Navigating the complexities of tax regulations can be daunting, but a proactive approach using accounting software to manage your deductions can yield significant returns. By transforming this annual requirement into a year-round strategy, you can unlock capital, improve cash flow, and build a more resilient financial foundation for your company.

This article will serve as your comprehensive guide to understanding tax deductions from A to Z, covering everything from basic concepts and claimable expenses to financial management strategies that ensure it becomes a tool for business growth, not just an annual administrative chore.

Key Takeaways

|

What Is a Tax Deduction and Why Is It Crucial for Your Business?

Understanding the definition of a tax deduction is the first step toward using it as a strategic tool in your company’s finances. In simple terms, a tax deduction is an expense that can be subtracted from your company’s gross income, which ultimately reduces your taxable income.

It is important to remember that this reduction does not directly cut the amount of tax you owe; instead, it lowers the income base on which your taxes are calculated. With a lower taxable income, the amount of income tax the company must pay automatically decreases, directly impacting your bottom line.

Understanding the Main Types of Tax Deductions

Not all business expenditures are treated equally under tax regulations, making it essential to understand the primary categories of tax deductions. Here is a more detailed explanation of the most common types of tax reductions.

Not all business expenditures are treated equally under tax regulations, making it essential to understand the primary categories of tax deductions. Here is a more detailed explanation of the most common types of tax reductions.

1. Business operating expenses

This is the most common category of tax deductions and includes the costs you incur to run your day-to-day business operations. These expenses are considered ordinary and necessary for your industry, such as office rent, employee salaries, utility bills (electricity, water, and internet), and marketing costs.

2. Capital expenditures and depreciation

Unlike operating costs, capital expenditures are expenses for purchasing long-term assets with a useful life of more than one year, such as buildings, production machinery, vehicles, or office equipment.

According to the Internal Revenue Service (IRS), understanding depreciation rules is vital because it can provide significant tax benefits over many years, allowing you to recover the cost of substantial investments systematically.

3. Employee-related expenses

All costs associated with employee compensation and welfare are generally significant tax deductions for a company. This includes not only base salaries and wages but also the cost of benefits such as health insurance, pension funds, and training and development programs aimed at enhancing their skills.

For instance, a $2,000 tax credit will directly cut your tax bill by $2,000, regardless of your tax bracket. Understanding this fundamental difference will help you and your finance team prioritize which tax incentives are most beneficial for the company, often making tax credits a more sought-after form of tax relief.

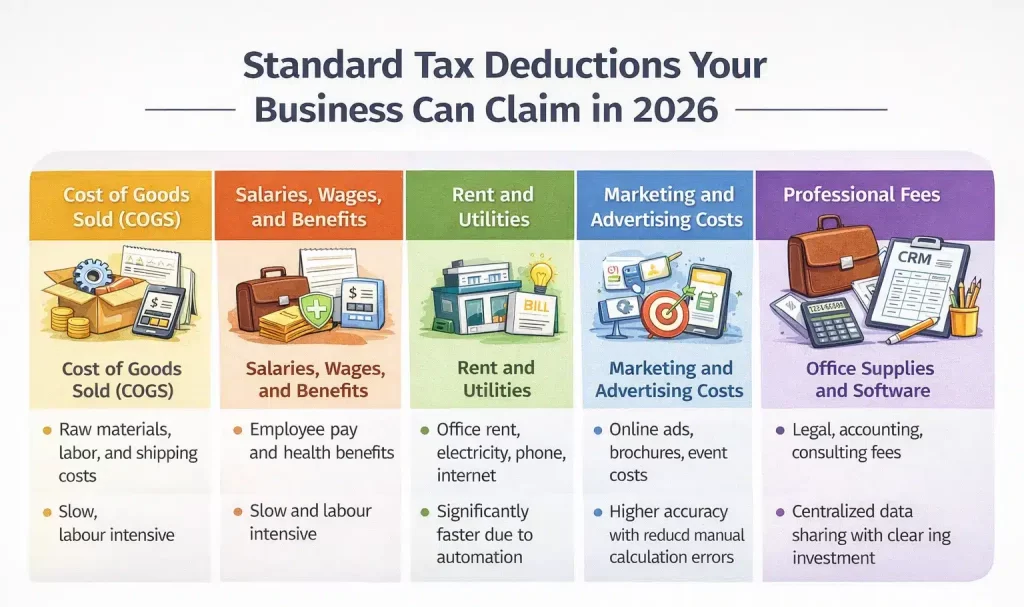

Standard Tax Deductions Your Business Can Claim in 2026

Although tax regulations can vary by jurisdiction, several categories of business expenses are almost universally claimable as tax deductions. Knowing this list will help you ensure no potential reduction is missed. Here are some of the most common tax deductions your business can leverage in 2026.

Although tax regulations can vary by jurisdiction, several categories of business expenses are almost universally claimable as tax deductions. Knowing this list will help you ensure no potential reduction is missed. Here are some of the most common tax deductions your business can leverage in 2026.

1. Cost of Goods Sold (COGS)

For businesses that sell products, the Cost of Goods Sold (COGS) is one of the largest deductions. It includes all direct costs associated with producing or acquiring the goods you sell, such as the cost of raw materials, direct labor, and shipping costs to obtain those materials.

2. Salaries, wages, and benefits

Salaries, wages, bonuses, and commissions you pay to employees are fully deductible expenses. Additionally, costs for employee benefits, such as the company’s contribution to health insurance, pension programs, educational assistance, and perks like free lunches, are included in this category.

3. Rent and utilities

The cost of renting office space, a warehouse, or your retail facility is a clear-cut deduction. The same applies to utility costs necessary to operate at these locations, including electricity, gas, water, telephone services, and internet.

4. Marketing and advertising costs

All expenses you incur to promote your business are generally deductible. This covers a wide range of costs, from digital advertising on social media and Google to the cost of printing brochures and promotional materials, to expenses for hosting product launch events.

5. Professional fees (legal and accounting)

The fees you pay for professional services from accountants, lawyers, or business consultants can be deducted from your taxes. These expenses are considered necessary to ensure your business operates legally, manages its finances correctly, and receives strategic advice.

6. Office supplies and software

Expenditures for everyday office supplies such as paper, pens, printer ink, and other consumables are fully deductible. Furthermore, the cost of software used in your business, whether it is a one-time license or a monthly subscription for accounting software, CRM, or project management tools, also falls into the category of a valid tax deduction.

The Process of Claiming Tax Deductions: A Step-by-Step Guide

Once you understand the types of tax deductions and the strategies to maximise them, the next step is to understand the practical process of claiming them. This process may seem complicated, but with a systematic and organised approach, you can navigate it with greater confidence. Here is a step-by-step guide to the tax deduction claim process.

| Step | What You Need to Do |

|---|---|

| 1 | Gather all financial documents Collect bank statements, business credit card reports, sales and purchase invoices, expense receipts, and payroll records accumulated throughout the year. |

| 2 | Categorise expenses correctly Review each transaction and assign it to the correct expense category such as rent, salaries, marketing, or utilities to avoid misclassification. |

| 3 | Calculate the total deductible amount Sum expenses per category and calculate the total deductions. Accounting software can automate this step by generating an income statement for the tax period. |

| 4 | Fill out the appropriate tax forms Enter the calculated deductions into the corporate income tax return forms required in your jurisdiction, following specific instructions carefully. |

| 5 | Keep records for audit purposes Store all supporting documents and financial records for several years in line with applicable tax regulations and audit requirements. |

How to Maximise Tax Deductions with Smart Financial Management

Knowing what qualifies as a tax deduction is only half the battle; the more strategic part is how to maximise it through innovative and proactive financial management. This is not about finding legal loopholes but about building a system that ensures every legitimate expense is recorded and claimed correctly.

Here are some practical strategies you can implement.

1. Implement meticulous record-keeping

This is the foundation of everything, because without careful records, you will inevitably miss out on many potential deductions. Make it a habit to save all proof of transactions, whether it is invoices from suppliers, receipts for office supply purchases, or records of business travel.

2. Plan major purchases strategically

The timing of large asset purchases can have a significant impact on your tax liability for a particular year. For example, if you plan to buy new machinery or upgrade your computer systems, doing so before the end of the tax year can provide you with a depreciation deduction for that year.

3. Review your financial statements regularly

Your financial statements, such as the income statement and balance sheet, are the roadmaps that show your company’s financial health. By reviewing them regularly, at least monthly, you can identify spending trends and discover potential deductions that might have been overlooked.

4. Leverage technology for accurate tracking

Relying on manual record-keeping or simple spreadsheets is highly prone to human error and can be incredibly time-consuming. Adopting technology is the most effective step to ensure accuracy and efficiency in tracking deductible expenses.

Using an integrated system like an Accounting ERP can take tax deduction management to the next level. This software not only records expenses but also links them to other business modules, such as procurement, inventory, and sales.

Consequently, every cost arising from operational activities is automatically documented and categorised correctly, minimising the risk of any expenditure being missed. The resulting financial reports are much more accurate and ready for tax reporting purposes.

Modernising Accounting Operations Without Adding Complexity

A modern ERP system can make financial management less dependent on manual work and individual spreadsheets. When reporting is slow, data is spread across departments, and reconciliation takes days, tax tracking and decision making become reactive instead of planned.

An integrated accounting setup helps by connecting finance with inventory, purchasing, and sales, so your numbers reflect what is actually happening across the business. That means fewer duplicate entries, clearer visibility on cash position, and more reliable reporting for both internal planning and compliance needs.

Key capabilities to look for in an accounting and finance system:

- Bank Integration – Auto Reconciliation: Automatically matches bank transactions with internal bookkeeping records, drastically reducing manual reconciliation time and ensuring accuracy.

- AI-Generated Reports and Explainer: Utilises artificial intelligence to generate comprehensive financial reports with automated explanations, making complex data easier to understand for strategic decision-making.

- E-Faktur and DJP Integration: Streamlines tax compliance by integrating directly with the Directorate General of Taxes (DJP), automating the creation and submission of e-Faktur for Indonesian businesses.

- Multi-Level Analytical Reporting: Enables in-depth financial analysis by comparing statements across projects, branches, or business entities, providing granular insights into performance.

- Automated Cash Flow Reports: Generates real-time cash flow statements, offering a clear view of your company’s liquidity to help you manage funds and plan for future expenses effectively.

If you want to see what the investment could look like for your setup, you can use the banner to view pricing details or estimate a budget based on the modules you need.

Conclusion

A tax deduction is not just a year end task. When you manage it consistently, it becomes a practical way to protect cash flow and keep more budget available for growth.

If your process is still manual, the harder part is not the calculation. It is keeping records clean, categorising expenses correctly, and producing reports fast when you need them. This is where an accounting system can help by automating documentation, simplifying reporting, and giving you clearer visibility into spending.

Try our free demo to see how you can ensure that no deduction is missed, and your team can focus on what is most important: growing the business. This shift from administrative burden to strategic advantage is the true power of effective tax management.

FAQ About Tax Deduction

-

What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, and the value of the savings depends on your tax bracket. In contrast, a tax credit directly reduces your tax bill on a dollar-for-dollar basis, making it more valuable.

-

Can I deduct home office expenses in 2026?

Yes, you can deduct home office expenses if you use a part of your home exclusively and regularly for business. The deduction can be based on the actual costs or a simplified rate, but documentation is key to proving eligibility.

-

What are the most commonly missed tax deductions for small businesses?

Many small businesses overlook deductions for bank fees, software subscriptions, professional development courses, and mileage for business-related travel. Meticulous record-keeping is essential to capture all these eligible expenses.