed capital allowances, disposing of plant or machinery can trigger a balancing adjustment (balancing allowance or balancing charge) under Malaysia’s tax rules, so you need clean documentation and proper calculations.

If the asset is electronic equipment, you should treat end-of-life handling seriously because Malaysia regulates scheduled wastes under the Environmental Quality (Scheduled Wastes) Regulations 2005, and it expects responsible handling by waste generators and licensed contractors.

Key Methods in Asset Disposal

The right method depends on the asset’s condition, remaining value, and what you want to achieve. Sometimes you want cash recovery. Sometimes you want speed. Sometimes you want risk reduction. The mistake is choosing a method by habit instead of by numbers.

1. Sale

You sell an asset when it still has market value and someone else can use it. This method helps you recover cash and often reduces storage and maintenance costs immediately. To keep the transaction clean, you set a fair price, document the sale properly, and record the difference between proceeds and net book value. If you do it right, a sale improves cash flow and strengthens your asset controls at the same time.

2. Scrapping or Retirement

You scrap an asset when it has no realistic resale value or it becomes unusable. You remove it physically, then record a loss if the asset still has remaining book value. This method does not generate revenue, but it keeps your books honest and prevents dead assets from inflating your fixed asset register. If you scrap IT equipment in Malaysia, treat it as a compliance-sensitive activity.

E-waste and other categories can fall under scheduled waste rules, so you should use proper handling and keep evidence that supports responsible disposal.

3. Trade-in or Exchange

A trade-in works when a vendor accepts your old asset as partial payment for a new one. You reduce the cash outlay and shorten the replacement cycle. From an accounting perspective, you still close the old asset properly and record the new asset with documentation that clearly states the trade-in value. If your documents look vague, your numbers will look questionable later.

4. Donation

Donation means you transfer the asset to a charitable or non-profit organization. You do not receive cash, but you may gain CSR value and, depending on the facts and documentation, tax-related considerations. The key is evidence. You remove the asset from your books at its book value, and you keep official documentation from the receiving organization so your reporting stays defensible.

An Effective Asset Disposal Process from Start to Finish

A good disposal process feels repeatable. It should not rely on someone’s memory or last-minute scrambling. When you standardize the workflow, you reduce errors, shorten cycle time, and keep your audit trail intact.

1. Identify assets for disposal

Start with routine asset audits and practical triggers. You flag assets that have reached the end of their useful life, break down too often, sit unused, or no longer match your operating strategy. The goal is to stop carrying assets that no longer earn their place in your operations.

2. Determine the book value and fair value of the asset

Your finance team calculates net book value by subtracting accumulated depreciation from the acquisition cost. Then you estimate fair value using relevant market references, recent second-hand pricing, or a professional appraisal for high-value items. This step stops you from guessing. It also helps you choose the method that makes the most sense financially.

3. Select the most appropriate disposal method

Now you decide based on data. If fair value looks strong and there is demand, selling often gives the best recovery. If the asset has no realistic value, scrapping keeps things clean and reduces risk. If you plan a replacement and a vendor offers a trade-in, you can simplify procurement.

If you want CSR impact and the asset still has usable life, donation can work. The important part is consistency. You want a decision you can explain in one sentence without sounding like you improvised.

4. Execute the disposal process

Execution is where controls matter most. If you sell the asset, keep the negotiation trail, invoice, and proof of payment. If you scrap electronics, handle data before the device leaves your site. Ask yourself this: would you feel okay if someone recovered the drive tomorrow?

For Malaysia, PDPA makes this more than a best practice when devices may contain employee or customer personal data. You should apply a clear data sanitization process and keep proof of what you did.

5. Document and record the accounting entries

Documentation is not paperwork for the sake of paperwork. It is what protects you during audits and internal reviews. Keep a disposal request, approvals, valuation evidence, disposal proof, and vendor documents where relevant. In Malaysia, this matters even more when disposal affects capital allowances or involves scheduled wastes.

Then your finance team records the journal entry, removes the asset and accumulated depreciation, and captures any gain or loss so the financial statements reflect reality.

Accounting for Asset Disposal: Journals and Calculations

Disposal accounting has one job: remove the old asset cleanly and capture the financial result of letting it go. If you do it well, your fixed asset register stays accurate, and your income statement tells the truth.

1. How to calculate gain or loss on disposal

You calculate gain or loss by comparing what you receive from disposal with the net book value at disposal date. The basic formula stays simple: proceeds minus net book value. A positive result gives you a gain. A negative result gives you a loss. You typically present this as a non-operating item so readers can separate disposal outcomes from day-to-day operating performance.

2. Example journal entries for each disposal method

Your journal entry should remove the asset’s cost and its accumulated depreciation from the books. In a sale, you debit Cash and Accumulated Depreciation, credit the Fixed Asset account, then record the balancing difference as either Gain on Disposal or Loss on Disposal so the entry balances.

Trade-ins add complexity because you also recognize the new asset and the trade-in value, but the core idea stays the same. You close the old asset properly and support every number with documents.

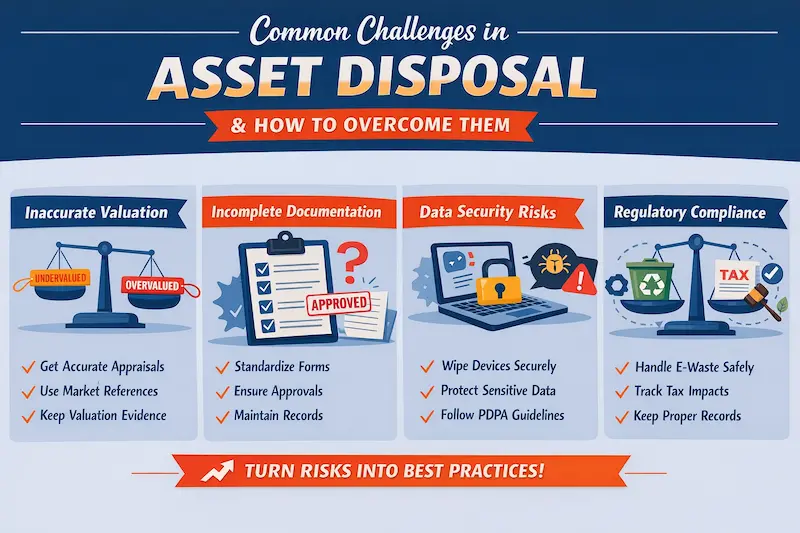

Common Challenges in the Asset Disposal Process and How to Overcome Them

Disposal problems usually show up in four places: valuation, documentation, data security, and compliance. If you control these, disposal turns into a routine instead of a risk.

1. Inaccurate asset valuation

Old assets can be difficult to price. If you undervalue, you lose recovery value. If you overvalue, you waste time and distort your gain or loss calculation. Use appraisers for high-value items and market references for common assets. Then keep evidence. The goal is not perfect pricing. The goal is defensible pricing.

2. Lack of complete documentation

Missing documents turn disposal into an audit trap. People forget who approved what and why. You can fix this by Implement standardized procedures by formalizing forms and making approvals non-negotiable. When every disposal follows the same documentation checklist, your process becomes faster and easier to defend.

3. Data security risks in electronic assets

A disposed device can still carry sensitive company data and personal data. Without proper wiping, you expose your business to reputational damage and regulatory risk. For Malaysia, PDPA raises the stakes, so build a clear sanitization procedure, follow it every time, and keep proof of completion.

4. Compliance with environmental and tax regulations

Some assets come with extra rules. Electronics and certain components can connect to scheduled waste handling requirements, while disposal can also impact tax outcomes when capital allowances apply. Malaysia’s scheduled wastes framework and capital allowance rules both reward one habit: documentation that matches the numbers and the disposal method.

The Role of Technology in Optimizing the Asset Disposal Process

If you run the asset lifecycle through spreadsheets and scattered files, disposal becomes slower and riskier than it needs to be. Depreciation drifts, approvals get lost, and teams disagree on the latest asset status. Then an audit arrives, and everyone starts searching for evidence at the same time.

Technology can help when it supports a clear workflow. A good system centralizes asset records, keeps depreciation consistent, stores disposal evidence, and reduces manual journal work. But it will not save a weak process. If the workflow stays unclear, software only helps you move faster in the wrong direction.

Conclusion

Asset disposal is not just an admin task. It is where you close an asset’s lifecycle in a way that keeps your financial statements honest, your operations tidy, and your audit trail easy to defend. A consistent process helps you avoid ghost assets, cut valuation mistakes, and make decisions based on numbers, not guesswork.

Keep it simple: choose the right method for the asset’s condition and value, execute it with clear controls, then document everything so finance can record the transaction properly. In Malaysia, this discipline matters because disposal can affect tax outcomes, e-waste handling, and data protection when devices contain personal information. When records, documents, and entries stay aligned, disposal becomes a routine that supports better planning.

HashMicro offers the ideal solution for businesses seeking to streamline their general ledger management. Request a free demo today and see firsthand how HashMicro’s software can streamline your accounting processes, improve accuracy, and drive financial efficiency.

Frequently Asked Questions

-

What is the difference between asset disposal and depreciation?

Depreciation is the process of allocating an asset’s cost over its useful life to reflect its decline in value. In contrast, asset disposal is the physical and accounting act of removing the asset from the books when it is no longer in use. Depreciation occurs during ownership, while disposal happens at the end of the asset’s lifecycle.

-

When is the right time to perform an asset disposal?

The right time to dispose of an asset is when it no longer provides economic value to the company. This can occur when it is fully depreciated, severely damaged beyond economical repair, technologically obsolete, or no longer fits the company’s changing operational needs.

-

How does asset disposal affect a company’s taxes?

Asset disposal can impact a company’s tax liability through the recognized gain or loss. A gain on sale is typically considered taxable income, while a loss can often be used to reduce taxable income. Furthermore, donating assets to qualified organizations may result in tax deductions, making it essential to consult with a tax professional.

-

What assets typically go through the disposal process?

Nearly all types of fixed assets eventually undergo disposal. Common examples include company vehicles, office equipment like computers and furniture, manufacturing machinery, and properties such as buildings or land that are no longer used for core business activities.