Malaysia’s e-invoicing mandate is gradually changing how businesses handle billing and tax compliance. Introduced by the Inland Revenue Board of Malaysia (LHDN) in collaboration with MDEC, the system is designed to modernise the country’s tax infrastructure. However, not every business or transaction falls within the scope of this mandate.

Whether you are a small enterprise just getting to grips with Malaysia’s digital invoicing requirements, a finance professional navigating complex transaction categories, or a compliance officer determining your organisation’s obligations, this guide provides everything you need.

Understanding which categories qualify for an e-invoice exemption is important not only to avoid penalties but also to make sound compliance decisions. This guide covers who qualifies, which transactions are excluded, how to apply for an exemption, and what obligations still apply even during an exemption period.

Key Takeaways

Table of Content

|

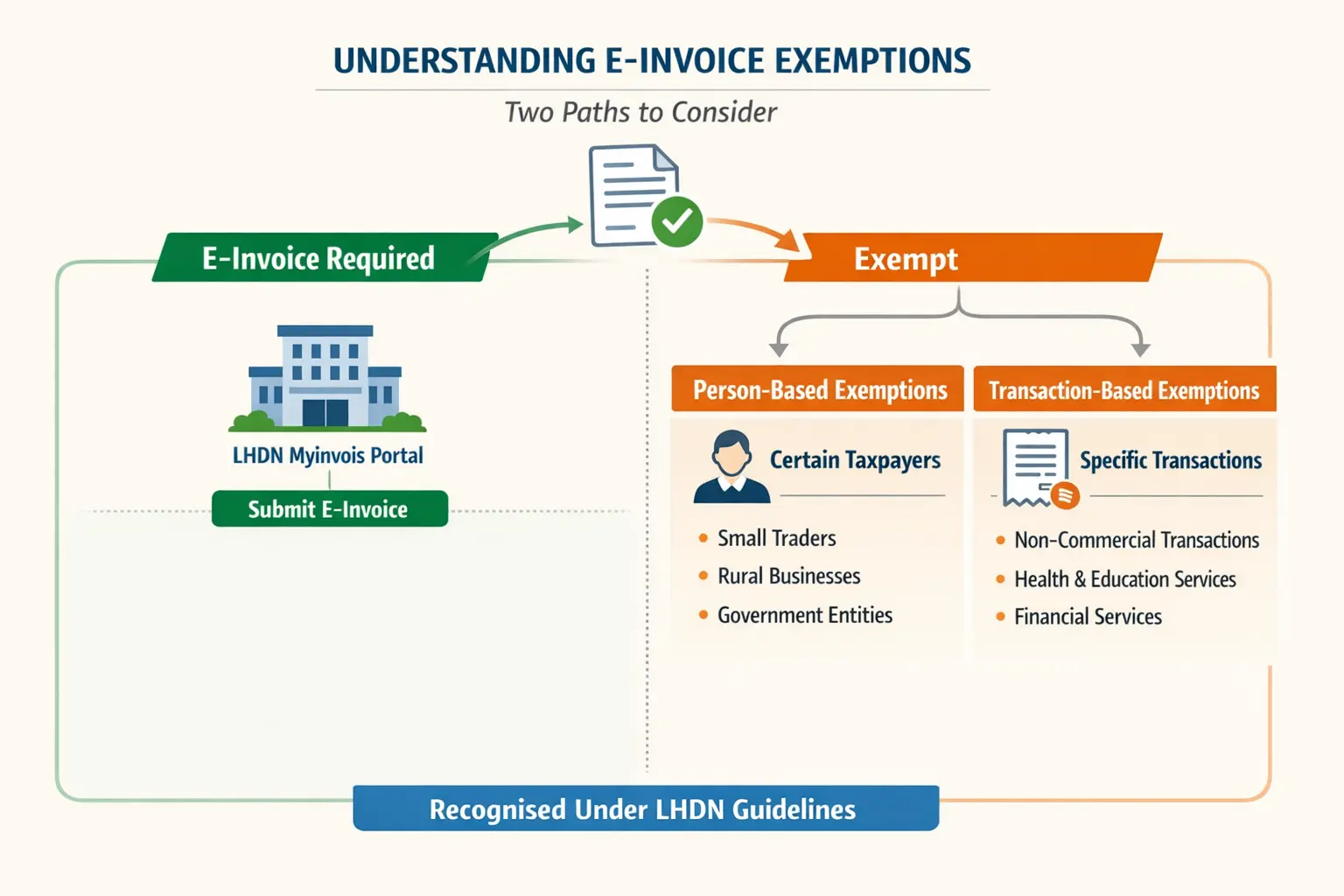

What Is E-Invoice Exemption and Why Does It Matter?

An e-invoice exemption is a formal or categorical exclusion that allows certain taxpayers or specific transaction types to be exempt from issuing or receiving e-invoices through LHDN’s MyInvois portal.

These exemptions are not administrative workarounds. Rather, they are deliberate policy decisions that recognise the practical differences across business sizes, industries, and transaction types. For example, the ‘validate-then-submit’ workflow in MyInvois works smoothly for large corporations with ERP systems but can be challenging for small traders, rural businesses, or entities handling non-commercial transactions.

There are two types of exemptions to understand:

- Person-based exemptions, apply to specific categories of taxpayers who are excluded from the e-invoice requirement entirely.

- Transaction-based exemptions, apply to particular types of transactions, even when the issuing party would otherwise be required to issue e-invoices.

Both types are recognised under LHDN’s official guidelines. Understanding the difference between them is the first step toward accurate compliance decisions.

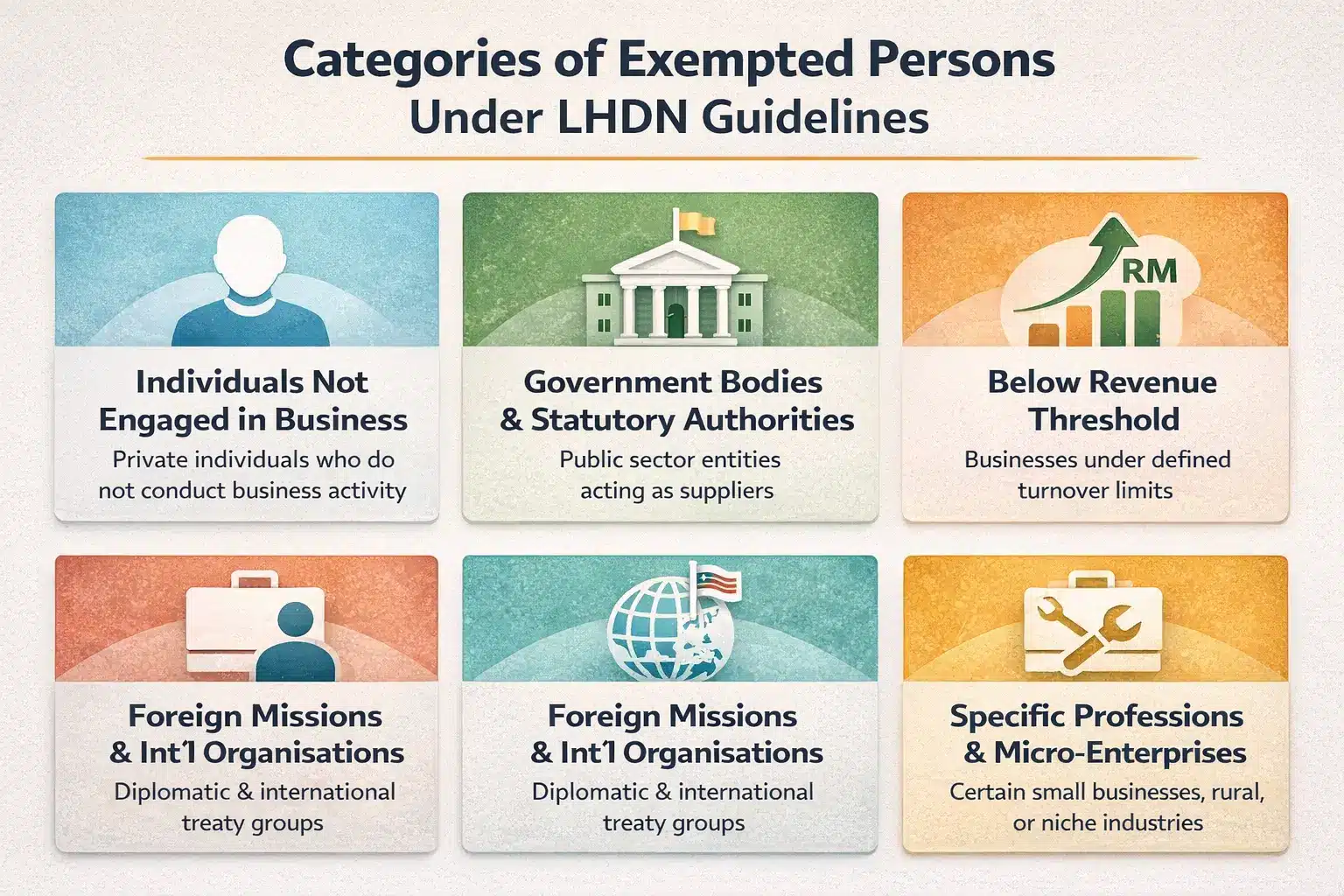

Categories of Exempted Persons Under LHDN Guidelines

LHDN identifies specific categories of taxpayers who are either permanently or temporarily exempt from issuing e-invoices. In most cases, exemptions are not automatic they require either formal application, fall within defined revenue thresholds, or are governed by statutory provisions.

1. Individuals Not Engaged in Business

Private individuals who do not conduct any business activity are exempt. For instance, someone selling a personal asset does not fall within the e-invoice mandate. However, if that same individual operates a business even informally their obligations may change depending on turnover and business registration.

2. Government Bodies and Statutory Authorities (as Suppliers)

Certain government entities and statutory bodies, when acting as suppliers, may be exempt from issuing e-invoices. This reflects both the unique nature of government billing and the logistical challenges of integrating public sector systems with MyInvois within short timeframes.

Note that government bodies receiving invoices from private businesses are not exempt from requiring their vendors to issue e-invoices.

3. Taxpayers Below the Revenue Threshold

The most widely applicable exemption covers businesses whose annual turnover falls below defined thresholds. Malaysia’s e-invoice implementation has been phased based on revenue brackets:

- Phase 1 (August 2024): Businesses with annual turnover above RM100 million.

- Phase 2 (January 2026): Businesses with annual turnover between RM25 million and RM100 million.

- Phase 3 (July 2026): All remaining taxpayers conducting business in Malaysia.

Businesses that have not yet reached their phase’s go-live date are in a temporary exemption period, not permanently exempt. Once their phase begins, full compliance is required. However, during the interim period, they are not required to issue e-invoices and may continue using conventional invoicing methods.

4. Foreign Missions, Embassies, and International Organisations

Diplomatic missions and international organisations operating under formal treaty arrangements generally qualify for exemptions due to their privileged legal status under instruments such as the Vienna Convention.

5. Specific Individual Professions and Micro-Enterprises

Certain very small businesses and sole proprietors may apply for exemption where the compliance burden is deemed disproportionate to the regulatory benefit. LHDN has shown flexibility here, particularly for rural businesses, cottage industries, and micro-traders with limited internet access or technical capacity.

Understanding the e-invoice implementation timeline and requirements in Malaysia is essential for any business attempting to determine where it sits within these categories and what obligations will apply once each phase is enforced.

Exempted Transaction Types: What Transactions Are Excluded?

Even where a business is not categorically exempt, certain types of transactions may still be excluded from e-invoice requirements. These transaction-based exclusions are especially relevant for sectors that involve complex or sensitive billing arrangements.

1. Employment Income

Salary payments and employment-related compensation are excluded. Employers do not need to issue e-invoices for wages, bonuses, or similar payments. Employment income is already documented under the EA (Employment Act) and reported through the PCB (Potongan Cukai Bulanan) payroll deduction system, so adding e-invoices would create unnecessary duplication.

2. Alimony and Maintenance Payments

Payments made for alimony, maintenance, or similar legally mandated personal financial obligations are also excluded. These transactions are personal in nature and do not constitute commercial activity.

3. Disposal of Investments

Transactions involving stocks, shares, bonds, and similar instruments are excluded. Such transactions are documented through securities settlement systems and brokerage statements, processes that are separate from standard commercial invoicing.

4. Disposal of Real Property

The sale or transfer of real property including land, buildings, and permanent fixtures is excluded from e-invoice requirements. Property transactions in Malaysia are already governed by a comprehensive legal framework including instruments like sale and purchase agreements, transfer forms, and stamp duty documentation that makes additional e-invoice requirements redundant.

5. Dividend Payments

Dividend distributions to shareholders are excluded. Dividends are documented through dividend vouchers, tax certificates, and company resolutions, which already satisfy Companies Act provisions and tax reporting obligations.

6. Government Grants and Subsidies

Government grants, subsidies, and similar non-commercial payments are excluded. These disbursements are policy instruments not commercial exchanges and standard e-invoicing documentation is neither appropriate nor required.

7. Zakat, Sadaqah, and Religious Contributions

Religious payments including zakat (obligatory Islamic almsgiving) and sadaqah (voluntary charitable giving) are excluded. These transactions are governed by Islamic law principles and administered through established religious authorities with their own accountability frameworks.

8. Certain Financial Instruments and Transactions

Transactions involving specific financial instruments, derivatives, and banking activities may also be excluded, depending on their nature and existing regulatory oversight. Banks and financial institutions already operate under Bank Negara Malaysia’s prudential frameworks, which impose documentation requirements that are distinct from commercial e-invoicing.

For businesses dealing with more complex billing arrangements, it is also worth understanding how self-billed e-invoices work in Malaysia, as certain exempted transaction categories may still require alternative documentation approaches where the buyer, rather than the supplier, issues the invoice.

How to Apply for E-Invoice Exemption Through LHDN

For businesses that believe they qualify for an exemption but are not automatically excluded by a clearly defined category, LHDN provides a formal application process.

Step 1: Determine Your Eligibility Basis

Before initiating any application, clearly identify the legal or regulatory basis for the exemption before starting any application. The basis whether revenue threshold, business type, or transaction category determines what supporting documents are required.

Step 2: Prepare Supporting Documentation

Compile relevant documents, which typically include:

- Business registration certificates and SSM filings

- Latest audited financial statements or management accounts demonstrating annual turnover

- a description of business activities and the transactions for which exemption is sought

- and any relevant statutory provisions or regulatory approvals that support your exemption claim

Step 3: Submit Your Application to LHDN

Applications for e-invoice exemptions are submitted through LHDN’s official channels, which may include the MyTax portal or specific correspondence with the LHDN branch handling your tax file. LHDN has indicated that applications should be submitted with sufficient lead time before the applicable implementation phase date to ensure timely processing.

Step 4: Await LHDN’s Decision

LHDN will review the application and may request additional information. Do not treat a pending application as an approved exemption. Formal written confirmation from LHDN is required before any transaction is treated as exempt.

Step 5: Maintain Records of Exemption Approval

Once an exemption is granted, businesses must maintain proper records of the approval documentation. These records may be requested during tax audits or compliance reviews. The exemption approval letter from LHDN should be treated as a critical compliance document and stored securely within your financial records management system.

Common Misconceptions About E-Invoice Exemption in Malaysia

Given the complexity of Malaysia’s e-invoice framework, several misconceptions have emerged among business owners, accountants, and compliance teams. Addressing these directly helps ensure decisions are based on accurate information.

Misconception 1: “If My Business Is Small, I’m Automatically Permanently Exempt”

This is one of the most common and dangerous misconceptions. Small businesses below the current phase threshold are in a temporary exemption period, not a permanent one. Phase 3 (July 2026) brings all remaining businesses into the e-invoice mandate, regardless of size. Planning for compliance as early as possible is essential.

Misconception 2: “Exempt Transactions Don’t Need Any Documentation”

As discussed earlier, exemption from e-invoicing does not mean exemption from documentation. Businesses must still issue appropriate conventional invoices or receipts and maintain full financial records. The exemption relates specifically to the obligation to submit documentation through the MyInvois portal, not to documentation requirements generally.

Misconception 3: “B2C Transactions Are Fully Exempt”

While there are specific provisions that acknowledge the unique challenges of high-volume B2C transactions particularly in retail B2C transactions are not categorically exempt from e-invoicing. LHDN has introduced a “consolidated e-invoice” mechanism that allows businesses to issue a single e-invoice covering multiple B2C transactions over a period, rather than individual e-invoices for every sale. This is an accommodation, not a full exemption.

Misconception 4: “Receiving an Exempted Invoice Means I Don’t Need to Report It”

From the buyer’s perspective, receiving an invoice for an exempted transaction does not eliminate the need to properly account for that expense in the business’s financial records and tax returns. Tax deductibility, input tax claims (where SST is involved), and proper expenditure recording obligations remain regardless of the invoice’s e-invoice status.

Misconception 5: “The Exemption Application Process Is Simple and Always Approved”

LHDN treats exemption applications seriously and will not approve applications that do not meet the established criteria. Businesses must submit well-documented applications with clear justification, and there is no guarantee of approval unless the eligibility criteria are clearly and convincingly met. Attempting to claim exemption without formal LHDN approval is a compliance risk that could expose businesses to penalties.

Preparing for Full Compliance: Steps Businesses Should Take Now

Even if your business currently qualifies for an e-invoice exemption whether based on revenue, business type, or transaction category the direction of travel in Malaysia is clearly toward universal e-invoice compliance over time. Preparing right now rather than waiting reduces operational risk and makes the transition smoother.

Conduct a Comprehensive Invoice Audit

Map out every type of invoice your business issues and receives. Categorise each by transaction type, counterparty type (B2B, B2C, B2G), and the applicable regulatory framework. This reveals which transactions will require e-invoice compliance in future phases.

This audit will reveal which transactions may be exempt now but will require e-invoice compliance in the future, and which transactions may be exempt permanently.

Evaluate Your Current Invoicing Technology

Assess whether your existing accounting or ERP software supports integration with MyInvois. Many enterprise-grade solutions already offer or are developing API connectivity with LHDN’s platform.

Train Your Finance and Accounts Teams

E-invoice compliance is not just a technology question it is also a people and process question. Your finance team needs to understand the new documentation workflows, the validation process, the treatment of rejected or cancelled e-invoices, and the record-keeping requirements.

Investing in training now will reduce errors and compliance risks when full implementation is required.

Engage Your Tax Advisor or Accountant

Given the evolving nature of Malaysia’s e-invoice guidelines with LHDN issuing multiple rounds of updated guidelines, supplementary FAQs, and sector-specific guidance engaging a qualified tax professional is strongly advisable. An experienced advisor can help you determine your exact obligations, identify genuinely applicable exemptions, and ensure your compliance posture is defensible in the event of an audit.

Stay Updated on LHDN Announcements

LHDN has demonstrated a willingness to adjust implementation timelines, expand exemption categories, and issue clarifying guidance as the e-invoice rollout progresses. Monitoring LHDN’s official website, gazette notifications, and authorised announcements ensures that your business is always working with the most current information.

This is particularly important for businesses in transitional phases or those that have applied for exemptions that may be subject to periodic review.

Consider a Pilot Implementation

Even if your business is not yet required to issue e-invoices, voluntarily piloting the system with a subset of transactions can be extremely valuable. It allows your team to identify integration challenges, understand the validation and rejection workflow, and build internal capacity before mandatory compliance dates arrive. LHDN encourages voluntary early adoption and has made MyInvois available for this purpose.

Penalties for Non-Compliance and the Risk of Incorrectly Claiming Exemption

Understanding exemptions also requires understanding the consequences of getting them wrong. Malaysia’s Income Tax Act 1967 and the specific provisions enacted to support the e-invoice framework impose penalties for non-compliance that businesses must take seriously.

Penalties Under the Income Tax Act

Failure to issue e-invoices when required or issuing non-compliant invoices can result in penalties under Section 120 of the Income Tax Act. These can include fines, surcharges, and in serious cases, criminal prosecution

Audit and Investigation Risk

Businesses that claim exemptions without proper documentation face elevated audit risk. LHDN can cross-reference tax registries, and inconsistencies between declared exemption claims and actual transaction patterns are likely to attract attention during routine reviews.

Reputational and Commercial Risk

Beyond regulatory penalties, businesses that fail to comply with e-invoice requirements or that are found to have improperly claimed exemptions face reputational damage that can affect their commercial relationships. Increasingly, large corporations and government procurement officers are requiring their suppliers to demonstrate e-invoice compliance as a condition of doing business, making non-compliance a commercial disadvantage as well as a legal one.

Conclusion

E-invoice exemptions in Malaysia are carefully calibrated provisions not permanent escape routes. From person-based exclusions to specific transaction types, the framework acknowledges the diversity of Malaysia’s economic landscape while maintaining a clear trajectory toward universal digital compliance.

As Malaysia’s digital invoicing environment continues to mature, the businesses that navigate it best will be those that use the exemption period not as a reason to delay, but as an opportunity to prepare. Mapping your invoice types, evaluating your technology stack, training your team, and engaging a qualified tax advisor are all steps that pay dividends regardless of when your compliance deadline arrives.

What matters most for any business is not simply identifying whether an exemption applies today, but understanding the full scope of that exemption, what compliance obligations persist during the exemption period, and how to prepare for the eventual end of that exempted status.

FAQ about E-Invoice Exemption In Malaysia

-

Does my business need to apply for an e-invoice exemption, or is it automatic?

It depends on the category. Businesses below the current phase threshold are in an automatic temporary exemption period. However, most other exemptions particularly those based on business type or specific circumstances require a formal application to LHDN with supporting documentation.

-

What happens if I incorrectly claim an e-invoice exemption?

Incorrectly claiming an exemption exposes your business to penalties under Section 120 of the Income Tax Act, audit risk, and potential reputational damage. Always obtain formal written confirmation from LHDN before treating any transaction as exempt.

-

Are all B2C transactions exempt from e-invoicing?

No. B2C transactions are not categorically exempt. LHDN offers a ‘consolidated e-invoice’ option that allows businesses to issue a single e-invoice covering multiple B2C transactions within a period but this is an operational accommodation, not a full exemption.

-

How long does it take for LHDN to process an exemption application?

Processing timelines vary depending on the complexity of the application and current application volumes. LHDN recommends submitting applications well before the applicable implementation phase date. Do not assume approval unless you have received formal written confirmation.