For businesses, understanding what is superannuation is essential for compliance and payroll accuracy. Superannuation is a mandatory retirement savings system where employers contribute a set percentage of an employee’s earnings into a super fund. These funds are then invested to grow over time.

The system also supports long-term financial stability. It reduces reliance on the Age Pension and helps workers build retirement savings throughout their careers. Therefore, employers play a direct role in supporting employee outcomes.

In practice, businesses must follow strict rules around handling super contributions, payments, and reporting. Missing obligations can lead to penalties, so staying informed and organised is critical.

Key Takeaways

Superannuation is a mandatory system where businesses contribute a percentage of employee earnings into retirement funds.

The Super Guarantee rate is increasing over time, requiring businesses to apply the correct percentage to employee earnings.

Most employees and some contractors qualify for super, making correct classification essential for compliance.

Super must be paid on time, as late payments result in penalties and additional charges.

What Is Superannuation?

To answer what is superannuation, it helps to look at how it works in real terms. Employers must contribute a percentage of an employee’s earnings into a super fund, where the money is invested until retirement.

Superannuation sits within a three-part retirement system. It works alongside the Age Pension and voluntary contributions, creating a combined safety net for workers after they stop working.

From a legal perspective, superannuation is governed by the Superannuation Guarantee laws. This means contributions are not optional, and businesses must meet strict obligations set by the tax office.

Once contributions are paid, the money belongs to the employee. The business simply processes and transfers it, so accuracy and timing are essential to avoid penalties.

Australian financial platforms can be used to manage superannuations by centralising contributions, automating compliance checks, and giving employers real-time visibility over staff fund balances.

What Is the Current Super Guarantee Rate?

The Super Guarantee rate is the minimum percentage businesses must contribute to employee super funds. It increased to 11.5% from 1 July 2024 and will reach 12% by 1 July 2026.

This percentage applies to Ordinary Time Earnings, so businesses must calculate it correctly. Errors in this area often lead to underpayments and compliance issues.

To apply the rate properly, you need to understand what counts as earnings.

What counts as Ordinary Time Earnings

OTE generally includes:

- Base salary and wages for standard hours

- Shift loadings for evenings or weekends

- Commissions linked to performance

- Bonuses tied to ordinary work

- Paid leave such as annual or sick leave

- Most allowances, except reimbursements

What is excluded from OTE

Some payments do not attract super:

- Overtime payments outside normal hours

- Expense reimbursements such as travel costs

- Parental leave payments in most cases

- Workers’ compensation when not working

- Lump sum termination payments

Maximum contribution base

There is also a quarterly cap on super contributions. For example, businesses only need to apply the SG rate up to the maximum earnings threshold per quarter, which limits excessive contributions.

Who Do You Need to Pay Super For?

Most workers are entitled to super, including full-time, part-time, and casual employees. Even small earnings qualify, as the previous minimum threshold no longer applies.

Standard employees

Businesses must pay super for employees regardless of residency status. This also includes directors and family members working in the company.

Under 18 rule

Employees under 18 must work more than 30 hours in a week to qualify. Therefore, businesses need to track weekly hours carefully to stay compliant.

Contractors and labour rules

Contractors may still qualify for super if they are paid mainly for their labour. If they cannot delegate work and are paid for time rather than results, super usually applies.

How does superannuation work?

Superannuation builds over time through employer contributions and investment growth. It continues until the employee reaches retirement conditions.

Accumulation period

During employment, businesses calculate and send contributions to a super fund. These funds invest the money across different assets to grow balances over time.

Super funds include:

- Industry funds that return profits to members

- Retail funds run by financial companies

- Public sector funds for government workers

- Corporate funds set up by large companies

- Self-managed funds controlled by members

How super is taxed

Super has tax advantages but still includes some tax rules:

- Contributions are generally taxed at 15%

- Investment earnings are also taxed up to 15%

- Withdrawals after age 60 are usually tax free

Accessing super

Employees can access super once they reach preservation age and meet release conditions. Retirement is the most common trigger, although limited early access options exist.

When Is Super Due?

Super payments must be made on time to avoid penalties. Businesses usually pay quarterly, with strict deadlines set after each quarter ends.

If a payment arrives late, even by one day, the Super Guarantee Charge applies. This includes interest and extra fees, which are not tax deductible.

Superannuation laws are enforced strictly, so businesses must follow payment schedules closely and maintain accurate records.

How Superannuation Applies Across Sectors

Different industries face unique challenges when applying super rules. Workforce structure and pay types often affect compliance.

1. Retail and hospitality

These sectors rely on casual and younger workers. Therefore, managers must track hours carefully, especially for employees under 18.

2. Construction and trades

Contractor arrangements are common, but many still qualify for super. Businesses must assess each contract to avoid misclassification risks.

3. Healthcare and services

Salary packaging is widely used, so super must be calculated on the correct earnings. Accuracy is critical to avoid compliance issues.

4. Technology and professional services

Higher salaries often exceed contribution thresholds. Super payment tracking software must apply caps correctly to prevent overpayments.

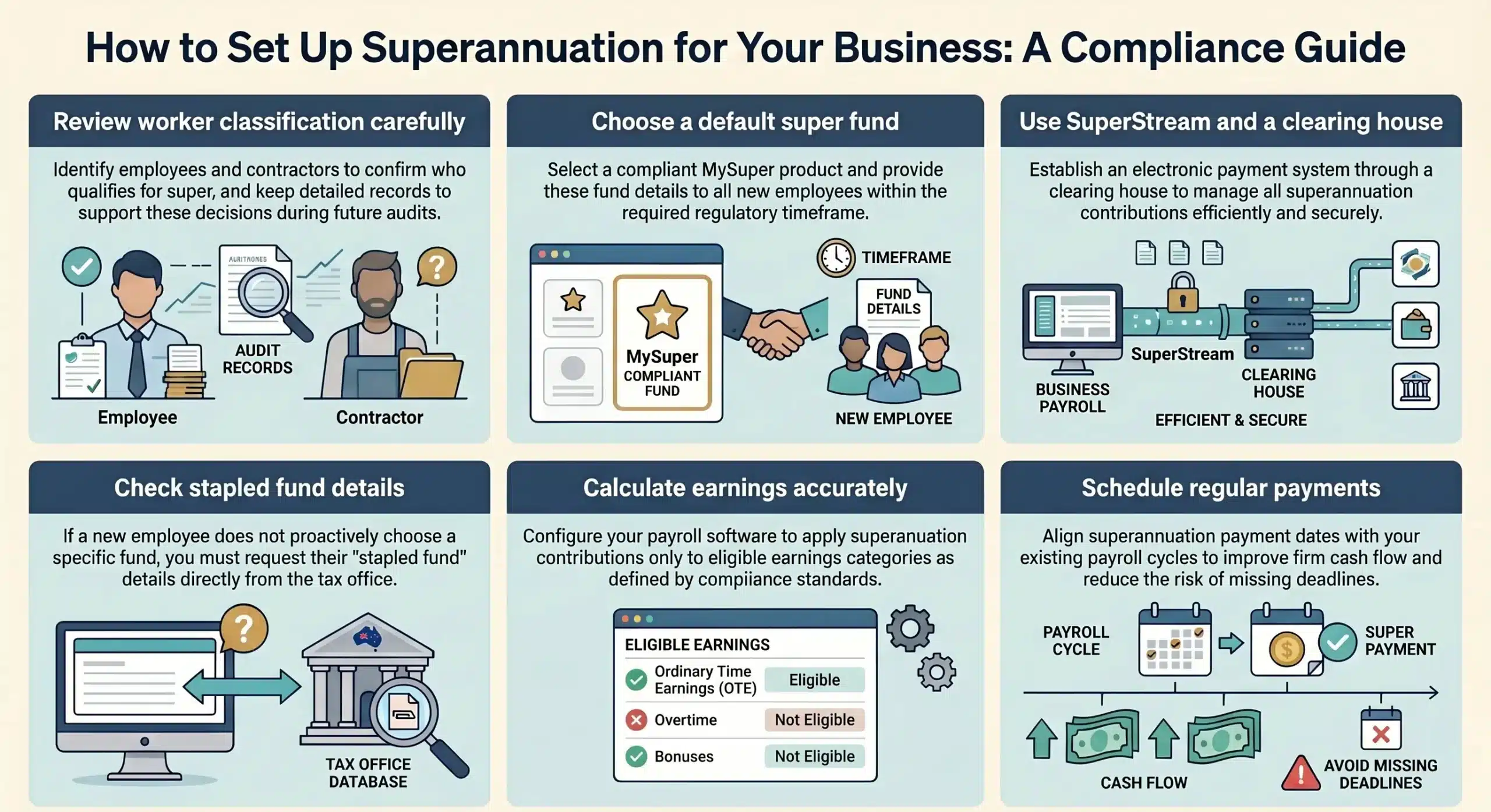

Setting Up Superannuation for Your Business

Setting up super correctly ensures smooth payroll and avoids penalties. A structured approach and super-compliant payroll tools makes compliance easier to manage.

- Review worker classification carefully

Identify employees and contractors, then confirm who qualifies for super. Keep records to support decisions during audits. - Choose a default super fund

Select a compliant MySuper product and provide details to new employees within the required timeframe. - Use SuperStream and a clearing house

Set up electronic payments through a clearing house to manage contributions efficiently. - Check stapled fund details

Request fund details from the tax office if an employee does not choose a fund. - Calculate earnings accurately

Configure payroll to apply super only to eligible earnings categories. - Schedule regular payments

Align payments with payroll cycles to improve cash flow and reduce missed deadlines.

Common Superannuation Pitfalls and How to Avoid Them

Superannuation errors can lead to serious penalties, so prevention is essential. Utilizing a system for super payments reliably overcome these issues.

1. Missing deadlines

Late payments trigger extra charges and remove tax deductions. To avoid this, process payments early to allow for clearing times.

2. Contractor misclassification

Incorrectly treating contractors as exempt can result in back payments. Always assess working arrangements carefully.

3. Incorrect earnings calculations

Mistakes in OTE lead to underpayments or overpayments. Regular payroll reviews help maintain accuracy.

4. Poor record keeping

Businesses must keep records for at least five years. Store documents centrally to ensure easy access during audits.

Advanced Superannuation Practices for Forward-Thinking Employers