Navigating corporate finance requires a clear understanding of how a company funds its growth. Every business must strike a careful balance between using its own equity and borrowing external funds. This capital structure is the foundation for managing risk, ensuring long-term stability, and maximizing shareholder value.

Relying too heavily on borrowed money exposes a business to significant vulnerabilities. As highlighted in resent research of corporate financial risk and capital structure, high leverage severely restricts managerial flexibility. The study, which analyzed over 1,200 firm-year observations, revealed a stark negative correlation (Coefficient = -9.399, p < 0.001) between a firm’s gearing ratio and its capacity to fund long-term sustainability initiatives. However, avoiding debt altogether can mean missing out on critical expansion opportunities.

To measure this delicate balance, analysts and managers rely on the gearing ratio. By using the proper gearing ratio formula, stakeholders gain a clear, mathematical snapshot of a company’s leverage. It strips away qualitative noise, revealing exactly how much of the business is funded by creditors versus shareholders to guide sound strategic planning.

Key Takeaways

|

Understanding the Concept of Gearing in Business Finance

Gearing or financial leverage measures the proportion of a company’s operations funded by interest-bearing debt versus shareholder equity. “Highly geared” firms rely heavily on debt instruments like bonds and loans, while “low gearing” indicates a preference for equity financing through shares or retained earnings.

This concept is rooted in the fundamental accounting equation, where the gearing ratio specifically analyzes the internal balance between liabilities and equity on the right side of the ledger.

Understanding this balance is critical because debt and equity carry distinct trade-offs. Debt is generally cheaper due to tax-deductible interest and creditor priority, but it imposes fixed obligations that can lead to insolvency if unmet. However, equity is more expensive and dilutive but requires no mandatory payments, providing a vital financial cushion during economic downturns.

The Core Gearing Ratio Formula Explained

The term “gearing ratio” is actually a broad category that encompasses several different calculations, all designed to measure financial leverage. However, when financial professionals refer to the gearing ratio formula, they are typically referring to one of two primary calculations. Understanding both variations is crucial for comprehensive financial analysis.

The Debt-to-Equity Gearing Formula

The most common and straightforward gearing ratio formula compares total debt directly to total equity. The mathematical expression is:

Gearing Ratio = (Total Debt / Total Equity) × 100

In this formula:

- Total Debt: This includes all interest-bearing liabilities. It encompasses both short-term debt (obligations due within one year, such as short-term bank loans and the current portion of long-term debt) and long-term debt (obligations due after one year, such as bonds payable and long-term bank loans). It is important to note that non-interest-bearing operational liabilities, such as accounts payable or accrued expenses, are typically excluded from this calculation.

- Total Equity: This represents the total shareholders’ equity as reported on the balance sheet. It includes common stock, preferred stock, additional paid-in capital, and retained earnings.

This formula is often expressed as a percentage. For example, a gearing ratio of 60% indicates that for every dollar of equity, the company has 60 cents of debt.

The Debt-to-Capital Gearing Formula

An alternative, and sometimes preferred, gearing ratio formula calculates the proportion of debt relative to the total capital employed by the business. Total capital is the sum of total debt and total equity. The mathematical expression is:

Gearing Ratio = [Total Debt / (Total Debt + Total Equity)] × 100

This variation is particularly useful because it shows the percentage of the company’s total financing that is provided by creditors. A result of 40% using this formula means that 40% of the company’s total capital structure is made up of debt, while the remaining 60% is equity. Both formulas are valid and widely used. The choice between them often depends on regional preferences, industry standards, or the specific requirements of a financial institution or analyst. The key is to be consistent in the application of the chosen formula when comparing multiple companies or tracking a single company’s performance over time.

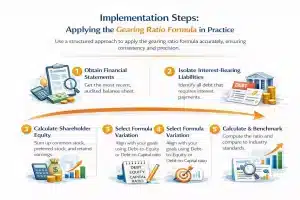

Implementation Steps: Applying the Gearing Ratio Formula in Practice

Applying the gearing ratio formula effectively requires a systematic approach to ensure accuracy and consistency. Whether you are a business owner evaluating your own capital structure or an analyst reviewing a prospective investment, follow these core implementation steps:

- Step 1: Obtain the Latest Financial Statements. Gather the company’s most recent balance sheet. Ensure the data is audited and up-to-date to reflect the current financial reality.

- Step 2: Isolate Interest-Bearing Liabilities. Carefully identify all forms of debt that require interest payments. This includes long-term bank loans, corporate bonds, lease obligations, and short-term debt. Exclude non-interest-bearing operational liabilities, such as accounts payable and accrued expenses.

- Step 3: Calculate Total Shareholder Equity. Sum up all equity components, encompassing common stock, preferred stock, additional paid-in capital, and retained earnings.

- Step 4: Select the Appropriate Formula Variation. Choose the specific gearing ratio formula that aligns with your analytical goals most commonly the debt-to-equity ratio or the debt-to-capital ratio.

- Step 5: Calculate and Benchmark. Plug the extracted figures into your chosen formula, express the result as a percentage, and benchmark it against historical company data and direct industry competitors.

Translating a mathematical formula into a professional audit requires a systematic approach to data collection and verification. The following steps provide the necessary framework to move from a theoretical calculation to a practical, real-world application of the gearing ratio.

Step-by-Step Guide on How to Calculate Gearing Ratio

To truly master the gearing ratio formula, it is helpful to walk through a practical, step-by-step calculation using a hypothetical company’s financial statements. Let us consider “Global Tech Manufacturing Ltd.” a mid-sized industrial equipment producer, and calculate its gearing ratio for the fiscal year ending 2023.

Step 1: Locate and Aggregate Total Debt

The first step is to examine the company’s balance sheet to identify all interest-bearing debt. Do not simply take the “Total Liabilities” figure, as this includes operational liabilities that do not carry interest and therefore do not represent financial leverage in the traditional sense. Looking at Global Tech Manufacturing’s balance sheet:

- Short-Term Bank Loans: $500,000

- Current Portion of Long-Term Debt: $200,000

- Long-Term Corporate Bonds: $2,500,000

- Long-Term Bank Mortgages: $800,000

- Accounts Payable: $400,000 (Exclude – non-interest bearing)

- Accrued Taxes: $150,000 (Exclude – non-interest bearing)

Calculation:

$500,000 + $200,000 + $2,500,000 + $800,000 = $4,000,000 Total Debt.

Step 2: Locate Total Shareholders’ Equity

Next, locate the shareholders equity section on the balance sheet. This section represents the residual interest in the assets of the entity after deducting all its liabilities. Looking at Global Tech Manufacturing’s balance sheet:

- Common Stock: $1,000,000

- Preferred Stock: $500,000

- Retained Earnings: $3,500,000

Calculation:

$1,000,000 + $500,000 + $3,500,000 = $5,000,000 Total Equity.

Step 3: Apply the Gearing Ratio Formula

Now, we can apply both variations of the gearing ratio formula to understand Global Tech Manufacturing’s leverage position.

Using the Debt-to-Equity Formula:

Gearing Ratio = ($4,000,000 / $5,000,000) × 100 Gearing Ratio = 0.80 × 100 = 80%

Using the Debt-to-Capital Formula:

- Total Capital = $4,000,000 (Debt) + $5,000,000 (Equity) = $9,000,000

- Gearing Ratio = [$4,000,000 / $9,000,000] × 100 Gearing Ratio

- Gearing Ratio = 0.444 × 100 = 44.4%

By following these precise steps, analysts can avoid common pitfalls, such as inadvertently including accounts payable in the debt calculation, which would artificially inflate the perceived financial risk of the company.

Interpreting Gearing Ratio Results

Calculating the number is only the first step; the true value lies in correctly interpreting what the result means for the business. The interpretation of a gearing ratio is highly contextual, but there are general guidelines that financial professionals follow.

| Gearing Level | Typical Threshold | Core Meaning | Key Implications |

|---|---|---|---|

| High Gearing | > 50% | Aggressively financing growth with debt. | Magnifies profits and losses. High ROE during growth, but carries a high risk of default during downturns. Very sensitive to interest rate fluctuations. |

| Low Gearing | < 25% - 30% | Conservative structure relying primarily on equity and retained earnings. | Financially stable and low-risk. However, it may indicate overly conservative management missing out on cheap debt to fuel expansion. |

Gearing Ratio vs. Debt-to-Equity Ratio: Key Differences

The Impact of Gearing on Financial Risk and Return

The strategic decision of how to structure a company’s capital and consequently, its gearing ratio has a profound impact on both the risk profile of the business and the potential returns for its investors. This dynamic is often referred to as the “double-edged sword” of financial leverage.

The Leverage Effect on Profitability

To understand the upside of gearing, one must understand how debt can amplify returns. Imagine a company that has an opportunity to invest $1,000,000 in a new production facility that will generate a 15% annual return ($150,000).

Scenario A: Zero Gearing (100% Equity) If the company uses $1,000,000 of shareholder equity to fund the project, the return on equity (ROE) is simply 15% ($150,000 return / $1,000,000 equity).

Scenario B: 50% Gearing (50% Debt, 50% Equity) Now, suppose the company funds the project with $500,000 of equity and borrows $500,000 from a bank at an annual interest rate of 5%. The project still generates $150,000. However, the company must pay $25,000 in interest ($500,000 × 5%). The net profit is $125,000 ($150,000 – $25,000). Now, calculate the ROE: $125,000 net profit / $500,000 equity = 25%. By introducing debt (gearing), the company successfully amplified the shareholders’ return on investment from 15% to 25%.

This mathematical phenomenon is why private equity firms and aggressive corporate managers frequently utilize high gearing ratios; it is a powerful tool for maximizing shareholder wealth during good economic times.

Risks During Economic Downturns

The downside of gearing becomes apparent when the economic environment shifts. Let us revisit the previous example, but imagine a severe recession hits, and the new production facility only generates a 3% return ($30,000).

- Scenario A: Zero Gearing The company makes $30,000. The ROE drops to 3%. While disappointing, the company is fundamentally safe. It has no mandatory interest payments to make.

- Scenario B: 50% Gearing The project generates $30,000, but the company still owes the bank $25,000 in fixed interest payments. The net profit is reduced to a mere $5,000. The ROE plummets to 1% ($5,000 / $500,000). Worse still, if the project generated a 0% return, the company with zero gearing simply breaks even. The geared company, however, loses $25,000 and must fund that interest payment from cash reserves or by selling assets.

This illustrates how high gearing ratios drastically compress the margin of error for a business and elevate the risk of insolvency during difficult periods.

Sector-Specific Gearing Ratio Benchmarks

A common mistake made by novice financial analysts is attempting to evaluate a gearing ratio in a vacuum. A ratio of 60% might be dangerously high for one type of business but perfectly normal—and even optimal—for another. To conduct a comprehensive financial ratio analysis, one must compare the company’s gearing against specific industry benchmarks.

Capital-Intensive Industries

Industries that require massive upfront investments in physical assets naturally operate with higher gearing ratios.

- Telecommunications and Utilities: Companies in these sectors must build extensive infrastructure (cell towers, power plants, electrical grids) before they can generate a single dollar of revenue. Because these companies typically enjoy highly stable, predictable, and often regulated cash flows, banks are willing to lend them massive sums of money. It is not uncommon to see utility companies operating safely with gearing ratios between 60% and 80%.

- Airlines and Shipping: Purchasing fleets of aircraft or cargo ships requires billions of dollars. These industries rely heavily on debt financing and lease agreements. Consequently, their gearing ratios are historically high, making them highly sensitive to fuel price shocks and global economic slowdowns.

- Real Estate Investment Trusts (REITs): Real estate is inherently a debt-driven industry. REITs use mortgages to acquire properties, aiming to generate rental income that exceeds the mortgage interest. A gearing ratio of 50% to 70% is standard in commercial real estate.

Asset-Light and Technology Sectors

Conversely, industries that do not require significant physical infrastructure typically operate with much lower gearing ratios.

- Software as a Service (SaaS) and Technology: Tech companies rely on intellectual property and human capital rather than factories and machinery. Because their assets are largely intangible, banks are often hesitant to provide traditional debt financing. Furthermore, the rapid pace of technological change makes their future cash flows less predictable than a utility company. As a result, tech companies usually rely heavily on venture capital and equity financing, resulting in gearing ratios that are frequently below 20%, and sometimes completely debt-free.

- Consulting and Professional Services: Law firms, accounting agencies, and management consultants require very little capital to operate. Their primary expense is payroll. Therefore, they have little need for long-term debt, and their gearing ratios are typically negligible.

When evaluating a company’s gearing ratio formula output, the analyst must ask: “Is this ratio appropriate for the specific operational realities and cash flow predictability of this specific industry?”

Strategies to Manage and Improve Your Gearing Ratio

A company’s gearing ratio is not static; it fluctuates continuously as debts are paid down, new loans are taken out, and profits are generated or lost. Corporate management teams must actively manage their capital structure to maintain an optimal gearing ratio. If a company finds its gearing ratio has drifted too high or too low, several strategic levers can be pulled.

Strategies for Reducing a High Gearing Ratio (Deleveraging)

If a company is over-leveraged and facing pressure from creditors or the threat of a credit downgrade, management must take steps to reduce the gearing ratio.

- Debt Repayment via Retained Earnings: The most organic way to reduce gearing is to improve operational profitability and use the excess cash flow to aggressively pay down principal debt balances. This reduces the numerator in the gearing ratio formula.

- Equity Issuance: A company can issue new shares of common or preferred stock to the public or private investors. The capital raised is then used to retire debt. This is a highly effective dual-action strategy: it simultaneously decreases total debt (the numerator) and increases total equity (the denominator), causing the gearing ratio to drop rapidly. However, this strategy dilutes the ownership percentage of existing shareholders.

- Asset Sales and Divestitures: Management can choose to sell off non-core assets, underperforming divisions, or excess real estate. The cash generated from these sales is immediately deployed to pay off debt.

- Reducing Dividend Payments: By cutting or suspending dividend payments to shareholders, a company retains more of its net income within the business. This increases the retained earnings account, which boosts total equity and naturally lowers the gearing ratio over time.

Strategies for Increasing a Low Gearing Ratio (Leveraging Up)

If a company is under-leveraged and wishes to optimize its cost of capital and boost shareholder returns, it can employ strategies to increase its gearing.

- Debt-Funded Expansion: The company can take out bank loans or issue corporate bonds to finance the acquisition of a competitor, build new manufacturing facilities, or heavily fund research and development. This increases the numerator in the formula.

- Share Repurchases (Buybacks): A highly popular strategy in modern corporate finance is using cash reserves—or even borrowing money specifically for this purpose—to buy back the company’s own shares on the open market. When shares are repurchased, they are retired, which reduces total shareholder equity (the denominator). This mathematically increases the gearing ratio and concentrates future earnings among a smaller pool of remaining shares, driving up Earnings Per Share (EPS).

- Special Dividends: The company can issue a massive, one-time cash payment to shareholders. This drastically reduces retained earnings (lowering equity) and pushes the gearing ratio upward.

Common Mistakes When Analyzing Gearing Ratios

Even seasoned financial professionals can make errors when calculating and interpreting the gearing ratio formula. Being aware of these common pitfalls is essential for accurate financial analysis.

Ignoring Off-Balance Sheet Financing

A dangerous pitfall is missing off-balance sheet liabilities, such as operating leases, which can make a company’s debt look artificially low. While modern accounting rules have closed many of these loopholes by requiring leases to be recorded, you must still carefully check the financial footnotes to ensure all hidden, debt-like obligations are included in your calculations.

Overlooking the Cost of Debt

A high gearing ratio isn’t always bad if the borrowed money is cheap. Analysts often focus on total debt volume while ignoring the interest rates. Locked-in, low fixed rates mean efficient capital use, whereas variable rates can quickly cause a cash flow crisis. Always pair the gearing ratio with the interest coverage ratio to assess true debt affordability.

Failing to Benchmark by Industry

Comparing gearing ratios across different sectors is a major analytical error. Capital-intensive industries like real estate naturally carry higher debt, so a 60% ratio might be perfectly healthy. However, that exact same ratio could signal severe distress for a software startup. Always benchmark a company’s leverage strictly against direct competitors and historical industry averages.

Confusing Book Value with Market Value

When calculating equity, analysts often default to the historical “book value” found on the balance sheet. This can severely understate a company’s true worth, especially for modern businesses with strong intangible assets. Using the market value of equity (market capitalization) often provides a much more realistic picture, preventing a robust company from appearing artificially over-leveraged.

Advanced Practices in Leverage Analysis

To gain a truly comprehensive view of financial leverage, advanced practitioners never look at the gearing ratio in isolation. Instead, they employ dynamic trend analysis, tracking the ratio over multiple quarters or years. This longitudinal approach helps identify deliberate shifts in corporate strategy, such as a multi-year deleveraging plan, or serves as an early warning system for emerging financial distress.

Advanced financial modeling also involves stress-testing the gearing ratio under various adverse economic scenarios. Analysts will model how a sudden 2% hike in interest rates or a 15% drop in operating revenue would impact the company’s ability to maintain its current capital structure.

Furthermore, seasoned professionals consistently pair gearing metrics with the interest coverage ratio. While the gearing ratio formula calculates the absolute, structural level of debt, the interest coverage ratio reveals whether the company generates sufficient operating income (EBIT) to actually service that debt. Combining these two metrics provides a holistic, bulletproof assessment of both capital structure composition and long-term debt sustainability.

Conclusion

The gearing ratio is a vital tool for assessing a company’s financial structure and long-term health. It clearly illustrates the balance between interest-bearing debt and shareholder equity. By providing a mathematical snapshot of leverage, it helps stakeholders ignore qualitative noise. Maintaining this balance is essential for ensuring stability while pursuing aggressive growth. It remains a foundational metric for any robust risk management strategy.

Correct interpretation depends heavily on industry benchmarks and current economic conditions. Analysts must look beyond simple percentages to evaluate debt maturity and interest rates. A ratio that works for a utility company may signal crisis for a tech startup. Avoiding common pitfalls requires a deep dive into financial footnotes and market values. This comprehensive view allows for better strategic navigation during market shifts.

Calculating these metrics manually often increases the risk of errors and strategic delays. Modern businesses rely on automated tools for real-time visibility into their capital structure. Advanced software streamlines reporting, ensuring your financial data is always accurate and actionable. This efficiency allows leadership to focus on high-level goals rather than manual data entry. To see how our system simplifies financial analysis, schedule a free demo today.

FAQ About Gearing Ratio Formula

-

How do creditors and investors view high gearing differently?

Creditors prioritize capital preservation and use the gearing ratio to assess default risk, often setting “debt covenants” to limit borrowing. Conversely, investors often favor strategic gearing as a tool to amplify Return on Equity (ROE) and maximize shareholder wealth during periods of economic growth.

-

Why should analysts scrutinize financial footnotes when calculating gearing?

Footnotes often reveal “hidden” or off-balance sheet liabilities, such as operating leases and contingent debts, that are not visible on the main balance sheet. Ignoring these details can result in an artificially low gearing ratio, leading to a false sense of financial security.

-

Why is a “good” gearing ratio entirely dependent on the industry?

Capital-intensive sectors like utilities or real estate can safely handle higher gearing due to stable, predictable cash flows. In contrast, asset-light industries like SaaS or technology typically maintain low gearing because their lack of physical collateral makes high debt loads much riskier.

-

How does debt maturity affect the interpretation of a gearing ratio?

The gearing ratio only shows the volume of debt, not when it is due. A company with high short-term debt faces immediate refinancing risks if interest rates rise, whereas a company with long-term, fixed-rate debt is much more stable, even if their total gearing percentages are the same.

-

Why is it important to pair gearing with the interest coverage ratio?

While the gearing ratio measures the structural composition of capital, the interest coverage ratio measures a company’s ability to pay its interest obligations from current earnings. Together, they confirm if a company’s debt levels are both structurally sound and operationally sustainable.