Accounting has served as a cornerstone of business transparency for centuries. In today’s modern landscape, accounting software is the essential foundation for financial health, providing real-time precision and accuracy. This evolution aligns perfectly with Malaysia’s Digital Economy Blueprint (MyDIGITAL), which encourages local enterprises to adopt cloud-based financial solutions to enhance regional competitiveness

Understanding and implementing a comprehensive Trial Balance can be a solution for overcoming these operational challenges. Leveraging a digital Trial Balance ensures that a company’s financial recording process remains fast, accurate, and highly efficient in an increasingly competitive market.

Utilizing a trial balance is key to long-term efficiency and sound data management. To ensure healthy financial records, accounting software plays an essential role in maintaining accuracy and decision-making stays on track.

Key Takeaways

|

Understanding Trial Balance

Trial Balance is a key accounting report used to verify that total debits and credits are equal within a double-entry system. By identifying discrepancies like errors or missing entries, it ensures data integrity.

Trial Balance effectively bridges the gap between daily transaction recording and the preparation of accurate financial statements. By streamlining data management, it boosts operational efficiency and significantly reduces errors before data is processed. A trial balance document isn’t a formal document that can be shared with external parties

Data from trial balance supports informed decision-making by providing a reliable snapshot of a company’s financial health. With precise financial reporting, businesses can maintain compliance, improve planning, and strengthen overall financial performance.

Why is Trial Balance Important?

Trial Balance’s main goal is to ensure that total debit and credit balances in the general ledger remain perfectly equal. This equilibrium reflects the core principle of double-entry accounting, where every transaction impacts at least two accounts with matching values.

Beyond detecting clerical errors, a verified Trial Balance streamlines the preparation of formal financial statements. It serves as the authoritative data source for generating accurate income statements, balance sheet for business, and statements of owner’s equity.

1. Detecting Calculation Errors

The primary purpose of a trial balance is to detect discrepancies between total debits and credits, which serve as immediate indicators of potential mistakes in journal entries or ledger postings. These errors often manifest as incorrect calculations, transposed figures, or inaccuracies in recording specific account balances.

When an imbalance is identified, accountants can promptly investigate and rectify the issue before moving to the next phase of the accounting cycle. This proactive detection minimizes the risk of compounding errors and ensures that financial data remains reliable and accurate.

2. Providing a foundation for financial statement preparation

Once all account balances are compiled and confirmed to be in equilibrium, the trial balance acts as a definitive blueprint for preparing key financial statements. Revenue and expense balances are extracted directly from this document to develop the income statement.

All verified financial data organized in a single cohesive document that makes the reporting process significantly more systematic and efficient. Furthermore, this ensures consistent alignment between internal records with external reports.

3. Supporting internal and external audit activities

For both internal and external auditors, the trial balance can help simplify the entire audit process. It provides a high-level summary of a company’s financial transactions for a specific period, allowing auditors to gain appropriate testing procedures.

Auditors can trace selected transactions, confirm the validity, and assess whether the financial statements fairly represent the company’s position. This alignment with applicable accounting standards ultimately strengthens the credibility and transparency of the organization.

3 Types of Trial Balance in Accounting

There are three types of Trial Balance in accounting with different purposes for the financial reporting process. It’s important to understand the differences between these types to ensure the accounting data is correct and accurate for a financial report.

1. Unadjusted Trial Balance

The unadjusted trial balance is the first draft prepared at the end of an accounting period, immediately after all day-to-day transactions have been posted from the journal to the general ledger. This aims to identify any mathematical errors or posting discrepancies before the adjustment process begins.

The document contains the raw balances of all accounts, providing a starting point for accountants to see which entries require further attention or end-of-period adjustments.

2. Adjusted Trial Balance

The adjusted trial balance is created after adjusting journal entries have been recorded and posted. This type is the most critical one because it reflects the true financial position of the company under the accrual-based accounting principles.

Once the debits and credits in this report are confirmed to be equal, it serves as the official source of data for constructing the primary financial statements, including income statement and balance sheet.

3. Post-Closing Trial Balance

The post-closing trial balance is the final check performed after the closing entries have been completed. All temporary accounts, such as revenues, expenses, and dividends, have been closed and their balances transferred to retained earnings, leaving them with a zero balance.

This report only lists permanent accounts, which include assets, liabilities, and equity. Its purpose is to verify that the ledger is in perfect equilibrium and ready to begin the new fiscal period without any carry-over errors from the previous cycle.

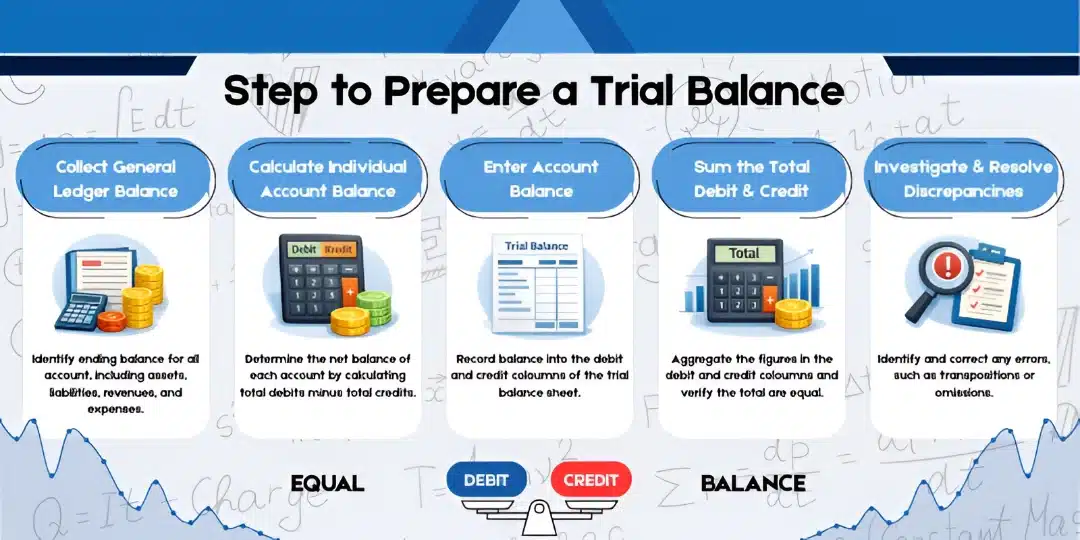

How to Create a Trial Balance?

Creating a trial balance requires a systematic and well-structured approach to ensure every financial transaction is accurately recorded and remains balanced. In today’s modern technology, implementing a standardized workflow is essential for preserving data integrity and minimizing reporting errors.

Many companies use modern accounting software to simplify and improve the efficiency of the trial balance process. A clear and organized trial balance preparation process not only improves accounting accuracy, but also supports compliance, financial transparency, and efficient decision-making.

1. Collect General Ledger Balances

Identify and list the final ending balances for every account within the general ledger, including assets, liabilities, equity, revenues, and expenses. It is critical to verify that every business transaction for the specific accounting period has been accurately recorded and posted to ensure the data is complete.

2. Calculate Individual Account Balance

Once all postings are finalized, determine the net balance for each ledger account by calculating the difference between total debits and total credits. Accounts where debits exceed credits will carry a debit balance, while those with higher credits will result in a credit balance. These calculation stages prevent minor mathematical discrepancies from accumulating and causing an imbalance in the final report.

3. Enter Account Balances

Record each account’s balance into the appropriate debit or credit column of your trial balance sheet. Typically, assets and expenses are placed in the debit column, while liabilities, equity, and revenues are recorded in the credit column. This step represents the key stage in the verification process.

4. Sum the Total Debits and Credits

Sum the figures in the debit column and repeat the process for the credit column to find the grand totals. For the trial balance to be considered successful, these two sums must be exactly equal, proving that the accounting equation remains in equilibrium. This step helped confirm that at every debit recorded, there was a corresponding and equal credit.

5. Investigate and Resolve Discrepancies

If the column totals don’t match, it must conduct a thorough investigation of journal entries, ledger postings, and prior calculations to pinpoint the source of the error. Common issues such as transposition errors or omitted entries must be corrected immediately to ensure the integrity of the data. Resolving these discrepancies is essential to adjusting entries and formal financial reporting.

Example of Trial Balance

The table below provides a representation of a standard trial balance, showcasing the essential structure used by finance professionals to verify ledger accuracy. The first column lists each specific account name, followed by dedicated columns for Debit and Credit entries. In accordance with the principles of normal balances, each account will hold a figure in only one of these two columns, depending on its classification as an asset, liability, equity, revenue, or expense.

The ultimate goal of this document is to ensure that the grand totals of both columns are equal. This mathematical equilibrium confirms that the company’s transaction recording process has strictly adhered to the double-entry accounting principle.

| Account Name | Debit (RM) | Credit (RM) |

|---|---|---|

| Cash | 150,000 | |

| Accounts Receivable | 75,000 | |

| Inventory | 120,000 | |

| Office Equipment | 80,000 | |

| Accounts Payable | 90,000 | |

| Owner’s Capital | 250,000 | |

| Service Revenue | 180,000 | |

| Salary Expense | 55,000 | |

| Rent Expense | 20,000 | |

| Total | 500,000 | 500,000 |

Common Errors in Trial Balance

A balanced trial balance doesn’t always guarantee accuracy, it’s proven by WorldCom’s $180 billion financial collapse because manipulated $3.8 billion by capitalizing expenses. This case underscores the necessity through data verification in modern accounting, as it demonstrates how easily high-level discrepancies can bypass basic checks.

Although a trial balance ensures mathematical equilibrium between total debits and credits, it is not foolproof and can still conceal underlying accounting errors within the general ledger. Therefore, understanding these hidden discrepancies is essential for maintaining data accuracy and ensuring the total integrity of financial reporting.

1. Transposition Errors

A transposition error occurs when two adjacent digits are accidentally reversed during data entry, for example recording RM220,000 as RM250,000. While this is a common human mistake, it inevitably causes an imbalance in the trial balance totals. Identifying these errors quickly is essential for maintaining data integrity, as even a small swap can lead to significant discrepancies in final financial reporting.

2. Posting Errors

Posting errors occur when a correct transaction amount is recorded on the correct side (debit or credit), but is assigned to the wrong ledger account. For instance, a payment for “Rent Expense” might be mistakenly posted to “Utilities Expense,” which misleads management regarding departmental spending while keeping the trial balance totals equal. Detailed charts of accounts and automated validation is essential to ensure that every figure resides in the proper category.

3. Error of Omission

An error of omission happens when a business transaction is completely excluded from the accounting records, meaning neither the debit nor the credit side was ever entered. Because the double-entry system remains mathematically balanced despite the missing data, this error is difficult to detect through a trial balance. To catch these omissions, companies have to review source documents like invoices and receipts.

4. Duplicate transactions

A duplicate transaction error arises when the same entry is recorded and posted to the general ledger more than once. This inflation of both debits and credits allows the trial balance to remain in equilibrium, masking the fact that assets, expenses, or revenues are overstated. Regular audits and modern accounting software are the most effective ways to eliminate redundancies and ensure accurate financial statements.

Trial Balance in Modern Financial

In today’s modern landscape, trial balance has undergone a radical transformation driven by advanced financial automation. Modern financial software and Enterprise Resource Planning (ERP) systems have automated these repetitive workflows, empowering finance teams to shift their focus from data entry to high-level financial analysis and strategic decision-making. Here are key features of a modern accounting system:

- Unified System Integration: Data from diverse departments, including sales, procurement, and inventory flows directly into the general ledger.

- Real-Time General Ledger Updates: Modern software captures every transaction immediately based on the double-entry principle.

- Automated Bank Reconciliation: Enhances accuracy through simple record-matching, significantly reducing manual entry errors and speeding up the closing process.

- Advanced Financial Management:

On-Demand Trial Balance: Generate precise financial snapshots instantly for stakeholders.

Comprehensive Reporting: Detailed analytics that offer deep insights into how the business is running.

Multi-Currency Support: Essential for managing international trade and global transactions easily.

- Optimized Data Flow: Integrated ERP modules ensure that financial data moves easily across the entire business for maximum transparency.

These integrated ERP systems ensure that every transaction is captured immediately following the double-entry principle, maintaining a ledger that is perpetually current. As a result, a trial balance can be generated on-demand with total precision, providing stakeholders with real-time visibility into the company’s financial health and operational efficiency.

Automation with Accounting Software

Accounting software fundamentally change how companies manage their trial balance. This software automatically posts every transaction from various modules into the general ledger in real-time.

When a user needs to view the trial balance, the system can generate it instantly without any manual calculations, which drastically reduces the risk of transposition or posting errors. With integrated financial software features, managers can access accurate data at any time for faster and more informed decision-making, transforming a once-tedious task into a powerful analytical resource.

Optimize Your Business Financial Management with ERP System

ERP system designed to automate and simplify business processes, including trial balance management. With a comprehensive solution, companies can overcome challenges such as slow reporting, manual data errors, and the difficulty of tracking financial status in real-time.

Through its advanced Accounting Software module, companies can process transactions faster, reduce human error, and obtain accurate data in real-time. The system is equipped with features for automatic approval workflows, real-time tracking, and direct integration with other modules.

ERP software is designed with full integration between modules, so data from various departments such as accounting, inventory, purchasing, and sales can be interconnected. This provides better visibility into the entire business operation and ensures that every decision is based on accurate and up-to-date information.

ERP for Accounting Software Features:

- Real-Time General Ledger: Automatically updates all accounts as transactions occur, ensuring the trial balance can be generated instantly with the most current data.

- Automated Bank Reconciliation: Streamlines matching bank statements with company records, reducing manual effort and ensuring cash balances are always accurate.

- Comprehensive Financial Reporting: Generates a wide range of financial reports, including the trial balance, income statement, and balance sheet, with just a few clicks.

- Multi-Currency Management: Supports transactions in multiple currencies and automatically handles conversions and revaluations, which is ideal for businesses operating internationally.

- Seamless Integration with Other Modules: Connects flawlessly with sales, purchasing, and inventory modules to ensure data flows smoothly across the business, eliminating data silos.

Enhance operational efficiency, data transparency, and business process automation. To see how accounting software can concretely help your business, do not hesitate to try our free demo now.

Conclusion

Trial balance is a component of the accounting cycle, serving as a primary pillar for ensuring the accuracy and integrity of financial data. The trial balance role is crucial as a first line of defense in detecting errors. By identifying errors early, businesses can prevent minor mistakes from escalating into significant reporting failures.

Amid the rapid technological advancements, the process of preparing a trial balance has evolved from a time-consuming manual task into an efficient automated function. Integrating modern accounting software and ERP systems, also mastering the trial balance is the key to maintaining a transparent, efficient, and reliable financial foundation.

Experience firsthand modern accounting software tools can simplify your trial balance process. Try and explore free demo to see how automation can resolve your issues!

FAQ About Trial Balance in Accounting

-

What is the main difference between a Trial Balance and a Balance Sheet?

Trial Balance is an internal check to ensure debits and credits match, while a Balance Sheet is a formal financial statement showing a company’s assets, liabilities, and equity for external stakeholders.

-

How is a Trial Balance different from Financial Statements?

Trial Balance is a preliminary diagnostic tool used to verify ledger accuracy. Financial statements are the final products that are used to communicate business performance after all data is verified.

-

What should you do if a trial balance doesn’t balance?

First, calculate the exact difference between total debits and credits, then check for transposition errors or omitted entries. Re-verify all balance transfers and ensure every transaction follows double-entry principles before calculating the totals again.

-

How is the Trial Balance related to audits?

It serves as the primary starting point for both internal and external audits by providing a summarized view of all account balances. Auditors use it to trace transactions, identify high-risk discrepancies, and verify that the financial statements are grounded in accurate ledger data.