A project reaches 80% completion, yet the margin that started at 15% has quietly eroded to 6%. The finance team traces it back and discovers material cost overruns from Phase 2 that went unnoticed until supplier invoices stacked up at month end. By then, the damage was already done.

This is not a rare occurrence. According to a survey of Malaysian contractors registered with CIDB, 96% agreed that most construction projects face cost overruns, typically between 5% and 10% of the contract sum. The root cause is rarely incompetence. It is visibility. Actual cost data only becomes complete after invoices are processed, often weeks after spending has occurred. At that point, options for course correction are limited.

Construction accounting software addresses this gap by consolidating cost tracking, project progress, and cashflow into a single system. Instead of discovering budget overruns at month end, project teams can identify deviations within weeks, while there is still room to renegotiate with suppliers, reallocate resources, or adjust scope before small variances snowball into significant losses.

Key Takeaways

|

More than Just Numbers on a Spreadsheet

Construction accounting is a specialized field tailored to the financial and operational complexities of the construction industry. It deals with unique challenges such as extended project durations, intricate cost breakdowns, and detailed contract requirements.

Unlike traditional manufacturing, construction is project-driven. Each project varies in scope, location, and resources. This variability makes it harder for construction firms to achieve the same level of efficiency as businesses operating in stable, repetitive production environments.

Why Construction Firms Need Specialised Accounting

- Margins are thin, and visibility is slow

Construction typically operates on single digit margins. A 3% cost overrun on a RM 20 million project is RM 600,000 gone. If that overrun only surfaces when invoices are reconciled at month end, the window for correction has already closed. - Cash comes in stages, not streams

Progress claims, retention, variation orders, and liquidated damages all affect when money actually arrives. A project can be profitable on paper but cause cashflow stress if billings lag behind actual expenditure. Construction accounting ties revenue recognition to physical progress, not just invoice dates. - Multiple projects mean multiple blind spots

Running five jobs simultaneously sounds manageable until one underperforming site quietly drains resources from the others. Without job level tracking, the profitable projects subsidise the struggling ones, and no one notices until annual accounts reveal the damage. - Disputes are expensive, and documentation is the only defence

Variation claims, extension of time requests, and final account negotiations all depend on records. A clear audit trail is not just compliance. It is leverage.

Hashy AI Fact

Need to know!

Hashy AI supports construction accounting by improving visibility into equipment utilization and maintenance costs across varied, project-based environments.

Request a free demo today!

Difference between Construction Accounting and Regular Accounting

While the core principles of accounting remain consistent across industries, the practical demands of construction accounting set it apart from more traditional approaches.

In regular accounting, such as in retail, service, or manufacturing businesses, revenue tends to be straightforward, operations are centralized, and costs are easier to anticipate. Meanwhile, construction introduces a more complex, project-driven model that requires specialized handling. Here are the key differences:

| Aspect | Regular Accounting | Construction Accounting |

|---|---|---|

| Project-Based vs. Operational Accounting | Revolves around product lines, retail outlets, or standardized services. | Project-specific, with each job having unique scopes, risks, and financial requirements. |

| Centralized vs. Mobile Operations | Businesses typically operate from fixed, centralized locations. | Construction companies work across multiple sites with a mobile workforce. |

| Simple vs. Complex Contracts | Standard contracts with single-point payments. | Custom, long-term contracts with staged billing, retainage, and progress-based revenue recognition. |

| Stable vs. Volatile Cost Structures | Direct costs are predictable and consistent. | Costs vary due to fluctuating labor, materials, compliance, and project-specific factors. |

| Minimal vs. Frequent Scope Changes | Product or service changes are rare and limited. | Change orders are frequent and must be documented, priced, and tracked accurately. |

These differences also highlight the importance of structured project controls in construction.

Explore how punch lists support construction project workflows.

Financial Statements in Construction Accounting

To do that, construction firms rely on a set of specialized financial statements tailored to the industry’s complex demands.

Here are the five reports that make or break a project’s financial outcome.

1. Work-in-Progress (WIP) Schedule

The WIP schedule acts as an early warning system, flagging the gap between work completed and what’s actually been billed. For a general contractor managing a six-month infrastructure build in Selangor, spotting that gap early is the difference between smooth cash flow and a rush to pay vendors.

When used consistently, WIP reports help firms recognize revenue more accurately and adjust before overruns silently eat into profits. Miss it, and the real damage only shows up when it’s too late to fix.

2. Construction-in-Progress (CIP) Report

While WIP highlights what’s been billed, the CIP report focuses on what’s been spent. It tracks the accumulation of project costs in real time (labor, materials, subcontractors) against progress milestones.

For example, a firm building a mixed-use tower in Kuala Lumpur might use the CIP to detect whether costs are front-loading too early. Without that visibility, it’s easy to underestimate expenses, only to find out halfway through that the project’s margin has already collapsed.

3. Job Cost Sheets

If the P&L is the big picture, job cost sheets are the close-up lens. These reports dissect every detail, from labor, materials, equipment, to subcontractor costs on a project-by-project basis.

For a Penang-based contractor juggling multiple renovations, these sheets reveal when one job quietly starts drifting off budget. The real value is when decision-makers can intervene early before a minor deviation snowballs into a margin wipeout.

4. Profit and Loss (P&L) Statement

The P&L shows whether the numbers actually add up at the end of the day, or if something quietly went wrong. It captures total income and expenses, but its real power lies in comparison.

A firm handling public roadwork in Johor and private builds in Shah Alam can use the P&L to spot which project types consistently pull profits and which ones, despite appearances, might not be worth bidding on again.

5. Balance Sheet

In construction, the balance sheet tells a more layered story than most. Beyond assets and liabilities, it captures industry-specific figures. Retention still held by clients, upfront mobilization advances, or the slow depreciation of tower cranes parked onsite.

For Malaysian firms preparing to bid on government contracts or secure financing from banks, this isn’t just paperwork. It’s proof of stability, liquidity, and operational credibility. A single line item out of place can mean the difference between winning a tender or missing out entirely.

These differences also make it important to understand how materials and on-site resources should be managed to keep construction costs accurate. Understand site inventory control for construction sites.

Common Mistakes in Construction Accounting

At this point, you have learned that accounting for construction is complex with its own challenges. And with challenges often come mistakes that, at the very least, waste contractors’ time to correct them.

What kind of mistakes do contractor accountants usually make? Here are the six main mistakes to pay attention to:

1. Disorganization

For small contractors, staying financially organized often takes a back seat to more immediate chaos—like shifting project timelines and unpredictable labor availability.

But neglecting the structure of your accounting process doesn’t just create clutter; it opens the door to deeper problems: missed costs, tax missteps, and budget overruns that go unnoticed until it’s too late.

The fix isn’t always more manpower. Often, it’s smarter systems, like construction accounting software.

2. Poor Job Cost Estimates

Behind many failed projects is a single underestimated bid. Costing a job too low can lead to razor-thin—or nonexistent—margins. Price it too high, and the work disappears into a competitor’s pipeline.

The risk doesn’t stop at profit margins either: for firms using percentage-of-completion accounting, bad estimates distort revenue recognition and financial statements.

3. Inaccurate Recognition of Joint Ventures

Joint ventures are a fixture in large construction projects, often formed to spread financial risk and combine resources. But they also come with complex accounting demands—and missing them can quietly distort your books.

Depending on how much control or capital a company brings to the table, it may need to apply very different accounting treatments. Yet, many firms only discover this after the reporting period ends, when it’s far harder—and costlier—to correct.

4. Incorrect Overhead Calculations

Overhead is the silent variable that can skew job costing without warning. Contractors often spread overhead as a percentage across projects, but when that base calculation is off, so is everything else.

The challenge? Construction overhead is notoriously volatile. Office rent, insurance, maintenance, even training; they fluctuate, and they’re easy to overlook.

If those costs aren’t reviewed regularly and factored in properly, profits shrink without anyone noticing until the numbers no longer add up.

5. Mismanaged Change Orders

Change orders can be profit engines or silent liabilities. On paper, they offer contractors a chance to bill for additional work and keep projects adaptive. But when accepted through casual, undocumented conversations onsite, they often slip through; unpriced, unapproved, and poorly tracked.

As a result, costs climb while revenue reporting lags behind. Change orders need more than verbal agreement. They need clear estimates, proper documentation, and written approval before the first nail goes in.

6. Accepting Unreasonable Contract Terms

It’s hard to push back when a contract could land your firm its biggest project yet. But saying yes too quickly can lock you into terms that punish more than protect.

Penalties tied to delays, third-party issues, or even unpredictable weather can turn a promising job into a financial drain. Contractors need to treat contracts like the blueprint for risk. A legal review may feel like a formality, but it’s necessary to get it done.

If you’d like to see how HashMicro Construction Accounting Software can simplify your project planning, simply click the pricing scheme in the banner below.

Construction Accounting Best Practices

Since we have covered the basics in the previous sections, let’s move on to the best practices for construction accounting:

1. Prioritise Accurate Job Costing

For contractors, every project must be tracked individually. Accurate job costing lets businesses identify which projects are profitable and which are draining resources. This insight is vital for making timely decisions before profits are affected.

Effective costing begins with precise estimates, covering labour, materials, and overhead. In Malaysia, where contractors often manage multiple sites across states, tracking labour costs across a mobile workforce can be a major challenge.

Making job costing a shared priority across the organisation, supported by clear cost codes and internal training, helps improve accuracy.

2. Consider Cash Basis Accounting (for Smaller Firms)

For smaller construction businesses or subcontractors in Malaysia, cash basis accounting is often a practical approach. It’s easier to maintain and usually comes with lower bookkeeping costs.

More importantly, it offers a clear picture of your actual cash position, crucial for companies operating with tight cash flow.

Because income is only recorded when payment is received, you avoid paying tax on outstanding invoices. Similarly, recording expenses when they’re paid means you may be able to lower your tax bill by purchasing materials before the financial year ends.

3. Plan a Tax Strategy That Fits Your Business

Choosing the right tax approach is critical. Malaysian contractors often work with long-term or staggered projects, so methods like percentage-of-completion accounting can be useful. This is commonly used in large infrastructure or public-sector projects.

For contractors handling residential builds or smaller-scale developments, the completed contract method may be more beneficial. It allows revenue and expenses to be recorded only upon project completion, ideal for deferring taxable income to a later year.

Business structure also plays a role. Many Malaysian construction firms are set up as sole proprietorships or partnerships. These “pass-through” entities allow owners to offset business losses against personal income, potentially reducing personal tax liability.

4. Leverage Construction Accounting Software

Investing in construction-specific accounting software can transform financial operations. A good system automates job costing, tracks accounts payable and receivable, and generates real-time financial reports.

Importantly, the software should support flexible tax and revenue recognition methods, including those approved by Malaysia’s Lembaga Hasil Dalam Negeri (LHDN). Accurate records not only ease annual tax filing but also reduce the risk of penalties during audits.

Leverage Your Construction Accounting Practices with the Right Software

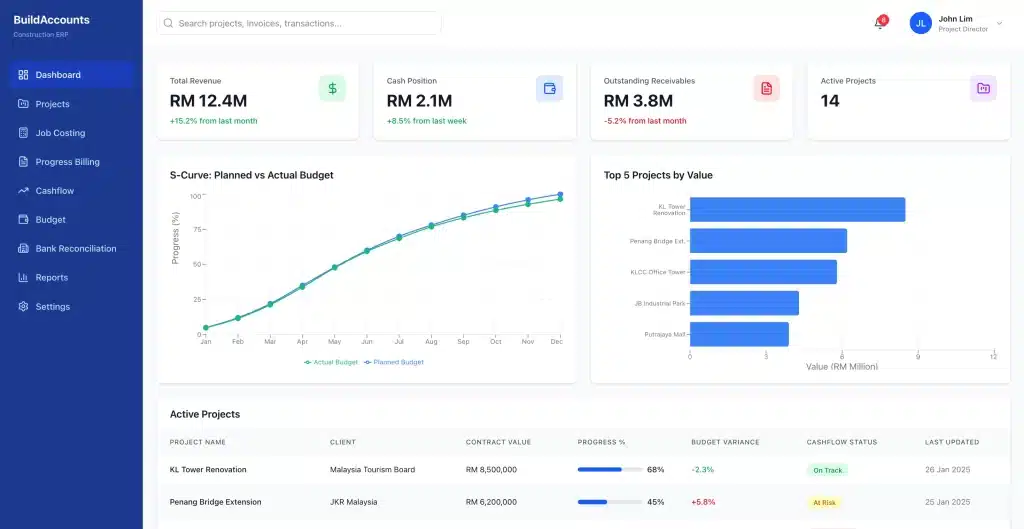

The features that matter most in construction accounting software are not the same as general accounting tools. Job costing, progress billing, multi-project tracking, and cashflow forecasting tied to project milestones are non-negotiable for firms managing multiple active sites.

The features that matter most in construction accounting software are not the same as general accounting tools. Job costing, progress billing, multi-project tracking, and cashflow forecasting tied to project milestones are non-negotiable for firms managing multiple active sites.

When evaluating options, consider these core capabilities:

- Cashflow visibility by project: Construction cash moves in stages, not steady streams. The system should show incoming and outgoing cash per project, not just company-wide totals, so finance teams can spot liquidity gaps before they become critical.

- Budget tracking with visual progress: An S-curve view of planned versus actual expenditure helps project managers see at a glance whether spending is on track or accelerating faster than progress.

- Variance reporting: Comparing actual costs against budgeted figures at the line item level reveals where overruns originate. Without this, deviations only surface at month end when correction options are limited.

- Forecast capability: Using historical project data to generate forward-looking budgets helps firms plan resources more accurately for upcoming phases or new tenders.

- Bank reconciliation: Automatic matching between internal records and bank statements reduces manual checking and catches discrepancies early.

Several providers serve the Malaysian market with construction-specific accounting features. HashMicro, for example, offers an integrated system with budget S-curve visualisation, forecast budgeting, and project-level financial reporting.

ISS, a multinational facility services company operating across multiple countries including Malaysia, adopted HashMicro’s accounting system to address the complexity of managing finances across diverse service contracts and locations. The integration allowed their finance team to consolidate reporting, automate reconciliation processes, and gain clearer visibility into cost performance across different business units.

HashMicro’s construction accounting module offers these capabilities within a broader ERP ecosystem, meaning project finances can connect directly with procurement, inventory, and operational data. For firms that need accounting to work alongside other business functions rather than in isolation, this integration reduces manual data transfer and the errors that come with it.

Before committing to any system, request a demo using your actual project data, not generic samples. Test how it handles progress claims, retention accounting, and variation orders. These are where general accounting tools typically fall short.

Our guide to the best construction accounting solutions in Malaysia for 2026 highlights reliable options designed to handle job costing, progress billing, and multi-entity reporting.

Conclusion

Construction accounting operates under different rules. Costs are tied to projects, not departments. Revenue follows physical progress, not invoice dates. Cashflow depends on retention clauses and payment certifications that general accounting tools were never designed to handle.

For firms managing multiple sites or contracts, the real challenge is not just tracking numbers but connecting them. Material costs need to link with procurement. Budget variances need to surface before they compound into losses. Finance cannot operate in a silo when every decision affects project margins.

A system that integrates accounting with procurement, assets, and project tracking within one platform removes the manual workarounds that slow teams down. If your current setup struggles with project-level financials, book a free demo to see how a specialised solution compares.

FAQ on Construction Accounting

-

What is retention (retainage) in construction accounting?

Retention (or retainage) is a percentage of payment—typically 5–10%—held back by clients until the project or specific milestones are fully completed. It’s a safeguard to ensure contractors and subcontractors meet contractual obligations before receiving full payment.

-

What are soft costs in construction accounting?

Soft costs refer to indirect expenses not directly tied to physical construction—such as architectural fees, engineering, financing, permits, insurance, general administration, and legal fees. These are classified separately from “hard” labor and material costs.

-

What is notional profit and why is it used?

Notional profit is an estimated profit calculated by subtracting incurred costs from Work-in-Progress (WIP). It helps smooth out profit reporting across long-term construction projects by recognizing earnings proportionally as work progresses.

-

What are the best accounting software for construction companies?

The best construction accounting software are those that combine job costing, progress billing, revenue recognition, and project-based financial reporting in one place. In Malaysia, many contractors prefer systems that support both cash and accrual methods, multi-project tracking, and LHDN-compliant tax treatments. HashMicro is one of the recommended options because it offers construction-specific automation, real-time cost monitoring, and integrated project accounting that helps contractors maintain accurate financial visibility across all sites.